- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Soil Sensor Technology Market Size, Share | CAGR of 11.3%

Global Soil Sensor Technology Market Size, Share, Growth By Sensor Type (Moisture, Temperature, Nutrient, pH), By Connectivity (Wired, Wireless, IoT-Enabled), By Application (Precision Agriculture, Greenhouses, Landscaping, Environmental Monitoring), By End-User (Farmers, Research, Government) Region, Key Players – Dynamics, Smart Farming IoT & Precision Agronomy Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

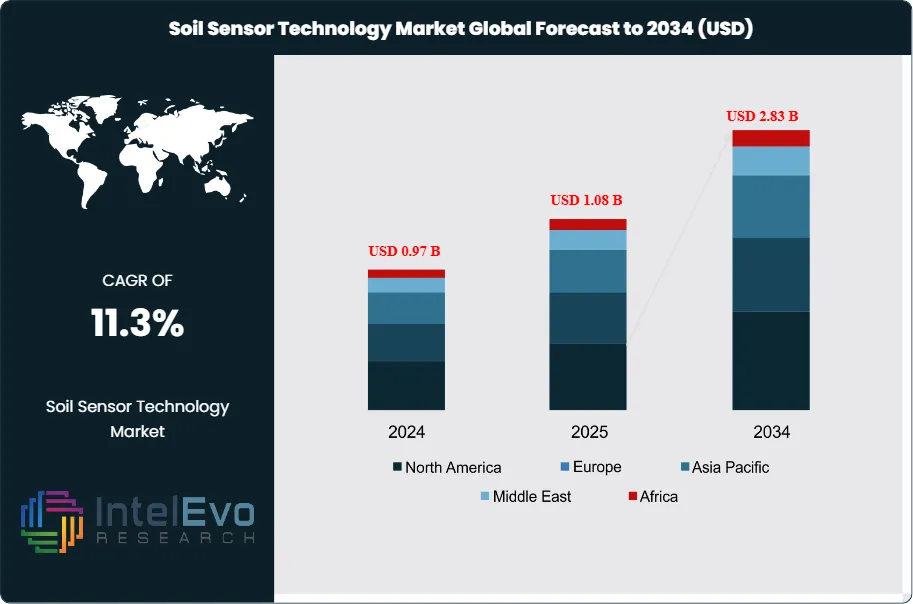

| USD 1.08 Billion | USD 2.83 Billion | 11.3% | North America, 37.5% |

The Soil Sensor Technology Market was valued at USD 0.97 Billion in 2024 and reached USD 1.08 Billion in 2025. The market is projected to grow to USD 2.83 Billion by 2034, expanding at a CAGR of 11.3% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 1.75 Billion across the analysis window.

Get More Information about this report -

Request Free Sample ReportDemand stems from converging pressures across precision agriculture, climate adaptation policy, and water-use regulation. The U.S. Department of Agriculture's Natural Resources Conservation Service (NRCS) has channeled funding toward soil health under its Climate-Smart Mitigation Activities, and the Secretary of Agriculture's memorandum dated December 31, 2025 elevated soil health and precision nutrition as central pillars of federal R&D allocations beginning in 2026. These priorities translate into procurement signals for capacitance probes, time-domain reflectometry (TDR) sensors, and multi-parameter probes used in nutrient-management and water-use efficiency programs.

The regulatory environment stiffened materially during late 2025. Directive (EU) 2025/2360, the EU Soil Monitoring Law, took force on December 16, 2025, requiring all 27 Member States to monitor physical, chemical, and biological soil descriptors at five-year minimum intervals. The directive sets a 2050 horizon for healthy soils across the bloc and obliges Member States to transpose the framework within three years, accelerating procurement of in-situ instrumentation across both private and public-sector buyers.

Technology layers are consolidating around multi-parameter probes that measure moisture, temperature, electrical conductivity (EC), pH, and nitrogen-phosphorus-potassium (NPK) concentrations from a single insertion. LoRaWAN and NB-IoT have stabilized as the dominant low-power connectivity protocols for soil and asset monitoring, while satellite IoT options including those from Astrocast and Sony Semiconductor Solutions Corporation address coverage gaps in remote farmland. Edge processing inside gateway devices now supports near-real-time irrigation triggers, with response latencies measured in minutes rather than hours.

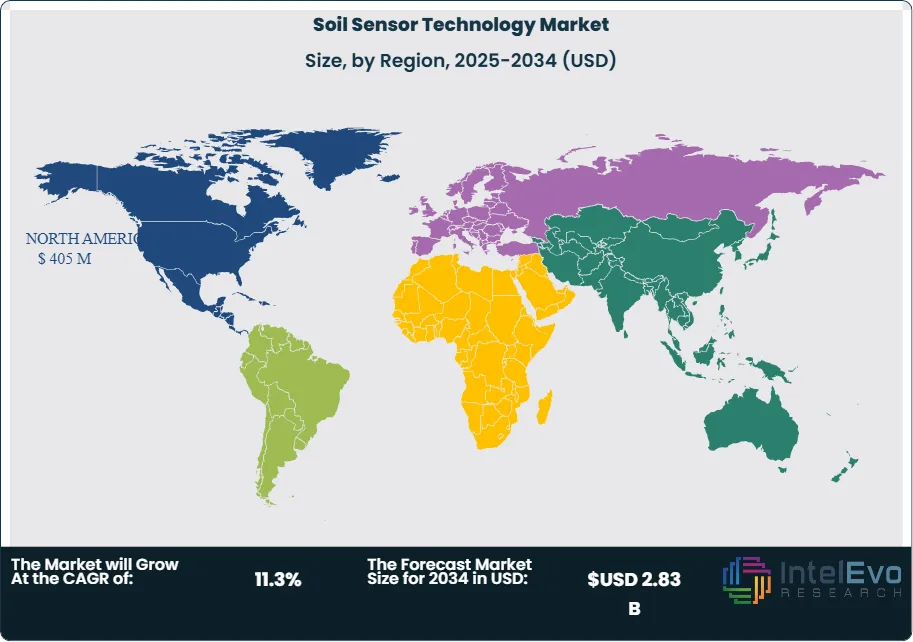

North America accounted for the largest revenue share at 37.5% in 2025, equivalent to roughly USD 405 Million, driven by mechanized agriculture in the Midwest, USDA conservation funding, and dense channel partnerships among irrigation OEMs and sensor vendors. Asia Pacific is positioned as the fastest-growing region through 2034, supported by India's Soil Health Card Scheme integration into the Rashtriya Krishi Vikas Yojana from 2022-23, China's smart agriculture projects, and Japan's November 2025 collaboration between Internet Initiative Japan and Sony Semiconductor Solutions Corporation on soil moisture and irrigation navigation services.

The forward outlook through 2034 hinges on three conditions: continued declines in module cost for capacitance and TDR sensors; broadening compliance demand from EU Member States transposing Directive (EU) 2025/2360; and sustained adoption among large commercial farms operating center pivot irrigation systems. CropX Technologies, METER Group, Inc., Sentek Technologies, and Campbell Scientific, Inc. retain leading positions, with intensifying competition from Lindsay Corporation's METOS-aligned offerings following its January 6, 2025 minority stake in Pessl Instruments GmbH.

Market Definition & Scope

The global soil sensor technology market comprises in-situ electronic instrumentation that measures physical, chemical, and biological soil parameters and transmits the data to control systems, agronomic platforms, or research databases. The market encompasses soil moisture sensors (capacitance, time-domain reflectometry, frequency-domain reflectometry, tensiometers), soil temperature sensors, soil pH sensors, electrical-conductivity and salinity sensors, nutrient sensors targeting nitrogen, phosphorus, and potassium, and multi-parameter probes that integrate three or more measurement channels in a single body.

Scope inclusions cover sensor hardware, embedded telemetry units required for data transmission, and the calibration and integration services bundled at point of sale. Excluded items include standalone farm management software platforms sold without hardware, soil-laboratory analytical instruments such as benchtop spectrometers, satellite-only soil moisture estimation services, and weather stations without a buried soil-contact sensor element. The parent market is the agricultural sensor and precision agriculture segment, valued at USD 2.3 Billion in 2025; soil sensor technology represents approximately 47% of that parent.

, By Connectivity (Wired, Wireless, IoT-Enabled), By Application (Precision Agriculture, Greenhouses, Landscaping, Environmental Monitoring), By End-User (Farmers, Research, Government) Region, Key Players – Dynamics, Smart Farming IoT & Precision Agronomy Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The soil sensor technology market reached USD 1.08 Billion in 2025 and is projected to climb to USD 2.83 Billion by 2034 at an 11.3% CAGR, an absolute dollar opportunity of USD 1.75 Billion.

- Segment Dominance (Sensor Type): Soil moisture sensors led with 42.0% revenue share in 2025, equivalent to roughly USD 454 Million.

- Segment Dominance (Application): Open-field agriculture commanded 48.0% share at USD 518 Million in 2025, anchored by row-crop deployments under center pivot irrigation systems.

- Driver: Water-scarcity policy is the primary growth driver, with agriculture accounting for an estimated 70% of global freshwater withdrawals; sensor-led irrigation has demonstrated water-use reductions of up to 30% in U.S. field trials.

- Restraint: Initial capital expenditure for multi-probe networks ranges from a few thousand dollars to six figures per farm, which slows adoption among smallholders below 50 hectares.

- Opportunity: The trailing nine-year window offers an absolute dollar opportunity of USD 1.75 Billion, concentrated in multi-parameter probes (forecast to grow at roughly 14.5% CAGR) and wireless connectivity deployments.

- Trend: Wireless connectivity captured an estimated 58.0% of unit shipments in 2025, displacing legacy wired installations as LoRaWAN and NB-IoT module pricing fell.

- Regional: North America held 37.5% revenue share in 2025 at approximately USD 405 Million, supported by USDA NRCS Climate-Smart Mitigation Activities funding allocations.

Key Insights Summary

- On December 16, 2025, Directive (EU) 2025/2360 (Soil Monitoring Law) took effect, requiring all 27 EU Member States to deploy harmonized soil-health monitoring within a three-year transposition window.

- During November 2025, Reinke Manufacturing began bundling a complimentary CropX soil sensor with every new center pivot irrigation system sold under the ReinCloud 3 platform integration.

- In October 2025, CropX Technologies released the Strato 1 in-field weather station, designed to operate alongside its existing twist-in soil moisture probe network.

- Per the U.S. Secretary of Agriculture's memorandum dated December 31, 2025, federal research grants beginning in 2026 will prioritize soil health, precision nutrition, and water-use efficiency.

- During August 2025, CropX brought to market a soil-resident system that tracks nitrogen and salt movement through the profile in real time, addressing accuracy critiques of conductivity-proxy NPK probes.

- On November 17, 2025, Internet Initiative Japan and Sony Semiconductor Solutions Corporation began establishing soil moisture sensors and irrigation navigation services across Japanese smart-farm pilot sites.

Competitive Landscape Overview

The global soil sensor technology market is moderately fragmented. The top four vendors, namely CropX Technologies, METER Group, Inc., Sentek Technologies, and Campbell Scientific, Inc., collectively hold an estimated 27% to 32% of revenue based on aggregated company disclosures and channel-partner footprints, with the remainder distributed across mid-tier specialists and a long tail of regional manufacturers. Competition is technology-led at the upper end of the market, with vendors differentiating on probe accuracy, calibration libraries, telemetry battery life, and breadth of integration with farm management software.

The mid-market has turned price-sensitive following the entry of Chinese OEMs offering 7-in-1 and 8-in-1 multi-parameter probes at sub-USD 100 unit pricing through RS485-Modbus interfaces. The competitive picture shifted noticeably during 2024-2025: Lindsay Corporation closed its 49.9% stake in Pessl Instruments GmbH on January 6, 2025 and integrated the METOS sensor portfolio with its FieldNET irrigation platform. CropX Technologies continues to broaden through integration partnerships and product launches, while Deere & Company and CNH Industrial have moved planter-mounted sensing into commercial fleets, intensifying pressure on pure-play sensor vendors.

Competitive Landscape Matrix

| Company | HQ | Position | Key Product | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| CropX Technologies | Israel/US | Leader | CropX agronomic farm management system | Deployed across 50+ countries | Rolled out unified ReinCloud 3 integration in November 2025 |

| METER Group, Inc. | United States | Leader | TEROS capacitance probes and ZENTRA software | North America, Europe | Continued ZENTRA platform expansion through Q4 2025 |

| Sentek Technologies | Australia | Leader | Drill & Drop and EnviroScan multi-depth probes | Asia Pacific, Australia, Africa | Operates dealer presence across more than 80 countries |

| Campbell Scientific, Inc. | United States | Leader | CS650 and CS655 reflectometry sensors | North America, Europe | Continued partnerships with research stations in 2025 |

| Stevens Water Monitoring | United States | Challenger | HydraProbe series | North America | Maintained federal-agency contract base into 2025 |

| Irrometer Company | United States | Challenger | Granular matrix and tensiometer sensors | North America | Sustained presence through irrigation-channel partners |

| Delta-T Devices | United Kingdom | Niche Player | ML3 ThetaProbe and PR2 profile probe | Europe, research markets | Continued export to government soil monitoring programs |

| Acclima, Inc. | United States | Niche Player | TDR-315 digital reflectometry probes | North America | Deepened OEM partnerships for irrigation equipment |

| Sensoterra | Netherlands | Niche Player | Single-depth wireless soil moisture sensors | Europe | Broadened integration partner roster across 2025 |

| Spectrum Technologies | United States | Niche Player | WatchDog and FieldScout product families | North America | Expanded distributor footprint into Latin America |

Segmentation Analysis

The global soil sensor technology market segments by sensor type, connectivity, application, and end-user. Each segmentation type reveals distinct adoption curves, pricing dynamics, and competitive structure across the 2025-2034 forecast period.

By Sensor Type

Soil moisture sensors led the soil sensor technology market with 42.0% revenue share in 2025, equivalent to approximately USD 454 Million. Capacitance probes dominate within the moisture sub-category given their accuracy in heterogeneous soil profiles and tolerance for in-ground operation across multi-year deployments. METER Group's TEROS family, Sentek's Drill & Drop, and CropX's twist-in probes anchor the moisture sub-segment. Time-domain reflectometry products from Acclima, Inc. and Campbell Scientific, Inc. compete in research and commercial deployments where volumetric water content tolerances below 2% are required. Tensiometers, a legacy technology, retain relevance for high-value horticulture including berry, vegetable, and vineyard plantings sensitive to soil-water-tension thresholds.

Multi-parameter sensors held 21.5% share at roughly USD 232 Million in 2025 and represent the fastest-growing sub-segment through 2034 at an estimated 14.5% CAGR. Devices integrating moisture, temperature, EC, pH, and NPK measurements remove the procurement and installation overhead of deploying separate single-parameter probes. Chinese manufacturers have driven aggressive pricing on RS485-Modbus 7-in-1 probes, while higher-end units from METER Group and Sentek target commercial growers needing calibrated outputs for nutrient-management decisions. Compared with single-parameter moisture probes, multi-parameter units carry approximately 2.5x to 4x average selling price but reduce deployment density requirements.

Soil nutrient (NPK) sensors accounted for 12.0% share at USD 130 Million in 2025, while soil pH sensors held 9.5%, EC and salinity sensors 8.0%, and dedicated soil temperature sensors 7.0%. Nutrient sensors face lingering accuracy critiques because most field-deployable NPK probes derive readings from electrical conductivity proxies rather than ion-selective electrochemistry; the August 2025 CropX nitrogen-and-salt tracking system targets that gap with direct measurement of ion movement through the profile. Total sub-segment shares within sensor type sum to 100.0%.

By Connectivity

Wireless soil sensors captured 58.0% of revenue in the soil sensor technology market in 2025 at approximately USD 626 Million and continue to gain share through 2034. The shift reflects falling LoRaWAN and NB-IoT module pricing, multi-year battery lives that reduce service overhead, and the broader rollout of satellite IoT options for farms outside terrestrial coverage. Sony Semiconductor Solutions Corporation's November 2025 collaboration with Internet Initiative Japan signals satellite IoT entering Japanese smart-farm deployments at commercial scale.

Wired soil sensors retained 42.0% share at USD 454 Million in 2025, holding ground in research stations, geotechnical engineering, and large-scale commercial deployments where data integrity must be guaranteed across multi-decade datasets. Federal soil monitoring programs, including the Missouri Soil Monitoring Project expanded under the National Integrated Drought Information System (NIDIS) in March 2025, continue to specify wired or hybrid wired-wireless installations to meet hydrologic forecasting tolerances.

By Application

Open-field agriculture led the soil sensor technology market with 48.0% revenue share at USD 518 Million in 2025, anchored by row-crop deployments in maize, soybean, wheat, cotton, and sugarcane operations. Center pivot irrigation systems remain the dominant insertion point for sensor procurement, with the Reinke-CropX free-sensor bundling program disclosed in November 2025 illustrating how irrigation OEMs are now treating sensors as core peripherals rather than aftermarket accessories. Protected cultivation, including greenhouse and vertical-farm applications, took 12.5% share at USD 135 Million and is forecast to grow above the market average through 2034 as controlled-environment agriculture broadens across China, the Netherlands, and the U.S. Southeast.

Construction and mining accounted for 10.5% share at USD 113 Million in 2025, where soil moisture and density measurements underpin earthworks compaction testing and wetland delineation. Forestry and landscaping captured 9.0%, research and environmental monitoring 11.0%, and sports turf, residential, and other end-uses 9.0%. The research and environmental monitoring sub-segment is positioned to gain share following the December 16, 2025 entry into force of Directive (EU) 2025/2360, which requires Member States to deploy harmonized monitoring networks within a three-year transposition deadline. Application sub-segment shares sum to 100.0%.

By End-User

Large commercial farms held 41.5% revenue share in the soil sensor technology market at approximately USD 448 Million in 2025, propelled by economies of scale in sensor-network deployment and the financing capacity to absorb six-figure full-stack precision agriculture buildouts. Mid-size farms accounted for 22.0% at USD 238 Million, research institutes and government agencies 14.5% at USD 157 Million, small and cooperative farms 12.0% at USD 130 Million, and non-agricultural end-users including mining, construction, and turf operations 10.0% at USD 108 Million.

The small and cooperative farm sub-segment is gaining share through sensor-as-a-service contracts that lower entry barriers, with monthly subscription fees replacing lump-sum hardware purchases. Research institutes and government agencies will accelerate procurement against the EU Soil Monitoring Law's harmonized-monitoring obligations and against U.S. federal soil-data programs continued under the December 31, 2025 USDA Secretary's R&D memorandum. End-user sub-segment shares total 100.0%.

Regional Analysis

The global soil sensor technology market spans North America, Europe, Asia Pacific, Latin America, and Middle East & Africa, with regional shares summing to 100.0%.

North America

North America led the soil sensor technology market with 37.5% revenue share in 2025, equivalent to USD 405 Million. The United States accounted for the bulk of regional demand, with Canada and Mexico contributing supporting volumes through Western Canadian wheat operations and Mexican greenhouse exports respectively. USDA NRCS Climate-Smart Mitigation Activities funding, the December 31, 2025 USDA Secretary's R&D memorandum prioritizing soil health, and federal Inflation Reduction Act allocations sustained procurement through 2025. The Missouri Soil Monitoring Project expansion announced by NIDIS in March 2025 added sensor capacity at more than 35 stations and authorized up to 10 new ones, funded through the American Rescue Plan Act.

Europe

Europe held 24.5% revenue share at USD 265 Million in the soil sensor technology market in 2025. Germany, France, Spain, the Netherlands, and Italy anchor regional demand, with deployments concentrated in cereals, viticulture, and protected horticulture. Directive (EU) 2025/2360, in force from December 16, 2025, materially restructures the regional opportunity by requiring all 27 Member States to monitor physical, chemical, and biological soil descriptors at minimum five-year intervals through 2050. The associated three-year transposition window pulls forward sensor procurement across both private and public-sector buyers. Horizon Europe's Mission Soil program, including AI4SoilHealth and BENCHMARKS projects, channels grant funding into sensor-calibrated reference sites across the bloc.

Asia Pacific

Asia Pacific captured 27.0% revenue share at USD 292 Million in 2025 and is the fastest-growing regional market through 2034. China leads regional volumes via state-supported smart agriculture projects and soil pollution remediation programs. India's Soil Health Card Scheme, merged into the Rashtriya Krishi Vikas Yojana from 2022-23 under the Soil Health and Fertility component, drives demand for portable testing units across more than 28 states and union territories. On November 17, 2025, Internet Initiative Japan and Sony Semiconductor Solutions Corporation began establishing soil moisture sensors and irrigation navigation services across Japanese smart-farm zones. Australia and South Korea contribute through specialty-crop and orchard deployments, with Sentek Technologies anchoring Australian dealer channels from its Stepney, South Australia headquarters.

Latin America

Latin America accounted for 6.5% revenue share at USD 70 Million in 2025. Brazil dominates regional volumes through soybean, sugarcane, and citrus operations, with Argentina and Chile contributing through wine-grape and stone-fruit exports. Adoption is concentrated among large estates, while smallholder penetration stays limited by capital cost. Brazilian agribusinesses have begun deploying CropX-integrated platforms across Mato Grosso and Goiás soybean operations, while Chilean exporters use Sentek probes for vineyard moisture management.

Middle East & Africa

Middle East and Africa held 4.5% revenue share at USD 49 Million in 2025. Israel, Saudi Arabia, the United Arab Emirates, and South Africa lead regional deployments, with Israeli vendor CropX Technologies headquartered in Tel Aviv playing both domestic and export roles. Gulf states have channeled sovereign-wealth funding into controlled-environment agriculture and saline-soil mitigation programs, where multi-parameter probes measuring EC and salinity carry premium relevance. Sub-Saharan deployments remain donor-driven, with development-bank programs financing pilot soil moisture networks across Kenya, Ethiopia, and Senegal.

Country Analysis

The global soil sensor technology market concentrates around four national markets that together accounted for approximately 60% of 2025 revenue: the United States, China, India, and Germany.

United States

The United States soil sensor technology market was valued at USD 335 Million in 2025 with a country-specific CAGR of 10.8% projected through 2034. Demand is anchored by row-crop agriculture across the Corn Belt, specialty produce in California's Central Valley, and federal soil monitoring programs administered by USDA-NRCS, the U.S. Geological Survey, and NOAA. The December 31, 2025 USDA Secretary's memorandum elevated soil health and water-use efficiency as priority research domains for 2026 funding cycles, signaling sustained federal demand. State-level programs, including the Missouri Soil Monitoring Project expansion and California Sustainable Groundwater Management Act compliance frameworks, layer additional procurement above the federal baseline.

China

The Chinese soil sensor technology market reached USD 165 Million in 2025 with a country-specific CAGR of 14.6% through 2034, the fastest among the major national markets. State-supported smart agriculture projects, soil pollution remediation programs, and Ministry of Agriculture and Rural Affairs precision-farming subsidies anchor demand. Domestic OEMs including JXCT, Niubol, and a long tail of Shenzhen-based manufacturers have driven aggressive pricing on multi-parameter probes, while imported high-end probes from METER Group and Sentek hold preferred positioning in research and export-oriented horticulture operations. China's Smart Agriculture Projects continue funding sensor-network buildouts across Heilongjiang, Shandong, and Sichuan grain-producing zones.

India

The Indian soil sensor technology market was valued at USD 78 Million in 2025 with a country-specific CAGR of 14.2% through 2034. The Soil Health Card Scheme, which had distributed more than 22 crore cards across two phases between 2015 and 2019, continues under the Rashtriya Krishi Vikas Yojana from 2022-23 as the Soil Health and Fertility component. The scheme tests 12 critical soil parameters including pH, electrical conductivity, and organic carbon at three-year intervals across more than 28 states and union territories. Domestic startups and an expanding imported-instrument distribution channel serve commercial farms in Maharashtra, Punjab, and Andhra Pradesh, while donor-funded pilots reach into rainfed smallholder zones.

Germany

The German soil sensor technology market reached USD 65 Million in 2025 with a country-specific CAGR of 11.5% through 2034. Demand stems from cereals and rapeseed agriculture, the protected-horticulture cluster around Lower Saxony, and a substantial research-station footprint anchored by the Julius Kühn-Institut and university test plots. Following the December 16, 2025 entry into force of Directive (EU) 2025/2360, the German federal government is tasked with transposing the directive within three years, pulling forward procurement. Germany's domestic vendor base remains limited, with imported probes from METER Group, Sentek, Delta-T Devices Ltd., and Pessl Instruments capturing the majority of installed base.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Sensor Type

- Moisture Sensors

- Temperature Sensors

- Nutrient Sensors

- pH Sensors

- Others

By Connectivity

- Wired

- Wireless

- IoT-Enabled

By Application

- Precision Agriculture

- Greenhouses

- Turf & Landscaping

- Environmental Monitoring

- Others

By End-User

- Farmers

- Agricultural Research Institutes

- Greenhouse Operators

- Government & Environmental Agencies

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 1.08 B |

| Forecast Revenue (2034) | USD 2.83 B |

| CAGR (2025-2034) | 11.3% |

| Historical data | 2021-2025 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Sensor Type, (Moisture Sensors, Temperature Sensors, Nutrient Sensors, pH Sensors, Others), By Connectivity, (Wired, Wireless, IoT-Enabled), By Application, (Precision Agriculture, Greenhouses, Turf & Landscaping, Environmental Monitoring, Others), By End-User, (Farmers, Agricultural Research Institutes, Greenhouse Operators, Government & Environmental Agencies, Others), |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | CROPX TECHNOLOGIES, METER GROUP, INC., SENTEK TECHNOLOGIES, CAMPBELL SCIENTIFIC, INC., STEVENS WATER MONITORING SYSTEMS, INC., IRROMETER COMPANY, INC., DELTA-T DEVICES LTD., ACCLIMA, INC., SENSOTERRA BV, THE TORO COMPANY, LINDSAY CORPORATION, SPECTRUM TECHNOLOGIES, INC., AQUASPY INC., AQUACHECK PVT. LTD., PESSL INSTRUMENTS GMBH, VEGETRONIX, INC., LIBELIUM COMUNICACIONES DISTRIBUIDAS S.L., SDEC FRANCE, IMKO MICROMODULTECHNIK GMBH, HYDROPOINT DATA SYSTEMS, INC., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Connectivity (Wired, Wireless, IoT-Enabled), By Application (Precision Agriculture, Greenhouses, Landscaping, Environmental Monitoring), By End-User (Farmers, Research, Government) Region, Key Players – Dynamics, Smart Farming IoT & Precision Agronomy Trends & Forecast 2026-2034")

, By Connectivity (Wired, Wireless, IoT-Enabled), By Application (Precision Agriculture, Greenhouses, Landscaping, Environmental Monitoring), By End-User (Farmers, Research, Government) Region, Key Players – Dynamics, Smart Farming IoT & Precision Agronomy Trends & Forecast 2026-2034")

, By Connectivity (Wired, Wireless, IoT-Enabled), By Application (Precision Agriculture, Greenhouses, Landscaping, Environmental Monitoring), By End-User (Farmers, Research, Government) Region, Key Players – Dynamics, Smart Farming IoT & Precision Agronomy Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Soil Sensor Technology Market?

Global Soil Sensor Technology Market was valued at USD 0.97 billion in 2024 and is projected to reach USD 2.83 billion by 2034, at a CAGR of 11.3% (2026–2034).

Who are the major players in the Soil Sensor Technology Market?

CROPX TECHNOLOGIES, METER GROUP, INC., SENTEK TECHNOLOGIES, CAMPBELL SCIENTIFIC, INC., STEVENS WATER MONITORING SYSTEMS, INC., IRROMETER COMPANY, INC., DELTA-T DEVICES LTD., ACCLIMA, INC., SENSOTERRA BV, THE TORO COMPANY, LINDSAY CORPORATION, SPECTRUM TECHNOLOGIES, INC., AQUASPY INC., AQUACHECK PVT. LTD., PESSL INSTRUMENTS GMBH, VEGETRONIX, INC., LIBELIUM COMUNICACIONES DISTRIBUIDAS S.L., SDEC FRANCE, IMKO MICROMODULTECHNIK GMBH, HYDROPOINT DATA SYSTEMS, INC., Others

Which segments covered the Soil Sensor Technology Market?

By Sensor Type, (Moisture Sensors, Temperature Sensors, Nutrient Sensors, pH Sensors, Others), By Connectivity, (Wired, Wireless, IoT-Enabled), By Application, (Precision Agriculture, Greenhouses, Turf & Landscaping, Environmental Monitoring, Others), By End-User, (Farmers, Agricultural Research Institutes, Greenhouse Operators, Government & Environmental Agencies, Others),

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Soil Sensor Technology Market

Published Date : 17 Jul 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date