- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Space Data Analytics Market Size, Share & Forecast | CAGR 20.9%

Global Space Data Analytics Market Size, Share, Analysis By Service (Data Analytics & Processing Services, Geospatial Analytics, Predictive & Prescriptive Analytics, Image Processing & Interpretation, AI & Machine Learning Analytics, Managed Analytics Services), By Vertical (Defense, Agriculture, Energy, Environmental Monitoring, Transportation, Government), By End-Use, By Data Type, Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

|---|---|---|---|

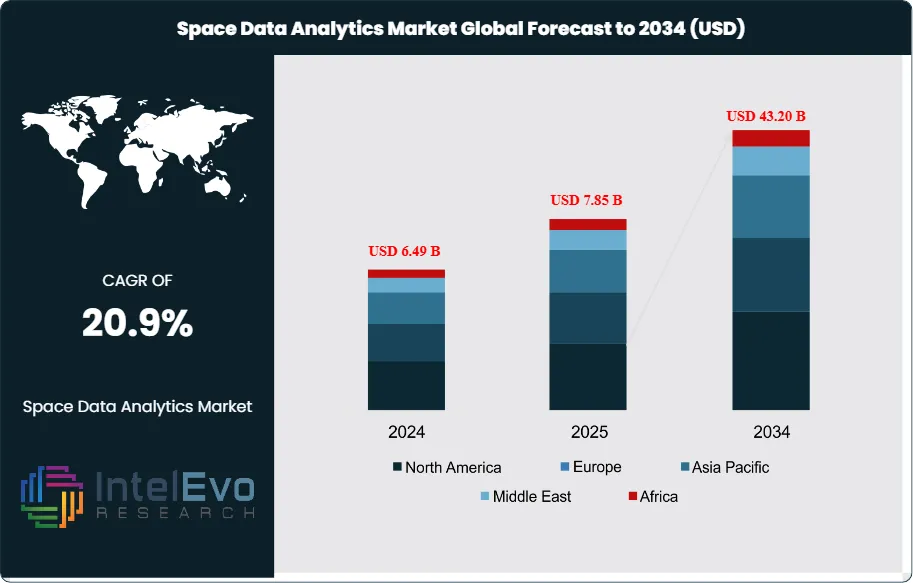

| USD 7.85 Billion | USD 43.20 Billion | 20.9% | North America, 41.3% |

The Space Data Analytics Market was valued at approximately USD 6.49 Billion in 2024 and reached USD 7.85 Billion in 2025. The market is projected to grow to USD 43.20 Billion by 2034, expanding at a CAGR of 20.9% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 35.35 Billion over the analysis period. The Space Data Analytics Market covers the commercial space for software, AI platforms, and services that transform raw satellite-acquired data including Earth observation imagery, Synthetic Aperture Radar (SAR), radio frequency (RF) signals, weather sensing, and automatic identification system (AIS) maritime tracking into actionable insights for defense, agriculture, energy, insurance, maritime, environmental monitoring, and urban planning applications.

Get More Information about this report -

Request Free Sample ReportDemand growth is anchored in three structural shifts. First, the National Reconnaissance Office (NRO) awarded billions of dollars in five-year base commercial imagery contracts with five additional option years through 2032 to Maxar, BlackSky, and Planet Labs, establishing sustained U.S. government demand. Second, the National Geospatial-Intelligence Agency (NGA) Luno B commercial data indefinite delivery indefinite quantity (IDIQ) contract carries a USD 200 million ceiling over a five-year base ordering period, with Planet Labs and BlackSky among selected vendors providing economic, environmental, and geopolitical monitoring. Third, private space economy investment and small satellite constellation deployment continues accelerating, with SpaceX's Starlink, Maxar's WorldView Legion, Planet's Pelican constellation, and Capella's SAR fleet driving exponential growth in available raw data requiring analytics processing.

Major contract and technology developments accelerated through 2024-2025. In December 2025 Planet Labs reported Q3 FY26 record revenue of USD 81 million (up 33% year-over-year) with remaining performance obligations (RPOs) increasing 361% YoY to USD 672 million and backlog increasing 216% YoY to USD 734.5 million. In July 2025 Planet Labs secured a USD 280 million contract with the German government for environmental monitoring and security imagery services. In July 2025 Neo Space Group completed the acquisition of the UP42 geospatial marketplace from Airbus Defence and Space. In March 2025 Juvare partnered with ICEYE to integrate real-time SAR-driven disaster response solutions. In December 2024 Maxar Technologies partnered with Satellogic to integrate high-resolution tasking with frequent-revisit capabilities.

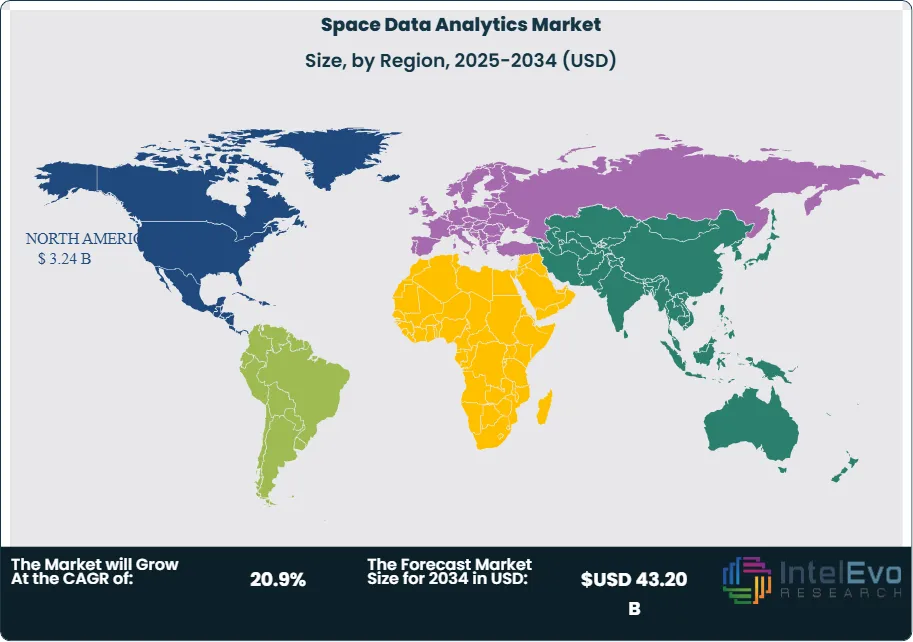

North America held approximately 41.3% of global Space Data Analytics Market revenue in 2025, equivalent to USD 3.24 Billion, anchored by the United States presence of Maxar Vantor, Planet Labs, BlackSky, HawkEye 360, Capella Space, and Spire Global alongside NRO and NGA government demand. Europe captured approximately 23% share at USD 1.81 Billion, led by Airbus Defence and Space (Pleiades Neo, SPOT), ICEYE Finland, and national space agency programs. Asia Pacific held 21% share at USD 1.65 Billion and is projected to grow fastest at approximately 23% CAGR through 2034, anchored by India's ISRO, China's CNSA, Japan's JAXA, and the South Korean Ministry of Science. Latin America and Middle East & Africa collectively held the remaining 14.7% share.

Forward visibility through 2034 rests on three catalysts. First, artificial intelligence and machine learning integration into satellite data pipelines enables automated change detection, predictive analytics, and multi-sensor fusion at unprecedented scale, with Planet Labs, BlackSky, and Maxar deploying AI-enabled partner solutions. Second, the Allied data analytics segment within satellite services is projected to grow at 20.8% CAGR from 2024 to 2034, outpacing raw imagery growth and reflecting the shift toward higher-value insights delivery. Third, climate change monitoring, ESG compliance under the EU Corporate Sustainability Reporting Directive (CSRD), and Task Force on Climate-related Financial Disclosures (TCFD) frameworks drive expanding commercial demand beyond traditional defense applications. These forces together support the 20.9% forecast CAGR in the Space Data Analytics Market through 2034.

Market Definition & Scope

The Space Data Analytics Market is defined as the commercial space for software platforms, artificial intelligence services, and specialist analytical services that transform raw satellite-derived data into actionable insights delivered to commercial and government end-users. The market encompasses three core technology categories: imagery analytics (optical, hyperspectral, multispectral processing with object detection, change detection, and land classification), Synthetic Aperture Radar (SAR) analytics (all-weather all-time imaging from Capella Space, ICEYE, and Umbra), and non-imaging data analytics (RF geolocation from HawkEye 360, weather from Spire, and AIS maritime tracking).

This analysis includes analytic software platforms (Planet Analytic Feeds, BlackSky Spectra AI, Maxar SecureWatch, EOS Data Analytics), data-as-a-service subscriptions, custom analytical services, cloud processing and API infrastructure, and AI-enabled value-added services. The scope explicitly excludes raw satellite hardware manufacturing, launch services and vehicles, ground station infrastructure hardware, satellite communications services without analytics layers, and general-purpose cloud computing without space-specific analytics modules. The parent space economy reached approximately USD 596 billion in 2024 per Space Foundation estimates, with the Space Data Analytics Market representing the software and insights layer above the satellite data services sub-segment, which itself totaled approximately USD 14 billion in 2025.

, By Vertical (Defense, Agriculture, Energy, Environmental Monitoring, Transportation, Government), By End-Use, By Data Type, Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The Space Data Analytics Market grew from USD 7.85 Billion in 2025 to a projected USD 43.20 Billion in 2034, expanding at a 20.9% CAGR.

- Segment Dominance (By Service): Image data analytics held approximately two-thirds of satellite data services revenue in 2024 per Allied Market Research, with data analytics as the fastest-growing service category at 20.8% CAGR through 2034.

- Segment Dominance (By End-Use): The defense and intelligence vertical captured approximately 25% market share in 2024 per Grand View Research, driven by NRO, NGA, NATO, and allied defense agency procurement.

- Driver: Planet Labs reported Q3 FY26 backlog of USD 734.5 million (up 216% YoY) in December 2025, reflecting sustained commercial and government demand for satellite-derived insights.

- Restraint: High satellite fleet deployment capital costs and regulatory complexity around dual-use export controls under U.S. ITAR, EAR, and EU dual-use framework constrain pure-play analytics competitors from scaling.

- Opportunity: The NGA Luno B IDIQ contract carries a USD 200 million ceiling over a five-year base ordering period, providing sustained federal demand for commercial economic, environmental, and geopolitical monitoring.

- Trend: AI integration and multi-sensor data fusion accelerated through 2024-2025, with Planet Labs deploying AI-enabled partner solutions and Maxar Vantor-Satellogic integration combining high-resolution tasking with frequent-revisit capabilities.

- Regional: North America held approximately 41.3% revenue share in 2025 at USD 3.24 Billion, anchored by NRO, NGA, and DoD procurement alongside U.S.-headquartered satellite operators.

Key Insights Summary

- Planet Labs PBC reported Q3 FY26 record revenue of USD 81 million (up 33% year-over-year) with remaining performance obligations (RPOs) up 361% YoY to USD 672 million and backlog up 216% YoY to USD 734.5 million in December 2025.

- In July 2025 Planet Labs secured a USD 280 million contract with the German government for environmental monitoring and security imagery services, representing one of the largest single government commitments in European space data procurement.

- BlackSky Technology was awarded a USD 200 million multi-year Luno B contract with the National Geospatial-Intelligence Agency (NGA) in 2024-2025, growing its backlog from USD 261 million at year-end 2024 to approximately USD 390 million.

- Planet Labs signed a USD 230 million multi-year commercial agreement with SKY Perfect JSAT, the US subsidiary of Asia's largest geostationary satellite operator, to build and operate a constellation of ten low-Earth-orbit Pelican satellites beginning in 2027.

- In July 2025 Neo Space Group completed its acquisition of the UP42 geospatial marketplace from Airbus Defence and Space, consolidating European satellite data distribution infrastructure.

- In December 2024 Maxar Technologies partnered with Satellogic to integrate Maxar's high-resolution tasking capability with Satellogic's frequent-revisit optical imagery, enhancing combined fleet revisit metrics without additional capital expenditure.

- In March 2025 Juvare partnered with ICEYE to integrate real-time SAR-driven satellite solutions into emergency response and disaster management platforms, improving situational awareness for government customers.

Competitive Landscape Overview

The Space Data Analytics Market is moderately concentrated with the top four companies including Planet Labs, Maxar Vantor, BlackSky, and Airbus Defence and Space collectively holding an estimated 50 to 58% of global revenue in 2025. Competition is structured across three tiers: U.S. commercial constellation operators including Planet Labs, Maxar Vantor, BlackSky, Capella Space, HawkEye 360, and Spire Global that combine owned satellite fleets with integrated analytics platforms; European national champions including Airbus Defence and Space (Pleiades Neo, SPOT), ICEYE Finland, and e-GEOS Italy operating under national space agency anchor contracts; and defense prime contractors including L3Harris Technologies, Lockheed Martin, Northrop Grumman, and Boeing providing geospatial intelligence analytics integration for U.S. government customers.

The competitive environment shifted sharply through 2024-2025 toward AI-enabled analytics platforms, multi-sensor integration, and government contract concentration. Maxar Technologies rebranded its intelligence business to Vantor in June 2025 following the Advent International take-private completion. Planet Labs achieved four consecutive quarters of adjusted EBITDA profitability through Q3 FY26 with 98% recurring annual contract value (ACV). BlackSky secured its first Gen-3 satellite revenue and saw 2025 revenue guidance of USD 125-142 million. Government concentration increased with Planet, BlackSky, and Maxar all winning NGA Luno B IDIQ positions. The NRO Electro-Optical Commercial Layer (EOCL) program extension into 2026 provides sustained BlackSky Gen-2 imagery demand. Consolidation pressure intensifies, illustrated by Neo Space Group's UP42 acquisition and Maxar Vantor-Satellogic partnership deepening.

Competitive Landscape Matrix

| Company | HQ | Position | Key Platform | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| Planet Labs PBC | San Francisco, CA, USA | Leader | Planet Analytic Feeds; SkySat and PlanetScope imagery; daily global monitoring | Global | Reported Q3 FY26 record revenue of USD 81M (+33% YoY) and USD 734.5M backlog (+216% YoY) in December 2025 |

| Maxar Technologies (Vantor) | Westminster, CO, USA | Leader | WorldView high-resolution imagery; Precision3D; SecureWatch analytics | Global | Completed Maxar Intelligence rebrand to Vantor in June 2025; continued Satellogic integration partnership |

| BlackSky Technology Inc. | Herndon, VA, USA | Leader | Spectra AI; Gen-2 and Gen-3 imagery; real-time geospatial intelligence | United States, International | Awarded USD 200M multi-year Luno B contract with NGA; backlog grew from USD 261M to USD 390M in 2025 |

| Airbus Defence and Space | Toulouse, France | Leader | Pleiades Neo; SPOT imagery; OneAtlas geospatial platform | Europe, Global | Completed divestment of UP42 geospatial marketplace to Neo Space Group in July 2025 |

| Spire Global, Inc. | Vienna, VA, USA | Challenger | Spire weather data; AIS maritime; ADS-B aviation; RF geolocation | Global | Secured UK Met Office multi-year weather data contract in Q3 2024; continued constellation expansion 2025 |

| ICEYE Oy | Espoo, Finland | Challenger (SAR) | ICEYE SAR imagery; flood and disaster monitoring products | Europe, Global | Partnered with Juvare in March 2025 to integrate real-time SAR data into emergency response platforms |

| HawkEye 360, Inc. | Herndon, VA, USA | Niche (RF) | RF geolocation and signal intelligence analytics | United States, Global | Appointed new CEO in Q1 2025 to drive global expansion; continued defense and maritime domain focus 2025 |

| Capella Space Corporation | San Francisco, CA, USA | Niche (SAR) | Capella SAR constellation; Synthetic Aperture Radar tasking | United States, Global | Continued SAR constellation expansion with sub-50cm resolution imagery for defense customers 2025 |

| Satellogic Inc. | Montevideo, Uruguay | Niche | Aleph satellite tasking; high-resolution optical imagery | Latin America, Global | Expanded Maxar Vantor integration partnership announced December 2024 for high-resolution tasking |

| L3Harris Technologies, Inc. | Melbourne, FL, USA | Leader (Defense) | Geospatial intelligence platforms; ENVI; IDL imagery analytics | United States, Global | Continued NRO and DoD geospatial intelligence contract execution with multi-year backlog 2025 |

Segmentation Analysis

The Space Data Analytics Market segments across service, vertical, end-use, data type, and deployment. Procurement leaders at defense agencies, commodity trading desks, and ESG compliance teams building a space data analytics procurement checklist should benchmark providers on revisit frequency (hours to days), resolution (sub-30cm optical through 10m SAR), analytical product depth (imagery, vector, API feeds), ITAR and dual-use export control compliance, historical archive depth, and AI model integration across each segmentation dimension.

By Service

Image data services led the Space Data Analytics Market with approximately 66% revenue share in 2025, equivalent to USD 5.18 Billion, anchored by Planet Labs daily PlanetScope imagery, Maxar WorldView Legion sub-30cm resolution, BlackSky Gen-2 and Gen-3 imagery, Airbus Pleiades Neo 30cm products, and Capella Space SAR imagery. The image data segment continues leading due to high-resolution imagery demand across agriculture, defense, urban planning, and environmental monitoring. Advancements in multispectral and hyperspectral imaging have enhanced accuracy and detail. Data analytics services captured approximately 34% share at USD 2.67 Billion and are projected to grow fastest at 20.8% CAGR through 2034 per Allied Market Research. Analytics services include Planet Analytic Feeds, BlackSky Spectra AI, EOS Data Analytics, Ursa Space Systems oil storage analytics, and specialized AI-enabled partner solutions.

By Vertical

Defense and intelligence led the Space Data Analytics Market with approximately 31% revenue share in 2025, equivalent to USD 2.43 Billion, anchored by U.S. NRO, NGA, DoD, and allied defense agency procurement. Environmental monitoring captured 18% share at USD 1.41 Billion, growing under EU CSRD disclosure requirements, TCFD climate risk frameworks, and COP28 commitments. Agriculture held 14% share at USD 1.10 Billion, driven by precision agriculture adoption across John Deere, Bayer Crop Science, Corteva, and commodity traders including Cargill, ADM, and Bunge using satellite-derived yield forecasting. Energy and power captured 12% share anchored by oil storage monitoring, pipeline surveillance, and renewable asset optimization. Engineering and infrastructure held 9%, insurance 7%, maritime 6% through AIS-satellite fusion, and transportation/logistics 3%.

By End-Use

The commercial end-use segment captured approximately 48% of Space Data Analytics Market revenue in 2025 and is projected to grow fastest at 21.8% CAGR per Allied Market Research, reflecting accelerating industry adoption of cost-effective high-resolution satellite data. Commercial applications include agricultural yield forecasting, oil storage and commodity analytics, insurance claims verification, real estate and construction monitoring, and retail site selection. Government and military held 52% share at approximately USD 4.08 Billion, anchored by sustained NRO Electro-Optical Commercial Layer extensions, NGA Luno B IDIQ awards (USD 200 million ceiling each for Planet Labs and BlackSky), NATO partnership contracts, and European national defense programs. Space data analytics implementation timelines typically range from 3 months for subscription-based analytics feeds to 18-24 months for custom defense integration programs.

By Data Type

Optical imagery analytics led the Space Data Analytics Market with approximately 62% revenue share in 2025, anchored by daily to sub-daily revisit constellations from Planet Labs (PlanetScope, SkySat), Maxar (WorldView Legion), BlackSky (Gen-2, Gen-3), Airbus (Pleiades Neo, SPOT), and Satellogic. Synthetic Aperture Radar (SAR) analytics captured 18% share at USD 1.41 Billion, growing fastest at approximately 25% CAGR through 2034 given all-weather, all-time imaging capability, led by ICEYE, Capella Space, Umbra, and Synspective. RF and signal intelligence analytics held 8% share led by HawkEye 360 and Kleos Space. Weather and environmental analytics captured 7% led by Spire Global, GHGSat for methane detection, and Tomorrow.io. AIS maritime and ADS-B aviation analytics held the remaining 5% share led by Spire and Exactearth.

Regional Analysis

The Space Data Analytics Market divides across North America, Europe, Asia Pacific, Latin America, and Middle East & Africa, with North America leading in 2025 and Asia Pacific growing fastest through 2034.

North America

North America held 41.3% of global Space Data Analytics Market revenue in 2025, equivalent to USD 3.24 Billion. The United States contributed 94% of regional revenue, Canada at 5%, and Mexico at 1%. The National Reconnaissance Office (NRO) awarded multi-billion-dollar five-year base commercial imagery contracts with five-year option extensions through 2032 to Maxar, Planet Labs, and BlackSky. The National Geospatial-Intelligence Agency (NGA) Luno B IDIQ carries a USD 200 million ceiling with Planet and BlackSky among selected vendors. The Department of Defense Defense Innovation Unit (DIU) Hybrid Space Architecture program drives prototype orders for commercial satellite integration. The U.S. Space Force operates the Commercial Augmentation Space Reserve program. NASA's Commercial Satellite Data Acquisition (CSDA) program funds commercial geospatial procurement. Major U.S. players include Maxar Vantor, Planet Labs, BlackSky, HawkEye 360, Capella Space, Spire Global, and L3Harris.

Europe

Europe captured 23.0% share in 2025 at USD 1.81 Billion, with France, Germany, the United Kingdom, Italy, and Finland leading. The European Union Copernicus program provides the world's largest free-and-open Earth observation data flow through Sentinel-1, Sentinel-2, Sentinel-3, and Sentinel-6 satellites. The European Space Agency (ESA) coordinates continental infrastructure alongside national agencies including France's CNES, Germany's DLR, the UK Space Agency, Italy's ASI, and the French-Italian Pleiades partnership. Airbus Defence and Space operates Pleiades Neo and SPOT constellations generating billions of EUR in annual revenue. ICEYE Finland leads commercial SAR. German Aerospace Center (DLR) awarded Planet Labs a three-year contract in September 2024 for Earth observation data and analytics. Horizon Europe allocates substantial funding to space analytics research through 2027. The UK National Space Strategy commits GBP 10 billion through 2030.

Asia Pacific

Asia Pacific captured 21.0% share in 2025 at USD 1.65 Billion and is projected to grow fastest at approximately 23% CAGR through 2034 per industry analysis. China leads regional deployment with the China National Space Administration (CNSA) and commercial operators Chang Guang Satellite (Jilin-1 constellation) and Spacety operating the largest non-Western commercial constellation. India's Indian Space Research Organisation (ISRO) and commercial entity Pixxel operate high-resolution Earth observation. Japan's JAXA coordinates national programs alongside commercial vendors Axelspace and Synspective (SAR). South Korea's Korea Aerospace Research Institute (KARI) expands under the Korean Space Launch Vehicle (KSLV) program. Australia's Australian Space Agency and Myriota anchor Oceania. BlackSky won multi-year contracts totaling approximately USD 20 million to support India's commercial Earth observation capabilities in 2024-2025.

Latin America

Latin America held 8.5% share in 2025 at approximately USD 667 Million, led by Brazil, Argentina, Mexico, and Uruguay. Brazil's Instituto Nacional de Pesquisas Espaciais (INPE) operates the CBERS program jointly with China. Argentina's CONAE operates the SAOCOM SAR constellation. Satellogic, headquartered in Montevideo, Uruguay, operates one of the largest commercial optical Earth observation fleets globally with over 20 operational satellites. Mexico's Agencia Espacial Mexicana coordinates national programs. Regional growth is driven by deforestation monitoring under Amazon conservation frameworks, precision agriculture across soybean and sugarcane production, and disaster response during recurring hurricane and flooding events. Currency volatility and capital constraints limit faster expansion, though multinational buyers increasingly procure through regional subsidiaries.

Middle East & Africa

The Middle East & Africa region held 6.2% share in 2025 at approximately USD 487 Million. The United Arab Emirates leads regional adoption through the Mohammed bin Rashid Space Centre (MBRSC) operating KhalifaSat and DubaiSat-2, and the UAE Space Agency coordinating the national program. Saudi Arabia's Saudi Space Agency and Neo Space Group, which acquired UP42 from Airbus in July 2025, position the Kingdom as a rising geospatial services hub. Israel's ImageSat International operates the EROS commercial constellation alongside Elbit Systems and Israel Aerospace Industries. Egypt's National Authority for Remote Sensing and Space Sciences coordinates African remote sensing. South Africa's SANSA and Dragonfly Aerospace anchor Sub-Saharan domestic capabilities. Nigeria's NASRDA operates NigeriaSat series. Regional growth is driven by defense spending, infrastructure monitoring, and energy sector asset surveillance.

Country Analysis

The Space Data Analytics Market concentrates in four national markets that together contribute more than 60% of 2025 global revenue: the United States, China, France, and Germany.

United States

The United States generated approximately USD 3.05 Billion in Space Data Analytics Market revenue in 2025, with a country CAGR of 21.5% through 2034. The National Reconnaissance Office (NRO) awarded multi-billion-dollar Electro-Optical Commercial Layer (EOCL) contracts to Maxar, Planet Labs, and BlackSky on five-year base terms through 2032. The National Geospatial-Intelligence Agency (NGA) Luno B IDIQ contract with USD 200 million ceiling selected Planet Labs and BlackSky as vendors. The Department of Defense Defense Innovation Unit (DIU) Hybrid Space Architecture mission drives commercial integration. NASA's Commercial Satellite Data Acquisition (CSDA) program funds geospatial procurement for civil science. Major U.S. buyers include the USDA Farm Service Agency, the U.S. Geological Survey, the National Oceanic and Atmospheric Administration (NOAA), and Fortune 500 commercial subscribers across energy, insurance, and logistics. Domestic vendors Maxar Vantor, Planet Labs, BlackSky, HawkEye 360, Capella Space, Spire Global, and L3Harris dominate.

China

China contributed approximately USD 750 Million in Space Data Analytics Market revenue in 2025, with a country CAGR of 23.0% through 2034, the fastest among major markets. The China National Space Administration (CNSA) and China Academy of Space Technology (CAST) coordinate civilian space programs. Chang Guang Satellite Technology operates the Jilin-1 constellation comprising over 100 satellites, the largest non-U.S. commercial Earth observation fleet. Spacety operates the Hisea-1 and Chaohu-1 SAR satellites. MinoSpace operates commercial optical imagery services. The 14th Five-Year Plan for Space Science and Development allocated substantial funding to commercial space operators. The Belt and Road Initiative drives international geospatial service exports to partner countries. U.S. export controls under ITAR limit cross-border technology flows, creating separate technology ecosystems. Domestic demand from natural resources, agriculture, and urban planning ministries anchors commercial revenue growth.

France

France generated approximately USD 490 Million in Space Data Analytics Market revenue in 2025, with a country CAGR of 20.2% through 2034. Airbus Defence and Space (headquartered in Leiden, Netherlands with significant French operations in Toulouse) operates the Pleiades, Pleiades Neo, SPOT, and OneAtlas geospatial platforms from France. The Centre National d'Etudes Spatiales (CNES) coordinates national space activities alongside the European Space Agency (ESA) at the Kourou launch facility in French Guiana. Airbus-Thales Alenia Space partnerships produce the Pleiades Neo 30cm constellation. The France 2030 plan committed EUR 1.5 billion to space acceleration through 2030. Major French buyers include the Ministere des Armees (defense), the Institut National de l'Information Geographique et Forestiere (IGN), and Air France-KLM for aviation applications. Airbus completed divestment of the UP42 geospatial marketplace to Neo Space Group in July 2025.

Germany

Germany contributed approximately USD 450 Million in Space Data Analytics Market revenue in 2025, with a country CAGR of 21.0% through 2034. The German Aerospace Center (DLR) operates the TerraSAR-X and TanDEM-X SAR constellation alongside coordinating the German National Space Strategy. Planet Labs Germany GmbH secured a three-year contract with DLR in September 2024 for Earth observation data and analytics for research and development. In July 2025 Planet Labs secured an additional USD 280 million contract with the German government for environmental monitoring and security imagery services. Major German players include OHB SE (Bremen-based satellite manufacturer with analytics partnerships), Constellr (hyperspectral), and Airbus Defence and Space's German operations. The German Federal Ministry for Economic Affairs and Climate Action supports commercial space through the KMU Innovativ program. Major German buyers include the Federal Office for Cartography and Geodesy (BKG) and the Federal Intelligence Service (BND).

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Service

- Data Analytics and Processing Services

- Geospatial Analytics Services

- Predictive and Prescriptive Analytics Services

- Image Processing and Interpretation Services

- Data Visualization and Reporting Services

- Artificial Intelligence and Machine Learning Analytics Services

- Consulting and Advisory Services

- Managed Analytics Services

By Vertical

- Defense and Intelligence

- Agriculture and Forestry

- Energy and Utilities

- Environmental Monitoring and Climate Research

- Transportation and Logistics

- Government and Public Sector

- Maritime

- Mining and Natural Resources

- Telecommunications

- Urban Planning and Smart Cities

- Others (Insurance, Media, Academic Research)

By End-Use

- Commercial Enterprises

- Government Agencies

- Defense Organizations

- Research Institutes and Academic Organizations

- Space Agencies

- Non-Governmental Organizations (NGOs)

- Others

By Data Type

- Earth Observation Data

- Satellite Imagery Data

- Remote Sensing Data

- Geospatial and Location-Based Data

- Synthetic Aperture Radar (SAR) Data

- Weather and Meteorological Data

- Navigation and Positioning Data

- Communication Satellite Data

- Scientific and Deep Space Mission Data

- Others (Hyperspectral and Multispectral Data)

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 7.85 B |

| Forecast Revenue (2034) | USD 43.20 B |

| CAGR (2025-2034) | 20.9% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Service, (Data Analytics and Processing Services, Geospatial Analytics Services, Predictive and Prescriptive Analytics Services, Image Processing and Interpretation Services, Data Visualization and Reporting Services, Artificial Intelligence and Machine Learning Analytics Services, Consulting and Advisory Services, Managed Analytics Services), By Vertical, (Defense and Intelligence, Agriculture and Forestry, Energy and Utilities, Environmental Monitoring and Climate Research, Transportation and Logistics, Government and Public Sector, Maritime, Mining and Natural Resources, Telecommunications, Urban Planning and Smart Cities, Others (Insurance, Media, Academic Research)), By End-Use, (Commercial Enterprises, Government Agencies, Defense Organizations, Research Institutes and Academic Organizations, Space Agencies, Non-Governmental Organizations (NGOs), Others), By Data Type, (Earth Observation Data, Satellite Imagery Data, Remote Sensing Data, Geospatial and Location-Based Data, Synthetic Aperture Radar (SAR) Data, Weather and Meteorological Data, Navigation and Positioning Data, Communication Satellite Data, Scientific and Deep Space Mission Data, Others (Hyperspectral and Multispectral Data)) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | PLANET LABS PBC, MAXAR TECHNOLOGIES (VANTOR), BLACKSKY TECHNOLOGY INC., AIRBUS DEFENCE AND SPACE, SPIRE GLOBAL, INC., ICEYE OY, HAWKEYE 360, INC., CAPELLA SPACE CORPORATION, SATELLOGIC INC., L3HARRIS TECHNOLOGIES, INC., NORTHROP GRUMMAN CORPORATION, LOCKHEED MARTIN CORPORATION, EOS DATA ANALYTICS, INC., URSA SPACE SYSTEMS INC., SYNSPECTIVE INC., UMBRA LAB, INC., CHANG GUANG SATELLITE TECHNOLOGY, IMAGESAT INTERNATIONAL N.V., E-GEOS S.P.A., NV5 GLOBAL, INC., GHGSAT INC., CONSTELLR GMBH, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Vertical (Defense, Agriculture, Energy, Environmental Monitoring, Transportation, Government), By End-Use, By Data Type, Industry Trends & Forecast 2026-2034")

, By Vertical (Defense, Agriculture, Energy, Environmental Monitoring, Transportation, Government), By End-Use, By Data Type, Industry Trends & Forecast 2026-2034")

, By Vertical (Defense, Agriculture, Energy, Environmental Monitoring, Transportation, Government), By End-Use, By Data Type, Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Space Data Analytics Market?

The Global Space Data Analytics Market was valued at USD 6.49 Billion in 2024 and is projected to reach USD 43.20 Billion by 2034, growing at a CAGR of 20.9% from 2026 to 2034. Growth is driven by increasing Earth observation satellite deployments, rising demand for geospatial intelligence, and the adoption of AI and machine learning for satellite data analysis across defense, climate monitoring, precision agriculture, disaster management, and smart infrastructure applications worldwide.

Who are the major players in the Space Data Analytics Market?

PLANET LABS PBC, MAXAR TECHNOLOGIES (VANTOR), BLACKSKY TECHNOLOGY INC., AIRBUS DEFENCE AND SPACE, SPIRE GLOBAL, INC., ICEYE OY, HAWKEYE 360, INC., CAPELLA SPACE CORPORATION, SATELLOGIC INC., L3HARRIS TECHNOLOGIES, INC., NORTHROP GRUMMAN CORPORATION, LOCKHEED MARTIN CORPORATION, EOS DATA ANALYTICS, INC., URSA SPACE SYSTEMS INC., SYNSPECTIVE INC., UMBRA LAB, INC., CHANG GUANG SATELLITE TECHNOLOGY, IMAGESAT INTERNATIONAL N.V., E-GEOS S.P.A., NV5 GLOBAL, INC., GHGSAT INC., CONSTELLR GMBH, Others

Which segments covered the Space Data Analytics Market?

By Service, (Data Analytics and Processing Services, Geospatial Analytics Services, Predictive and Prescriptive Analytics Services, Image Processing and Interpretation Services, Data Visualization and Reporting Services, Artificial Intelligence and Machine Learning Analytics Services, Consulting and Advisory Services, Managed Analytics Services), By Vertical, (Defense and Intelligence, Agriculture and Forestry, Energy and Utilities, Environmental Monitoring and Climate Research, Transportation and Logistics, Government and Public Sector, Maritime, Mining and Natural Resources, Telecommunications, Urban Planning and Smart Cities, Others (Insurance, Media, Academic Research)), By End-Use, (Commercial Enterprises, Government Agencies, Defense Organizations, Research Institutes and Academic Organizations, Space Agencies, Non-Governmental Organizations (NGOs), Others), By Data Type, (Earth Observation Data, Satellite Imagery Data, Remote Sensing Data, Geospatial and Location-Based Data, Synthetic Aperture Radar (SAR) Data, Weather and Meteorological Data, Navigation and Positioning Data, Communication Satellite Data, Scientific and Deep Space Mission Data, Others (Hyperspectral and Multispectral Data))

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date