- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Speech Generating Devices Market Size, Trends, Share|CAGR of 11.81%

Global Speech Generating Devices Market Size, Share & Analysis Report by Product Type (Synthesized Speech Devices, Text-to-Speech Devices, Picture Communicators), Device Type (Fixed Display, Dynamic Display), Distribution Channel (Medical Supply Stores, Online Stores), End User (Hospitals, Clinics, Academic & Research Institutes), Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025–2034

Report Overview

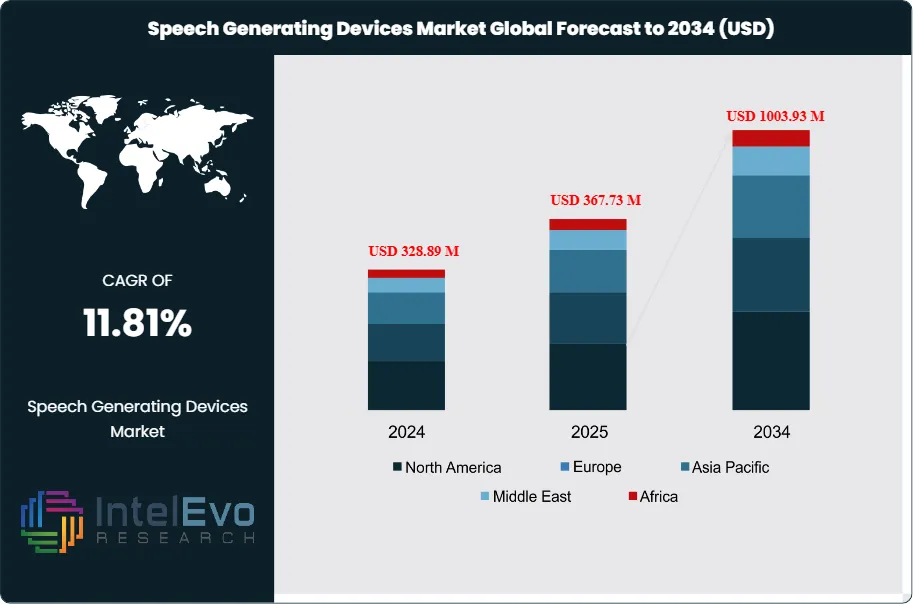

The Speech Generating Devices Market size is expected to be worth around USD 1003.93 Million by 2034, from USD 328.89 Million in 2024, growing at a CAGR of 11.81% during the forecast period from 2024 to 2034. The Speech Generating Devices (SGD) market encompasses electronic devices that enable users with speech impairments to communicate by generating voice output. The market size was valued between USD 282.7-291.09 million in 2024, with projections reaching USD 583.35 million to USD 1,013.9 million by 2033-2034, depending on various growth scenarios and technological adoption rates. These devices serve as vital communication aids for individuals with conditions such as autism spectrum disorder, cerebral palsy, amyotrophic lateral sclerosis (ALS), and acquired brain injuries.

Get More Information about this report -

Request Free Sample ReportThe SGD market is experiencing robust growth driven by increasing awareness of assistive technologies and rising incidence of neurological disorders. Technological advancements are leading to the development of innovative speech generating devices, with portable and user-friendly devices gaining significant traction. The integration of artificial intelligence and machine learning capabilities has enhanced the functionality and user experience of modern SGDs, making them more accessible to diverse user populations.

North America leads the SGD market in 2024, driven by significant healthcare investments, strong demand for dedicated speech generation devices, and a well-established distribution network. East Asia is estimated to capture significant share of the global speech generating device market share in 2024, representing a significant growth opportunity driven by increasing healthcare awareness and technological adoption.

The COVID-19 pandemic initially disrupted manufacturing and supply chains but ultimately accelerated the adoption of digital health solutions. Remote therapy sessions and telehealth services increased demand for portable and user-friendly SGDs that could be effectively used in home settings, leading to innovation in cloud-based and mobile-compatible devices.

Global supply chain disruptions have affected component availability and manufacturing costs, particularly impacting the production of advanced electronic components essential for SGD functionality. However, this has also encouraged regional manufacturing initiatives and diversification of supply chains, potentially benefiting local markets in the long term.

, Device Type (Fixed Display, Dynamic Display), Distribution Channel (Medical Supply Stores, Online Stores), End User (Hospitals, Clinics, Academic & Research Institutes), Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025–2034")

Key Takeaways

- Market Growth: The Speech Generating Devices Market is expected to reach USD 1003.93 Million by 2034, propelled by increasing awareness of communication disorders, rising prevalence of autism and neurological conditions, and technological advancements in AI-powered speech synthesis.

- Product Type Dominance: Speech Generating Text-to-Speech Devices lead due to advanced AI integration and customization capabilities.

- Device Type Dominance: Fixed Display Devices dominate, driven by cost-effectiveness and user familiarity.

- Distribution Channel Dominance: Online Stores hold a leading position, owing to convenience and accessibility.

- End User Dominance: Hospitals dominate the SGD end-user market due to high patient volumes and established clinical expertise in device selection and implementation.

- Driver: Rising autism prevalence awareness and technological advancements in AI-powered speech synthesis are accelerating market growth through improved accessibility and communication outcomes.

- Restraint: High device costs and limited insurance coverage create barriers, particularly for individuals and families without comprehensive healthcare benefits.

- Opportunity: Emerging markets expansion and integration of AI/machine learning technologies offer significant growth potential through improved affordability and enhanced communication capabilities.

- Trend: Personalization through AI and cloud-based solutions are transforming the market by enabling customized communication experiences and remote therapy delivery.

- Regional Analysis: North America leads owing to advanced healthcare infrastructure and strong reimbursement policies. Asia-Pacific regions show high promise due to increasing healthcare awareness and growing elderly population.

Product Type Analysis:

Speech Generating Text-to-Speech Devices dominate the market through their sophisticated artificial intelligence integration that delivers highly natural communication experiences for users with speech impairments. These advanced systems leverage machine learning algorithms to provide personalized voice synthesis that closely mimics natural speech patterns, enabling more authentic social interactions and improved quality of life for users. The customizable voice options allow individuals to select or even preserve their own voice characteristics through voice banking technology, maintaining personal identity in communication. AI-powered features include contextual understanding, predictive text capabilities, and adaptive learning that improves communication efficiency over time.

Device Type Analysis:

Fixed display devices maintain market leadership through their established reliability and cost-effectiveness, providing users with consistent, predictable interface experiences that have proven successful over time. Their dominance reflects the comfort level that existing users, caregivers, and clinicians have developed with familiar interface designs that require minimal learning curves and offer dependable performance. However, dynamic display devices are experiencing significant growth momentum as they deliver enhanced flexibility and adaptability for diverse communication needs. These advanced systems can modify their interface layouts, vocabulary sets, and communication options based on specific contexts, user preferences, and evolving requirements.

Distribution Channel Analysis:

Distribution channel analysis reveals a transformative shift in SGD accessibility through evolving purchasing pathways that reflect changing consumer behaviors and technological adoption. Online platforms have emerged as significant distribution channels, offering enhanced convenience through comprehensive product comparison tools, detailed specifications, and competitive pricing structures that appeal to cost-conscious consumers and caregivers. These digital channels provide accessibility advantages for users in remote locations and enable informed decision-making through user reviews and educational resources. Traditional medical supply stores continue to play crucial roles, particularly in institutional procurement processes where professional consultation and hands-on evaluation are essential. These established channels offer specialized expertise, device trials, insurance navigation support, and ongoing technical assistance that remain valuable for complex device selection decisions.

End User Analysis:

Hospitals dominate as primary end-users due to their comprehensive patient volumes, well-established procurement frameworks, and clinical specialists who possess the expertise necessary for appropriate device selection and implementation strategies. These facilities benefit from dedicated speech-language pathology departments and multidisciplinary teams that can effectively assess patient needs and coordinate device integration into treatment plans. Clinics serve as essential secondary markets, functioning as primary contact points for ongoing therapeutic support, device training, and long-term user education. Academic and research institutions represent a vital market segment focused on advancing SGD technology through research initiatives, device development programs, and professional training that prepares future clinicians and researchers in assistive technology implementation and innovation.

Region Analysis:

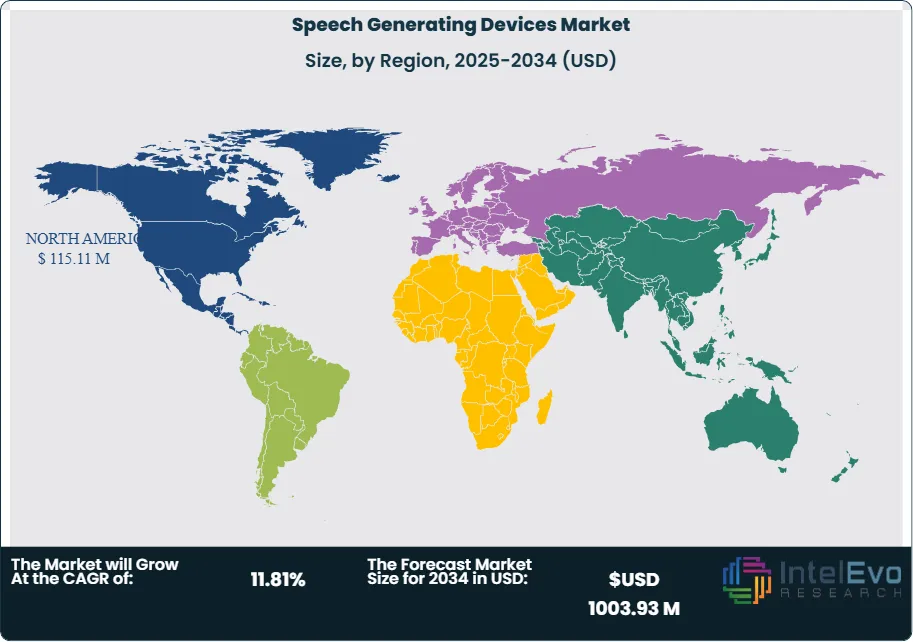

North America Leads With 35% Market Share In Speech Generating Devices Market. North America leads the SGD market, driven by significant healthcare investments, strong demand for dedicated speech generation devices, and a well-established distribution network. The United States specifically represents the largest single-country market, benefiting from comprehensive healthcare infrastructure, favorable reimbursement policies, and high awareness of assistive technologies among healthcare providers and families.

Asia-Pacific represents a significant growth opportunity, fueled by rapidly aging populations, increasing healthcare expenditure, and growing awareness of assistive technologies. Countries like Japan and South Korea are leading adoption due to advanced technology infrastructure and government support for accessibility initiatives.

Europe maintains a substantial market presence, particularly in countries with strong social healthcare systems that provide coverage for assistive devices. The region's focus on inclusive education and workplace accessibility drives consistent demand.

Emerging markets in Latin America, Middle East & Africa show promising growth potential, though adoption rates remain limited by economic factors and healthcare infrastructure development. These regions are expected to experience accelerated growth as economic conditions improve and awareness of SGD benefits increases among healthcare professionals and communities.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

Product Type

- Speech Generating Synthesized Speech Devices

- Speech Generating Text-to-Speech Devices

- Speech Generating Picture Communicators

Device Type

- Fixed Display Devices

- Dynamic Display Devices

Distribution Channel

- Medical Supply Stores

- Online Stores

- Other Channels

End User

- Hospitals

- Clinics

- Academic and Research Institutes

Region:

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 367.73 M |

| Forecast Revenue (2034) | USD 1003.93 M |

| CAGR (2025-2034) | 11.81% |

| Historical data | 2018-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | Product Type (Speech Generating Synthesized Speech Devices, Speech Generating Text-to-Speech Devices, Speech Generating Picture Communicators); Device Type (Fixed Display Devices, Dynamic Display Devices); Distribution Channel (Medical Supply Stores, Online Stores, Other Channels); End User (Hospitals, Clinics, Academic and Research Institutes) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Tobii Dynavox, PRC-Saltillo, Lingraphica , AssistiveWare (Proloquo2Go), Smartbox Assistive Technology, Jabbla, AbleNet, Compass by Komp, Therapy Box, Liberator Ltd., Saztec International, Enabling Devices, Abilia Toby Churchill, Saltillo Corporation |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, Device Type (Fixed Display, Dynamic Display), Distribution Channel (Medical Supply Stores, Online Stores), End User (Hospitals, Clinics, Academic & Research Institutes), Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025–2034")

, Device Type (Fixed Display, Dynamic Display), Distribution Channel (Medical Supply Stores, Online Stores), End User (Hospitals, Clinics, Academic & Research Institutes), Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025–2034")

, Device Type (Fixed Display, Dynamic Display), Distribution Channel (Medical Supply Stores, Online Stores), End User (Hospitals, Clinics, Academic & Research Institutes), Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025–2034")

Select Licence Type

Connect with our sales team

Speech Generating Devices Market

Published Date : 23 Jul 2025 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date