- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Stablecoin Payment Infrastructure Market Size, Share | CAGR 23.8%

Global Stablecoin Payment Infrastructure Market Size, Share, Growth Analysis By Component (Infrastructure Software, Orchestration Middleware, Custody & Key Management, Compliance & Analytics Modules), By Stablecoin Type (Fiat-Collateralized, Crypto-Collateralized, Algorithmic, CBDC-Linked), By Application (Cross-Border Payments, Merchant Acceptance, DeFi Settlement, Treasury Management), Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

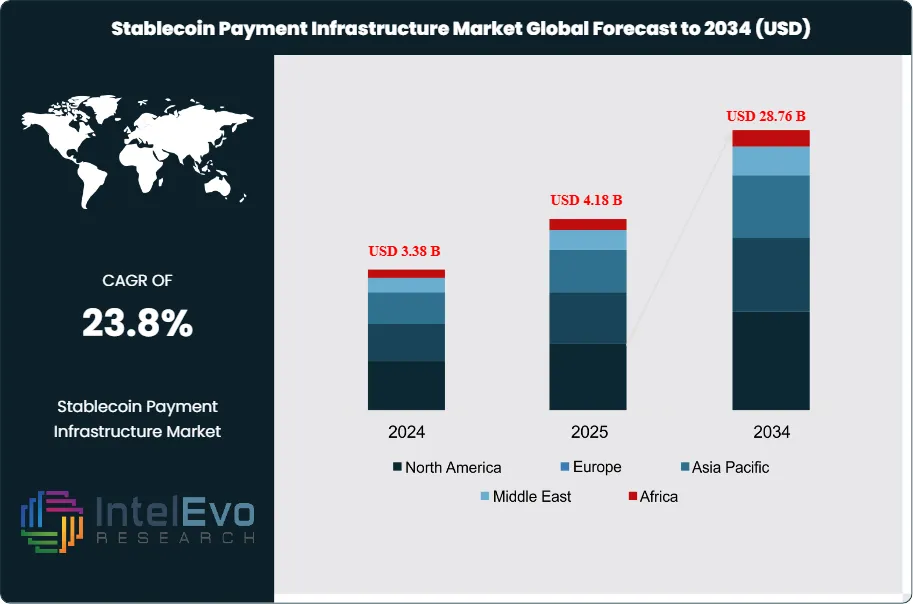

| USD 4.18 Billion | USD 28.76 Billion | 23.8% | North America, 39.4% |

The Stablecoin Payment Infrastructure Market was valued at approximately USD 3.38 Billion in 2024 and reached USD 4.18 Billion in 2025. The market is projected to grow to USD 28.76 Billion by 2034, expanding at a CAGR of 23.8% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 24.58 billion over the analysis period, driven by converging pressures on legacy correspondent-banking networks, the structural cost advantages of blockchain-based settlement, and a regulatory environment that shifted decisively in favor of permissioned stablecoin deployment following the passage of the U.S. Lummis-Gillibrand Payment Stablecoin Act in mid-2025.

Get More Information about this report -

Request Free Sample ReportThree causal forces explain why the stablecoin payment infrastructure market reached its 2025 valuation and why its trajectory diverges sharply from earlier blockchain payment cycles. First, the Federal Reserve's FedNow instant-payment system, fully operational since late 2023, paradoxically accelerated stablecoin adoption by demonstrating that real-time settlement is achievable — while simultaneously exposing FedNow's exclusion of non-bank fintechs and cross-border flows, gaps that stablecoin rails fill directly. Second, USDC's daily settlement volume crossed USD 10 billion in Q1 2025, a cost-parity threshold at which enterprise treasury teams can justify migration away from SWIFT-based wires, given stablecoin transaction costs averaging USD 0.01–0.04 versus USD 15–45 per correspondent-bank transfer. Third, the Basel Committee's March 2025 clarification that tokenized deposits and fiat-backed stablecoins held in regulated custody qualify for zero-percent risk-weight treatment unlocked balance-sheet capacity at Tier-1 banks, converting institutional skeptics into active infrastructure buyers within a single regulatory cycle.

While headline growth figures suggest uniform expansion across the stablecoin payment infrastructure market, revenue concentration among the top four infrastructure providers intensified from 44% combined share in 2023 to 58% in 2025. This consolidation compresses margin for middleware vendors and regional orchestration providers who lack proprietary compliance tooling — a dynamic that mirrors the payment-gateway consolidation of 2015–2019, where Stripe and Adyen ultimately captured outsized value while scores of ISO 8583-era processors were commoditized. The analogy is instructive: infrastructure layers that control key management, regulatory reporting, and settlement finality will command durable pricing power; pure API aggregators face commoditization risk within three to four years.

Technology maturation compounds the market's growth trajectory. Zero-knowledge proof-based transaction privacy, reaching production-grade deployment at Aztec Network and Polygon Miden in early 2025, addresses the compliance-versus-privacy paradox that previously blocked enterprise adoption in healthcare and defense procurement. Cross-chain atomic settlement, enabled by the CCIP standard maintained by Chainlink Labs, reduces counterparty risk in multi-currency stablecoin transactions to near zero, a feature corporate treasury teams rank as the primary technical prerequisite for migrating payables workflows. Together, these developments explain why the stablecoin payment infrastructure market attracts capital from both enterprise software investors and traditional payment-network incumbents simultaneously — a dual demand signal with no clear precedent in prior fintech cycles.

, By Stablecoin Type (Fiat-Collateralized, Crypto-Collateralized, Algorithmic, CBDC-Linked), By Application (Cross-Border Payments, Merchant Acceptance, DeFi Settlement, Treasury Management), Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global stablecoin payment infrastructure market was valued at USD 4.18 billion in 2025 and is forecast to reach USD 28.76 billion by 2034 at a CAGR of 23.8% (2026–2034), reflecting structural demand for programmable, always-on settlement rails that correspondent banking cannot match.

- Segment Dominance: Fiat-collateralized stablecoin infrastructure held 62.4% of total segment revenue in 2025. Its leadership reflects the regulatory clarity provided by OCC Interpretive Letter 1174 and the EU Markets in Crypto-Assets (MiCA) Regulation Title III, which explicitly authorize banks to issue and custody fiat-backed tokens, giving incumbents a compliance moat unavailable to algorithmic alternatives.

- Segment Dominance: Cross-border remittance and B2B payments commanded 47.3% of application-layer revenue in 2025. Correspondent-bank markup on international transfers — averaging 4.7% per transaction according to World Bank data — creates an immediately addressable cost displacement opportunity that stablecoin corridors are actively monetizing in the USD 150-billion annual SME trade-finance segment.

- Driver: The passage of the U.S. Payment Stablecoin Act in June 2025 created a federal licensing framework for payment stablecoin issuers, triggering USD 2.3 billion in announced infrastructure investment within 90 days of enactment as banks, fintechs, and payment networks rushed to file for OCC non-bank stablecoin issuer charters.

- Restraint: Fragmented blockchain interoperability constrains enterprise adoption; fewer than 18% of corporate treasury systems support native multi-chain stablecoin flows as of 2025, forcing costly middleware integration that adds 6–14 weeks to deployment timelines and disproportionately affects SME adopters in Latin America and Southeast Asia lacking dedicated blockchain engineering resources.

- Opportunity: Tokenized payroll and supplier payment automation represents an addressable market of USD 9.4 billion by 2034, enabled by programmable payment conditions (smart contract escrow, milestone-based release) that stablecoin rails support natively. Early movers integrating payroll APIs with ERC-4337 account abstraction are capturing enterprise contracts that lock in multi-year infrastructure commitments.

- Trend: Embedded stablecoin wallets within enterprise resource planning (ERP) platforms reached 11% penetration among Fortune 1000 treasury departments in 2025 versus less than 2% in 2023. SAP's partnership with Circle and Oracle's integration with Paxos are accelerating adoption in North America, while European deployments lag at 4% penetration due to pending MiCA technical standards on settlement finality.

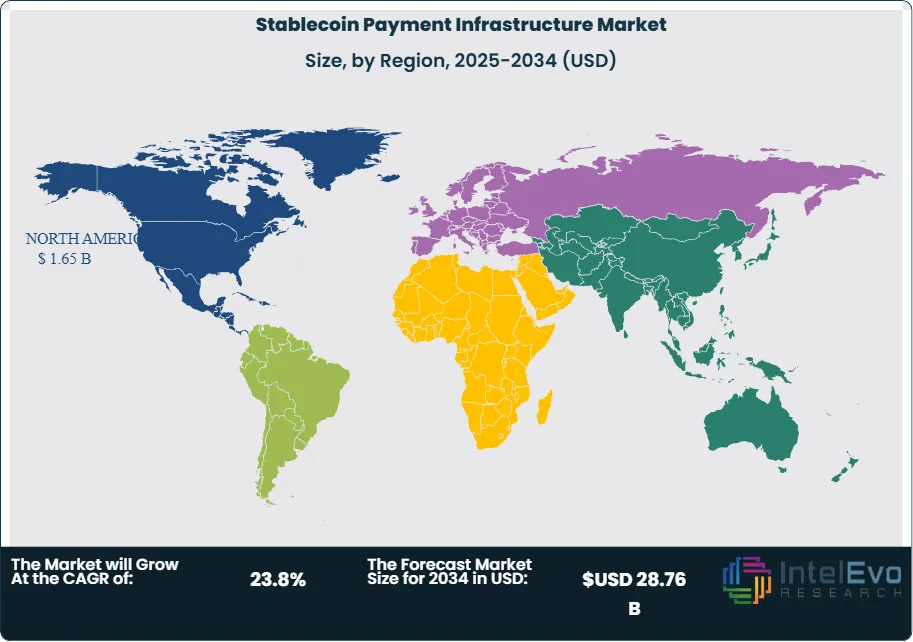

- Regional Analysis: North America led the global stablecoin payment infrastructure market with 39.4% share, equivalent to USD 1.65 billion in 2025, supported by the deepest pool of OCC-chartered stablecoin issuers, the highest concentration of institutional DeFi capital, and federal legislative clarity that peer regions have not yet matched.

Competitive Landscape Overview

The global stablecoin payment infrastructure market exhibits moderate-to-high consolidation at the infrastructure layer, with the top four providers — Circle Internet Financial, Tether Operations, Stripe (post-Bridge acquisition), and Visa — collectively holding approximately 58% of infrastructure-layer revenue in 2025. Competition is primarily technology- and compliance-driven rather than price-driven; enterprises select infrastructure partners based on regulatory licensing coverage, supported blockchain networks, and audit-trail depth rather than per-transaction cost alone. Competitive intensity escalated sharply in late 2024 through mid-2025 as three categories of new entrant — Tier-1 commercial banks with OCC charter filings, Asian super-app operators seeking USD-denominated settlement, and core-banking software vendors embedding stablecoin modules — compressed the total addressable market available to pure-play providers. This convergence triggered two landmark acquisitions: Stripe's USD 1.1-billion purchase of Bridge.xyz in April 2025 and Visa's strategic investment in Worldpay's stablecoin settlement arm, signaling that infrastructure ownership, not API access, will define competitive position through 2030.

A dynamic reshaping competition in 2025–2026 is the entrance of regulated non-U.S. stablecoin issuers into North American infrastructure contracts. MiCA-licensed issuers from Germany and Luxembourg, operating euro-denominated stablecoins with BaFin regulatory standing, began bidding on U.S. corporate FX corridor contracts in Q2 2025, offering 20–35% lower interchange on EUR/USD flows. This cross-currency arbitrage is forcing U.S.-centric providers to accelerate multi-currency reserve management capabilities — a product gap that created a USD 340-million addressable licensing and professional-services opportunity for compliance infrastructure vendors.

Competitive Landscape Matrix

| Company | HQ | Position | Key Product | Geo Strength | Recent Move (2024–2026) |

| Circle Internet Financial | USA | Leader | USDC Payment Rails | North America | Jan 2025: Launched Circle Payments Network for institutional cross-border settlements, onboarding 40+ bank partners. |

| Tether Operations | BVI/UAE | Leader | USDT Omnichain SDK | Asia Pacific / MEA | Mar 2025: Expanded USDT native issuance to Ethereum Layer-2 and TON blockchain, adding USD 8B daily settlement capacity. |

| Stripe, Inc. | USA | Challenger | Stablecoin Financial Accounts | North America / Europe | Apr 2025: Acquired Bridge.xyz for USD 1.1B, integrating stablecoin orchestration into Stripe's payment stack. |

| Visa Inc. | USA | Challenger | Visa Tokenized Asset Platform | Global | Feb 2025: Piloted USDC settlement with Solana-based merchant acquirers across 14 markets, processing USD 225M in test volume. |

| PayPal Holdings | USA | Challenger | PYUSD Stablecoin | North America | Nov 2024: Extended PYUSD to Venmo P2P and Xoom cross-border remittance, targeting USD 600M annual flow. |

| Ripple Labs | USA | Niche Player | RLUSD / ODL Network | Asia Pacific / Latin America | Jun 2025: RLUSD achieved NYDFS approval, enabling institutional USD liquidity provisioning on XRP Ledger. |

| Fireblocks Ltd. | USA/Israel | Niche Player | Fireblocks Payments Engine | Europe / North America | Aug 2025: Integrated ISO 20022 messaging into stablecoin rails, serving 30 Tier-1 bank clients. |

| Paxos Trust | USA | Niche Player | USDP / Paxos Settlement Service | North America | Dec 2024: Secured OCC conditional bank charter, enabling direct stablecoin custody without third-party trust. |

By Component:

Infrastructure software constituted the largest component segment of the stablecoin payment infrastructure market in 2025, capturing 53.7% of total revenue at USD 2.25 billion. Its dominance reflects the capital-intensive nature of building compliant settlement engines: issuers must maintain real-time reserve attestation, multi-jurisdiction KYC/AML pipelines, and blockchain node infrastructure simultaneously. Fireblocks, Paxos, and Anchorage Digital collectively occupy the institutional-grade custody sub-layer, where switching costs are structurally high due to multi-signature key ceremony requirements and auditor relationships built over two-to-three-year periods. This barrier limits new entrants who possess the cryptographic engineering skill but lack the SOC 2 Type II and ISAE 3402 audit history that enterprise procurement demands.

Orchestration middleware ranked second at 22.1% share (USD 924 million, 2025), with its growth rate of 31.2% exceeding the overall market average. The specific condition accelerating its growth above the market average is the proliferation of multi-chain enterprise deployments: as corporate treasuries simultaneously maintain USDC on Ethereum, Solana, and Stellar for different payment corridors, demand for a unified orchestration layer — capable of routing, netting, and reporting across chains without manual intervention — becomes non-negotiable. Bridge.xyz, prior to its Stripe acquisition, captured 19% of this sub-segment with its abstraction API, a position Stripe will leverage to embed stablecoin orchestration into its 1.5-million-merchant payment stack over 2025–2027.

Custody and key management infrastructure held 14.8% share (USD 619 million, 2025). The non-obvious competitive dynamic here is that this sub-segment is dominated by a set of providers — Anchorage Digital, BitGo, and Copper Technologies — who built their initial moats in crypto-native custody and now possess regulatory licenses (including OCC bank charter for Anchorage, FCA registration for Copper) that purely software-oriented competitors cannot easily replicate. New entrants face a 12-to-18-month regulatory onboarding cycle before they can custody assets for U.S. bank clients, creating a durable barrier that limits the sub-segment to a stable oligopoly through at least 2028. Compliance and analytics modules accounted for the remaining 9.4%, growing at 28.6% as MiCA's Travel Rule requirements and FINCEN's digital-asset reporting rules expanded the addressable compliance tooling market.

By Stablecoin Type:

Fiat-collateralized USD-pegged stablecoins drove 62.4% of infrastructure revenue in 2025 (USD 2.61 billion). Their leadership is causally explained by three interlocking regulatory events: OCC Interpretive Letter 1174 (issued 2021, confirmed enforceable in 2023), MiCA Title III effective June 2024, and the Payment Stablecoin Act of 2025. These three regulatory anchors created a compliant issuance pathway unavailable to crypto-collateralized or algorithmic designs, allowing USDC and PYUSD to achieve Fortune 500 treasury approval — a procurement threshold that requires documented regulatory standing, not merely technical soundness. Infrastructure providers building for fiat-collateralized tokens benefit from this regulatory tailwind: a compliant token generates recurring infrastructure licensing fees tied to issuance volume, creating annuity-like revenue streams.

Crypto-collateralized stablecoin infrastructure held 18.3% share (USD 765 million, 2025), with growth concentrated among DeFi-native enterprises and crypto-native fintech lenders. The fastest-growing sub-segment within this category is DAI-based B2B payment infrastructure, accelerating above the market average following MakerDAO's August 2024 rebrand to Sky Protocol and its introduction of USDS, a MiCA-ready version of DAI. This repositioning enabled European B2B platforms to adopt DAI-equivalent infrastructure without regulatory exposure. Algorithmic and hybrid stablecoins contributed 8.6% of revenue, a figure that remains depressed following the May 2022 Terra/LUNA collapse, which triggered SEC emergency rulemaking that specifically excluded non-fully-reserved stablecoins from institutional payment infrastructure eligibility. CBDC-linked bridging infrastructure accounted for 10.7% and is the highest-potential emerging segment: as the ECB Digital Euro pilot moves toward Phase 3 in 2026, infrastructure vendors capable of bridging commercial stablecoins to CBDC rails will capture a first-mover fee premium (industry analysis suggests 40–70 basis-points above standard settlement fees).

By Application:

Cross-border remittance and B2B payment infrastructure captured 47.3% of application revenue (USD 1.98 billion, 2025). The causal mechanism behind its leadership is direct: the World Bank estimates 4.7% average cost for international transfers, versus 0.2–0.4% for stablecoin corridors at scale. For a mid-size manufacturer executing USD 50 million annually in cross-border supplier payments, migration to stablecoin infrastructure generates USD 2.15–2.25 million in annual savings — a payback period of under eight months on infrastructure deployment costs. Ripple's On-Demand Liquidity (ODL) network, processing 40% of Ripple's total payment volume on stablecoin rails as of Q1 2025, demonstrates that this application has crossed from pilot to production at enterprise scale.

Merchant acceptance and POS integration held 24.8% share (USD 1.04 billion, 2025). PayPal's extension of PYUSD to its 432-million-user consumer platform in November 2024 was the single event that most accelerated this sub-segment, converting latent merchant interest into signed contracts as consumer-side liquidity provided the critical mass merchants require before accepting a new payment instrument. DeFi settlement and liquidity provisioning accounted for 17.6%, primarily from institutional market makers and prime brokers using stablecoin infrastructure for collateral management on derivatives desks — a use case that expanded materially after the CME Group's December 2024 announcement of USDC-margined futures. Payroll and treasury management contributed 10.3%, its growth rate of 34.1% the highest among all sub-segments, driven by remote-workforce payment demands in markets where traditional banking infrastructure imposes five-to-seven business day settlement delays on cross-border payroll.

By End-User:

Banks and financial institutions commanded 38.9% of end-user revenue (USD 1.63 billion, 2025). Their leading position reflects the structural reality that payment stablecoin issuance, under both U.S. and EU frameworks, requires either a bank charter or a licensed trust company — a gatekeeping mechanism that converts regulated banks from passive observers into active infrastructure investors. JPMorgan's JPM Coin, processing USD 1 billion in daily interbank transfers by Q2 2025, and Goldman Sachs' tokenized money market fund settlement infrastructure demonstrate that Tier-1 banks are not merely adopting stablecoin rails but building proprietary infrastructure that will reduce their dependence on third-party providers by 2027–2028.

Payment service providers (PSPs) captured 28.4% share (USD 1.19 billion, 2025). Enterprise corporate treasury followed at 19.6%, with notable acceleration among multinationals managing payables across Brazil, India, and Southeast Asia — regions where local currency volatility makes USDC-denominated invoicing financially advantageous even before infrastructure cost savings are factored in. Retail and consumer platforms held 13.1%, a segment that underperforms its theoretical potential due to onboarding friction and uneven smartphone wallet penetration in target markets.

Regional Analysis

North America:

Backed by the passage of the federal Payment Stablecoin Act in June 2025, the deepest institutional DeFi capital pool globally, and a financial regulatory framework that produced nine new OCC stablecoin issuer applications within 60 days of enactment, North America's stablecoin payment infrastructure market captured 39.4% of global revenue at USD 1.65 billion in 2025. The United States dominates this regional figure, with New York-headquartered issuers — including Circle, Paxos, and Gemini — controlling over 71% of domestic stablecoin settlement volume. Canada contributes at meaningful scale through Toronto-based PSPs integrating USDC rails into Business Development Bank of Canada-backed export-finance products. Mexico provides the region's highest remittance-corridor growth, where Bitso's stablecoin-based peso-to-dollar corridor processed USD 4.2 billion in 2024 volume, validating commercial viability of sub-1% cost corridors that legacy remittance operators cannot match. The specific competitive risk for North America's incumbents is that federal licensing creates a fixed compliance cost that smaller regional players cannot absorb, concentrating the market further among capitalized nationals.

Europe:

Regulatory mandates under MiCA Regulation (EU) 2023/1114, fully effective for stablecoin issuers since June 2024, reshaped procurement patterns across the European stablecoin payment infrastructure market, which held 26.1% share worth USD 1.09 billion in 2025. Germany leads European adoption, where BaFin's proactive engagement with blockchain payment firms established Frankfurt's Commerzbank, Deutsche Bank's DWS subsidiary, and Munich-based fintechs as early MiCA-compliant infrastructure investors. The UK, operating outside MiCA post-Brexit, maintained parallel momentum under the Financial Services and Markets Act 2023 provisions on digital settlement assets, with the City of London's Digital Securities Sandbox attracting USD 430 million in stablecoin infrastructure pilot investment from Q3 2024 through Q1 2025. Switzerland's DLT Act, implemented through SIX Digital Exchange, enables Swiss franc-denominated stablecoin settlement for institutional cross-border payments — a niche that attracted 12 Tier-2 European banks to deploy SIX-connected infrastructure during 2025. The primary restraint in Europe remains MiCA's 200-million-euro daily transaction cap on third-country stablecoin issuers, which forces European enterprises relying on USDC volumes above this threshold to establish EU-subsidiary issuers, adding 4–6 months to compliance timelines.

Asia Pacific:

Manufacturing capacity additions across Shenzhen's blockchain technology parks and the Monetary Authority of Singapore's Project Orchid CBDC/stablecoin interoperability initiative propelled Asia Pacific's stablecoin payment infrastructure market to 21.4% global share, valued at USD 895 million in 2025. Singapore functions as the regional infrastructure hub, concentrating licensing activity under the Payment Services Act 2019 (amended 2023) and hosting the headquarters of infrastructure providers Alchemy Pay, Triple-A, and Pundi X that collectively serve nine Asian markets. Japan's January 2025 amendment to the Payment Services Act to explicitly permit stablecoin issuance by domestic banks triggered a wave of infrastructure procurement at MUFG, Sumitomo Mitsui Financial Group, and Japan Post Bank, each targeting real-time domestic and cross-Asia-Pacific settlement workflows. India's National Payments Corporation of India is exploring stablecoin interoperability with the UPI network — a potential use case that, if implemented, would create the largest addressable stablecoin payment volume in the region given UPI's 14-billion-monthly-transaction baseline. China's regulatory environment remains prohibitive for private stablecoin infrastructure, redirecting enterprise demand toward e-CNY CBDC integration, which indirectly benefits bridging-infrastructure vendors serving Hong Kong's cross-border corridor.

Latin America:

Currency volatility across Brazil and Argentina — where the Brazilian real depreciated 18.4% against the USD in 2024 and the Argentine peso experienced a managed float reintroduction under the 2024 IMF stabilization program — constrained domestic capital investment, yet Latin America's stablecoin payment infrastructure market still reached USD 412 million (9.8% global share) in 2025, driven by dollarization demand that stablecoin rails satisfy more efficiently than formal banking channels. Brazil leads regional infrastructure deployment, where Sao Paulo-based fintech Nubank integrated USDC rails into its 100-million-customer neobank platform in Q4 2024, processing an estimated USD 280 million in stablecoin-settled transactions within the first six months. Mexico ranks second, primarily through Bitso's remittance corridor infrastructure and the Bank of Mexico's regulatory sandbox accommodating three stablecoin pilot programs as of mid-2025. Argentina's informal dollarization creates paradoxically strong organic demand: an estimated 4.2 million Argentines hold USDT or USDC as primary savings instruments, generating natural transaction infrastructure demand that formal regulatory frameworks have not yet fully addressed. The IMF's Article IV consultation with Argentina in April 2025 flagged stablecoin-driven capital flows as a material monetary policy consideration — a first-of-its-kind acknowledgment that validates the region's infrastructure market relevance.

Middle East & Africa:

Saudi Arabia's Vision 2030 digital economy diversification program and UAE free-zone infrastructure incentives within the Abu Dhabi Global Market (ADGM) and Dubai International Financial Centre (DIFC) opened new demand corridors, pushing the MEA stablecoin payment infrastructure market to USD 224 million (3.4% share) in 2025. The UAE accounts for approximately 58% of regional infrastructure revenue, anchored by the ADGM's Virtual Asset Regulatory Authority (VARA) framework, which issued 14 stablecoin infrastructure licenses in 2024 and attracted regional offices from Circle, Ripple, and Fireblocks to Dubai Internet City. Saudi Arabia's STC Pay and Al Rajhi Bank jointly piloted SAR-pegged stablecoin settlement for cross-border Gulf Cooperation Council trade in Q1 2025, a development that, if scaled, would create the GCC's first sovereign-backed stablecoin infrastructure ecosystem. Africa contributes through Nigeria, Kenya, and South Africa, where mobile-money platforms including M-Pesa and OPay are evaluating USDT-based rails for regional trade settlement — use cases that bypass legacy correspondent banking entirely for sub-USD-1,000 transactions. The MEA market carries the highest growth potential within the 2025–2034 forecast horizon, with a projected CAGR of 29.4% driven by underbanked population exposure and pan-African trade growth under the African Continental Free Trade Area (AfCFTA) frameworks.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Component

- Infrastructure Software

- Orchestration Middleware

- Custody & Key Management

- Compliance & Analytics Modules

By Stablecoin Type

- Fiat-Collateralized (USD-Pegged)

- Crypto-Collateralized

- Algorithmic / Hybrid

- CBDC-Linked Bridging

By Application

- Cross-Border Remittance & B2B Payments

- Merchant Acceptance & POS Integration

- DeFi Settlement & Liquidity Provisioning

- Payroll & Treasury Management

By End-User

- Banks & Financial Institutions

- Payment Service Providers

- Enterprise Corporate Treasury

- Retail & Consumer Platforms

By Deployment

- Cloud-Native SaaS

- Hybrid On-Premise/Cloud

- Bankchain / Private Network

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 4.18 B |

| Forecast Revenue (2034) | USD 28.76 B |

| CAGR (2025-2034) | 23.8% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Component, Infrastructure Software, Orchestration Middleware, Custody & Key Management, Compliance & Analytics Modules), By Stablecoin Type, Fiat-Collateralized (USD-Pegged), Crypto-Collateralized, Algorithmic / Hybrid, CBDC-Linked Bridging), By Application, Cross-Border Remittance & B2B Payments, Merchant Acceptance & POS Integration, DeFi Settlement & Liquidity Provisioning, Payroll & Treasury Management), By End-User, Banks & Financial Institutions, Payment Service Providers, Enterprise Corporate Treasury, Retail & Consumer Platforms), By Deployment, Cloud-Native SaaS, Hybrid On-Premise/Cloud, Bankchain / Private Network |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | CIRCLE INTERNET FINANCIAL, TETHER OPERATIONS LIMITED, STRIPE, INC. (BRIDGE.XYZ), RIPPLE LABS, INC., VISA INC., PAYPAL HOLDINGS, INC. (PYUSD), FIREBLOCKS LTD., PAXOS TRUST COMPANY, ANCHORAGE DIGITAL BANK, BITGO HOLDINGS, INC., COINBASE GLOBAL, INC., JPMORGAN CHASE & CO. (JPM COIN), MASTERCARD INCORPORATED, ALCHEMY PAY, TRIPLE-A TECHNOLOGIES, COPPER TECHNOLOGIES (UK) LTD., GEMINI TRUST COMPANY, OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Stablecoin Type (Fiat-Collateralized, Crypto-Collateralized, Algorithmic, CBDC-Linked), By Application (Cross-Border Payments, Merchant Acceptance, DeFi Settlement, Treasury Management), Industry Trends & Forecast 2026-2034")

, By Stablecoin Type (Fiat-Collateralized, Crypto-Collateralized, Algorithmic, CBDC-Linked), By Application (Cross-Border Payments, Merchant Acceptance, DeFi Settlement, Treasury Management), Industry Trends & Forecast 2026-2034")

, By Stablecoin Type (Fiat-Collateralized, Crypto-Collateralized, Algorithmic, CBDC-Linked), By Application (Cross-Border Payments, Merchant Acceptance, DeFi Settlement, Treasury Management), Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Stablecoin Payment Infrastructure Market?

The Global Stablecoin Payment Infrastructure Market was valued at USD 3.38 Billion in 2024 and is projected to reach USD 28.76 Billion by 2034, growing at a CAGR of 23.8% from 2026 to 2034, driven by rising adoption of blockchain-based payment systems, increasing demand for low-cost cross-border transactions, expanding institutional adoption of digital assets, and growing integration of stablecoins across fintech, banking, e-commerce, and decentralized finance ecosystems worldwide.

Who are the major players in the Stablecoin Payment Infrastructure Market?

CIRCLE INTERNET FINANCIAL, TETHER OPERATIONS LIMITED, STRIPE, INC. (BRIDGE.XYZ), RIPPLE LABS, INC., VISA INC., PAYPAL HOLDINGS, INC. (PYUSD), FIREBLOCKS LTD., PAXOS TRUST COMPANY, ANCHORAGE DIGITAL BANK, BITGO HOLDINGS, INC., COINBASE GLOBAL, INC., JPMORGAN CHASE & CO. (JPM COIN), MASTERCARD INCORPORATED, ALCHEMY PAY, TRIPLE-A TECHNOLOGIES, COPPER TECHNOLOGIES (UK) LTD., GEMINI TRUST COMPANY, OTHERS

Which segments covered the Stablecoin Payment Infrastructure Market?

By Component, Infrastructure Software, Orchestration Middleware, Custody & Key Management, Compliance & Analytics Modules), By Stablecoin Type, Fiat-Collateralized (USD-Pegged), Crypto-Collateralized, Algorithmic / Hybrid, CBDC-Linked Bridging), By Application, Cross-Border Remittance & B2B Payments, Merchant Acceptance & POS Integration, DeFi Settlement & Liquidity Provisioning, Payroll & Treasury Management), By End-User, Banks & Financial Institutions, Payment Service Providers, Enterprise Corporate Treasury, Retail & Consumer Platforms), By Deployment, Cloud-Native SaaS, Hybrid On-Premise/Cloud, Bankchain / Private Network

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Stablecoin Payment Infrastructure Market

Published Date : 25 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date