- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Software Protection Dongle Market Size | Growth, Trends, CAGR 9.3%

Global Software Protection Dongle Market Size, Share & Industry Analysis By Type (USB Dongles, Parallel Port Dongles, Network Dongles), By Application (Engineering & CAD Software, Industrial Automation, Healthcare IT, Media & Entertainment, Professional & Enterprise Software), By End User (SMEs, Large Enterprises, Government & Defense), By Security Level (Standard, Advanced Encryption, Cloud-Integrated Licensing), Regional Outlook, Competitive Landscape, Market Dynamics, Emerging Trends & Forecast 2025–2034

Report Overview

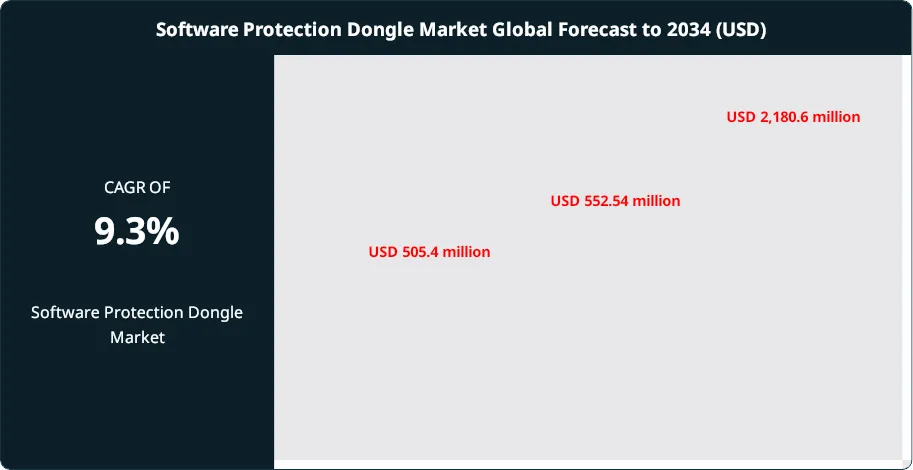

The Software Protection Dongle Market is estimated at USD 505.4 million in 2024 and is projected to reach approximately USD 2,180.6 million by 2034, registering a compound annual growth rate (CAGR) of 9.3% over 2025–2034. This robust expansion is driven by the rising need to combat software piracy, license misuse, and unauthorized access across engineering, industrial automation, healthcare, and professional software applications. Increasing adoption of hardware-based security solutions, combined with the growth of high-value proprietary software and subscription licensing models, is reinforcing demand for secure dongle-based protection. Additionally, integration of encryption, cloud authentication, and IoT-enabled license management is positioning software protection dongles as a critical component of modern digital rights management strategies, supporting sustained market momentum over the forecast period.

Get More Information about this report -

Request Free Sample ReportThis steady expansion reflects the rising importance of hardware-based security solutions in safeguarding intellectual property and preventing unauthorized software use. Historically, the market has grown in line with increasing concerns over piracy and compliance requirements, with demand accelerating in recent years as enterprises prioritize stronger access controls and licensing enforcement. The forecast trajectory indicates consistent double-digit growth in several regional segments, supported by both regulatory mandates and enterprise adoption of secure licensing models.

Growth is driven by multiple demand-side and supply-side factors. On the demand side, enterprises across industries are investing in dongle-based protection to secure proprietary applications, particularly in sectors such as engineering, design, and healthcare where software misuse can result in significant financial or compliance risks. On the supply side, vendors are expanding product portfolios with multi-factor authentication, cloud integration, and remote license management features, which enhance the utility of dongles beyond simple access control. Challenges remain, including the risk of physical loss or damage to devices, integration costs for large-scale deployments, and competition from software-only protection models. However, the resilience of hardware-based solutions continues to support their adoption, particularly where regulatory compliance and high-value intellectual property are at stake.

Technological advances are reshaping the market. Vendors are embedding encryption algorithms, secure key storage, and AI-driven monitoring into dongle solutions, enabling real-time detection of unauthorized access attempts. Integration with cloud-based license management platforms is also gaining traction, allowing enterprises to balance physical security with digital flexibility. These developments are expected to expand adoption in both established and emerging markets.

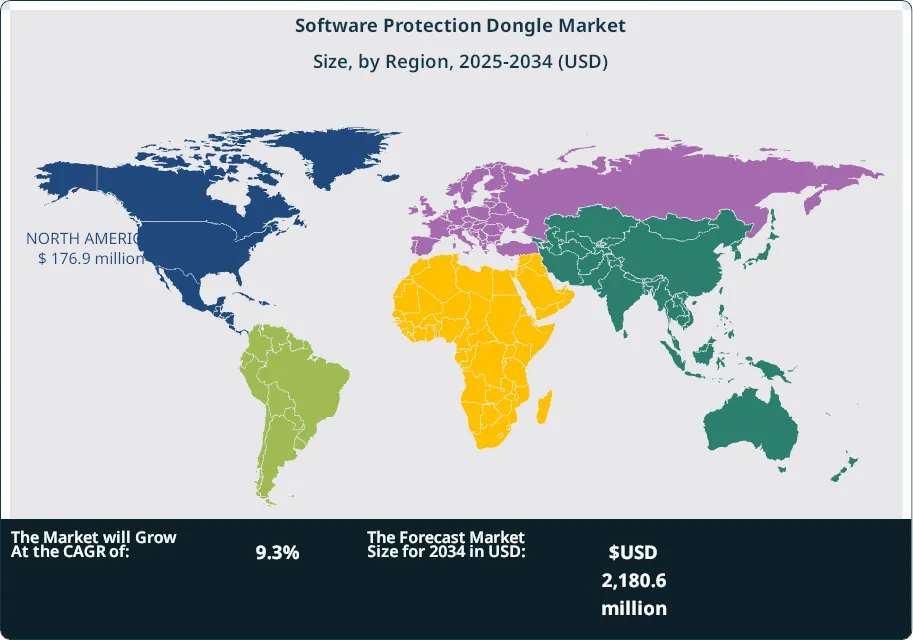

Regionally, North America accounted for 35.2% of global revenue in 2024, valued at USD 171.1 million, with the United States alone contributing USD 155.7 million. Europe remains a significant market, supported by stringent intellectual property regulations and strong demand from industrial software providers. Asia-Pacific is emerging as a key growth hub, driven by rapid digitalization, rising software development activity, and increasing enforcement of anti-piracy measures in markets such as China and India. For investors, opportunities lie in regions where regulatory frameworks are tightening and enterprise software adoption is accelerating, positioning the market for sustained expansion through 2034.

, By Application (Engineering & CAD Software, Industrial Automation, Healthcare IT, Media & Entertainment, Professional & Enterprise Software), By End User (SMEs, Large Enterprises, Government & Defense), By Security Level (Standard, Advanced Encryption, Cloud-Integrated Licensing), Regional Outlook, Competitive Landscape, Market Dynamics, Emerging Trends & Forecast 2025–2034")

Key Takeaways

- Market Growth: The global software protection dongle market will expand from USD 505.4 million in 2024 to USD 2,180.6 million by 2034, reflecting a CAGR of 9.3%. Growth is supported by rising concerns over software piracy and the need for secure licensing models across industries.

- Product Type: USB dongles account for 72.15% of total revenue in 2024, driven by their ease of deployment and compatibility with enterprise software environments. Their dominance is expected to continue as vendors integrate encryption and remote license management features.

- Application: Enterprise software represents 41.3% of market share, underscoring the critical role of dongles in protecting high-value applications used in engineering, design, and healthcare. This segment will remain a key revenue contributor through 2034.

- Organization Size: Large enterprises generate 58.48% of demand, reflecting their higher exposure to intellectual property risks and compliance requirements. Smaller firms are adopting dongles at a slower pace due to cost and integration barriers.

- Industry Vertical: IT and telecom leads with 49.3% share, as software vendors and service providers rely heavily on dongles to safeguard proprietary platforms and prevent unauthorized distribution.

- Driver: Rising global software piracy, estimated to cost the industry over USD 46 billion annually, is a primary driver of dongle adoption. Enterprises are investing in hardware-based protection to mitigate financial and compliance risks.

- Restraint: Physical dependency on dongles creates operational risks. Loss, theft, or hardware failure can disrupt access to mission-critical applications, limiting adoption in highly mobile or cloud-centric environments.

- Opportunity: Asia-Pacific presents the strongest growth potential, with double-digit CAGR expected through 2034. Expanding software development ecosystems in China and India, combined with stricter enforcement of intellectual property laws, will accelerate adoption.

- Trend: Vendors are integrating dongles with cloud-based license management and AI-driven monitoring. This hybrid approach enables enterprises to combine physical security with digital flexibility, enhancing long-term adoption prospects.

- Regional Analysis: North America leads with 35.2% share in 2024, valued at USD 171.1 million, supported by strong U.S. demand at USD 155.7 million. Europe follows with robust adoption in industrial software, while Asia-Pacific is emerging as the fastest-growing region, offering significant investment opportunities.

Type Analysis

As of 2025, USB dongles remain the dominant product category in the global software protection dongle market, accounting for more than 72% of total revenue. Their widespread use is supported by compatibility with standard computing devices and ease of deployment, making them the preferred choice for enterprises seeking reliable licensing enforcement. The segment continues to expand as organizations prioritize hardware-based protection to safeguard intellectual property against piracy and unauthorized access.

USB dongles are valued for their plug-and-play functionality, low integration costs, and ability to store encrypted licensing keys securely. These features have driven adoption across IT and telecom, gaming, and engineering software providers, where safeguarding proprietary applications is critical. Parallel port dongles and other formats retain niche roles, primarily in legacy systems, but their market share is shrinking as enterprises transition to USB-based solutions.

Looking ahead, USB dongles are expected to maintain their lead as vendors integrate advanced encryption, cloud connectivity, and remote license management capabilities. This evolution positions the segment to support both offline and hybrid software environments, ensuring continued relevance through 2034.

Application Analysis

Enterprise software continues to represent the largest application segment, holding more than 41% of global market share in 2025. The segment’s dominance reflects the high value of applications such as enterprise resource planning (ERP), customer relationship management (CRM), and engineering design tools, which require robust protection against piracy and misuse.

The shift toward subscription-based licensing models has further increased reliance on dongles, as enterprises seek mechanisms to enforce compliance in real time. Hardware-based protection ensures uninterrupted access to mission-critical applications while reducing financial and reputational risks associated with unauthorized use.

Media and entertainment, healthcare, and education are also expanding application areas. In particular, the media sector faces rising piracy risks, while healthcare providers adopt dongles to secure diagnostic and imaging software. These segments are expected to post above-average growth rates, though enterprise software will remain the primary revenue driver through the forecast period.

Organization Size Analysis

Large enterprises account for nearly 59% of global demand in 2025, reflecting their reliance on high-value software assets and complex IT infrastructures. These organizations deploy dongles to secure ERP platforms, advanced design tools, and proprietary applications that are central to operations across multiple geographies.

The segment’s leadership is reinforced by larger budgets and the ability to integrate hardware-based protection at scale. With global operations and distributed teams, large enterprises require consistent enforcement of licensing agreements across regions, a need effectively addressed by dongle-based solutions.

Small and medium-sized enterprises (SMEs) are gradually increasing adoption, particularly in markets with rising software piracy rates. However, cost sensitivity and limited IT resources remain barriers, keeping their share below that of large enterprises. Over the next decade, SME adoption is expected to accelerate as vendors introduce lower-cost, cloud-integrated dongle solutions.

Industry Vertical Analysis

The IT and telecom sector leads the market with a share of nearly 49% in 2025. The industry’s dependence on proprietary software for network management, cybersecurity, and communications infrastructure makes protection a top priority. The rollout of 5G networks and expansion of IoT ecosystems further amplify the need for secure licensing mechanisms.

BFSI and healthcare are emerging as high-growth verticals. Financial institutions are adopting dongles to secure trading platforms and compliance software, while healthcare providers rely on them to protect imaging and diagnostic applications. Manufacturing also represents a growing segment, as industrial software becomes increasingly digitized and exposed to piracy risks.

The IT and telecom segment will remain the largest contributor, but diversification across BFSI, healthcare, and manufacturing indicates a broadening market base. This trend underscores the expanding role of dongles in safeguarding intellectual property across multiple industries.

Regional Analysis

North America continues to lead the global market in 2025, accounting for more than 35% of total revenue, or approximately USD 180 million. The United States remains the largest contributor, supported by a mature enterprise software ecosystem and stringent intellectual property regulations. High adoption across IT, financial services, and healthcare reinforces the region’s leadership.

Europe follows closely, with strong demand from industrial software providers and compliance-driven adoption in markets such as Germany and the United Kingdom. The region’s emphasis on data privacy and regulatory enforcement supports steady growth.

Asia Pacific is emerging as the fastest-growing region, with double-digit CAGR projected through 2034. Rising software development activity in China and India, combined with stricter enforcement of anti-piracy laws, is driving adoption. Latin America and the Middle East & Africa remain smaller markets but present long-term opportunities as digital transformation accelerates and enterprises seek cost-effective protection solutions.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Type

- USB Dongles

- Parallel Port Dongles

- Others

By Application

- Enterprise Software

- Media & Entertainment

- Healthcare

- Education

- Others

By Organization Size

- Large Enterprises

- SMEs

By Industry Vertical

- IT & Telecom

- BFSI

- Healthcare

- Manufacturing

- Others

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2024) | USD 505.4 million |

| Forecast Revenue (2034) | USD 2,180.6 million |

| CAGR (2024-2034) | 9.3% |

| Historical data | 2020-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Type, (USB Dongles, Parallel Port Dongles, Others), By Application, (Enterprise Software, Media & Entertainment, Healthcare, Education, Others), By Organization Size, (Large Enterprises, SMEs), By Industry Vertical, (IT & Telecom, BFSI, Healthcare, Manufacturing, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Feitian Technologies Co., Ltd., Wibu-Systems AG, Donglify Ltd., Thales Group, SecuTech Solution, Inc., Microcosm Ltd., Keylok, Inc., Marx CryptoTech LP, Electronic Team, Inc., Other Major Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Engineering & CAD Software, Industrial Automation, Healthcare IT, Media & Entertainment, Professional & Enterprise Software), By End User (SMEs, Large Enterprises, Government & Defense), By Security Level (Standard, Advanced Encryption, Cloud-Integrated Licensing), Regional Outlook, Competitive Landscape, Market Dynamics, Emerging Trends & Forecast 2025–2034")

, By Application (Engineering & CAD Software, Industrial Automation, Healthcare IT, Media & Entertainment, Professional & Enterprise Software), By End User (SMEs, Large Enterprises, Government & Defense), By Security Level (Standard, Advanced Encryption, Cloud-Integrated Licensing), Regional Outlook, Competitive Landscape, Market Dynamics, Emerging Trends & Forecast 2025–2034")

, By Application (Engineering & CAD Software, Industrial Automation, Healthcare IT, Media & Entertainment, Professional & Enterprise Software), By End User (SMEs, Large Enterprises, Government & Defense), By Security Level (Standard, Advanced Encryption, Cloud-Integrated Licensing), Regional Outlook, Competitive Landscape, Market Dynamics, Emerging Trends & Forecast 2025–2034")

Frequently Asked Questions

How big is the Software Protection Dongle Market?

The global Software Protection Dongle Market was valued at USD 505.4 million in 2024 and is projected to reach USD 2,180.6 million by 2034, growing at a CAGR of 9.3% during 2025–2034. Rising software piracy, demand for secure licensing, hardware-based encryption, and adoption across engineering, healthcare, and industrial software are driving long-term market growth.

Who are the major players in the Software Protection Dongle Market?

Feitian Technologies Co., Ltd., Wibu-Systems AG, Donglify Ltd., Thales Group, SecuTech Solution, Inc., Microcosm Ltd., Keylok, Inc., Marx CryptoTech LP, Electronic Team, Inc., Other Major Players

Which segments covered the Software Protection Dongle Market?

By Type, (USB Dongles, Parallel Port Dongles, Others), By Application, (Enterprise Software, Media & Entertainment, Healthcare, Education, Others), By Organization Size, (Large Enterprises, SMEs), By Industry Vertical, (IT & Telecom, BFSI, Healthcare, Manufacturing, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Software Protection Dongle Market

Published Date : 07 Jan 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date