- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Strategy Games Market Size Growth & Forecast | CAGR of 10.8%

Global Strategy Games Market Size, Share & Analysis By Device Type (Mobile, PC, Tablets, Other Device Types), By Business Model (Free-to-Play (Ad-Supported), Freemium, Subscription-Based), By Monetization Model, Esports Influence, Player Engagement Trends & Forecast 2025–2034

Report Overview

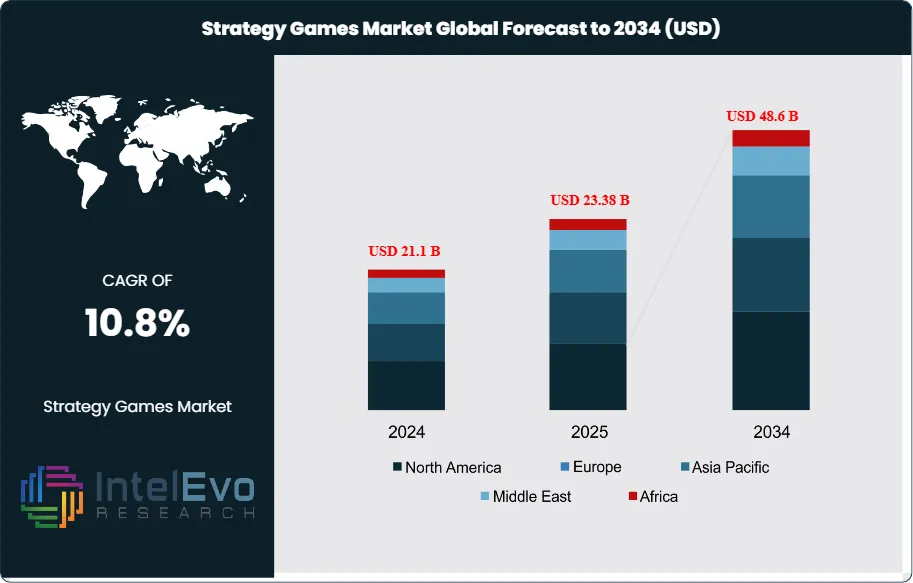

The Strategy Games Market is valued at approximately USD 21.1 billion in 2024 and is projected to reach nearly USD 48.6 billion by 2034, expanding at a CAGR of around 10.8% during 2025–2034. This surge reflects the explosive rise of mobile-first gaming, cross-platform ecosystems, and AI-driven live operations that keep players engaged longer. With esports visibility, influencer-powered discovery, and creator economies scaling rapidly, the strategy gaming segment is entering its most profitable decade. The mix of real-time PvP, social competition, and immersive content drops is transforming strategy games into global entertainment powerhouses.

Get More Information about this report -

Request Free Sample ReportGrowth reflects a steady broadening of the player base and rising monetization depth across premium, free-to-play, and live-service models. Asia-Pacific led with a 40.1% share in 2024—about USD 7.05 billion—supported by mobile-first engagement and competitive communities, while North America and Europe remain sizable revenue pools on PC and console. The forecast implies a net addition of approximately USD 20.8 billion and a near 2.2× expansion of addressable spend over the period, with the mix tilting toward always-online, multiplayer-centric formats.

Demand is underpinned by the intellectual appeal of real-time and turn-based strategy (RTS/TBS), esports-driven visibility, and deeper social loops that lift retention. On the supply side, digital distribution and cross-platform tooling lower barriers for independent studios, even as production values and live-ops expectations push up budgets and staffing needs. Key risks include platform-policy shifts, approval timelines in tightly regulated markets, data-privacy obligations that raise user-acquisition costs, and the ongoing need to balance monetization with fair-play design.

Technology is a central accelerant. Advancements in artificial intelligence and machine learning are yielding adaptive opponents, procedural map generation, and smarter matchmaking, elevating replayability and increasing lifetime value. Cloud infrastructure and analytics enable at-scale telemetry, rapid balance patches, and content cadence, while cross-play, cross-progression, and mod support expand network effects and extend product lifecycles. Automation in testing and content pipelines is shortening iteration cycles, allowing developers to respond faster to meta shifts without compromising stability.

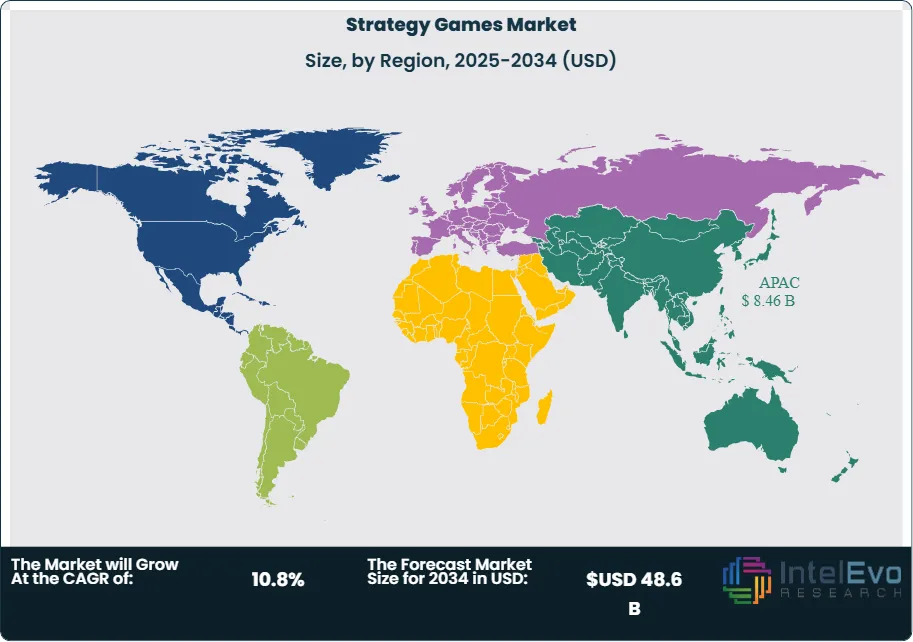

Regionally, Asia-Pacific is expected to remain the volume anchor, with mobile connectivity and competitive ecosystems in markets such as China, Korea, and Japan driving high engagement. Europe is an investment bright spot: targeted public funding—e.g., the UK’s grants of over £3 million to 22 studios and Germany’s ongoing program of up to €50 million annually covering as much as 50% of prototype costs—continues to catalyze studio formation and innovation. North America offers premium ARPU and franchise longevity, while emerging hotspots across India and Southeast Asia present outsized upside as payment penetration and local publishing partnerships mature. Collectively, these dynamics position strategy games for durable, innovation-led growth through 2034.

, By Business Model (Free-to-Play (Ad-Supported), Freemium, Subscription-Based), By Monetization Model, Esports Influence, Player Engagement Trends & Forecast 2025–2034")

Key Takeaways

- Market Growth: The global Strategy Games market totals USD 21.1 billion (2024) and is projected to reach USD 48.6 billion by 2034 (10.8% CAGR), adding ~USD 27.5 billion in incremental revenue; expansion is propelled by mobile penetration, live-service monetization, and AI-enhanced gameplay depth.

- Device Type: Mobile led with 42.3% revenue share in 2024 (≈USD 7.45 billion), underpinned by smartphone ubiquity, 5G connectivity, and shorter session loops suited to on-the-go play.

- Business Model: Freemium captured 54.0% of 2024 revenue (≈USD 9.50 billion), reflecting the strength of in-app purchases, battle passes, and live-ops events that extend lifetime value and monetize broad player funnels.

- Driver: Integration of AI/ML and competitive multiplayer is lifting engagement—adaptive opponents, procedural content, and smarter matchmaking sustain replayability and session length across RTS/TBS titles (e.g., Supercell, Lilith, Paradox, Sega/Creative Assembly).

- Restraint: Economics remain pressured by platform fees of up to 30% on major mobile storefronts and tightening privacy/IDFA regimes, which elevate user-acquisition costs and raise breakeven thresholds for midcore titles.

- Opportunity: Asia–Pacific (APAC), already at 40.1% share and USD 7.05 billion (2024), could exceed ~USD 15.4 billion by 2034 if it maintains current share; outsized upside exists in India and Southeast Asia via vernacular content, esports partnerships, and localized payments.

- Trend: The genre is shifting toward cross-platform, live-service strategies—cross-play/progression, rapid balance patches, and mod support—while AI-assisted content pipelines shorten release cycles; the freemium mix (54% in 2024) signals continued tilt to service-led monetization.

- Regional Analysis: APAC leads (40.1% share; USD 7.05 billion in 2024), while Europe benefits from public funding—e.g., UK grants of £3 million to 22 studios and Germany’s program of up to €50 million annually covering up to 50% of prototype costs—supporting innovation; North America remains a high-ARPU base for premium PC/console franchises.

Device Type Analysis

Mobile remains the growth engine of strategy gaming in 2025, building on its 2024 lead (42.3% share) as 5G penetration, mid-range GPU gains, and lower data costs expand the playable audience. On a 2025 market of roughly USD 20.6 billion (implied from an 8.1% CAGR off 2024), mobile is projected to approach the mid-40s share, or ≈USD 9.1 billion at a 44% mix, driven by mid-core titles with deeper live-ops and touch-optimized UI/UX. PCs retain a resilient second position, favored by real-time and grand-strategy enthusiasts who value precision controls, mod ecosystems, and high-fidelity simulations; premium + DLC monetization and long-tail engagement support stable ARPU even as player time fragments across platforms.

Tablets occupy a defensible niche for map-dense, turn-based play thanks to larger screens and stylus support, while “other device types” (handheld PCs, cloud-ready consoles, hybrid devices) are the fastest-growing tail as cross-play and cross-progression blur device boundaries. Handheld PC adoption (e.g., Steam Deck-class devices) and improving game-streaming latency are expanding portable access to PC-grade complexity—supporting an ecosystem where device choice tracks session length, input preference, and content depth rather than hardware constraints.

Business Model Analysis

Freemium continues to dominate monetization in 2025, scaling from a 54.0% share in 2024 to an expected mid-50s mix as battle passes, cosmetic IAPs, and seasonal content deepen conversion. At a 55% assumption, freemium would generate ≈USD 11.3 billion in 2025, led by live-service strategy titles that pair frequent balance patches with limited-time events to lift payer share and average revenue per paying user.

Free-to-Play (ad-supported) remains the cost-of-entry for casual and emerging-market cohorts, capturing a material low-30s share as rewarded video and interstitial formats improve eCPMs without excessive churn. Subscription-based models—still a minority but rising into the low-teens—benefit from platform bundles and content vaults that de-risk discovery while smoothing revenue for publishers. Key headwinds across models include platform fees (often up to 30%), privacy-driven UA friction, and the need for tighter economy design to maintain fair-play sentiment as monetization depth increases.

Regional Analysis

Asia Pacific retains global leadership in 2025, extending its 2024 position (40.1% share; USD 7.05 billion) toward ≈USD 8.2–8.4 billion as mobile-first ecosystems in China, South Korea, Japan, India, and Southeast Asia deepen competitive play, creator-led discovery, and microtransaction familiarity. High tournament visibility and publisher-run leagues continue to reinforce strategy genres’ watchability and community retention.

North America remains the highest-ARPU market, anchored by PC/console franchises and robust DLC/mod communities that lengthen lifecycles. Europe sustains a broad base of strategy studios and players, supported by a mix of premium and live-service models and ongoing public support programs that encourage prototyping and innovation. Latin America and the Middle East & Africa, though smaller today, are expanding faster than the global average—often at low double-digit CAGRs—on improving payments, localized publishing, and budget Android hardware. Net-net, regional dynamics favor mobile-led scale in APAC and emerging markets, with PC/console monetization depth preserving margin in North America and Europe, positioning the category for durable, geographically diversified growth beyond 2025.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Device Type

- Mobile

- PC

- Tablets

- Other Device Types

By Business Model

- Free-to-Play (Ad-Supported)

- Freemium

- Subscription-Based

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2024) | USD 21.1 B |

| Forecast Revenue (2034) | USD 48.6 B |

| CAGR (2024-2034) | 10.8% |

| Historical data | 2020-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Device Type (Mobile, PC, Tablets, Other Device Types), By Business Model (Free-to-Play (Ad-Supported), Freemium, Subscription-Based) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Relic Entertainment, Ubisoft Entertainment SA, Bandai Namco Entertainment, Firaxis Games, Epic Games, Inc., Nintendo Co., Ltd., Creative Assembly, Blizzard Entertainment, Inc., Paradox Interactive AB, Electronic Arts Inc., Other Key Player |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Business Model (Free-to-Play (Ad-Supported), Freemium, Subscription-Based), By Monetization Model, Esports Influence, Player Engagement Trends & Forecast 2025–2034")

, By Business Model (Free-to-Play (Ad-Supported), Freemium, Subscription-Based), By Monetization Model, Esports Influence, Player Engagement Trends & Forecast 2025–2034")

, By Business Model (Free-to-Play (Ad-Supported), Freemium, Subscription-Based), By Monetization Model, Esports Influence, Player Engagement Trends & Forecast 2025–2034")

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date