- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Specialty Gas Market Size, Share & Forecast 2034 | 7.2% CAGR

Global Specialty Gas Market Size, Share, Analysis Report By Product (Noble Gases, Halogen Gases, Ultra-high Purity Gases, Carbon Gases, Others), End-user (Healthcare, Manufacturing, Chemicals, Electronics and Semiconductors, Automotive, Food and Beverage, Others), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034

Report Overview:

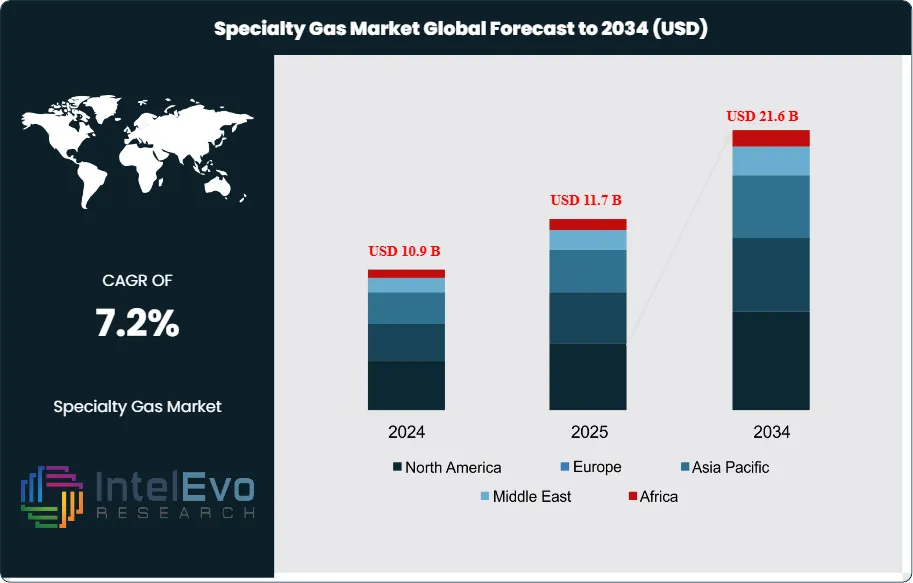

The Specialty Gas Market size is projected to reach USD 21.6 billion by 2034, up from USD 10.9 billion in 2024, growing at a CAGR of 7.2% during the forecast period from 2025 to 2034. Driven by rising demand across semiconductors, healthcare, renewable energy, and manufacturing industries, the market is witnessing strong expansion worldwide. Continuous advancements in gas purification and handling technologies are also propelling market innovation. As industries prioritize high-purity and eco-efficient gases, the specialty gas market is set to play a crucial role in shaping next-generation industrial ecosystems.

Get More Information about this report -

Request Free Sample ReportSpecialty gas refers to a category of gases that are produced with high levels of purity and are often tailored for specific applications requiring precise composition and consistency. Unlike bulk industrial gases, specialty gases are typically used in smaller quantities and are essential in industries such as healthcare, electronics, environmental monitoring, and scientific research. These gases may be either pure (like high-purity helium or nitrogen) or custom gas mixtures designed to meet exact specifications for tasks like instrument calibration, semiconductor manufacturing, or medical diagnostics. Due to their critical role in highly sensitive processes, specialty gases must adhere to stringent quality and regulatory standards, ensuring reliability and accuracy in their respective applications.

The specialty gas market is witnessing strong and sustained growth, driven by technological advancements, industrial expansion, and the rising demand for high-purity gases across multiple sectors. Specialty gases, which include rare gases, high-purity gases, and gas mixtures, are critical in applications that require precision, safety, and purity, such as electronics, healthcare, energy, and environmental monitoring.

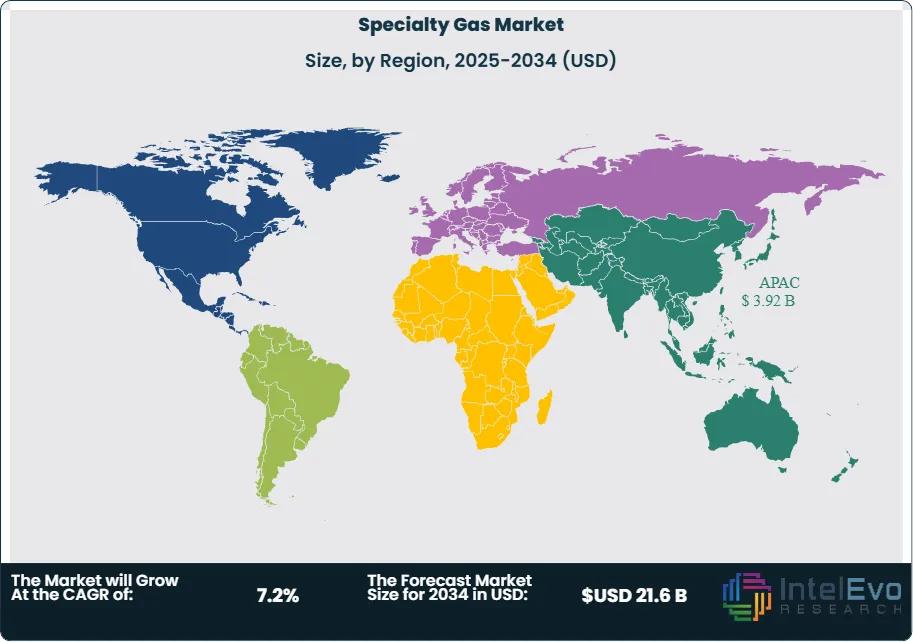

Asia Pacific's specialty gas market is growing rapidly, led by strong demand from electronics, healthcare, and industrial sectors. Countries like China and South Korea use specialty gases extensively in semiconductor and display manufacturing. Additionally, India's expanding healthcare infrastructure and Japan's focus on clean energy and environmental monitoring contribute to increased usage. Government support, technological advancements, and rising industrialization make Asia Pacific the largest and fastest-growing regional market for specialty gases.

The COVID-19 pandemic had a mixed impact on the specialty gas market. Initially, global lockdowns disrupted supply chains and reduced industrial demand, particularly in automotive and manufacturing sectors. However, the healthcare segment saw a surge in demand for medical-grade gases like oxygen and nitrous oxide, used in ventilators and critical care. Additionally, the pharmaceutical industry ramped up production and research activities, boosting the use of high-purity gases. As economies recovered, the demand rebounded across sectors, driving growth in electronics, healthcare, and environmental monitoring, solidifying the role of specialty gases in essential applications.

, End-user (Healthcare, Manufacturing, Chemicals, Electronics and Semiconductors, Automotive, Food and Beverage, Others), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

Key Takeaways:

- Market Growth: The specialty gas market is expected to reach USD 21.6 billion by 2034, growing at a robust CAGR of 7.2%, indicating strong market expansion.

- Product Segment Dominance: The product segment is dominated by ultra-high purity gases, accounting for over 27% of the market share. Specialty gases are crucial in industries like semiconductors and pharmaceuticals, where ultra-high purity is essential. In semiconductor manufacturing, these gases are used for processes like etching, deposition, and wafer cleaning, ensuring electronic components remain free from contamination. In pharmaceuticals, they maintain sterile environments during drug production, ensuring the quality and efficacy of medicines. The demand for these high-purity gases is driven by the need for contamination-free environments to uphold the highest standards of quality, safety, and efficiency in both industries.

- End-user Segment Insights: Electronics and semiconductors is anticipated to hold the largest market share. The semiconductor sector relies on ultra-high purity specialty gases for key processes such as etching, deposition, and lithography. These processes require precise control to ensure the production of high-quality, reliable electronic components. The need for contamination-free gases highlights the critical importance of specialty gases in achieving the required standards for semiconductor manufacturing.

- Driver: Rising demand from the electronics and semiconductor industry is driving the specialty gas market, as these gases are vital for chip manufacturing and advanced electronic applications.

- Restraint: The specialty gas market faces restraints due to high production and handling costs, stringent regulatory compliance for storage and transportation, and a lack of skilled professionals to handle specialized gas systems. These factors contribute to increased costs and operational challenges, limiting market growth, especially in emerging regions.

- Opportunity: The specialty gas market is poised for growth, particularly in the healthcare sector. With an aging population and improved healthcare services globally, the demand for medical gases like oxygen, nitrous oxide, and carbon dioxide is increasing. These gases are vital for patient care, anesthesia, and sterilization, driving growth due to more surgical procedures, emergency care, and home healthcare services.

- Trend: A key trend in the specialty gas market is the growing integration of digital technologies into gas management and distribution. With industries aiming for higher efficiency and precision, the use of advanced digital solutions is increasing. The adoption of Internet of Things (IoT) technology in specialty gas cylinders allows for real-time tracking of gas levels, usage, and location. This technology enhances operational efficiency and safety by providing accurate data on gas conditions, detecting irregularities such as leaks, and alerting managers to potential issues.

- Regional Analysis: Asia Pacific dominates the specialty gas market due to rapid industrial growth, especially in electronics, healthcare, and manufacturing. Countries like China, Japan, South Korea, and India lead in demand, driven by semiconductor production, medical advancements, and environmental monitoring. Rising investments, stringent regulations, and expanding industrial applications continue to propel market growth across the region.

Product Analysis:

The product segment is divided into noble gases, halogen gases, ultra-high purity gases, carbon gases, and others. The ultra-high purity gases segment dominated the market, with a market share of around 27% accounting for 2.8 billion 2024. Specialty gases are indispensable in industries like semiconductors and pharmaceuticals, where ultra-high purity is paramount. In semiconductor manufacturing, these gases are used in processes such as etching, deposition, and cleaning of silicon wafers. Even the smallest contamination can significantly impact the performance and reliability of electronic components. Similarly, in the pharmaceutical sector, these gases are employed in the production of drugs, ensuring that the environment remains sterile and free from any contaminants that could affect the quality and efficacy of medicines. The demand for these high-purity gases is driven by the need for contamination-free environments that are crucial to both industries. The precision required in manufacturing and drug formulation makes the use of these gases essential in maintaining the highest standards of quality, safety, and efficiency.

End-user Analysis:

The end-user segment is divided into healthcare, manufacturing, chemicals, electronics and semiconductors, automotive, food and beverage, and others. The electronics and semiconductors segment dominated the market, with a market share of around 20% accounting for 2.0 billion 2024. The semiconductor industry depends heavily on ultra-high purity (UHP) gases to ensure precision and quality in the manufacturing of integrated circuits and electronic components. These gases are crucial in processes such as etching, deposition, and lithography, which require extremely high purity to prevent contamination and maintain the integrity of the semiconductor wafers. In etching, gases like chlorine and hydrogen chloride are used to carve intricate patterns on the wafer, and any impurities can compromise the process. Similarly, in deposition, gases like silane are used to deposit thin layers of materials onto the wafer, where purity is essential to avoid defects. Lithography, which involves printing circuit patterns on the water's surface, also relies on ultra-pure gases like ozone and nitrogen to maintain optimal conditions. Even the smallest impurity can result in defects, affecting the quality and functionality of the final product. As semiconductor technologies advance, requiring smaller chips and more complex circuits, the demand for even higher purity gases has increased. With growing applications in fields like artificial intelligence, 5G, and autonomous vehicles, the need for precision and high-performance semiconductors continues to drive the requirement for ultra-pure specialty gases in the industry.

Region Analysis:

Asia-Pacific Leads With 36% Market Share in the Specialty Gas Market, Asia Pacific holds a dominant position in the global specialty gas market, driven by rapid industrialization, robust electronics manufacturing, and expanding healthcare infrastructure. Countries like China, Japan, South Korea, and India are at the forefront of this growth due to their strong presence in semiconductor production, pharmaceutical research, and environmental monitoring. China is the largest consumer and producer of specialty gases in the region, fueled by its massive electronics and automotive industries. Similarly, Japan and South Korea are key players in advanced technology and semiconductor manufacturing, both of which rely heavily on high-purity gases for processes like etching and deposition. India’s growing industrial base and investment in healthcare facilities have also increased the demand for medical and industrial specialty gases. Moreover, the region is witnessing rising awareness and regulatory pressure related to emissions and environmental safety, prompting greater adoption of calibration and specialty gases for monitoring and compliance.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Type

- High-Purity Gases

- Noble Gases (Helium, Argon, Neon, Krypton, Xenon)

- Carbon Gases (Carbon Dioxide, Carbon Monoxide)

- Halogen Gases (Chlorine, Fluorine)

- Specialty Acetylene and Hydrogen

- Other Specialty Gases

By End User

- Manufacturing Industries

- Laboratories & Research Institutions

- Hospitals & Healthcare Facilities

- Energy Companies

- Electronics Manufacturers

By Distribution Channel

- Direct Sales

- Distributors and Dealers

- Online Platforms

By Application

- Electronics & Semiconductors

- Healthcare & Biotechnology

- Chemicals & Petrochemicals

- Automotive & Aerospace

- Food & Beverages

- Energy & Power

- Others (Metallurgy, Environmental Testing)

By Region

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 11.7 B |

| Forecast Revenue (2034) | USD 21.6 B |

| CAGR (2025-2034) | 7.2% |

| Historical data | 2018-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Type (High-Purity Gases, Noble Gases (Helium, Argon, Neon, Krypton, Xenon), Carbon Gases (Carbon Dioxide, Carbon Monoxide), Halogen Gases (Chlorine, Fluorine), Specialty Acetylene and Hydrogen, Other Specialty Gases), By End User (Manufacturing Industries, Laboratories & Research Institutions, Hospitals & Healthcare Facilities, Energy Companies, Electronics Manufacturers), By Distribution Channel (Direct Sales, Distributors and Dealers, Online Platforms), By Application (Electronics & Semiconductors, Healthcare & Biotechnology, Chemicals & Petrochemicals, Automotive & Aerospace, Food & Beverages, Energy & Power, Others (Metallurgy, Environmental Testing)) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Air Products and Chemicals Inc., ILMO Products Company, Linde plc, Messer Group GmbH, Norco Inc., Taiyo Nippon Sanso Corporation, YUEYANG KAIMEITE ELECTRONIC AND SPECIALTY RARE GASES CO., Air Liquide, Coregas, Iwatani Corporation of America, MESA Specialty Gases & Equipment, Mitsui Chemicals Inc., Showa Denko K.K., Weldstar, Airgas Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, End-user (Healthcare, Manufacturing, Chemicals, Electronics and Semiconductors, Automotive, Food and Beverage, Others), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

, End-user (Healthcare, Manufacturing, Chemicals, Electronics and Semiconductors, Automotive, Food and Beverage, Others), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

, End-user (Healthcare, Manufacturing, Chemicals, Electronics and Semiconductors, Automotive, Food and Beverage, Others), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date