- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Smart Shoe Market Size, Share & Forecast 2034 | CAGR 13.5%

Global Smart Shoe Market Size, Share, Analysis By Product Type (Smart Running Shoes, Smart Walking Shoes, Smart Sports Shoes), By Application (Fitness Tracking, Sports Performance, Healthcare & Rehabilitation), By Technology (Sensor-Based, Bluetooth-Enabled, AI-Powered), By Distribution Channel (Online Retail, Specialty Stores, Sports Retail), By End-User (Men, Women, Children) Industry Region & Key Players – Segment Overview, Dynamics, Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

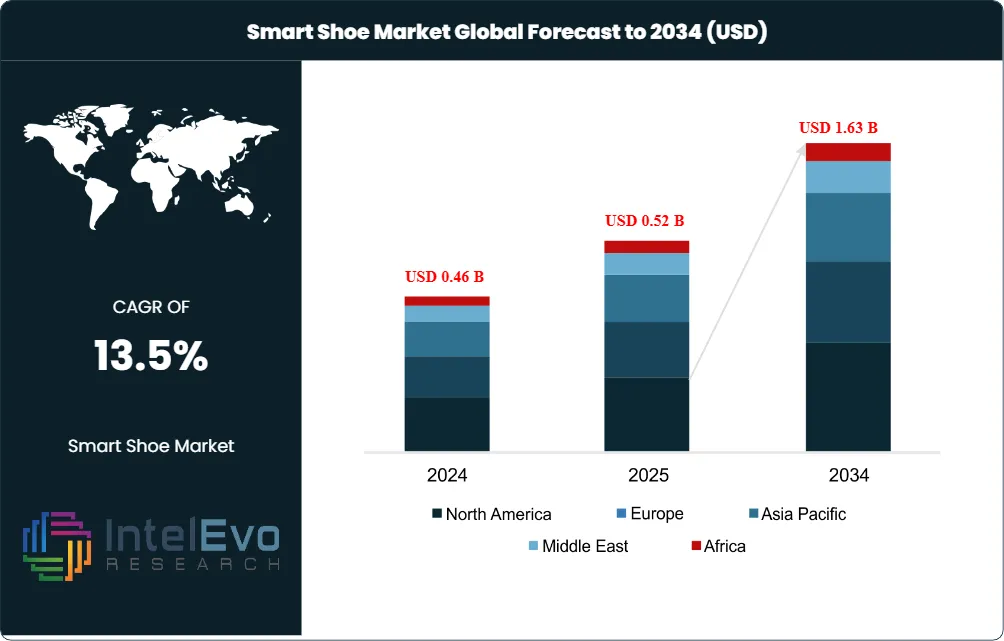

| USD 0.52 Billion | USD 1.63 Billion | 13.5% | North America, 40.6% |

The Smart Shoe Market was valued at USD 0.46 Billion in 2024 and USD 0.52 Billion in 2025. The market is projected to reach USD 1.63 Billion by 2034, expanding at a CAGR of 13.5% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 1.11 Billion over the analysis period.

Get More Information about this report -

Request Free Sample ReportThe smart shoe market sits between performance footwear, wearable electronics, and digital health. Demand is moving from step counting toward pressure mapping, gait analytics, self-adjusting fit, fall-risk monitoring, and running-shoe lifecycle tracking. Nike, adidas, Under Armour, Digitsole, Sensoria, ORPHE, Lechal, Salted, and FeetMe compete through different product routes, ranging from embedded shoe electronics to smart insoles and app-connected biomechanical platforms.

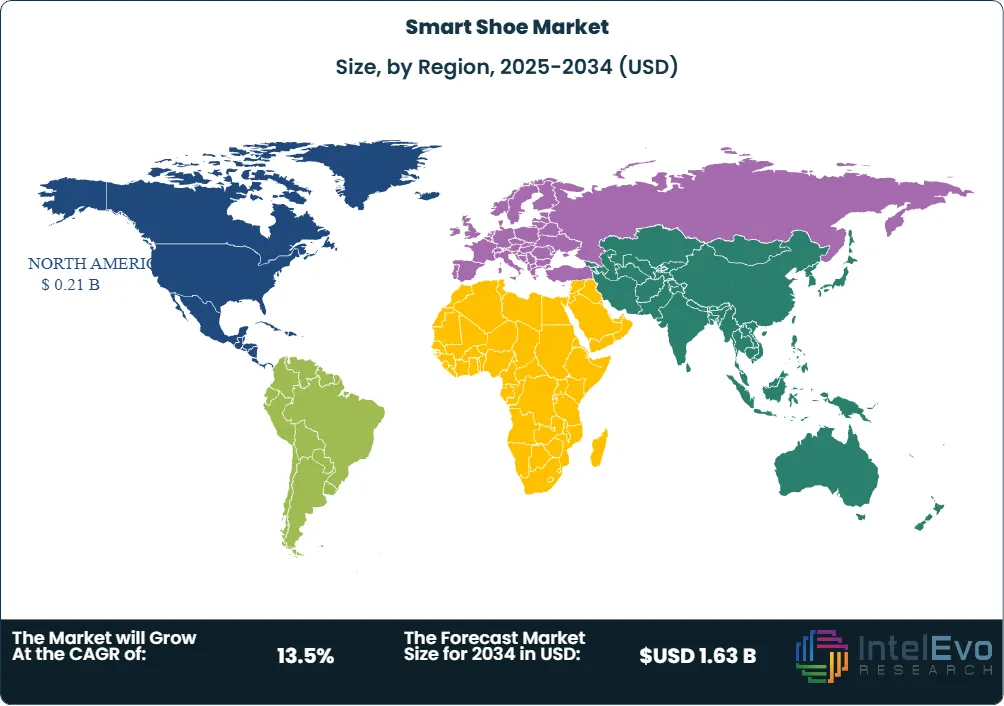

The base-year estimate reconciles multiple published 2025 market-size ranges, which cluster between approximately USD 0.41 Billion and USD 0.64 Billion for smart shoes and connected footwear. The adopted midpoint of USD 0.52 Billion reflects higher penetration in athletic running products than in clinical footwear, while excluding the broader smart insole market where estimates are much larger. North America accounted for 40.6% of 2025 revenue, equal to USD 0.21 Billion, because premium sports footwear, digital health reimbursement channels, and early consumer-wearable adoption are concentrated in the United States and Canada.

Regulation shapes the smart shoe market through intended-use boundaries. Fitness shoes that track distance, cadence, or shoe wear usually operate as low-risk wellness devices, while products claiming to detect diabetic foot ulcers, Parkinsonian gait, fall risk, or post-stroke mobility enter FDA digital health, EU Medical Device Regulation, and data-privacy review. This distinction creates a two-track market: consumer brands scale through retail distribution, while healthcare-oriented vendors build slower but higher-margin clinical sales channels.

Technology momentum accelerated in late 2025 and early 2026. Nike introduced Project Amplify in October 2025 as a powered footwear system for running and walking, and Nike Mind 001 and Mind 002 extended underfoot sensory stimulation into performance preparation. ORPHE INSOLE earned a CES 2026 Innovation Award with six pressure sensors, a 6-axis motion unit, wireless charging, and more than 24 hours of operation. Decathlon Kiprun disclosed the Kipnext Connect in April 2026 with Movmenta sensor technology for midsole-compression tracking ahead of a planned late-2026 launch.

The smart shoe market outlook through 2034 is strongest where sensor data changes a purchase or care decision. Running buyers will pay for injury prevention and shoe-replacement guidance when battery-free sensors reduce maintenance friction. Health systems will adopt connected insoles when pressure alerts lower ulcer risk or gait reports support rehabilitation documentation. By 2034, the category should remain smaller than smartwatches, but it will command premium pricing because the foot supplies motion and pressure data that wrist devices cannot capture.

Market Definition & Scope

The smart shoe market is defined as the global commercial activity surrounding footwear, insoles, embedded sensors, connectivity modules, software, and data services that collect or act on foot-based motion, pressure, location, fit, or health data. The market encompasses sensor-integrated athletic shoes, smart insoles, haptic-navigation shoes, self-lacing footwear, powered footwear systems, gait-analysis platforms, and connected diabetic-foot or rehabilitation products.

This analysis includes retail smart shoes, app-connected performance footwear, medical-grade smart insoles, sensor kits embedded by footwear manufacturers, and subscription analytics tied to gait or pressure data. It excludes standard running shoes without electronics, ordinary orthotic insoles, smart socks sold without footwear or insole hardware, and broad wearable devices such as smartwatches, smart rings, and AR glasses. The smart shoe market is a niche sub-segment of the global wearable electronics and athletic footwear markets, but it captures differentiated data from plantar pressure, stride mechanics, and foot-ground interaction.

, By Application (Fitness Tracking, Sports Performance, Healthcare & Rehabilitation), By Technology (Sensor-Based, Bluetooth-Enabled, AI-Powered), By Distribution Channel (Online Retail, Specialty Stores, Sports Retail), By End-User (Men, Women, Children) Industry Region & Key Players – Segment Overview, Dynamics, Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The smart shoe market increased to USD 0.52 Billion in 2025 and is projected to reach USD 1.63 Billion by 2034 at a 13.5% CAGR, adding USD 1.11 Billion in absolute dollar opportunity.

- Segment Dominance: Fitness and sports smart shoes held 46.8% of 2025 revenue, equal to USD 0.24 Billion, because running, basketball, golf, and training buyers pay for measurable performance feedback.

- Segment Dominance: Step tracking and performance analytics led application demand with 39.4% share in 2025, ahead of medical monitoring at 27.6% and navigation or assistive functions at 18.8%.

- Driver: Health and fitness wearables shipped in tens of millions of units quarterly during 2025, creating consumer familiarity with app-connected metrics and reducing adoption friction for footwear-based tracking.

- Restraint: High component cost remains the main barrier; premium smart shoes commonly add USD 40 to USD 180 above comparable conventional footwear, while clinical insoles can exceed USD 300 per pair.

- Opportunity: Medical monitoring and rehabilitation represent a USD 0.45 Billion revenue opportunity by 2034 as diabetic-foot surveillance, fall-risk assessment, and remote gait testing move into home-care programs.

- Trend: Battery-light designs are gaining share because ORPHE, Movmenta, and research-grade self-powered insoles show buyers prefer passive or wireless-charging electronics over shoes that require frequent charging.

- Regional: North America led the smart shoe market with 40.6% share in 2025, equal to USD 0.21 Billion, followed by Europe at 25.8% and Asia Pacific at 24.1%.

Key Insights Summary

- ORPHE INSOLE integrates six pressure sensors and a 6-axis motion unit, with wireless charging and more than 24 hours of continuous operation, setting a 2026 benchmark for compact connected-insole design.

- Ohio State University researchers described a self-powered smart insole in April 2025 using 22 sensors and machine-learning classification for eight motion states, demonstrating a pathway toward battery-light gait monitoring.

- Nike Project Amplify underwent testing with more than 400 participants before its October 2025 public reveal, signaling that powered footwear has moved from concept work into structured user validation.

- Decathlon Kiprun and Movmenta disclosed Kipnext Connect in April 2026 with a battery-free sensor that measures heel-foam compression, converting shoe-wear uncertainty into an app-readable replacement metric.

- Under Armour reported fiscal 2025 footwear revenue representing 23% of USD 5.2 Billion in company net revenue, leaving a large addressable base for connected running-shoe relaunches if adoption economics improve.

- adidas reported 2025 net sales of EUR 24.811 Billion and 12% currency-neutral footwear revenue growth, giving the company commercial scale to test sensor-enabled running products without relying on niche channels.

- FDA digital health policy treats low-risk wellness functions differently from higher-risk medical-device claims, creating separate commercialization pathways for fitness smart shoes and clinical gait-analysis footwear.

Competitive Landscape Overview

The smart shoe market is fragmented by revenue but concentrated by brand visibility. Nike, adidas, Under Armour, and Xiaomi hold the broadest consumer reach, while Digitsole, Sensoria, ORPHE, FeetMe, Lechal, and Salted hold specialized intellectual property in gait analytics, haptic navigation, pressure sensing, and golf-swing feedback. The top four companies account for an estimated 42% of 2025 commercial activity when footwear scale, connected-product history, and distribution access are weighted together.

Competition is not only between shoe brands. It is between three architectures: fully embedded smart footwear, removable smart insoles, and powered or assistive footwear systems. Embedded shoes protect the user experience but raise recycling and repair complexity. Removable insoles lower replacement cost and can fit multiple shoe models. Powered footwear, led by Nike Project Amplify and Dephy-enabled robotics, targets a higher-price performance and mobility category that could sit above conventional smart shoes.

Competitive Landscape Matrix

| Company Name | Headquarters | Position | Key Product/Solution | Geographic Strength | Recent Strategic Move |

| Nike, Inc. | United States | Leader | Project Amplify, Nike Mind, Adapt heritage | North America, Europe, China | Revealed Project Amplify and Nike Mind footwear platforms in October 2025 |

| adidas AG | Germany | Leader | Performance running footwear, sensor-ready digital programs | Europe, North America, China | Reported 12% currency-neutral footwear growth in 2025 and renewed running focus |

| Under Armour, Inc. | United States | Challenger | HOVR connected footwear heritage, MapMyRun ecosystem | North America, EMEA | Reported fiscal 2025 footwear revenue at 23% of company net revenue |

| Xiaomi Corporation | China | Challenger | Mi smart shoes and connected fitness devices | China, India, Southeast Asia | Expanded wearables base through 2025, supporting connected-footwear adjacency |

| Digitsole SAS | France | Niche Player | Digitsole Pro, smart insoles, thermal and gait features | Europe, North America | Maintained B2B smart-insole positioning for health and workplace use |

| ORPHE Inc. | Japan | Niche Player | ORPHE INSOLE, ORPHE CORE | Japan, United States | Earned CES 2026 Innovation Award recognition for ORPHE INSOLE |

| Sensoria Inc. | United States | Niche Player | Sensoria Core, smart socks, gait software | United States, Europe | Extended remote patient monitoring use cases through Sensoria Health programs |

| FeetMe SAS | France | Niche Player | FeetMe connected insoles and gait analytics | Europe, clinical channels | Published 2025 validation research comparing insoles with motion-capture systems |

| Lechal / Ducere Technologies | India | Niche Player | Haptic GPS shoes and insoles | India, global online | Continued haptic-navigation smart footwear for mobility and travel use |

| Salted Co., Ltd. | South Korea | Niche Player | IOFIT and Salted smart golf insoles | South Korea, United States | Targeted golf balance analytics and coaching applications through app-connected insoles |

Segmentation Analysis

The smart shoe market segments by product type, application, technology, distribution channel, and end-user, with revenue economics shaped by sensor cost, replacement cycles, app retention, and clinical-grade evidence.

By Product Type

The smart shoe market by product type is led by fitness and sports smart shoes, which captured 46.8% of 2025 revenue, equal to approximately USD 0.24 Billion. Nike, adidas, Under Armour, Puma, Salted, and ORPHE address this segment through running, basketball, training, and golf products that convert motion into coaching feedback. The segment wins because athletes already accept premium footwear replacement cycles of 300 to 500 miles, allowing electronics to be attached to performance value instead of treated as a separate gadget.

Smart insoles represented 31.7% of 2025 revenue, equal to USD 0.16 Billion. Digitsole, FeetMe, Sensoria, ORPHE, Lechal, and research-derived platforms use removable hardware to avoid the inventory burden of producing full shoe-size runs. Smart insoles are more attractive for clinics, rehabilitation centers, and eldercare programs because the same analytics layer can fit multiple footwear types. Their limitation is consumer attachment; a removable device must stay charged, positioned correctly, and comfortable over daily wear.

Self-lacing, powered, and assistive footwear accounted for 12.9% of 2025 revenue, while navigation and safety-oriented footwear represented 8.6%. Nike Adapt created the self-lacing reference point, but Nike Project Amplify moved the category toward movement assistance rather than fit convenience. Lechal remains relevant for haptic navigation, especially for runners and visually impaired users. Compared with smart insoles, powered footwear carries higher regulatory and product-liability exposure because motors and batteries affect movement mechanics.

By Application

Step tracking and performance analytics dominated the smart shoe market with 39.4% share in 2025, equivalent to USD 0.20 Billion. This application includes cadence, stride length, pace estimation, foot-strike analysis, jump metrics, balance analytics, and golf swing pressure mapping. Under Armour HOVR connected shoes, Sensoria gait software, Salted golf insoles, and ORPHE motion recognition address this use case. The category competes directly with smartwatches, but foot sensors measure impact, pronation, and plantar pressure that wrist sensors infer only indirectly.

Medical monitoring and rehabilitation held 27.6% share in 2025, equal to USD 0.14 Billion, and is projected to reach approximately USD 0.45 Billion by 2034. FeetMe, Digitsole, Sensoria Health, and academic spinout technologies target diabetic-foot risk, post-stroke gait monitoring, Parkinsonian gait, fall prevention, and musculoskeletal rehabilitation. The segment grows because aging populations and home-care programs need objective mobility data. It grows slower than fitness footwear because clinical claims require validation studies, risk management files, and regulated software controls.

Navigation, safety, and accessibility represented 18.8% of 2025 revenue, led by haptic guidance from Lechal and emergency-oriented products in India and other mobile-first markets. Fit automation and powered assistance accounted for the remaining 14.2%, anchored by Nike Adapt heritage and Project Amplify development. Fitness analytics scales faster today, but medical monitoring should narrow the gap by 2034 because a single avoided ulcer, fall, or rehabilitation readmission can justify higher device pricing.

By Technology

Pressure sensors and force-sensing resistor arrays led smart shoe market technology revenue with 38.5% share in 2025. ORPHE, FeetMe, Sensoria, Salted, and university prototypes use pressure mapping to capture load distribution, contact timing, and gait asymmetry. Inertial measurement units held 27.2% share and remain essential for cadence, acceleration, jump, and motion-state recognition. Bluetooth Low Energy and mobile-app connectivity accounted for 18.1%, while haptics, motors, and power electronics represented 16.2%.

Battery strategy is becoming a buying criterion. Shoes face sweat, impact, washing constraints, and end-of-life recycling problems that watches avoid. Wireless charging and more than 24-hour operation improve daily usability for ORPHE-style insoles. Battery-free or passive sensor designs, such as Movmenta's midsole-compression concept and self-powered research insoles, could reduce ownership friction. By 2034, vendors that combine low-maintenance power systems with privacy-preserving on-device analytics should gain share in healthcare and youth-sports settings.

By Distribution Channel

Online and brand-owned digital channels held 48.7% of 2025 revenue, equal to USD 0.25 Billion. Nike, adidas, Xiaomi, Digitsole, and Lechal can educate buyers through product pages, connected-app demos, and direct subscriptions that traditional shoe retailers struggle to explain. Specialty sports stores accounted for 28.4%, supported by running-store gait assessments and golf-fitting environments where pressure maps can influence immediate purchase decisions.

Clinical, orthotic, and institutional channels represented 15.6% of revenue, while mass retail and other channels accounted for 7.3%. Clinical channels have lower volume but better retention because device use is tied to therapy, fall-risk monitoring, or diabetic-foot care plans. Mass retail remains underpenetrated because mainstream consumers still compare smart shoes with ordinary footwear prices rather than with smartwatches or medical devices. A practical smart shoe procurement checklist now includes sensor accuracy, cleaning durability, app support life, data export, battery policy, and replacement economics.

By End-User

Individual fitness consumers accounted for 52.3% of smart shoe market revenue in 2025. This group includes runners, gym users, basketball players, golfers, and early adopters who want real-time feedback without laboratory gait testing. Healthcare providers, rehabilitation clinics, and eldercare organizations represented 22.1%, with patients and caregivers using connected footwear to monitor mobility outside the clinic. Sports teams, coaches, and training facilities held 14.6%, while industrial safety, defense, and accessibility users covered 11.0%.

The end-user mix will shift through 2034. Fitness consumers will keep the largest pool because replacement cycles are short and retail access is broad. Healthcare and eldercare should gain the highest CAGR because clinical gait data has monetary value in risk reduction and documentation. Sports teams will demand higher sampling rates and analytics exports, while industrial safety buyers will focus on fall alerts and fatigue detection. Smart shoe pricing benchmarks vary widely, from USD 100 to USD 250 for consumer connected shoes to more than USD 300 for clinical-grade insoles with reporting software.

Regional Analysis

The smart shoe market remains geographically concentrated in North America and Europe in 2025, while Asia Pacific provides the largest manufacturing base and the fastest adoption curve for lower-cost connected footwear.

North America led the smart shoe market with 40.6% share and USD 0.21 Billion in 2025 revenue. The United States contributes more than 88% of regional demand because Nike, Under Armour, Sensoria, and multiple rehabilitation-technology programs operate across U.S. retail and health channels. FDA digital health guidance supports wellness products that avoid diagnostic claims, but medical gait products must manage device software requirements. Nike Project Amplify, disclosed in October 2025 with Dephy collaboration, strengthened the region’s technology signal and shifted investor attention from passive tracking toward powered footwear assistance.

Europe held 25.8% of the smart shoe market in 2025, equal to USD 0.13 Billion. Germany, France, the United Kingdom, Italy, and the Netherlands anchor demand through running specialty retail, sports science institutes, and clinical rehabilitation centers. adidas, Puma, Digitsole, FeetMe, and several orthotics suppliers provide local capability. The EU Medical Device Regulation and GDPR create higher compliance costs than in pure consumer markets, but they also favor vendors with controlled data architecture and clinical documentation. Europe is particularly attractive for smart shoe vendors serving elderly mobility, post-stroke rehabilitation, and diabetic-foot monitoring.

Asia Pacific accounted for 24.1% share and USD 0.13 Billion in 2025 revenue, with China, Japan, South Korea, and India carrying most demand. Xiaomi, Li-Ning, ORPHE, Salted, and Lechal demonstrate that the region can produce both mass-market connected footwear and specialist smart-insole technology. Japan’s CES-recognized ORPHE INSOLE and South Korea’s golf-focused Salted platform show high-value niches, while India’s Lechal and newer connected footwear brands show mobile-first navigation and safety use cases. The region should record the fastest CAGR through 2034 because manufacturing cost, smartphone penetration, and youth fitness participation reinforce each other.

Latin America represented 5.9% share and USD 0.03 Billion in 2025 revenue. Brazil, Mexico, Chile, and Colombia lead adoption through running communities, private physiotherapy, and sports retail chains. Price sensitivity keeps demand focused on removable insoles and app-connected entry products rather than motorized systems. Vendors entering Latin America need Spanish and Portuguese app localization, durable battery policies, and distributors capable of post-sale support. The region’s upside is meaningful because conventional athletic footwear penetration is high, but smart-feature awareness remains low outside major cities.

Middle East and Africa held 3.6% share and USD 0.02 Billion in 2025 revenue. The United Arab Emirates, Saudi Arabia, Israel, and South Africa are the primary adoption centers. Gulf markets support premium running, wellness, and sports-tech purchases, while Israel provides health-tech and sensor-development capability. South Africa’s use case is more clinically oriented, with rehabilitation and diabetic-foot care shaping demand. Regional growth depends on import pricing, app-language support, and partnerships with hospitals, gyms, and sports clubs rather than broad mass-retail availability.

Country Analysis

The United States smart shoe market reached USD 0.19 Billion in 2025 and is projected to grow at a 12.9% country CAGR through 2034. Nike, Under Armour, Sensoria, FeetMe’s clinical research network, and Dephy-enabled robotics activity make the United States the category’s most influential commercialization base. FDA policy differentiates low-risk wellness apps from medical-device software, which helps consumer products scale while forcing clinical gait solutions to support claims with evidence. U.S. adoption is strongest in running, basketball, rehabilitation, diabetic-foot prevention, and eldercare mobility. Nike’s October 2025 Project Amplify reveal and 2026 FDA digital health updates gave domestic suppliers clearer direction on where fitness assistance ends and regulated medical claims begin.

China’s smart shoe market reached approximately USD 0.06 Billion in 2025 and is projected to grow at a 15.8% country CAGR through 2034. Xiaomi, Li-Ning, Anta-adjacent suppliers, and consumer electronics manufacturers can combine footwear with large connected-device user bases. China’s edge is cost control, sensor sourcing, and rapid product iteration through e-commerce. Demand is led by urban running, youth fitness, and app-enabled wellness rather than clinical-grade devices. Domestic vendors can undercut Western premium pricing, but export growth requires privacy controls, battery safety documentation, and software localization for Europe and North America.

Germany’s smart shoe market reached approximately USD 0.04 Billion in 2025 and is forecast to grow at a 12.4% country CAGR. adidas and Puma provide global sports-footwear influence, while German rehabilitation clinics and orthotic channels support medical smart-insole adoption. EU MDR and GDPR requirements increase documentation burdens, but German buyers value tested, durable devices with clear data processing. The country is a logical launch market for pressure-monitoring insoles, running-analysis shoes, and senior mobility programs because reimbursement-minded providers demand objective gait data rather than promotional fitness metrics.

Japan’s smart shoe market reached approximately USD 0.036 Billion in 2025 and is projected to grow at a 14.2% country CAGR. ORPHE, ASICS research activity, and Japan’s aging population create demand for compact, precise, and low-maintenance footwear electronics. ORPHE INSOLE’s CES 2026 recognition supports Japan’s position in thin sensor hardware and motion-recognition software. Healthcare use cases include fall risk, rehabilitation, and foot pressure analytics, while consumer demand is tied to running culture and high trust in compact wearable technology. Japan’s challenge is scaling globally beyond premium niches.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Product Type

- Smart Running Shoes

- Smart Walking Shoes

- Smart Sports Shoes

- Others

By Application

- Fitness Tracking

- Sports Performance

- Healthcare & Rehabilitation

- Others

By Technology

- Sensor-Based

- Bluetooth-Enabled

- AI-Powered

- Others

By Distribution Channel

- Online Retail

- Specialty Stores

- Sports Retail Stores

- Others

By End-User

- Men

- Women

- Children

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 0.52 B |

| Forecast Revenue (2034) | USD 1.63 B |

| CAGR (2025-2034) | 13.5% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product Type, (Smart Running Shoes, Smart Walking Shoes, Smart Sports Shoes, Others), By Application, (Fitness Tracking, Sports Performance, Healthcare & Rehabilitation, Others), By Technology, (Sensor-Based, Bluetooth-Enabled, AI-Powered, Others), By Distribution Channel, (Online Retail, Specialty Stores, Sports Retail Stores, Others), By End-User, (Men, Women, Children, Others), |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | NIKE, INC., ADIDAS AG, UNDER ARMOUR, INC., XIAOMI CORPORATION, DIGITSOLE SAS, ORPHE INC., SENSORIA INC., FEETME SAS, LECHAL / DUCERE TECHNOLOGIES PVT. LTD., SALTED CO., LTD., PUMA SE, ASICS CORPORATION, LI-NING COMPANY LIMITED, 361 DEGREES INTERNATIONAL LIMITED, BATA INDIA LIMITED, VIVOBAREFOOT LIMITED, SOLEPOWERTECH, IEE S.A., OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Fitness Tracking, Sports Performance, Healthcare & Rehabilitation), By Technology (Sensor-Based, Bluetooth-Enabled, AI-Powered), By Distribution Channel (Online Retail, Specialty Stores, Sports Retail), By End-User (Men, Women, Children) Industry Region & Key Players – Segment Overview, Dynamics, Trends & Forecast 2026-2034")

, By Application (Fitness Tracking, Sports Performance, Healthcare & Rehabilitation), By Technology (Sensor-Based, Bluetooth-Enabled, AI-Powered), By Distribution Channel (Online Retail, Specialty Stores, Sports Retail), By End-User (Men, Women, Children) Industry Region & Key Players – Segment Overview, Dynamics, Trends & Forecast 2026-2034")

, By Application (Fitness Tracking, Sports Performance, Healthcare & Rehabilitation), By Technology (Sensor-Based, Bluetooth-Enabled, AI-Powered), By Distribution Channel (Online Retail, Specialty Stores, Sports Retail), By End-User (Men, Women, Children) Industry Region & Key Players – Segment Overview, Dynamics, Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Smart Shoe Market?

Smart Shoe MarketThe Global Smart Shoe Market was valued at USD 0.46 Billion in 2024 and USD 0.52 Billion in 2025, and is projected to reach USD 1.63 Billion by 2034, growing at a CAGR of 13.5% from 2026 to 2034. Market growth is driven by AI-powered footwear, wearable fitness technology, and IoT-enabled smart shoes.

Who are the major players in the Smart Shoe Market?

NIKE, INC., ADIDAS AG, UNDER ARMOUR, INC., XIAOMI CORPORATION, DIGITSOLE SAS, ORPHE INC., SENSORIA INC., FEETME SAS, LECHAL / DUCERE TECHNOLOGIES PVT. LTD., SALTED CO., LTD., PUMA SE, ASICS CORPORATION, LI-NING COMPANY LIMITED, 361 DEGREES INTERNATIONAL LIMITED, BATA INDIA LIMITED, VIVOBAREFOOT LIMITED, SOLEPOWERTECH, IEE S.A., OTHERS

Which segments covered the Smart Shoe Market?

By Product Type, (Smart Running Shoes, Smart Walking Shoes, Smart Sports Shoes, Others), By Application, (Fitness Tracking, Sports Performance, Healthcare & Rehabilitation, Others), By Technology, (Sensor-Based, Bluetooth-Enabled, AI-Powered, Others), By Distribution Channel, (Online Retail, Specialty Stores, Sports Retail Stores, Others), By End-User, (Men, Women, Children, Others),

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date