- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Stem Cell Manufacturing Market Size & Forecast | CAGR 10.9%

Global Stem Cell Manufacturing Market Size, Share, Growth & Industry Analysis By Cell Type (iPSCs, MSCs, HSCs, Neural Stem Cells & Specialized Lineages), By Technology Platform (Bioreactor-Based Expansion, 2D Planar Culture, Microcarrier Suspension, Automated Closed Systems), By End-User (Biopharma, CDMOs, Research Institutes, Hospitals) Industry Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

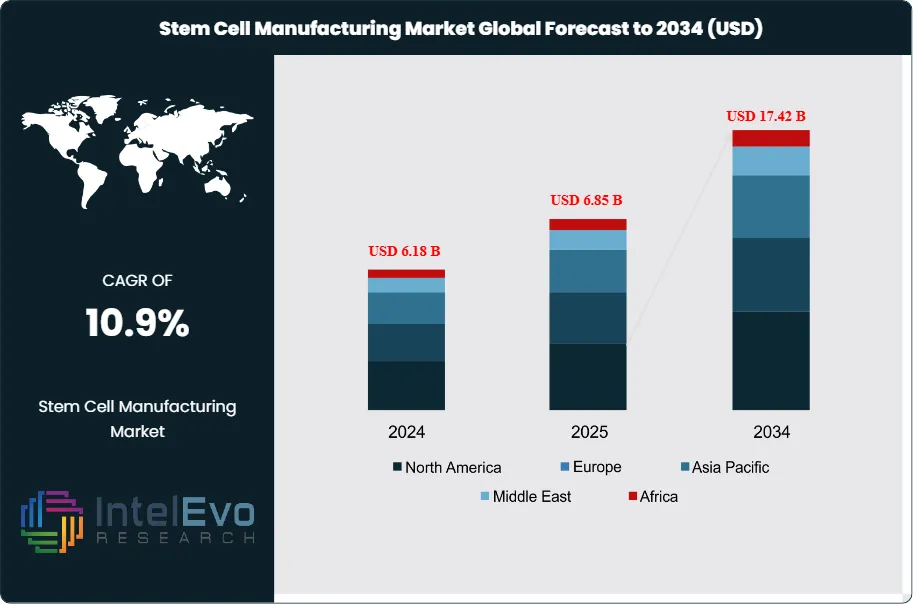

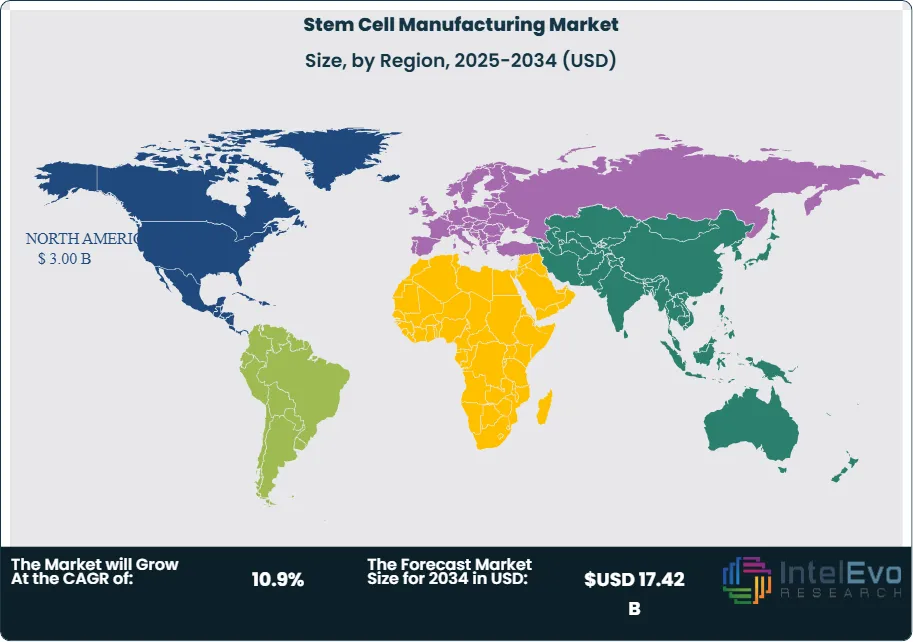

| USD 6.85 Billion | USD 17.42 Billion | 10.9% | North America, 43.8% |

The Stem Cell Manufacturing Market was valued at approximately USD 6.18 Billion in 2024 and reached USD 6.85 Billion in 2025. The market is projected to grow to USD 17.42 Billion by 2034, expanding at a CAGR of 10.9% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 10.57 Billion over the analysis period, reflecting the accelerating clinical translation of cell and gene therapies and the expanding role of stem cell-derived products in regenerative medicine, disease modeling, and drug discovery.

Get More Information about this report -

Request Free Sample ReportStem cell manufacturing encompasses the upstream expansion, differentiation, and cryopreservation of pluripotent stem cells, mesenchymal stem cells (MSCs), hematopoietic stem cells (HSCs), and induced pluripotent stem cells (iPSCs), as well as the bioprocessing equipment, culture media, reagents, and quality assurance systems that support commercial-scale production. The FDA CBER division governs U.S. clinical and commercial stem cell products under 21 CFR Part 1271 and Biologics License Application (BLA) requirements. The European Medicines Agency (EMA) regulates advanced therapy medicinal products (ATMPs) under the ATMP Regulation (EC) No 1394/2007, creating a unified compliance framework that directly shapes manufacturing investment decisions across the continent.

The stem cell manufacturing market is expanding rapidly because approvals for autologous and allogeneic cell therapies have increased materially since 2022, with cumulative CGT approvals in the U.S. exceeding 30 products by mid-2025. Each approval triggers significant scale-up investment in cGMP manufacturing capacity. CDMOs focused on cell therapy manufacturing, including Lonza Cell & Gene and Catalent Biologics, are committing combined capital expenditure exceeding USD 2.4 Billion through 2027 to expand stem cell production infrastructure. Simultaneously, the iPSC platform is creating a new category of allogeneic cell therapy manufacturing that offers substantial cost advantages over autologous approaches, with iPSC-derived product developers projecting manufacturing cost per dose reductions of 40–60% compared to patient-specific autologous programs.

North America leads the stem cell manufacturing market with 43.8% of global revenue in 2025, driven by NIH investment exceeding USD 2.1 Billion in stem cell research grants, a dense cluster of clinical-stage cell therapy companies in the Boston-Cambridge and San Francisco Bay Area corridors, and favorable regulatory engagement from the FDA's Center for Biologics Evaluation and Research. Asia Pacific is the fastest-growing regional market, expanding at a 13.8% CAGR through 2034, driven by Japan's regenerative medicine regulatory pathway under the Act on the Safety of Regenerative Medicine and significant investment in South Korea and China. Automation and closed-system bioprocessing are redefining manufacturing efficiency, with fully automated stem cell expansion platforms reducing operator-dependent variability and enabling the consistency required for commercial-scale therapy production.

, By Technology Platform (Bioreactor-Based Expansion, 2D Planar Culture, Microcarrier Suspension, Automated Closed Systems), By End-User (Biopharma, CDMOs, Research Institutes, Hospitals) Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The global stem cell manufacturing market was valued at USD 6.85 Billion in 2025 and is projected to reach USD 17.42 Billion by 2034, registering a CAGR of 10.9% over the forecast period 2026–2034.

- Segment Dominance: By cell type, induced pluripotent stem cells (iPSCs) represent the largest and fastest-growing sub-segment with 36.4% of the stem cell manufacturing market in 2025, driven by their broad applicability across allogeneic therapy development, drug screening, and disease modeling platforms.

- Segment Dominance: By end-user, pharmaceutical and biopharmaceutical companies account for 46.2% of total stem cell manufacturing spending in 2025, reflecting the concentration of commercial cell therapy pipeline activity and the associated upstream manufacturing investment in this segment.

- Driver: The rapid expansion of allogeneic iPSC-derived cell therapy pipelines is the primary demand driver; more than 120 iPSC-based clinical programs were active globally in 2025, each requiring scalable cGMP manufacturing capacity and specialized differentiation media systems.

- Restraint: Manufacturing complexity and high cost per dose remain the dominant market constraint; autologous stem cell therapy manufacturing costs average USD 80,000–350,000 per patient batch, limiting commercial viability and slowing market penetration in cost-sensitive health systems.

- Opportunity: Automated bioreactor-based expansion platforms represent an estimated USD 3.1 Billion addressable opportunity within the stem cell manufacturing market by 2034, enabling consistent, GMP-compliant scale-up at costs 30–50% lower than manual open-system processes.

- Trend: Closed-system manufacturing using single-use bioreactors and automated cell processing systems is the dominant technology trend; adoption among new cGMP stem cell manufacturing facilities reached 61% in 2025, up from 38% in 2021.

- Regional Analysis: North America leads the stem cell manufacturing market with 43.8% share and USD 3.00 Billion in revenue in 2025, supported by robust NIH funding, a high density of cell therapy developers, and established CDMO capacity in the U.S. and Canada.

Competitive Landscape Overview

The stem cell manufacturing market is moderately consolidated at the equipment and media supply level, with the top four players holding approximately 44% of global revenue in 2025. Competition centers on technological differentiation, particularly in bioreactor platform performance, specialty culture media formulations, and closed-system automation capability. M&A activity has intensified since 2023, as large life sciences instrument companies seek to acquire cell therapy manufacturing specialists. Three significant acquisitions occurred in 2024–2025 alone, reflecting strategic urgency among instrument and bioprocess suppliers to capture the growing CGT manufacturing supply chain. Pricing competition remains secondary to technical performance in this market, given the regulatory and clinical risk associated with switching manufacturing platforms mid-development.

Competitive Landscape Matrix

| Company | HQ | Position | Key Solution | Geo Strength | Recent Strategic Move |

| Thermo Fisher Scientific | USA | Leader | Gibco CTS Cell Therapy Systems | North America / Global | Acquired a cell therapy media specialist in Feb 2025 to expand its GMP culture media portfolio for iPSC manufacturing |

| Lonza Group | Switzerland | Leader | Nucleofector & Cocoon Platform | Europe / North America | Completed a USD 500M expansion of its Houston cell therapy CDMO facility in Jan 2025 |

| Miltenyi Biotec | Germany | Leader | CliniMACS Prodigy closed-system processor | Europe / North America | Launched the CliniMACS Prodigy XT for automated iPSC expansion in Dec 2024 |

| Sartorius AG | Germany | Leader | Biostat STR bioreactor series | Europe / Global | Partnered with a leading iPSC developer to co-develop GMP-grade expansion protocols in Mar 2025 |

| Cytiva (Danaher) | USA | Challenger | Xcellerex XDR bioreactor system | North America / Asia Pacific | Opened a Singapore cell therapy manufacturing applications lab in Apr 2025 |

| Becton Dickinson (BD) | USA | Challenger | FACSMelody cell sorter for QC | North America | Introduced AI-assisted cell sorting software for stem cell release testing in Jan 2025 |

| Catalent Cell & Gene | USA | Challenger | CGMP Cell Therapy Manufacturing Services | North America | Announced a 120,000 sq ft cell therapy expansion in Bloomington, Indiana in Jun 2025 |

| Waisman Biomanufacturing | USA | Niche Player | Academic GMP iPSC Manufacturing | North America | Partnered with three academic medical centers for iPSC banking programs in Feb 2025 |

| Nikon CeLL innovation | Japan | Niche Player | CellPathfinder AI cell monitoring | Asia Pacific | Deployed AI-enabled live cell imaging in 12 Japanese cell therapy facilities in Mar 2025 |

| OxGene (Oxford Biomedica) | UK | Niche Player | LentiVector viral delivery for iPSC | Europe | Signed a multi-year iPSC lentiviral vector supply agreement with a European CGT developer in May 2025 |

By Cell Type

The stem cell manufacturing market by cell type is led by induced pluripotent stem cells (iPSCs), which account for 36.4% of market revenue in 2025 at approximately USD 2.49 Billion. The dominance of iPSCs reflects their unique combination of unlimited self-renewal capacity and differentiation potential, which makes them the preferred starting material for allogeneic cell therapies across oncology, cardiovascular, neurology, and ophthalmology indications. iPSC-based manufacturing requires highly controlled reprogramming protocols, feeder-free culture conditions using defined GMP-grade media, and rigorous karyotype and genomic stability testing to ensure product consistency and safety before clinical administration. Mesenchymal stem cells (MSCs) represent the second-largest sub-segment with 28.7% of market revenue in 2025, driven by their extensive use in immunomodulatory and anti-inflammatory therapy development, as well as orthopedic and wound healing applications. Hematopoietic stem cells (HSCs) account for 21.4% of the market, supported by their established clinical role in bone marrow transplantation and the expanding pipeline of gene-modified HSC therapies for hemoglobinopathies and primary immunodeficiencies. Neural stem cells and other specialized lineages hold the remaining 13.5% share and are growing at above-market rates as neurological cell therapy pipelines advance through clinical stages.

By Technology Platform

Stem cell manufacturing by technology platform segments the market into bioreactor-based expansion systems, two-dimensional planar culture systems, microcarrier-based culture, and automated closed-system processing platforms. Bioreactor-based expansion systems hold the largest platform share at 38.2% in 2025, valued at approximately USD 2.62 Billion. Stirred-tank bioreactors supporting iPSC and MSC expansion provide the scalability required for commercial allogeneic therapy production, with single bioreactor runs yielding 100 million to 2 billion cells per batch depending on process optimization and bioreactor volume. Two-dimensional planar culture systems, including multi-layer cell factories and HYPERStack systems, account for 33.6% of the market and remain the primary platform for autologous therapy manufacturing where smaller batch volumes are standard. Microcarrier-based suspension culture holds 15.8% of market share and is gaining adoption for MSC expansion programs requiring higher cell yields than planar culture can provide. Automated closed-system processing platforms, encompassing integrated devices such as the Miltenyi CliniMACS Prodigy and similar systems, hold 12.4% and represent the fastest-growing platform segment at an estimated 16.2% CAGR through 2034 as the industry prioritizes manufacturing consistency, reduced contamination risk, and lower clean room dependency.

By End-User

The stem cell manufacturing market by end-user is dominated by pharmaceutical and biopharmaceutical companies, which account for 46.2% of total market revenue in 2025 at USD 3.16 Billion. These organizations are building or outsourcing large-scale stem cell manufacturing capacity to support clinical trial supply chains and, increasingly, commercial launch readiness for approved cell therapies. CDMOs specializing in cell and gene therapy manufacturing represent 24.8% of the market and constitute the fastest-growing end-user segment, as mid-size and small biotech companies without internal manufacturing capabilities outsource their GMP stem cell production. Academic research institutes and biobanks account for 17.3% of the market, primarily through demand for research-grade and early GMP-compliant iPSC and MSC manufacturing services tied to investigator-sponsored trials and translational programs. Hospitals and cell therapy centers hold 11.7% and continue to invest in in-house manufacturing capability for point-of-care autologous therapy production, particularly for hematopoietic and MSC applications where proximity between manufacturing and administration reduces vein-to-vein time and cold chain risk.

By Product Type

Stem cell manufacturing by product type includes cell culture media and reagents, bioreactors and bioprocessing equipment, cell therapy manufacturing services (CDMO), cryopreservation products, and quality control and testing solutions. Cell culture media and reagents hold the largest product share at 34.6% in 2025, equivalent to USD 2.37 Billion, driven by the high per-run consumption of specialty media formulations required for iPSC maintenance, directed differentiation, and clinical-grade expansion. Bioreactors and bioprocessing equipment account for 27.4% of market revenue, anchored by capital expenditure cycles tied to new cell therapy manufacturing facility buildouts. CDMO manufacturing services represent 22.8% of the market and are expanding rapidly as therapy developers outsource upstream manufacturing. Cryopreservation products, including controlled-rate freezing systems, cryogenic storage solutions, and thawing equipment, hold 9.6% of the market. Quality control and testing solutions, encompassing sterility testing, mycoplasma detection, potency assays, and flow cytometry-based release testing, account for 5.6% and are growing at above-average rates as regulatory expectations for release testing rigor increase with every new product approval.

Regional Analysis

North America

North America leads the global stem cell manufacturing market with a 43.8% share and USD 3.00 Billion in revenue in 2025. The United States is the dominant country market, accounting for approximately 91% of North American revenue. The FDA CBER’s active engagement with CGT developers through the Regenerative Medicine Advanced Therapy (RMAT) designation program has accelerated regulatory timelines for stem cell-derived therapies, incentivizing companies to invest in U.S.-based GMP manufacturing facilities early in clinical development. NIH funding for stem cell research exceeded USD 2.1 Billion in fiscal year 2025, with significant portions supporting translational manufacturing programs at academic medical centers. The Boston-Cambridge corridor, San Francisco Bay Area, and Research Triangle Park host the highest concentration of clinical-stage stem cell therapy developers, creating dense demand nodes for local CDMO capacity and bioprocessing equipment suppliers. Canada contributes approximately 9% of North American revenue, with the Centre for Commercialization of Regenerative Medicine (CCRM) in Toronto acting as a national hub for iPSC banking and CDMO capacity development. Mexico is an emerging market for medical tourism-related stem cell applications, though regulatory frameworks remain less defined relative to the U.S. and Canada.

Europe

Europe accounts for 27.6% of the global stem cell manufacturing market in 2025 at USD 1.89 Billion. The ATMP regulatory framework administered by the EMA provides a structured pathway for stem cell-derived therapeutic product approval across the EU, creating regulatory certainty that supports manufacturing investment. Germany is the leading European market, home to several major cell therapy developers and bioprocessing equipment manufacturers including Miltenyi Biotec and Sartorius, which collectively supply a significant share of global stem cell manufacturing tools. The United Kingdom maintains its position as a leading research hub post-Brexit, with the Cell and Gene Therapy Catapult in London providing CDMO services and manufacturing scale-up support to more than 80 companies in 2025. France is the third-largest European market, supported by the AFSSaPS ATMP authorization framework and Paris Saclay’s emerging cell therapy cluster. Switzerland benefits from the headquarters presence of Lonza Group, a dominant force in cell therapy CDMO services. The Netherlands, Sweden, and Belgium represent smaller but growing markets aligned with the broader European biotech investment wave. Hospital Exemption provisions under the ATMP Regulation allow academic hospitals in Europe to manufacture small volumes of stem cell products for individual patients, creating a distributed manufacturing base in parallel with commercial-scale capacity.

Asia Pacific

Asia Pacific holds a 19.8% share of the global stem cell manufacturing market in 2025 with USD 1.36 Billion in revenue and is the fastest-growing region, projected to expand at a 13.8% CAGR through 2034. Japan leads the Asia Pacific market, supported by the Act on the Safety of Regenerative Medicine (ASRM) and the Pharmaceuticals and Medical Devices Act (PMDA) conditional approval pathway, which allows commercialization of regenerative medicine products before comprehensive clinical data is available, accelerating time-to-market and manufacturing investment decisions. South Korea is the second-largest Asia Pacific market, with major pharmaceutical companies including Samsung Biologics and CJ HealthCare building out cell therapy manufacturing capabilities. China is a rapidly expanding market with domestic stem cell manufacturing investment accelerating under the National Medical Products Administration (NMPA) revised cell therapy guidance issued in 2023. Domestic companies such as OriCell Therapeutics and Cellular Biomedicine Group are scaling iPSC and MSC manufacturing with government support under the Healthy China 2030 initiative. India is an emerging market for stem cell research and manufacturing, with several university-affiliated centers offering GMP-grade HSC and MSC production for investigator-sponsored trials. Australia rounds out the key Asia Pacific markets, with funding from the Medical Research Future Fund supporting stem cell therapy manufacturing development programs.

Latin America

Latin America accounts for 5.0% of the global stem cell manufacturing market in 2025 with USD 0.34 Billion in revenue. Brazil is the dominant Latin American market, representing approximately 62% of regional revenue. The Brazilian Health Regulatory Agency (ANVISA) updated its cell therapy GMP guidelines in 2024 to align more closely with FDA and EMA standards, improving the investment environment for commercial-grade stem cell manufacturing facilities. The Butantan Institute and Instituto de Pesquisas Energeticas e Nucleares (IPEN) are among the public-sector institutions investing in GMP stem cell production capacity. Mexico is the second-largest market, though a dual environment exists between regulated hospital-based manufacturing for legitimate clinical trials and the well-documented stem cell medical tourism sector that operates with variable regulatory oversight. Argentina contributes to the regional market through academic medical center-based HSC manufacturing for bone marrow transplantation programs. Regional infrastructure constraints, including limited access to specialized cell therapy manufacturing equipment and GMP-grade reagents at competitive prices, continue to restrict the pace of market development across Latin America. Supply agreements with North American and European bioprocessing suppliers are beginning to improve equipment availability in the region.

Middle East & Africa

The Middle East and Africa region holds a 3.8% share of the global stem cell manufacturing market in 2025, representing USD 0.26 Billion in revenue. The UAE is the most active market in the region, with Dubai’s Health Authority and Abu Dhabi’s SEHA network investing in stem cell banking, clinical manufacturing, and research infrastructure as part of broader healthcare diversification programs. Saudi Arabia’s Vision 2030 healthcare transformation initiative has allocated significant capital to building domestic biopharmaceutical manufacturing capability, and stem cell therapy is identified as a priority therapeutic area within the Kingdom’s National Biotechnology Strategy. South Africa leads the African segment of the market, with the South African Health Products Regulatory Authority (SAHPRA) providing the most developed regulatory framework for cell therapy on the continent. The King Faisal Specialist Hospital and Research Centre in Riyadh operates one of the largest hematopoietic stem cell transplantation programs in the Middle East, creating demand for GMP-grade HSC manufacturing and processing capacity. Israel contributes materially to the regional market through a cluster of stem cell biotech companies including Pluri Inc. and Bonus BioGroup, which are expanding manufacturing capacity for MSC and iPSC-derived products. Infrastructure investment from Gulf sovereign wealth funds in healthcare and biotechnology is expected to accelerate stem cell manufacturing market growth in the MEA region through 2034.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Cell Type

- Induced Pluripotent Stem Cells (iPSCs)

- Mesenchymal Stem Cells (MSCs)

- Hematopoietic Stem Cells (HSCs)

- Neural Stem Cells & Other Specialized Lineages

By Technology Platform

- Bioreactor-Based Expansion Systems

- Two-Dimensional Planar Culture Systems

- Microcarrier-Based Suspension Culture

- Automated Closed-System Processing Platforms

By End-User

- Pharmaceutical & Biopharmaceutical Companies

- CDMOs (Cell & Gene Therapy Focused)

- Academic Research Institutes & Biobanks

- Hospitals & Cell Therapy Centers

By Product Type

- Cell Culture Media & Reagents

- Bioreactors & Bioprocessing Equipment

- CDMO Manufacturing Services

- Cryopreservation Products

- Quality Control & Testing Solutions

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 6.85 B |

| Forecast Revenue (2034) | USD 17.42 B |

| CAGR (2025-2034) | 10.9% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Cell Type, (Induced Pluripotent Stem Cells (iPSCs), Mesenchymal Stem Cells (MSCs), Hematopoietic Stem Cells (HSCs), Neural Stem Cells & Other Specialized Lineages), By Technology Platform, (Bioreactor-Based Expansion Systems, Two-Dimensional Planar Culture Systems, Microcarrier-Based Suspension Culture, Automated Closed-System Processing Platforms), By End-User, (Pharmaceutical & Biopharmaceutical Companies, CDMOs (Cell & Gene Therapy Focused), Academic Research Institutes & Biobanks, Hospitals & Cell Therapy Centers), By Product Type, (Cell Culture Media & Reagents, Bioreactors & Bioprocessing Equipment, CDMO Manufacturing Services, Cryopreservation Products, Quality Control & Testing Solutions) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | THERMO FISHER SCIENTIFIC, LONZA GROUP, MILTENYI BIOTEC, SARTORIUS AG, CYTIVA (DANAHER CORPORATION), BECTON DICKINSON AND COMPANY (BD), CATALENT CELL & GENE, WAISMAN BIOMANUFACTURING, NIKON CELL INNOVATION CO., LTD., OXFORD BIOMEDICA (OXGENE), PLURILOCK SECURITY / PLURI INC., CELLULAR DYNAMICS INTERNATIONAL (CDI), FUJIFILM CELLULAR DYNAMICS, BIO-TECHNE CORPORATION, NCARDIA, HITACHI SOLUTIONS, CORNING INCORPORATED, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Technology Platform (Bioreactor-Based Expansion, 2D Planar Culture, Microcarrier Suspension, Automated Closed Systems), By End-User (Biopharma, CDMOs, Research Institutes, Hospitals) Industry Trends & Forecast 2026–2034")

, By Technology Platform (Bioreactor-Based Expansion, 2D Planar Culture, Microcarrier Suspension, Automated Closed Systems), By End-User (Biopharma, CDMOs, Research Institutes, Hospitals) Industry Trends & Forecast 2026–2034")

, By Technology Platform (Bioreactor-Based Expansion, 2D Planar Culture, Microcarrier Suspension, Automated Closed Systems), By End-User (Biopharma, CDMOs, Research Institutes, Hospitals) Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Stem Cell Manufacturing Market?

Global Stem cell manufacturing market valued at USD 6.18B in 2024, reaching USD 17.42B by 2034, growing at a CAGR of 10.9% from 2026–2034.

Who are the major players in the Stem Cell Manufacturing Market?

THERMO FISHER SCIENTIFIC, LONZA GROUP, MILTENYI BIOTEC, SARTORIUS AG, CYTIVA (DANAHER CORPORATION), BECTON DICKINSON AND COMPANY (BD), CATALENT CELL & GENE, WAISMAN BIOMANUFACTURING, NIKON CELL INNOVATION CO., LTD., OXFORD BIOMEDICA (OXGENE), PLURILOCK SECURITY / PLURI INC., CELLULAR DYNAMICS INTERNATIONAL (CDI), FUJIFILM CELLULAR DYNAMICS, BIO-TECHNE CORPORATION, NCARDIA, HITACHI SOLUTIONS, CORNING INCORPORATED, Others

Which segments covered the Stem Cell Manufacturing Market?

By Cell Type, (Induced Pluripotent Stem Cells (iPSCs), Mesenchymal Stem Cells (MSCs), Hematopoietic Stem Cells (HSCs), Neural Stem Cells & Other Specialized Lineages), By Technology Platform, (Bioreactor-Based Expansion Systems, Two-Dimensional Planar Culture Systems, Microcarrier-Based Suspension Culture, Automated Closed-System Processing Platforms), By End-User, (Pharmaceutical & Biopharmaceutical Companies, CDMOs (Cell & Gene Therapy Focused), Academic Research Institutes & Biobanks, Hospitals & Cell Therapy Centers), By Product Type, (Cell Culture Media & Reagents, Bioreactors & Bioprocessing Equipment, CDMO Manufacturing Services, Cryopreservation Products, Quality Control & Testing Solutions)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Stem Cell Manufacturing Market

Published Date : 29 Apr 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date