- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Space Tourism Market Size, Share & Forecast 2034 | CAGR 53.4%

Global Space Tourism Market Size, Share, Analysis By Type (Suborbital Tourism, Orbital Tourism, Lunar Tourism, Space Station Tourism, Deep Space Tourism), By End-User (Individual Travelers, Corporate Clients, Research Institutions, Government-Sponsored Participants, Celebrity Travelers), By Sales Channel, By Customer Net Worth, Industry Trends, Market Dynamics & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

|---|---|---|---|

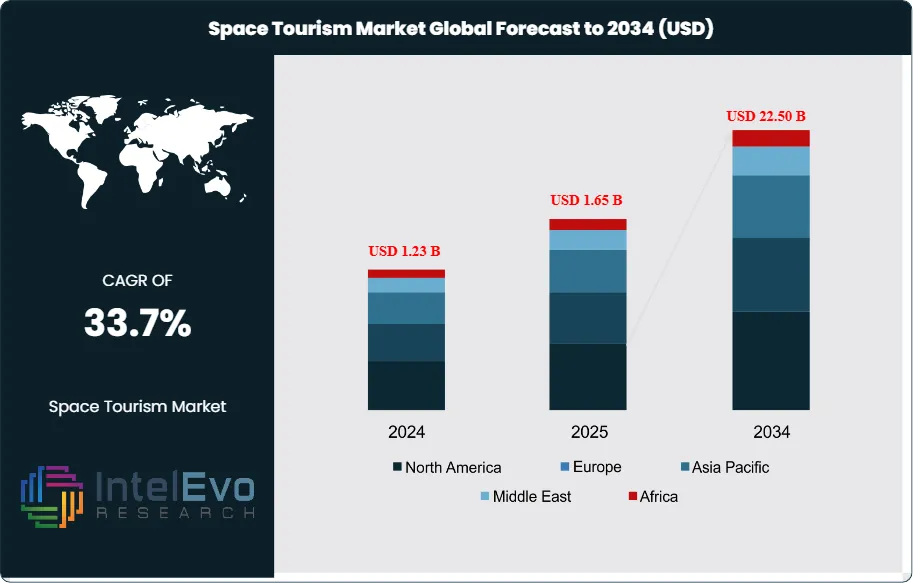

| USD 1.65 Billion | USD 22.50 Billion | 33.7% | North America, 40.4% |

The Space Tourism Market was valued at approximately USD 1.23 Billion in 2024 and reached USD 1.65 Billion in 2025. The market is projected to expand significantly to USD 22.50 Billion by 2034, growing at a robust CAGR of 33.7% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 20.85 Billion over the analysis period. Demand acceleration reflects expanding commercial flight cadence at SpaceX, Blue Origin, and Virgin Galactic, alongside Axiom Space orbital missions to the International Space Station and the entry of stratospheric balloon operators including Space Perspective and World View at lower price points.

Get More Information about this report -

Request Free Sample ReportSpaceX has consolidated leadership in orbital tourism following the September 2024 Polaris Dawn mission, which carried four private astronauts 1,400 kilometers from Earth and conducted the first commercial extravehicular activity (EVA). The April 2025 Fram2 mission flew the first crewed polar retrograde orbit, while Blue Origin completed its 15th New Shepard tourism mission (NS-36) in October 2025 with six passengers. By August 2025, SpaceX had flown approximately 14 to 20 private individuals to orbit across Inspiration4, Ax-1, Ax-2, Ax-3, and Polaris Dawn. Virgin Galactic completed seven Galactic commercial flights before pausing operations in June 2024 to develop Delta Class spacecraft for 2026 service resumption.

Regulatory transition altered the market through 2025-2026. The Federal Aviation Administration Office of Commercial Space Transportation (FAA AST) completed the full Part 450 transition on March 10, 2026, retiring legacy launch and reentry licenses under Title 14 CFR Parts 415, 417, and 431. The statutory human spaceflight regulatory moratorium (the learning period under the Commercial Space Launch Amendments Act of 2004) remains in effect until January 1, 2028, governing passenger safety under an informed-consent regime. The FAA Reauthorization Act of 2024 (P.L. 118-63) requires airspace integration upgrades by December 2026.

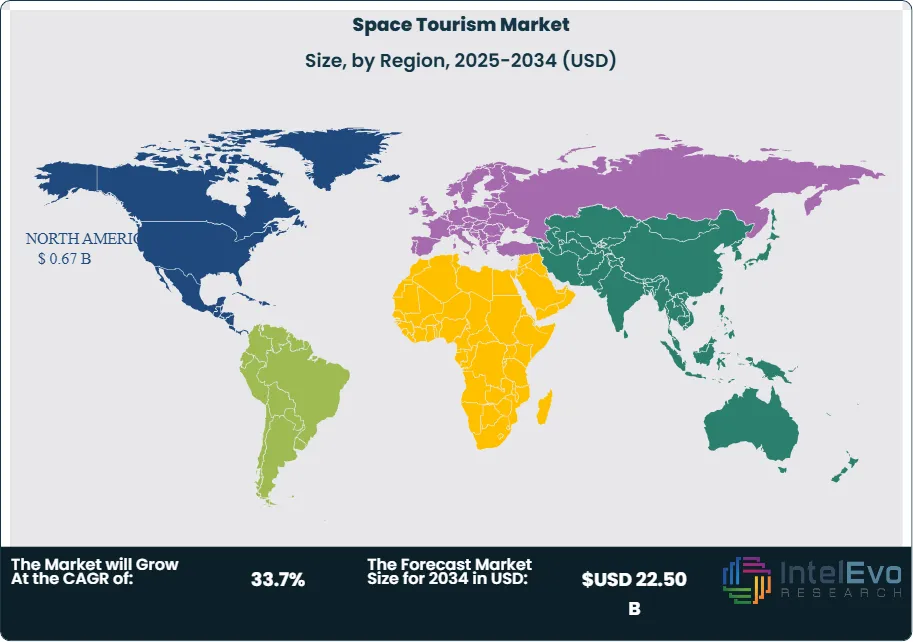

North America held the largest revenue share at 40.4% in 2025 valued at approximately USD 0.67 Billion, anchored by SpaceX, Blue Origin, Virgin Galactic, and Axiom Space launching from Kennedy Space Center, Cape Canaveral, Spaceport America, and West Texas. Asia Pacific captured 25.8% revenue share at USD 0.43 Billion, with China-based Deep Blue Aerospace announcing 1.5 billion yuan (USD 211,000) commercial spaceflight tickets for 2027 service. Sub-orbital flights captured 51.2% segment share in 2025 because lower ticket prices (USD 450,000 at Virgin Galactic versus approximately USD 50 million per Crew Dragon orbital seat) widen the addressable customer pool.

The forward outlook through 2034 hinges on three structural shifts. SpaceX Starship commercial operations targeting 100-passenger payloads at sub-million-dollar seat prices will collapse the per-seat cost curve. Axiom Space, Vast, and Sierra Space commercial space stations will replace ISS capacity post-2030 retirement. Stratospheric balloon operators including Space Perspective and World View will open the USD 50,000 to USD 125,000 price tier to ultra-high-net-worth (UHNW) individuals beyond the 22% of customers above USD 60 million net worth who currently dominate orbital seat purchases.

Market Definition & Scope

The space tourism market is defined as commercial activity providing non-professional travelers with access to spaceflight experiences for leisure, exploration, or experiential travel beyond Earth's atmosphere. The market encompasses sub-orbital missions reaching the Karman line (100 kilometers altitude), orbital spaceflight aboard Crew Dragon and successor vehicles, multi-day International Space Station stays brokered through Axiom Space and Space Adventures, future commercial space station accommodations, and adjacent stratospheric balloon experiences from Space Perspective and World View.

This analysis includes ticket revenue, mission charter fees, training programs, and pre-flight preparation services delivered to private customers. Excluded from scope are NASA and Department of Defense crew launches under federal contract, satellite launch services, cargo resupply missions to the ISS, and parabolic-flight zero-gravity experiences below 30,000 meters altitude that do not approach space. The space tourism market represents approximately 0.8% of the broader USD 200.87 Billion global space economy in 2025, signaling early-stage adoption with high forecast multiples.

, By End-User (Individual Travelers, Corporate Clients, Research Institutions, Government-Sponsored Participants, Celebrity Travelers), By Sales Channel, By Customer Net Worth, Industry Trends, Market Dynamics & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global space tourism market expands from USD 1.65 Billion in 2025 to USD 22.50 Billion by 2034, growing at a 33.7% CAGR over the forecast period.

- Segment Dominance by Type: Sub-orbital flights captured 51.2% revenue share in 2025 at approximately USD 0.85 Billion, anchored by Blue Origin New Shepard and Virgin Galactic VSS Unity ticket sales.

- Segment Dominance by End-User: Commercial private customers held 58.7% of revenue in 2025 because high-net-worth individuals represent the primary willing-to-pay buyer pool at current price tiers.

- Driver: Reusable launch vehicle economics led by SpaceX Falcon 9 (300-plus first-stage reuse cycles by May 2024) and Blue Origin New Shepard reuse have lowered marginal launch cost by an estimated 60-70% versus expendable systems.

- Restraint: Ticket prices remain prohibitive for mass adoption, with Virgin Galactic at approximately USD 450,000, SpaceX private Crew Dragon at approximately USD 50 million per seat, and Blue Origin auction seats reaching USD 28 million.

- Opportunity: Stratospheric balloon operators Space Perspective and World View targeting USD 50,000 to USD 125,000 ticket prices represent an estimated USD 3.4 Billion incremental opportunity by 2030.

- Trend: Commercial space station construction (Axiom Station, Vast Haven-1, Sierra Space Orbital Reef) targets ISS retirement-window capacity, with first habitable modules planned by 2027-2028.

- Regional: North America led with 40.4% share and USD 0.67 Billion revenue in 2025, while Asia Pacific captured 25.8% and is forecast as the fastest-growing region at a 36.8% CAGR through 2034.

Key Insights Summary

- SpaceX Polaris Dawn (September 10, 2024) flew four private astronauts to a 1,400-kilometer apogee on Crew Dragon, breaking the post-Apollo crewed altitude record set by Gemini 11 and conducting the first commercial extravehicular activity using SpaceX-developed EVA suits.

- Blue Origin completed NS-36 in October 2025, the company's 15th space tourism mission carrying six passengers on a 10-minute suborbital flight from West Texas beyond the Karman line, with NS-31 in April 2025 marking the first all-female crew including Lauren Sánchez, Katy Perry, and Gayle King.

- FAA Part 450 commercial launch and reentry regulations took full effect on March 10, 2026, retiring legacy licenses under Title 14 CFR Parts 415, 417, 431, and 435 and unifying performance-based licensing for all launch and reentry vehicles.

- The Commercial Space Launch Amendments Act of 2004 statutory learning period moratorium on FAA human spaceflight passenger-safety regulations remains in effect through January 1, 2028, with the industry operating under an informed-consent regime.

- SpaceX Falcon 9 first-stage boosters had completed 300-plus reuse cycles by May 2024, with certification underway to reuse a single booster up to 40 times, lowering marginal launch cost and supporting orbital tourism economics.

- Axiom Space has flown four private orbital missions to the International Space Station (Ax-1 through Ax-4) using SpaceX Crew Dragon, while Virgin Galactic disclosed more than 800 ticket reservations by 2022 ahead of Delta Class commercial service in 2026.

Competitive Landscape Overview

The space tourism market is moderately concentrated with the top four operators (SpaceX, Blue Origin, Virgin Galactic, and Axiom Space) accounting for an estimated combined 78% of global revenue in 2025. Competition splits along orbital and sub-orbital lines: SpaceX and Axiom Space dominate orbital missions through Crew Dragon, while Blue Origin and Virgin Galactic split sub-orbital flights. Stratospheric balloon entrants Space Perspective and World View extend the addressable market downward into the USD 50,000 to USD 125,000 price tier that rocket-based operators cannot serve at margin.

Strategic positioning is shifting through 2025-2026. Virgin Galactic paused commercial flights after Galactic 07 in June 2024 to develop Delta Class spacecraft for weekly service resumption in 2026, while SpaceX advances Starship toward 100-passenger payload capability. Blue Origin's January 2025 first launch of New Glenn (heavy-lift reusable) opens the door to lunar tourism, and Axiom Space construction of the Axiom Station modules positions the company for post-ISS commercial accommodation revenue. China's Deep Blue Aerospace targets 2027 commercial spaceflight at USD 211,000 per ticket.

Competitive Landscape Matrix

| Company Name | Headquarters | Market Position | Key Product/Solution | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| SpaceX | United States | Leader | Crew Dragon, Falcon 9, Starship orbital systems | Global, US-led | Operated Polaris Dawn (Sep 2024) and Fram2 polar orbit (Apr 2025) private missions |

| Blue Origin | United States | Leader | New Shepard suborbital, New Glenn heavy lift | North America | Completed NS-36 (15th tourism mission) in October 2025 with 6 passengers |

| Virgin Galactic | United States | Leader | VSS Unity spaceplane, Delta Class spacecraft | North America | Paused commercial flights after Galactic 07 (June 2024) for Delta Class development |

| Axiom Space | United States | Leader | Crew Dragon orbital ISS missions, Axiom Station modules | Global | Continued Ax-3 ISS mission and announced Ax-5 for 2026 |

| Space Perspective | United States | Challenger | Neptune stratospheric balloon capsule | North America | Unveiled Neptune test capsule in February 2024 ahead of 2025 commercial flights |

| Boeing | United States | Challenger | CST-100 Starliner orbital crew capsule | North America | Continuing Starliner certification testing through 2025 |

| Sierra Space | United States | Challenger | Dream Chaser spaceplane, Orbital Reef station | North America | Advanced Dream Chaser testing for ISS cargo and future crewed missions |

| World View | United States | Niche Player | Stratospheric balloon Explorer capsule | North America | Continued ticket sales at approximately USD 50,000 per seat |

| Space Adventures | United States | Niche Player | Brokered orbital missions via Roscosmos and SpaceX | Global | Maintains backlog of orbital tourism reservations including lunar flyby clients |

| Zero Gravity Corp | United States | Niche Player | G-Force One parabolic flight aircraft | North America | Expanded parabolic flight schedule across US spaceports through 2025 |

By Type

The space tourism market by type is led by sub-orbital flights, which captured 51.2% revenue share in 2025 valued at approximately USD 0.85 Billion. Sub-orbital missions dominate because lower ticket prices (Virgin Galactic at approximately USD 450,000) widen the addressable customer pool relative to orbital seats above USD 50 million. Blue Origin New Shepard completed 15 tourism missions through October 2025 with the NS-36 flight carrying six passengers, while Virgin Galactic VSS Unity flew seven Galactic commercial missions before the June 2024 service pause.

Orbital flights captured 48.8% revenue share in 2025 valued at approximately USD 0.81 Billion, dominated by SpaceX Crew Dragon missions including Inspiration4 (September 2021), Ax-1 through Ax-4, Polaris Dawn (September 2024), and Fram2 (April 2025). Multi-day orbital experiences command premium pricing because they include weightlessness exposure, Earth observation from low Earth orbit, and (in Polaris Dawn's case) extravehicular activity. Orbital is forecast at a 35.4% CAGR through 2034, slightly faster than sub-orbital at 32.1%, because Axiom Space, Vast, and Sierra Space commercial space stations will expand orbital accommodation capacity.

By End-User

Commercial private customers captured 58.7% of revenue in 2025 because high-net-worth individuals (HNWIs) represent the primary willing-to-pay buyer pool at current price tiers. The customer net-worth distribution skews to the USD 20-40 million tier (44% of buyers), USD 40-60 million (28.5%), and USD 60 million-plus (22.5%), with a small under-USD-20-million tier of 5% representing group-sponsored or charitable seats. Industry analysis indicates that Virgin Galactic disclosed more than 800 ticket reservations by 2022, validating depth of HNW demand.

Government end-users captured 28.6% revenue share in 2025 covering NASA private astronaut missions (Ax-1 through Ax-4 carried mixed government and commercial crew), training partnerships, and prestige flights from foreign space agencies. Government share is forecast to grow at a 37.5% CAGR through 2034 because international space agencies (UAE Space Agency, Saudi Space Agency, Indian Space Research Organisation) increasingly subsidize astronaut training missions on commercial vehicles. Research and other end-users including media production, scientific charter, and corporate prestige flights captured the residual 12.7%.

By Sales Channel

Launch provider direct sales captured 60.0% of revenue in 2025 because SpaceX, Blue Origin, and Virgin Galactic operate one-stop services from booking through training and flight. Direct channels eliminate intermediary commissions and let providers control the customer experience, particularly important at six-figure-and-above ticket prices where buyer expectations include personal vendor contact. Third-party partnerships captured 28.5% covering specialty operators including Space Adventures (broker for Roscosmos and SpaceX seats) and Axiom Space (broker for Crew Dragon ISS missions).

Travel and specialty agency channels captured 11.5% of revenue in 2025 covering luxury travel operators including Virtuoso, Black Tomato, and Tumlare that bundle space tourism into broader high-end travel itineraries. Third-party partnerships are forecast as the fastest-growing sales channel at a 38.7% CAGR through 2034 because operator partnerships with Marriott Bonvoy, Four Seasons, and Aman Resorts are bundling pre-flight luxury accommodation with launch tickets, creating higher attach rates per qualified buyer.

By Customer Net Worth

The USD 20 million to USD 40 million net-worth tier captured 44.0% of buyer share in 2025 because this customer band balances price elasticity with discretionary spending capacity sufficient for sub-orbital tickets. The USD 40 million to USD 60 million tier held 28.5% share, while the USD 60 million-plus ultra-high-net-worth (UHNW) tier captured 22.5% and dominates orbital seat purchases including Polaris Dawn and Axiom Space ISS missions. The under-USD-20-million tier accounted for the residual 5%, primarily through group-sponsored seats and charity auctions including the 2021 Blue Origin inaugural seat at USD 28 million.

Regional Analysis

North America

The global space tourism market spans five regions with sharply different operator footprints. North America held the largest 2025 share at 40.4%, valued at approximately USD 0.67 Billion. The United States anchored regional revenue through SpaceX launches from Kennedy Space Center LC-39A, Blue Origin operations at West Texas Launch Site One, and Virgin Galactic flights from Spaceport America in New Mexico. NASA Commercial Crew and Commercial Lunar Payload Services programs provide approximately USD 3 billion in five-year funding support. Canada contributes through Canadian Space Agency astronaut training partnerships.

Asia Pacific

Asia Pacific captured 25.8% revenue share in 2025 valued at approximately USD 0.43 Billion, and is forecast as the fastest-growing region at a 36.8% CAGR through 2034. China leads regional activity through Deep Blue Aerospace's announced 1.5 billion yuan (USD 211,000) commercial spaceflight tickets for 2027 service, alongside CAS Space and Galactic Energy reusable rocket development. Japan supports space tourism through MEXT and JAXA partnerships, with Yusaku Maezawa's dearMoon program (Starship-based lunar flyby) adding regional visibility. India's Indian Space Research Organisation (ISRO) Gaganyaan program may extend to commercial human spaceflight by 2030.

Europe

Europe represented 22.6% revenue share in 2025 valued at approximately USD 0.37 Billion. The European Space Agency (ESA), German Aerospace Center (DLR), and French CNES drive astronaut training partnerships rather than direct commercial operations, but European HNWIs purchase US-operator tickets at high rates. The United Kingdom Space Agency licensed Spaceport Cornwall for sub-orbital operations, while Sweden's Esrange Space Center hosts test campaigns. The EU Space Strategy for Security and Defence (March 2023) and the EU Space Act provide regulatory baselines applicable to space tourism by 2027.

Middle East and Africa

Middle East and Africa held 7.4% revenue share in 2025 valued at approximately USD 0.12 Billion. Saudi Arabia's Vision 2030 Saudi Space Agency has funded astronaut training and a 2023 Ax-2 mission seat for Rayyanah Barnawi (first Saudi woman in space) and Ali AlQarni. The UAE Space Agency operates a similar prestige-mission program through MBRSC, with Hazza Al Mansouri having flown to the ISS via Soyuz. Israel hosts academic and prestige programs including the Eytan Stibbe Ax-1 mission.

Latin America

Latin America captured 3.8% revenue share in 2025 valued at approximately USD 0.06 Billion. Brazil's HNW population purchases Virgin Galactic and Blue Origin seats at growing rates, and Mexico-based operators including Saltillo aerospace cluster vendors are evaluating sub-orbital tourism partnerships. Argentina's CONAE provides academic launch infrastructure rather than commercial spaceflight.

Country Analysis

United States

The United States space tourism market reached approximately USD 0.59 Billion in 2025, growing at a country-specific CAGR of 33.4% through 2034. Federal demand traces to FAA AST Part 450 licensing fully effective March 10, 2026, the statutory learning period moratorium under the Commercial Space Launch Amendments Act of 2004 (in effect through January 1, 2028), and NASA Commercial Crew funding of approximately USD 3 billion across five years. SpaceX, Blue Origin, Virgin Galactic, Axiom Space, Sierra Space, and Space Perspective collectively operated US flight cadence supporting more than 60 private astronauts to space across 2024-2025.

China

China generated approximately USD 0.18 Billion in 2025 space tourism revenue, growing at a country CAGR of 39.2% through 2034 (the highest single-country rate globally). The China National Space Administration (CNSA) and Ministry of Industry and Information Technology support reusable rocket development through Deep Blue Aerospace, CAS Space, Galactic Energy, and Orienspace. Deep Blue Aerospace announced 1.5 billion yuan (approximately USD 211,000) commercial spaceflight tickets for 2027 service in October 2024. Government support for commercial human spaceflight aligns with China Manned Space Engineering Office strategic priorities.

United Arab Emirates

The United Arab Emirates recorded approximately USD 0.05 Billion in 2025 space tourism revenue with a country CAGR of 35.7% through 2034. The UAE Space Agency and Mohammed bin Rashid Space Centre (MBRSC) drive prestige astronaut programs including Hazza Al Mansouri's 2019 Soyuz ISS mission and Sultan Al Neyadi's 2023 SpaceX Crew-6 mission. The UAE National Space Strategy 2030 and Dubai Vision 2050 fund sub-orbital flight pilots and tourism infrastructure development at the Mohammed bin Rashid Aerospace Hub.

United Kingdom

The United Kingdom generated approximately USD 0.04 Billion in 2025 space tourism revenue, with a country CAGR of 28.4% through 2034. The UK Space Agency licensed Spaceport Cornwall for sub-orbital operations and supports Cornwall, SaxaVord, and Sutherland spaceport development under the Space Industry Act 2018 and the Space Industry Regulations 2021. Sub-orbital flight from UK spaceports remains in pre-commercial pilot phase, with Virgin Orbit's January 2023 satellite launch failure delaying horizontal-launch tourism timelines. UK HNW customer purchases on US-based operators continue through Space Adventures and Virtuoso channels.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Type

- Suborbital Tourism

- Orbital Tourism

- Lunar Tourism

- Space Station Tourism

- Deep Space Tourism

By End-User

- Individual Travelers

- Corporate Clients

- Research and Educational Institutions

- Government-Sponsored Participants

- Celebrity and Influencer Participants

- Adventure Travel Enthusiasts

- Others

By Sales Channel

- Direct Sales

- Online Booking Platforms

- Travel Agencies and Tour Operators

- Luxury Travel Concierge Services

- Corporate Partnerships and Institutional Agreements

- Authorized Space Tourism Brokers

By Customer Net Worth

- High-Net-Worth Individuals (HNWIs) (USD 1 Million–USD 5 Million)

- Very-High-Net-Worth Individuals (VHNWIs) (USD 5 Million–USD 30 Million)

- Ultra-High-Net-Worth Individuals (UHNWIs) (Above USD 30 Million)

- Billionaires and Ultra-Elite Customers

- Affluent Consumers and Early Adopters

- Institutional and Sponsored Customers

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 1.65 B |

| Forecast Revenue (2034) | USD 22.50 B |

| CAGR (2025-2034) | 33.7% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Type, (Suborbital Tourism, Orbital Tourism, Lunar Tourism, Space Station Tourism, Deep Space Tourism), By End-User, (Individual Travelers, Corporate Clients, Research and Educational Institutions, Government-Sponsored Participants, Celebrity and Influencer Participants, Adventure Travel Enthusiasts, Others), By Sales Channel, (Direct Sales, Online Booking Platforms, Travel Agencies and Tour Operators, Luxury Travel Concierge Services, Corporate Partnerships and Institutional Agreements, Authorized Space Tourism Brokers), By Customer Net Worth, (High-Net-Worth Individuals (HNWIs) (USD 1 Million–USD 5 Million), Very-High-Net-Worth Individuals (VHNWIs) (USD 5 Million–USD 30 Million), Ultra-High-Net-Worth Individuals (UHNWIs) (Above USD 30 Million), Billionaires and Ultra-Elite Customers, Affluent Consumers and Early Adopters, Institutional and Sponsored Customers), |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | SPACEX, BLUE ORIGIN, VIRGIN GALACTIC, AXIOM SPACE, SPACE PERSPECTIVE, BOEING, SIERRA SPACE, WORLD VIEW ENTERPRISES, SPACE ADVENTURES, ZERO GRAVITY CORP, VAST SPACE, DEEP BLUE AEROSPACE, ROCKET LAB USA, AIRBUS, ZERO 2 INFINITY, ORBITE, PD AEROSPACE, BLUE ABYSS, STARCHASER INDUSTRIES, SPACE ISLAND GROUP, OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By End-User (Individual Travelers, Corporate Clients, Research Institutions, Government-Sponsored Participants, Celebrity Travelers), By Sales Channel, By Customer Net Worth, Industry Trends, Market Dynamics & Forecast 2026-2034")

, By End-User (Individual Travelers, Corporate Clients, Research Institutions, Government-Sponsored Participants, Celebrity Travelers), By Sales Channel, By Customer Net Worth, Industry Trends, Market Dynamics & Forecast 2026-2034")

, By End-User (Individual Travelers, Corporate Clients, Research Institutions, Government-Sponsored Participants, Celebrity Travelers), By Sales Channel, By Customer Net Worth, Industry Trends, Market Dynamics & Forecast 2026-2034")

Frequently Asked Questions

How big is the Space Tourism Market?

The Global Space Tourism Market was valued at USD 1.23 Billion in 2024 and is projected to reach USD 22.50 Billion by 2034, growing at a CAGR of 33.7% from 2026 to 2034. Growth is driven by reusable launch technologies, rising private space investments, increasing demand for luxury experiential travel, and the emergence of commercial space stations, orbital tourism, and next-generation human spaceflight experiences across the expanding global space economy.

Who are the major players in the Space Tourism Market?

SPACEX, BLUE ORIGIN, VIRGIN GALACTIC, AXIOM SPACE, SPACE PERSPECTIVE, BOEING, SIERRA SPACE, WORLD VIEW ENTERPRISES, SPACE ADVENTURES, ZERO GRAVITY CORP, VAST SPACE, DEEP BLUE AEROSPACE, ROCKET LAB USA, AIRBUS, ZERO 2 INFINITY, ORBITE, PD AEROSPACE, BLUE ABYSS, STARCHASER INDUSTRIES, SPACE ISLAND GROUP, OTHERS

Which segments covered the Space Tourism Market?

By Type, (Suborbital Tourism, Orbital Tourism, Lunar Tourism, Space Station Tourism, Deep Space Tourism), By End-User, (Individual Travelers, Corporate Clients, Research and Educational Institutions, Government-Sponsored Participants, Celebrity and Influencer Participants, Adventure Travel Enthusiasts, Others), By Sales Channel, (Direct Sales, Online Booking Platforms, Travel Agencies and Tour Operators, Luxury Travel Concierge Services, Corporate Partnerships and Institutional Agreements, Authorized Space Tourism Brokers), By Customer Net Worth, (High-Net-Worth Individuals (HNWIs) (USD 1 Million–USD 5 Million), Very-High-Net-Worth Individuals (VHNWIs) (USD 5 Million–USD 30 Million), Ultra-High-Net-Worth Individuals (UHNWIs) (Above USD 30 Million), Billionaires and Ultra-Elite Customers, Affluent Consumers and Early Adopters, Institutional and Sponsored Customers),

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date