- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

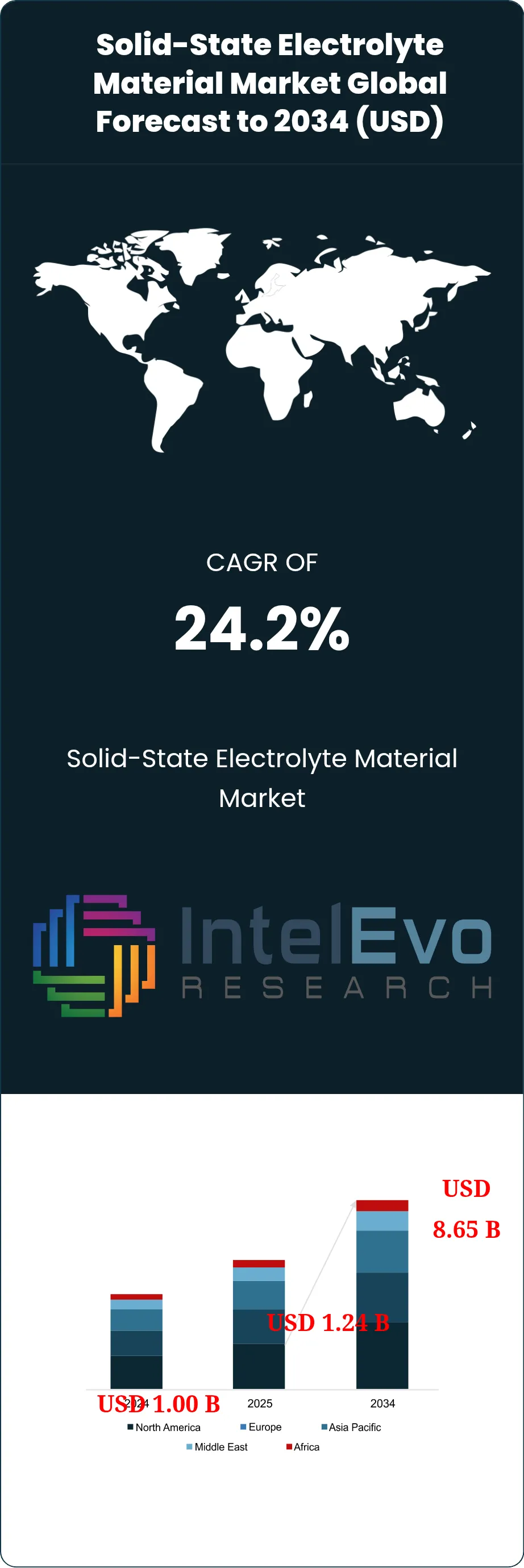

Global Solid-State Electrolyte Market Forecast 2034 | CAGR 24.2%

Global Solid-State Electrolyte Market Size, Share, Growth & Industry Analysis By Material Type (Sulfide-Based Electrolytes, Oxide Ceramic Electrolytes, Polymer Electrolytes, Composite & Hybrid Electrolytes), By Application (Electric Vehicle Batteries, Consumer Electronics, Grid-Scale Energy Storage, Aerospace & Defense), By Form (Powder, Thin Film, Pellet & Sheet) Industry Trends, Battery Innovation Landscape & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

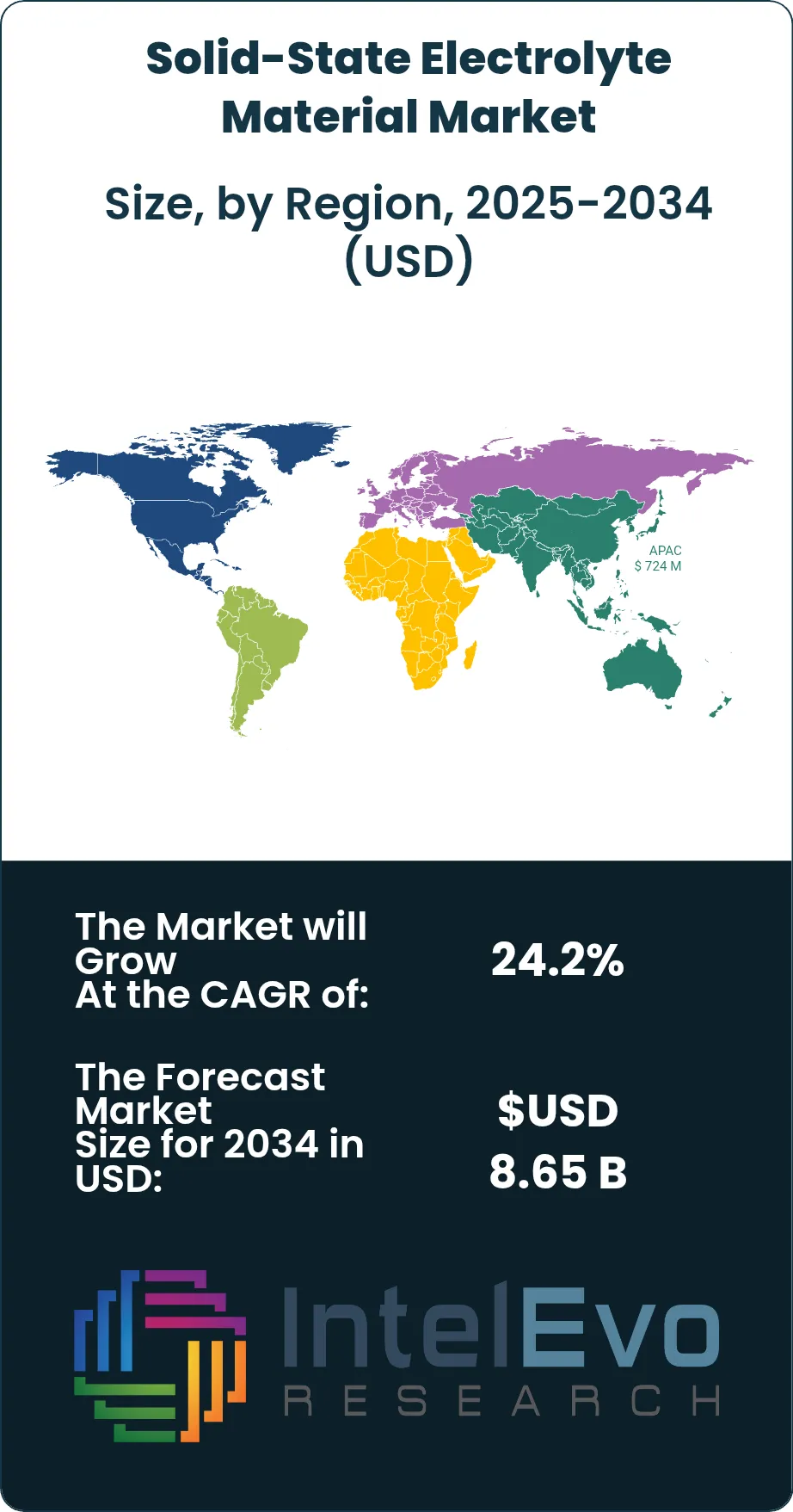

| USD 1.24 Billion | USD 8.65 Billion | 24.2% | Asia Pacific, 58.4% |

The Solid-State Electrolyte Material Market was valued at approximately USD 1.00 Billion in 2024 and reached USD 1.24 Billion in 2025. The market is projected to grow to USD 8.65 Billion by 2034, expanding at a CAGR of 24.2% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 7.41 Billion over the analysis period. Solid-state electrolyte materials serve as the ionic conduction medium in solid-state batteries, replacing flammable liquid electrolytes used in conventional lithium-ion batteries. These materials enable higher energy density, improved safety characteristics, and extended cycle life, making them essential for electric vehicle and energy storage system advancement.

Get More Information about this report -

Request Free Sample ReportThe solid-state electrolyte material market growth reflects intensifying automotive industry investment in battery technology. Major automakers have committed over USD 135 Billion collectively to solid-state battery development through 2030, with commercial vehicle deployment timelines advancing to 2027-2028. Solid-state batteries using these electrolyte materials deliver energy densities of 400-500 Wh/kg compared to 250-300 Wh/kg for current lithium-ion technology. This performance improvement translates to 40-80% range extension for electric vehicles at equivalent battery weight. The elimination of liquid electrolytes removes flammability risks and enables faster charging rates up to 80% capacity in under 15 minutes without thermal runaway concerns.

Material science advancement has progressed solid-state electrolyte material technology from laboratory demonstration to pilot-scale production. Sulfide-based electrolytes achieve ionic conductivity of 10-25 mS/cm at room temperature, approaching liquid electrolyte performance. Oxide ceramic electrolytes provide superior stability but require higher processing temperatures and exhibit lower conductivity. Polymer electrolytes offer manufacturing compatibility with existing production equipment but function optimally only at elevated temperatures. The industry consensus points toward sulfide materials for automotive applications and oxide ceramics for stationary storage, with hybrid approaches combining multiple material classes gaining research attention.

Regional production concentration shapes solid-state electrolyte material supply chain dynamics. Asia Pacific dominates with 58.4% market share in 2025, anchored by Japanese and Korean battery manufacturers and Chinese material suppliers. Japan leads in sulfide electrolyte synthesis technology through companies including Mitsui Mining, Idemitsu Kosan, and AGC. South Korea drives commercialization through Samsung SDI and LG Energy Solution battery development programs. North America represents 24.8% share through QuantumScape, Solid Power, and emerging players supported by Department of Energy funding. European Union battery alliance initiatives are establishing regional supply chains with 12.5% current share projected to increase through localization requirements under the EU Battery Regulation.

, By Application (Electric Vehicle Batteries, Consumer Electronics, Grid-Scale Energy Storage, Aerospace & Defense), By Form (Powder, Thin Film, Pellet & Sheet) Industry Trends, Battery Innovation Landscape & Forecast 2026–2034")

Key Takeaways

- Market Growth: The solid-state electrolyte material market expands from USD 1.24 Billion in 2025 to USD 8.65 Billion by 2034, registering a CAGR of 24.2% across the nine-year forecast period.

- Segment Dominance: Sulfide-based electrolytes command the largest share by material type at 48.5% in 2025, driven by superior ionic conductivity performance enabling room-temperature battery operation.

- Segment Dominance: Electric vehicle batteries lead application segmentation with 68.2% market share in 2025, reflecting automotive industry investment concentration in solid-state battery technology.

- Driver: Electric vehicle manufacturers have committed USD 135 Billion to solid-state battery development through 2030, creating sustained demand for high-performance electrolyte materials.

- Restraint: Manufacturing scale-up challenges persist with current sulfide electrolyte production costs at USD 150-300 per kilogram compared to USD 10-15 per kilogram for liquid electrolytes.

- Opportunity: Grid-scale energy storage applications represent a USD 1.8 Billion incremental opportunity through 2034 as solid-state batteries address fire safety concerns in utility installations.

- Trend: Hybrid electrolyte systems combining sulfide and polymer materials have entered pilot production at 4 facilities globally in 2025, addressing processability limitations of pure ceramic approaches.

- Regional Analysis: Asia Pacific maintains market leadership with 58.4% share representing USD 724 Million in 2025, driven by Japanese sulfide electrolyte technology and Korean battery manufacturing scale.

Competitive Landscape Overview

The solid-state electrolyte material market exhibits moderate concentration with the top four players controlling approximately 52% of global revenue in 2025. Competition centers on ionic conductivity performance, manufacturing scalability, and strategic partnerships with automotive OEMs. Japanese materials companies hold technology leadership in sulfide electrolyte synthesis, while US-based cell developers have secured significant automotive investment. Samsung SDI, Panasonic, QuantumScape, and Solid Power lead through differentiated technology platforms and OEM partnerships. Chinese entrants including CATL and Ganfeng Lithium are accelerating development timelines through substantial capital deployment. The competitive intensity has increased as commercialization timelines compress from 2030 to 2027-2028.

Competitive Landscape Matrix

| Company Name | HQ | Position | Key Solution | Geographic Strength | Recent Strategic Move (2024-2026) |

| Samsung SDI | South Korea | Leader | Sulfide-Based SSE | Asia Pacific | Mar 2025: Opened USD 2.1B solid-state battery plant in Korea |

| Panasonic Holdings | Japan | Leader | Oxide Ceramic Electrolyte | Asia Pacific, North America | Jan 2025: Partnered with Toyota on sulfide electrolyte production |

| QuantumScape | USA | Leader | Ceramic Separator Technology | North America | Jun 2025: Achieved 24-layer cell validation with OEM partners |

| Solid Power Inc. | USA | Leader | Sulfide Electrolyte Cells | North America | Sep 2025: Delivered A-sample cells to BMW and Ford |

| CATL | China | Challenger | Condensed Matter Battery | Asia Pacific | Apr 2025: Announced 500 Wh/kg SSB prototype |

| Mitsui Mining & Smelting | Japan | Challenger | Argyrodite Sulfide SSE | Asia Pacific | Nov 2024: Scaled production to 100 tonnes/year capacity |

| Idemitsu Kosan | Japan | Challenger | LGPS-Type Sulfide | Asia Pacific | Feb 2025: JV with Toyota for mass electrolyte production |

| Ganfeng Lithium | China | Challenger | Oxide and Sulfide SSE | Asia Pacific | Aug 2025: Invested USD 340M in SSE production facility |

| ProLogium Technology | Taiwan | Niche Player | Ceramic Oxide Electrolyte | Asia Pacific | Dec 2024: Secured EUR 500M for France gigafactory |

| Ilika plc | UK | Niche Player | Stereax Micro-batteries | Europe | Oct 2025: Launched Goliath SSB for EV applications |

By Material Type

Sulfide-based electrolytes dominate the solid-state electrolyte material market with 48.5% share valued at USD 601 Million in 2025. This segment encompasses argyrodite-type compounds including Li6PS5Cl and LGPS-type materials such as Li10GeP2S12 that achieve ionic conductivity of 10-25 mS/cm at room temperature. Sulfide electrolytes enable practical battery operation without heating systems required by other material classes. Japanese chemical companies including Mitsui Mining and Idemitsu Kosan have scaled production capacity to hundreds of tonnes annually, reducing material costs by 40% since 2022. The segment benefits from compatibility with high-nickel cathode materials used in electric vehicle batteries. Manufacturing challenges include moisture sensitivity requiring inert atmosphere processing and hydrogen sulfide generation during synthesis.

Oxide ceramic electrolytes account for 32.8% market share representing USD 407 Million in 2025. This category includes garnet-type LLZO materials, NASICON-type compounds, and perovskite-structured electrolytes. Oxide ceramics provide superior electrochemical stability with wide voltage windows exceeding 5V and complete air stability during handling. QuantumScape has demonstrated ceramic separator technology enabling lithium metal anodes with 80% capacity retention beyond 800 cycles. Manufacturing requires high-temperature sintering processes at 800-1200 degrees Celsius, increasing energy costs and limiting throughput. Ionic conductivity ranges from 0.1 to 1 mS/cm, necessitating thin-film architectures below 50 micrometers to minimize resistance. The segment finds application in high-performance cells where safety and longevity justify cost premiums.

Polymer electrolytes hold 14.2% share at USD 176 Million in 2025. Polymer-based materials including polyethylene oxide and polypropylene oxide derivatives offer processing advantages compatible with roll-to-roll manufacturing and existing lithium-ion production equipment. Room-temperature ionic conductivity remains limited at 0.001-0.01 mS/cm, requiring operating temperatures above 60 degrees Celsius for practical performance. The segment addresses niche applications where elevated temperature operation is acceptable, including certain industrial and grid storage deployments. Research focus has shifted toward composite approaches combining polymer matrices with ceramic fillers to improve ambient conductivity while maintaining processability advantages.

Composite and hybrid electrolytes represent 4.5% share valued at USD 56 Million in 2025. These materials combine characteristics of multiple electrolyte classes, typically incorporating ceramic particles within polymer or sulfide matrices. Composite approaches address interfacial contact challenges between rigid ceramic electrolytes and electrode materials while maintaining mechanical flexibility. Several automotive development programs have adopted hybrid architectures for initial commercial vehicles, balancing performance with manufacturing practicality. The segment grows at 28.5% CAGR through 2034 as hybrid approaches prove viability in commercial applications.

By Application

Electric vehicle batteries command the largest application share at 68.2% representing USD 846 Million in 2025. Automotive OEMs have established direct partnerships with solid-state electrolyte material suppliers to secure supply chains for planned vehicle launches. Toyota has invested over USD 13 Billion in solid-state battery development targeting 2027-2028 vehicle introduction. BMW, Ford, and Volkswagen maintain development agreements with QuantumScape and Solid Power for next-generation vehicle platforms. The application benefits from premium pricing acceptance in automotive markets where range extension and charging speed justify material costs. Energy density improvements from 250 to 450+ Wh/kg enable 500+ mile vehicle range with current battery pack volumes.

Consumer electronics batteries account for 18.5% share at USD 229 Million in 2025. Smartphones, wearables, and portable devices benefit from solid-state battery safety characteristics and energy density improvements enabling thinner product designs. Apple, Samsung Electronics, and other device manufacturers have explored solid-state technology for premium product lines. Manufacturing scale requirements are more manageable than automotive applications, enabling earlier commercial adoption. Micro-battery applications for medical implants and IoT sensors represent specialized niches where solid-state technology has achieved commercial deployment through companies including Ilika.

Grid-scale energy storage represents 8.8% share valued at USD 109 Million in 2025. Utility-scale battery installations have experienced fire safety incidents with liquid electrolyte systems, creating demand for inherently safer solid-state alternatives. While cost premiums currently limit adoption, solid-state batteries eliminate thermal runaway propagation risks that have caused facility evacuations and insurance challenges for grid storage projects. The application is projected to accelerate through 2034 as manufacturing scale reduces solid-state battery costs toward grid storage price thresholds. Stationary applications can accommodate higher operating temperatures, enabling polymer electrolyte deployment.

Aerospace and defense applications hold 4.5% share at USD 56 Million in 2025. Aviation and military applications prioritize energy density and safety over cost, making solid-state batteries attractive despite premium pricing. Urban air mobility vehicles and electric aircraft development programs have evaluated solid-state technology for propulsion batteries where weight is critical. Defense applications include soldier-carried equipment, unmanned systems, and satellite power systems. This segment tolerates costs ten times higher than automotive applications when performance requirements justify the investment.

Regional Analysis

Asia Pacific Solid-State Electrolyte Material Market

Asia Pacific dominates the solid-state electrolyte material market with 58.4% share valued at USD 724 Million in 2025. Japan leads regional technology development through materials companies and battery manufacturers that have pursued solid-state technology for over two decades. Japanese sulfide electrolyte producers including Mitsui Mining & Smelting, Idemitsu Kosan, and AGC have scaled production capacity and established partnerships with Toyota, Honda, and Nissan for automotive applications. Japan solid-state electrolyte material revenue reached USD 312 Million in 2025. South Korea contributes USD 248 Million through Samsung SDI and LG Energy Solution development programs integrated with their respective conglomerate material supply chains. China generates USD 118 Million as CATL, BYD, and Ganfeng Lithium accelerate domestic technology development supported by government subsidies and local EV market demand. Taiwan adds USD 46 Million through ProLogium Technology, which has attracted European investment for oxide electrolyte manufacturing.

North America Solid-State Electrolyte Material Market

North America holds 24.8% market share representing USD 307 Million in 2025 for solid-state electrolyte material. The United States dominates regional activity at USD 278 Million through venture-funded companies that have secured substantial automotive OEM investment. QuantumScape received over USD 1 Billion from Volkswagen and other investors for ceramic electrolyte commercialization. Solid Power has partnered with BMW and Ford for sulfide electrolyte cell development. Department of Energy funding through ARPA-E and Battery Manufacturing programs has supported university research and pilot production facilities. The Inflation Reduction Act battery manufacturing incentives extend to solid-state technology, with production tax credits available for domestic electrolyte material manufacturing. Canada contributes USD 29 Million through academic research programs and mining companies positioning for lithium and germanium supply chains critical to solid-state battery production.

Europe Solid-State Electrolyte Material Market

Europe represents 12.5% market share valued at USD 155 Million in 2025 within the solid-state electrolyte material market. Germany leads regional demand at USD 68 Million through automotive OEM development programs including BMW, Volkswagen, and Mercedes-Benz partnerships with US and Asian electrolyte technology companies. The EU Battery Regulation mandates increasing recycled content and carbon footprint disclosure, favoring localized supply chains. France generates USD 42 Million following ProLogium's EUR 500 Million investment announcement for a solid-state battery gigafactory near Dunkirk. The United Kingdom contributes USD 28 Million through Ilika and academic research programs supported by the Faraday Institution. European Investment Bank financing has targeted solid-state battery manufacturing under green transition initiatives. The European Battery Alliance has identified solid-state technology as strategic priority for regional battery independence.

Latin America Solid-State Electrolyte Material Market

Latin America accounts for 2.6% market share valued at USD 32 Million in 2025 within solid-state electrolyte material. Regional activity concentrates in lithium mining and processing rather than downstream electrolyte manufacturing. Chile and Argentina hold substantial lithium reserves essential for solid-state battery cathodes and certain electrolyte formulations. Brazil generates USD 18 Million through automotive industry research programs and university partnerships with global technology leaders. Mexico contributes USD 11 Million as automotive manufacturing investment includes battery supply chain development. The region positions as raw material supplier rather than electrolyte producer in current market structure, though policy initiatives aim to capture more value-added manufacturing.

Middle East and Africa Solid-State Electrolyte Material Market

Middle East and Africa represent 1.7% market share valued at USD 22 Million in 2025 for solid-state electrolyte material. The United Arab Emirates leads regional activity at USD 11 Million through sovereign wealth fund investments in global battery technology companies and research partnerships with Japanese and Korean firms. Saudi Arabia generates USD 8 Million through NEOM development plans that include advanced battery manufacturing facilities. Israel contributes through academic research programs but limited commercial production. South Africa maintains minimal market participation at USD 3 Million despite significant manganese resources used in certain cathode formulations. The region grows at 18.5% CAGR through 2034 as energy diversification strategies increase investment in battery technology and electric vehicle adoption accelerates in Gulf Cooperation Council countries.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Material Type

- Sulfide-Based Electrolytes

- Oxide Ceramic Electrolytes

- Polymer Electrolytes

- Composite and Hybrid Electrolytes

By Application

- Electric Vehicle Batteries

- Consumer Electronics Batteries

- Grid-Scale Energy Storage

- Aerospace and Defense Applications

By Form

- Powder

- Thin Film

- Pellet and Sheet

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 1.24 B |

| Forecast Revenue (2034) | USD 8.65 B |

| CAGR (2025-2034) | 24.2% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Material Type, (Sulfide-Based Electrolytes, Oxide Ceramic Electrolytes, Polymer Electrolytes, Composite and Hybrid Electrolytes), By Application, (Electric Vehicle Batteries, Consumer Electronics Batteries, Grid-Scale Energy Storage, Aerospace and Defense Applications), By Form, (Powder, Thin Film, Pellet and Sheet) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | SAMSUNG SDI CO., LTD., PANASONIC HOLDINGS CORPORATION, QUANTUMSCAPE CORPORATION, SOLID POWER INC., CATL (CONTEMPORARY AMPEREX TECHNOLOGY), MITSUI MINING & SMELTING CO., LTD., IDEMITSU KOSAN CO., LTD., GANFENG LITHIUM CO., LTD., PROLOGIUM TECHNOLOGY CO., LTD., ILIKA PLC, LG ENERGY SOLUTION, SK ON CO., LTD., AGC INC., TOYOTA MOTOR CORPORATION, MURATA MANUFACTURING CO., LTD., OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Electric Vehicle Batteries, Consumer Electronics, Grid-Scale Energy Storage, Aerospace & Defense), By Form (Powder, Thin Film, Pellet & Sheet) Industry Trends, Battery Innovation Landscape & Forecast 2026–2034")

, By Application (Electric Vehicle Batteries, Consumer Electronics, Grid-Scale Energy Storage, Aerospace & Defense), By Form (Powder, Thin Film, Pellet & Sheet) Industry Trends, Battery Innovation Landscape & Forecast 2026–2034")

, By Application (Electric Vehicle Batteries, Consumer Electronics, Grid-Scale Energy Storage, Aerospace & Defense), By Form (Powder, Thin Film, Pellet & Sheet) Industry Trends, Battery Innovation Landscape & Forecast 2026–2034")

Frequently Asked Questions

How big is the Solid-State Electrolyte Material Market?

Global Solid-state electrolyte market valued at USD 1.00B in 2024, reaching USD 8.65B by 2034, growing at a CAGR of 24.2% from 2026–2034.

Who are the major players in the Solid-State Electrolyte Material Market?

SAMSUNG SDI CO., LTD., PANASONIC HOLDINGS CORPORATION, QUANTUMSCAPE CORPORATION, SOLID POWER INC., CATL (CONTEMPORARY AMPEREX TECHNOLOGY), MITSUI MINING & SMELTING CO., LTD., IDEMITSU KOSAN CO., LTD., GANFENG LITHIUM CO., LTD., PROLOGIUM TECHNOLOGY CO., LTD., ILIKA PLC, LG ENERGY SOLUTION, SK ON CO., LTD., AGC INC., TOYOTA MOTOR CORPORATION, MURATA MANUFACTURING CO., LTD., OTHERS

Which segments covered the Solid-State Electrolyte Material Market?

By Material Type, (Sulfide-Based Electrolytes, Oxide Ceramic Electrolytes, Polymer Electrolytes, Composite and Hybrid Electrolytes), By Application, (Electric Vehicle Batteries, Consumer Electronics Batteries, Grid-Scale Energy Storage, Aerospace and Defense Applications), By Form, (Powder, Thin Film, Pellet and Sheet)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Solid-State Electrolyte Material Market

Published Date : 17 Apr 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date