- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Software Supply Chain Security Market Size, Share | CAGR 21.8%

Global Software Supply Chain Security Market Size, Share, Analysis By Offering (Solutions & Platforms, Managed Services, Consulting & Integration Services), By Solution Type (Software Composition Analysis, SBOM Management, CI/CD Pipeline Security, Artifact & Container Signing, Dependency & Repository Security), By Deployment Mode (Cloud, On-Premise, Hybrid), By Organization Size (Large Enterprises, SMEs), By Vertical (BFSI, IT & Technology, Government & Defense, Healthcare, Manufacturing) Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

|---|---|---|---|

| USD 2.4 Billion | USD 14.2 Billion | 21.8% | North America, 43.8% |

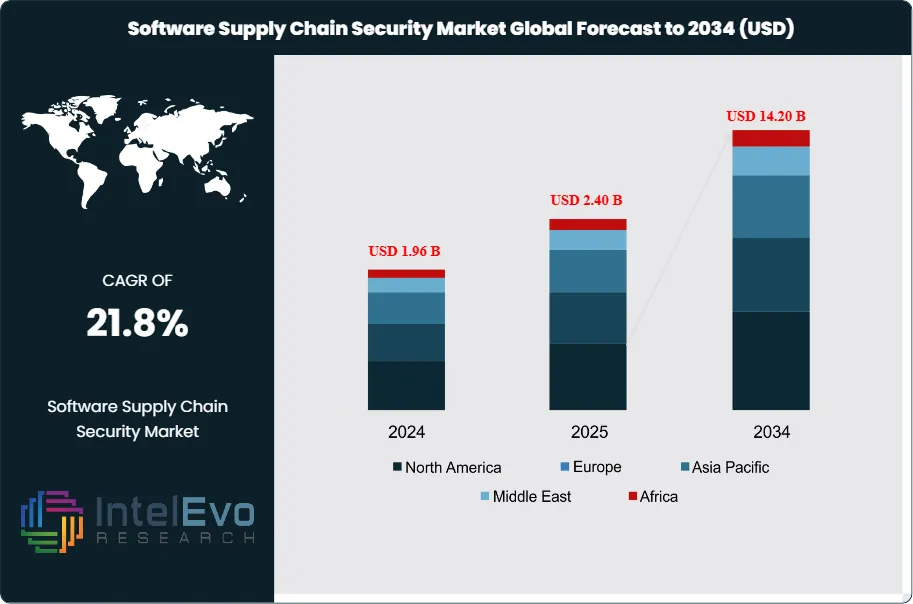

The Software Supply Chain Security Market was valued at approximately USD 1.96 Billion in 2024 and reached USD 2.40 Billion in 2025. The market is projected to grow to USD 14.20 Billion by 2034, expanding at a CAGR of 21.8% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 11.8 Billion over the analysis period. The software supply chain security market has matured into one of the fastest-scaling segments within cybersecurity, driven by the sharp increase in open-source component usage, the proliferation of CI/CD toolchains, and the shift of attacker economics from runtime breaches to code and dependency compromise.

Get More Information about this report -

Request Free Sample ReportDemand has accelerated following a chain of high-impact incidents involving compromised open-source packages, malicious typosquats, and build system intrusions. Open-source components now make up 70-90% of the average commercial codebase, and studies of enterprise repositories indicate that a typical application carries 150-200 transitive dependencies. Attackers have responded. Malicious package uploads to npm, PyPI, RubyGems, and NuGet exceeded 220,000 unique events in 2024, with a significant share traced to coordinated campaigns. Executive Order 14028 in the United States, the NIST Secure Software Development Framework (SSDF), and the EU Cyber Resilience Act have turned SBOMs, provenance, and dependency hygiene from best practice into procurement and regulatory requirements.

Supply-side activity has been equally intense. Venture capital invested over USD 2.8 Billion into software supply chain security specialists across 2023-2025, with multiple companies crossing the USD 1 Billion private valuation mark. Established security vendors have consolidated through acquisition, and cloud platforms have embedded supply chain scanning natively into developer tooling. AI-assisted reachability analysis, binary composition analysis, and automated remediation are reshaping buyer expectations. Enterprises now expect a single platform to cover dependency risk, secrets exposure, IaC misconfiguration, artifact signing, and build pipeline integrity.

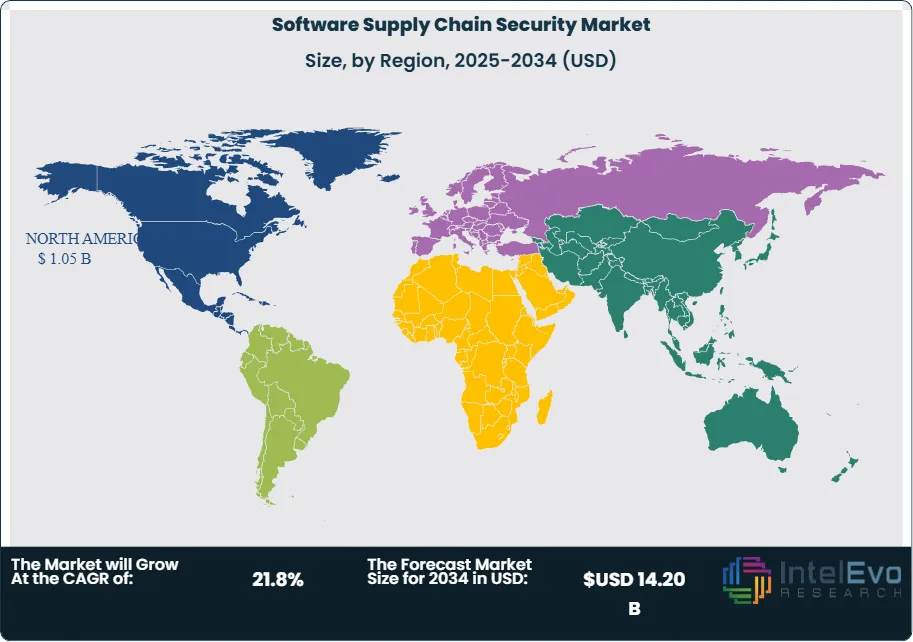

Regulatory momentum will remain the central growth catalyst. CISA's Secure by Design principles, the DoD CMMC 2.0 framework, PCI DSS 4.0 supply chain clauses, and mandatory SBOM delivery under FDA premarket guidance for medical devices are all pulling spend forward. North America continues to lead the software supply chain security market at 43.8% of 2025 value, supported by federal agency mandates and a concentrated vendor base. Europe is the second-largest region, propelled by the Cyber Resilience Act compliance cycle, while Asia Pacific is the fastest-growing regional pocket as Japan, South Korea, and Australia extend federal SBOM requirements to regulated industries.

, By Solution Type (Software Composition Analysis, SBOM Management, CI/CD Pipeline Security, Artifact & Container Signing, Dependency & Repository Security), By Deployment Mode (Cloud, On-Premise, Hybrid), By Organization Size (Large Enterprises, SMEs), By Vertical (BFSI, IT & Technology, Government & Defense, Healthcare, Manufacturing) Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The software supply chain security market was valued at USD 2.4 Billion in 2025 and is projected to reach USD 14.2 Billion by 2034, expanding at a CAGR of 21.8% across the 2026-2034 forecast period.

- Segment Dominance: Solutions and platforms captured 68.4% of software supply chain security market value in 2025, reflecting enterprise preference for integrated SCA, SBOM, and pipeline security suites.

- Segment Dominance: BFSI led vertical demand with 27.8% share in 2025, driven by regulator-enforced SBOM and third-party software attestation requirements under DORA and PCI DSS 4.0.

- Driver: Open-source components now account for 70-90% of enterprise codebases, and malicious package uploads exceeded 220,000 events in 2024, forcing continuous dependency screening at scale.

- Restraint: Alert fatigue remains a material restraint. Enterprise AppSec teams process 500-1,200 supply chain findings per week on average, with accurate reachability filtering deployed at under 35% of buyers.

- Opportunity: The shift to SBOM-mandated procurement under EO 14028, the EU Cyber Resilience Act, and FDA premarket guidance opens an incremental opportunity estimated at USD 3.2 Billion between 2026 and 2030.

- Trend: AI-assisted reachability analysis and autonomous remediation adoption rose to 38% of new platform deployments in 2025, cutting time to patch by 42-55% in benchmark deployments.

- Regional Analysis: North America led the software supply chain security market in 2025 with 43.8% share and USD 1.05 Billion in revenue, reinforced by federal procurement rules and a concentrated vendor base.

Competitive Landscape Overview

The software supply chain security market is moderately fragmented at the top of the stack and highly fragmented below it. The four largest vendors collectively accounted for an estimated 41.5% of platform revenue in 2025, with the balance spread across mid-sized specialists and early-stage challengers. Competition is primarily technology-driven, centered on reachability accuracy, SBOM depth, signed artifact support, and integration with dominant CI/CD toolchains. Acquisitions have intensified since 2024 as platform vendors absorb niche capabilities such as binary composition analysis, malicious package detection, and pipeline integrity. Large cybersecurity platforms are consolidating supply chain modules into broader ASPM and cloud security offerings, pressuring standalone vendors to demonstrate depth or partner with toolchain leaders.

Competitive Landscape Matrix

| Company | Headquarters | Market Position | Key Platform / Solution | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| Snyk | United States / United Kingdom | Leader | Snyk Developer Security Platform (SCA, Container, IaC) | North America, Europe | Acquired Probely in 2025 to extend DAST coverage into the developer workflow |

| Sonatype | United States | Leader | Nexus Repository Firewall and Lifecycle (SCA, SBOM) | North America, Europe | Launched Sonatype Cloud+ in 2025 for federated SBOM and policy enforcement |

| GitHub (Microsoft) | United States | Leader | GitHub Advanced Security (Dependabot, CodeQL, secret scanning) | North America, Europe, Asia Pacific | Made Advanced Security available as a standalone SKU for non-GitHub source in 2025 |

| JFrog | Israel / United States | Leader | JFrog Curation and JFrog Xray (artifact security, SBOM) | North America, Europe | Expanded JFrog Curation with ML-based malicious package detection in 2025 |

| Palo Alto Networks | United States | Challenger | Prisma Cloud Supply Chain Security (Bridgecrew heritage) | North America, Europe | Integrated supply chain scoring into Cortex Cloud consolidated platform in 2025 |

| Checkmarx | Israel / United States | Challenger | Checkmarx One (SCA, SAST, container, SCS) | North America, Europe | Released Checkmarx One AppSec Agents in 2025 for autonomous remediation |

| Chainguard | United States | Challenger | Chainguard Images and Chainguard Enforce | North America | Closed USD 140 Million Series D in 2024 at a USD 3.5 Billion valuation |

| Synopsys (Black Duck) | United States | Challenger | Black Duck SCA and Polaris | North America, Europe, Asia Pacific | Black Duck separated as an independent software security business in 2024 |

| ReversingLabs | United States / Croatia | Niche Player | Spectra Assure (binary-level supply chain analysis) | North America, Europe | Expanded Spectra Assure coverage to container and AI model artifacts in 2025 |

| Endor Labs | United States | Niche Player | Endor Labs Dependency Lifecycle Management | North America | Raised USD 93 Million Series B in 2024 to expand reachability-based SCA |

By Offering

Solutions and platforms dominated the software supply chain security market with 68.4% share in 2025, equivalent to USD 1.64 Billion. Integrated platforms covering software composition analysis, SBOM generation, artifact signing, secrets scanning, and pipeline configuration have become the default buying pattern among large enterprises. Buyers consolidate around single platforms to reduce tool sprawl, standardize policy, and unify reporting for audit and regulatory use. Differentiation within platforms is built on reachability analysis accuracy, dependency graph depth, and native support for major CI/CD runners including GitHub Actions, GitLab CI, Azure DevOps, and Jenkins.

Services contributed 31.6% at approximately USD 0.76 Billion in 2025. This category includes managed AppSec services, SBOM program consulting, policy design, and incident response for supply chain events. Services demand is pulled by regulated industries and federal contractors building toward NIST SSDF and EO 14028 attestation readiness. Systems integrators and specialist consultancies are scaling dedicated supply chain practices, and managed services providers are launching co-managed offerings where tooling is licensed by the vendor and operated by the MSSP. Growth through 2034 will be balanced, with solutions maintaining leadership but services benefitting from a recurring audit and attestation cycle.

By Solution Type

Software Composition Analysis (SCA) held the largest solution type share at 26.5% in 2025, reflecting the foundational role of dependency scanning in supply chain risk reduction. Modern SCA tools now extend beyond CVE matching into reachability analysis, license compliance, and malicious package detection. SBOM management and SBOM-enabled vulnerability exchange followed at 18.2%, driven by federal and sectoral mandates. CI/CD pipeline security held 17.4%, covering build runner hardening, token and secret protection, and pipeline configuration scanning.

Artifact and container signing solutions captured 14.8% in 2025, anchored by Sigstore, in-toto, and vendor-native attestation chains. Dependency and repository security, including curated open-source feeds and package firewalls, held 13.6%. Other solution types including secrets management integrations, policy engines, and post-release provenance verification made up the remaining 9.5%. SBOM tooling and artifact signing are expected to grow fastest through 2034 as regulatory pressure scales and procurement workflows require machine-readable attestation at every software delivery.

By Deployment Mode

Cloud-based deployment accounted for 64.2% of the software supply chain security market in 2025 at roughly USD 1.54 Billion. Multi-tenant SaaS delivery aligns with developer workflows that are already cloud-native and allows vendors to roll out threat intelligence, malicious package signatures, and reachability model updates continuously. On-premise deployment held 21.8% at USD 0.52 Billion, concentrated in defense, intelligence, and regulated financial environments where air-gapped or sovereign installation remains mandatory. Hybrid deployment captured 14.0% at USD 0.34 Billion, serving enterprises with split build environments or phased cloud migrations. Cloud will extend its lead through 2034, though hybrid is expected to outpace on-premise growth as regulated buyers adopt private SaaS and sovereign cloud models.

By Organization Size

Large enterprises dominated the software supply chain security market with 67.5% share in 2025, equivalent to USD 1.62 Billion. These organizations face the highest regulatory exposure, operate the most complex toolchains, and are the primary targets for pipeline and dependency attacks. They typically standardize on integrated platforms and invest in in-house AppSec teams of 15-50 engineers. SMEs contributed 32.5% at USD 0.78 Billion, served by developer-first SaaS offerings with usage-based pricing and default integrations into GitHub, GitLab, and major package registries. SME growth is expected to outpace large enterprise growth through 2034 as downstream procurement clauses push SBOM and attestation requirements into smaller suppliers.

By Vertical

BFSI led vertical demand at 27.8% share in 2025, worth USD 0.67 Billion, driven by DORA, PCI DSS 4.0, and sectoral third-party risk expectations. IT and technology captured 24.6% at USD 0.59 Billion, reflecting hyperscaler, SaaS, and platform vendor adoption. Government and defense held 14.2% at USD 0.34 Billion, anchored by EO 14028, CMMC 2.0, and federal self-attestation requirements. Healthcare followed at 12.4% or USD 0.30 Billion, pulled by FDA premarket cybersecurity guidance requiring SBOM with medical device submissions. Manufacturing contributed 9.8% as OT software supply chains draw post-incident scrutiny, and retail, telecom, and other verticals rounded out the remaining 11.2%. Regulatory mandates will continue to set pace-of-adoption across verticals through 2034.

Regional Analysis

North America

North America led the software supply chain security market in 2025 with 43.8% share and USD 1.05 Billion in revenue. The United States is the primary driver, supported by EO 14028 self-attestation requirements, OMB Memo M-22-18 and M-23-16, CISA Secure by Design principles, and NIST SSDF adoption across federal contractors. Hyperscalers, federal system integrators, and Fortune 500 financial institutions lead procurement. Canada contributes meaningfully via CCCS guidance and a growing cyber services industry in Ottawa, Toronto, and Montreal. Mexico remains a smaller pocket focused on BFSI and telecom sector adoption. Defense spend under CMMC 2.0 is adding structural tailwind through 2026-2028, and venture investment is concentrated in Silicon Valley, Seattle, Boston, and Austin, which continue to produce a disproportionate share of new supply chain security vendors.

Europe

Europe held 26.4% share at USD 0.63 Billion in 2025. Germany leads regional activity, driven by industrial software and automotive supplier compliance requirements under TISAX and BSI guidance. The United Kingdom ranks second, supported by the NCSC's software security code of practice and a deep financial services adoption base in London. France follows through ANSSI-driven procurement and sovereign cloud initiatives. The Netherlands rounds out the top four, serving as the primary regional testing ground for EU Cyber Resilience Act compliance tooling. The CRA, which imposes essential cybersecurity requirements and SBOM expectations on products with digital elements, is the single biggest demand catalyst. NIS2 enforcement, DORA for financial entities, and GDPR alignment on incident reporting are also reinforcing spend across the region through 2026-2028.

Asia Pacific

Asia Pacific captured 20.8% share at USD 0.50 Billion in 2025 and is the fastest-growing regional market. Japan leads the region, propelled by METI's Software Transparency initiative, JPCERT-driven advisory work, and widespread industrial software usage across automotive and electronics supply chains. China follows with a strong domestic vendor base, CAC-aligned procurement rules, and rapid scaling of DevSecOps among technology platforms. India holds the third position, driven by CERT-In incident reporting rules, a large captive IT services base, and BFSI sector modernization under RBI cybersecurity directives. South Korea is advancing rapidly under K-Shield and sectoral SBOM pilots, with MSIT prioritizing supply chain risk for critical infrastructure. Australia contributes strongly within the region through the Essential Eight, Critical Infrastructure Act, and active CISA-equivalent guidance from the ACSC.

Latin America

Latin America accounted for 4.6% share at USD 0.11 Billion in 2025. Brazil represents the largest country market, supported by LGPD compliance spend, Banco Central directives on financial sector cybersecurity, and fast-growing digital banking supply chain adoption. Mexico ranks second, with demand concentrated in BFSI, manufacturing, and federal IT modernization. Argentina holds the third position, driven by BCRA-aligned financial services adoption and growing SaaS export activity. Regional adoption is tempered by fragmented regulatory mandates and limited dedicated AppSec budgets below the top 100 enterprises. Channel growth is strongest through regional MSSPs and cloud marketplace resale, with multinational enterprises pulling supply chain security requirements into local operations via parent-company policy and global procurement standards. Federal procurement alignment with EO 14028-style attestations is expected to build through 2027-2030.

Middle East & Africa

The Middle East & Africa region held 4.4% share at USD 0.11 Billion in 2025. The United Arab Emirates leads, driven by TDRA frameworks, UAE Cybersecurity Council guidance, and aggressive Smart Dubai and Abu Dhabi Digital Strategy programs. Saudi Arabia follows, anchored by National Cybersecurity Authority (NCA) controls that now explicitly address software supply chain and third-party software risk, supported by Vision 2030 digital infrastructure programs. Israel contributes substantially as the innovation hub, with a disproportionate share of emerging supply chain security vendors headquartered in Tel Aviv and Herzliya. South Africa anchors sub-Saharan activity under POPIA and SARB cybersecurity expectations for the banking sector. Adoption across the broader region is scaling through government and BFSI verticals first, with oil and gas digitalization programs in the GCC adding further impetus through 2026-2030.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Offering

- Solutions & Platforms

- Services (Managed, Consulting, Integration)

By Solution Type

- Software Composition Analysis (SCA)

- SBOM Management

- CI/CD Pipeline Security

- Artifact & Container Signing

- Dependency & Repository Security

- Others (Secrets Management, Policy Engines, Provenance Verification)

By Deployment Mode

- Cloud

- On-Premise

- Hybrid

By Organization Size

- Large Enterprises

- Small & Medium Enterprises (SMEs)

By Vertical

- BFSI

- IT & Technology

- Government & Defense

- Healthcare

- Manufacturing

- Retail, Telecom & Others

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 2.40 B |

| Forecast Revenue (2034) | USD 14.20 B |

| CAGR (2025-2034) | 21.8% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Offering, (Solutions & Platforms, Services (Managed, Consulting, Integration)), By Solution Type, (Software Composition Analysis (SCA), SBOM Management, CI/CD Pipeline Security, Artifact & Container Signing, Dependency & Repository Security, Others (Secrets Management, Policy Engines, Provenance Verification)), By Deployment Mode, (Cloud, On-Premise, Hybrid), By Organization Size, (Large Enterprises, Small & Medium Enterprises (SMEs)), By Vertical, (BFSI, IT & Technology, Government & Defense, Healthcare, Manufacturing, Retail, Telecom & Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | SNYK, SONATYPE, GITHUB (MICROSOFT CORPORATION), JFROG LTD., PALO ALTO NETWORKS, CHECKMARX, CHAINGUARD, SYNOPSYS / BLACK DUCK, REVERSINGLABS, ENDOR LABS, ANCHORE, INC., VERACODE, MEND.IO, AQUA SECURITY, CYCODE, LEGIT SECURITY, APIIRO, SOCKET, INC., PHYLUM, GITLAB INC., OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Solution Type (Software Composition Analysis, SBOM Management, CI/CD Pipeline Security, Artifact & Container Signing, Dependency & Repository Security), By Deployment Mode (Cloud, On-Premise, Hybrid), By Organization Size (Large Enterprises, SMEs), By Vertical (BFSI, IT & Technology, Government & Defense, Healthcare, Manufacturing) Industry Trends & Forecast 2026-2034")

, By Solution Type (Software Composition Analysis, SBOM Management, CI/CD Pipeline Security, Artifact & Container Signing, Dependency & Repository Security), By Deployment Mode (Cloud, On-Premise, Hybrid), By Organization Size (Large Enterprises, SMEs), By Vertical (BFSI, IT & Technology, Government & Defense, Healthcare, Manufacturing) Industry Trends & Forecast 2026-2034")

, By Solution Type (Software Composition Analysis, SBOM Management, CI/CD Pipeline Security, Artifact & Container Signing, Dependency & Repository Security), By Deployment Mode (Cloud, On-Premise, Hybrid), By Organization Size (Large Enterprises, SMEs), By Vertical (BFSI, IT & Technology, Government & Defense, Healthcare, Manufacturing) Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Software Supply Chain Security Market?

The Global Software Supply Chain Security Market was valued at USD 1.96 Billion in 2024 and is projected to reach USD 14.20 Billion by 2034, growing at a CAGR of 21.8% from 2026 to 2034. Growth is driven by increasing software supply chain attacks, rising adoption of DevSecOps, software bill of materials (SBOM), code signing, vulnerability management, CI/CD pipeline security, open-source software governance, and secure software development lifecycle (SSDLC) practices across global enterprises.

Who are the major players in the Software Supply Chain Security Market?

SNYK, SONATYPE, GITHUB (MICROSOFT CORPORATION), JFROG LTD., PALO ALTO NETWORKS, CHECKMARX, CHAINGUARD, SYNOPSYS / BLACK DUCK, REVERSINGLABS, ENDOR LABS, ANCHORE, INC., VERACODE, MEND.IO, AQUA SECURITY, CYCODE, LEGIT SECURITY, APIIRO, SOCKET, INC., PHYLUM, GITLAB INC., OTHERS

Which segments covered the Software Supply Chain Security Market?

By Offering, (Solutions & Platforms, Services (Managed, Consulting, Integration)), By Solution Type, (Software Composition Analysis (SCA), SBOM Management, CI/CD Pipeline Security, Artifact & Container Signing, Dependency & Repository Security, Others (Secrets Management, Policy Engines, Provenance Verification)), By Deployment Mode, (Cloud, On-Premise, Hybrid), By Organization Size, (Large Enterprises, Small & Medium Enterprises (SMEs)), By Vertical, (BFSI, IT & Technology, Government & Defense, Healthcare, Manufacturing, Retail, Telecom & Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Software Supply Chain Security Market

Published Date : 01 Jun 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date