- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Subscription Economy Market Size, Trends & Forecast 2034 | 15.9% CAGR

Global Subscription Economy Market Size, Share, Analysis Report By Service Type (Membership Subscriptions, Content Subscriptions, Service Subscriptions, Product Subscriptions), Industry Vertical(Food & Beverage, Media & Entertainment, Transportation & Mobility, Information Technology, Healthcare & Wellness, E-commerce & Retail, Education, Others), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034

Report Overview:

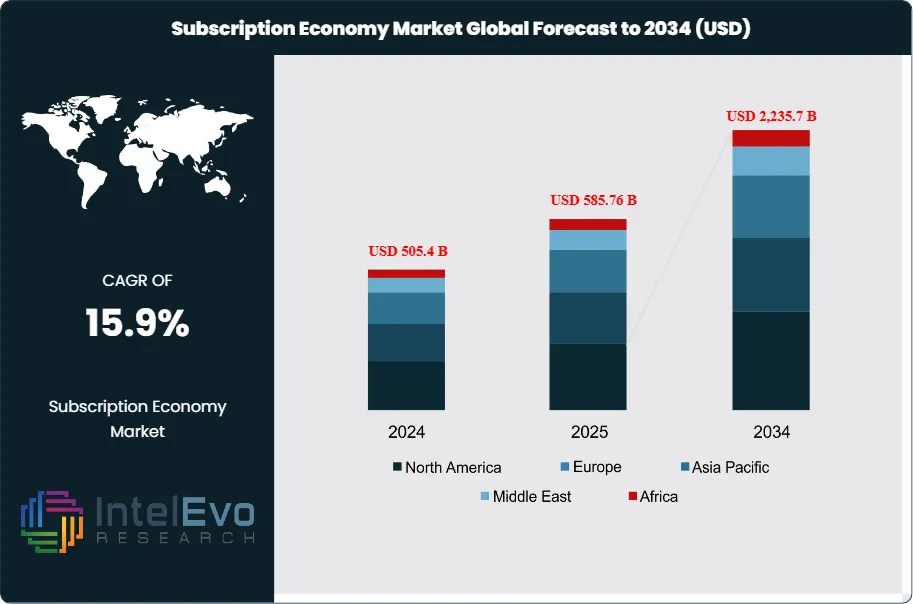

The Subscription Economy Market size is projected to reach approximately USD 2,235.7 Billion by 2034, up from USD 505.4 Billion in 2024, growing at a CAGR of 15.9% during the forecast period from 2025 to 2034. This robust growth is fueled by the accelerating adoption of subscription-based business models across industries such as media & entertainment, SaaS, e-commerce, automotive, and consumer goods. As consumers increasingly favor convenience and value-driven access over ownership, the subscription economy is reshaping global commerce dynamics. The rise of AI-powered personalization, flexible billing systems, and customer retention analytics is redefining brand loyalty and customer lifetime value, positioning subscription services at the core of the digital transformation era.

Get More Information about this report -

Request Free Sample ReportThe Subscription Economy describes a business model where consumers access products and services through recurring payments rather than one-time purchases. This approach spans membership subscriptions, content subscriptions, service subscriptions, and product subscriptions, reflecting the shift from ownership to access. Various industries ranging from media & entertainment and healthcare & wellness to e-commerce & retail are leveraging subscriptions to create predictable revenue streams and deepen customer relationships. Key factors fueling market growth include the proliferation of high-speed internet, the need for convenience, and changing consumer attitudes that favor experience and flexibility over ownership. Moreover, innovations in cloud technology and digital payment systems have made it easier for companies to launch and scale subscription-based models globally.

The market is further influenced by demographic trends and technological convergence. Millennials and Gen Z consumers are particularly inclined toward subscription services, valuing personalization, seamless user experiences, and instant access to digital and physical products. Additionally, companies such as Netflix, Spotify, and Adobe have set benchmarks for subscriber acquisition and retention strategies, encouraging businesses in diverse sectors to emulate their success. However, the market faces challenges such as subscription fatigue, data privacy regulations, and high churn rates, which companies must address through differentiated offerings and robust customer engagement strategies.

North America led the subscription e-commerce market with the largest share of 38% in 2024. This regional dominance stems from advanced digital infrastructure, high disposable income levels, established credit card penetration, and early adoption of innovative business models. The region's mature technology ecosystem, venture capital availability, and consumer willingness to embrace new service models create ideal conditions for subscription business growth and innovation.

The COVID-19 pandemic served as a significant catalyst for subscription economy acceleration, fundamentally altering consumer behavior and business operations across global markets. Lockdown measures and social distancing requirements drove massive adoption of digital services, streaming platforms, meal delivery subscriptions, and remote work tools, creating unprecedented demand for subscription-based solutions. The pandemic highlighted the value proposition of subscription models in providing continuous access to essential services, entertainment, and products during periods of uncertainty and limited mobility. Many consumers developed subscription habits during the pandemic that have persisted beyond lockdown periods, contributing to sustained market growth and permanent shifts in consumption patterns toward subscription-based models.

, Industry Vertical(Food & Beverage, Media & Entertainment, Transportation & Mobility, Information Technology, Healthcare & Wellness, E-commerce & Retail, Education, Others), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

Key Takeaways:

- Market Growth: The Subscription Economy Market is expected to reach USD 2,235.7 Billion by 2034, driven by digital transformation and consumer demand for convenience. Businesses across sectors are pivoting to subscriptions as a reliable revenue model.

- Service Type Dominance: Content subscriptions remain the largest segment, driven by platforms like Netflix, Disney+, and Spotify. Consumers increasingly favor on-demand access to entertainment over traditional ownership models.

- Industry Vertical Dominance: The media and entertainment industry leads the verticals, reflecting the surging appetite for streaming video, music, and gaming services.

- Driver: Technological advancements in cloud computing and digital payments have removed barriers to entry, empowering businesses to scale subscription services rapidly.

- Restraint: Subscription fatigue is a growing challenge, as consumers juggle multiple recurring charges, leading to higher churn and resistance to new subscriptions.

- Opportunity: Emerging markets present vast potential for expansion, especially in Asia-Pacific, where rising disposable income and internet access can unlock new subscriber bases.

- Trend: Personalization and AI-driven recommendations are transforming subscription experiences, enabling companies to boost retention and engagement through tailored offerings.

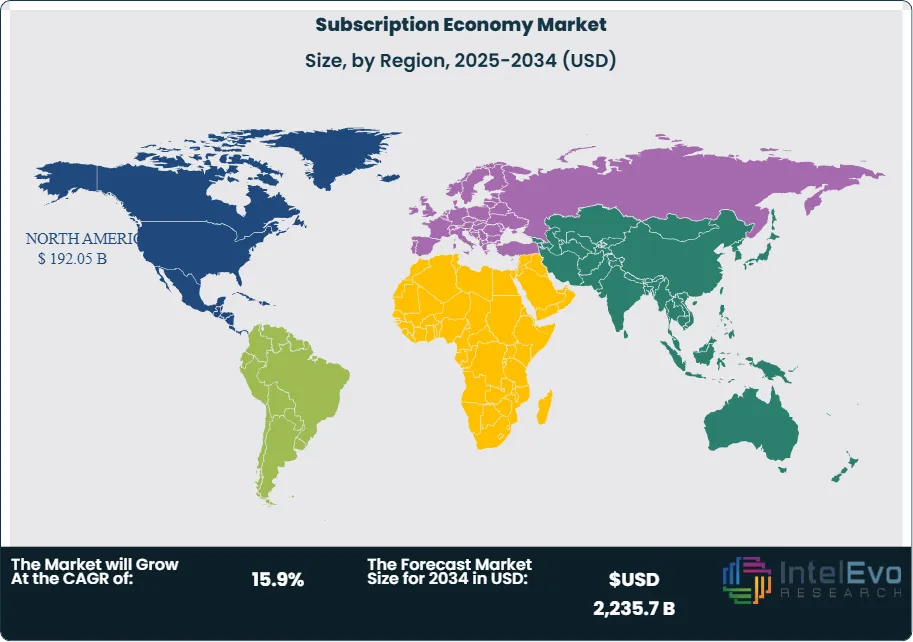

- Regional Analysis: North America leads the market owing to mature consumer readiness and robust technology infrastructure, while Asia Pacific is expected to witness the fastest growth.

Service Type Analysis:

Content subscriptions maintain their dominant position in the subscription economy, driven by the proliferation of streaming services, digital media platforms, and educational content providers. This segment benefits from continuous content creation, global content libraries, and sophisticated recommendation algorithms that enhance user engagement and retention. The success of platforms like Netflix, Spotify, and Disney+ demonstrates the scalability and profitability of content subscription models across different entertainment categories. Service subscriptions represent a rapidly growing segment encompassing cloud computing, software-as-a-service (SaaS), professional services, and digital tools. This category benefits from business digital transformation initiatives, remote work adoption, and the need for scalable, accessible solutions that can be accessed from anywhere. The B2B segment within service subscriptions shows particularly strong growth as enterprises seek cost-effective, flexible solutions for their operational needs.

Industry Vertical Analysis:

Media & Entertainment Leads With more than 40% Market Share In Subscription Economy Market. Media & Entertainment leads industry vertical adoption, encompassing streaming video, music, gaming, news, and digital publications. This sector benefits from global content distribution capabilities, personalized recommendation systems, and the ability to create binge-worthy experiences that drive subscriber engagement. The segment continues to evolve with live streaming, interactive content, and social viewing experiences that enhance the subscription value proposition. Information Technology represents the fastest-growing vertical, driven by cloud computing adoption, SaaS platform proliferation, and digital transformation initiatives across industries. This segment includes everything from productivity software and development tools to cybersecurity services and data analytics platforms. The B2B focus of many IT subscriptions provides higher average revenue per user and longer customer lifetime values.

Region Analysis:

North America Leads With over 45% Market Share In Subscription Economy Market. North America maintains its leadership position in the subscription economy, accounting for 38% of global market share, driven by several key factors including advanced digital infrastructure, high internet penetration rates, established credit card usage, and consumer willingness to adopt innovative service models. The United States dominates the regional market with major subscription platforms including Netflix, Spotify, Amazon Prime, and numerous SaaS providers that serve global audiences from American headquarters. Canada contributes significantly through its tech-forward population and supportive regulatory environment for digital services.

Europe represents the second-largest market, characterized by diverse regulatory environments, strong consumer protection laws, and varying subscription adoption rates across countries. The United Kingdom, Germany, and Nordic countries lead European adoption through high digital literacy rates and disposable income levels. The region's focus on data privacy and consumer rights creates both opportunities and challenges for subscription businesses.

Asia Pacific emerges as the fastest-growing region, fueled by rapid smartphone adoption, expanding middle-class populations, and improving digital payment infrastructure. China and India lead growth through massive user bases, local platform development, and government initiatives supporting digital economy expansion. The region's diverse economic conditions and regulatory environments create complex but lucrative expansion opportunities.

Latin America and Africa represent emerging markets with significant potential as mobile infrastructure improves and digital payment adoption increases. These regions benefit from leapfrogging traditional payment systems directly to mobile-based solutions, creating opportunities for subscription models that bypass traditional banking requirements.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Subscription Model Type

- Product-Based Subscriptions

- Service-Based Subscriptions

- Content & Digital Media Subscriptions

- Hybrid Subscription Models (Product + Service)

- Membership Subscriptions

By Payment and Billing Type

- Fixed Subscription

- Usage-Based Subscription

- Tiered or Freemium Models

- Pay-as-You-Go Models

- Lifetime Access Subscriptions

By Platform Type

- Web-Based Platforms

- Mobile App-Based Platforms

- Hybrid Platforms

- API-Integrated Platforms

By Enterprise Size

- Small & Medium Enterprises (SMEs)

- Large Enterprises

By End-Use Industry

- Media & Entertainment (Streaming, OTT Platforms)

- Software & SaaS

- E-commerce & Retail

- Automotive & Mobility Services

- Telecommunications

- Healthcare & Fitness

- Education & E-learning

- Financial Services (FinTech & InsurTech)

- Others (Travel, Gaming, Consumer Goods)

By Region

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 585.76 B |

| Forecast Revenue (2034) | USD 2,235.7 B |

| CAGR (2025-2034) | 15.9% |

| Historical data | 2018-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Subscription Model Type (Product-Based Subscriptions, Service-Based Subscriptions, Content & Digital Media Subscriptions, Hybrid Subscription Models (Product + Service), Membership Subscriptions), By Payment and Billing Type (Fixed Subscription, Usage-Based Subscription, Tiered or Freemium Models, Pay-as-You-Go Models, Lifetime Access Subscriptions), By Platform Type (Web-Based Platforms, Mobile App-Based Platforms, Hybrid Platforms, API-Integrated Platforms), By Enterprise Size (Small & Medium Enterprises (SMEs), Large Enterprises), By End-Use Industry (Media & Entertainment (Streaming, OTT Platforms), Software & SaaS, E-commerce & Retail, Automotive & Mobility Services, Telecommunications, Healthcare & Fitness, Education & E-learning, Financial Services (FinTech & InsurTech), Others (Travel, Gaming, Consumer Goods)) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Netflix, Zipcar, Spotify, Blue Apron, Disney+, HelloFresh, Xbox Game Pass, Teladoc, Microsoft, Peloton, Adobe, Salesforce, Amazon Prime, Zoom |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, Industry Vertical(Food & Beverage, Media & Entertainment, Transportation & Mobility, Information Technology, Healthcare & Wellness, E-commerce & Retail, Education, Others), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

, Industry Vertical(Food & Beverage, Media & Entertainment, Transportation & Mobility, Information Technology, Healthcare & Wellness, E-commerce & Retail, Education, Others), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

, Industry Vertical(Food & Beverage, Media & Entertainment, Transportation & Mobility, Information Technology, Healthcare & Wellness, E-commerce & Retail, Education, Others), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date