- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Subsea Production System Market Size, Share & Growth | CAGR 10.8%

Global Subsea Production System Market Size, Share, Analysis By Equipment Type (Subsea Trees, Umbilicals Risers & Flowlines, Subsea Manifolds, Subsea Control Systems, Subsea Processing Equipment), By Water Depth (Shallow Water, Deepwater, Ultra-Deepwater), By Application (Oil Production, Gas Production, Subsea Processing Including Boosting, Separation & Compression), By End-User (International Oil Companies, National Oil Companies, Independent Operators, EPC & Oilfield Services) Industry Region & Key Players – Market Dynamics, Competitive Strategies, Trends & Forecast 2026–2034

Report Overview

| Market Size | Forecast Value | CAGR | Leading Region |

|---|---|---|---|

| USD 14.2 Billion, 2025 | USD 35.8 Billion, 2034 | 10.8%, 2026–2034 | Europe, 28.4%, 2025 |

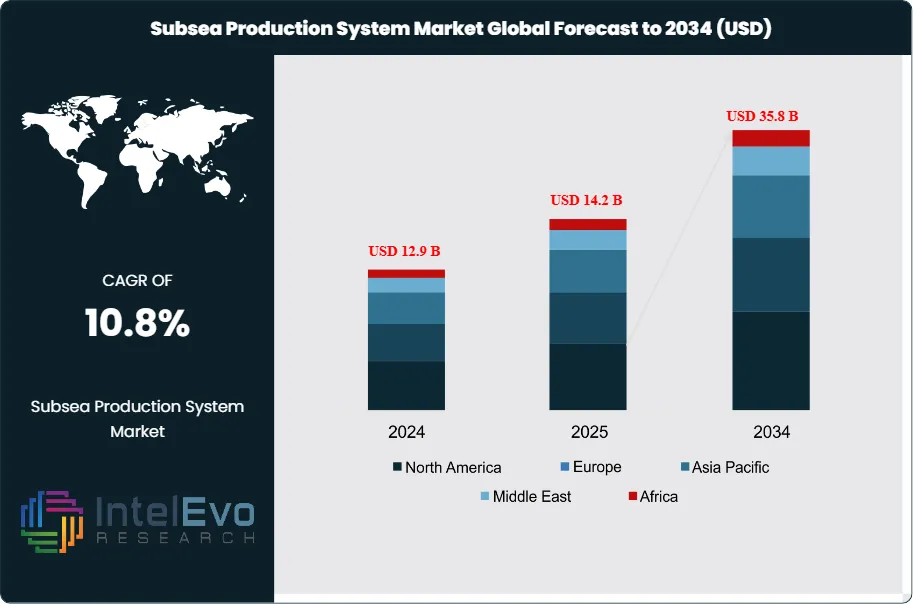

The Subsea Production System Market was valued at approximately USD 12.9 Billion in 2024 and increased to USD 14.2 Billion in 2025. The market is projected to reach nearly USD 35.8 Billion by 2034, expanding at a compound annual growth rate (CAGR) of 10.8% during the forecast period from 2026 to 2034. The subsea production system market is experiencing a sustained recovery and expansion cycle driven by renewed deepwater exploration programs, rising offshore capital expenditure commitments from international and national oil companies, and the technical maturation of all-electric subsea architectures that are lowering the cost threshold for frontier deepwater developments. Subsea production systems, encompassing subsea trees, manifolds, umbilicals, risers, flowlines, and associated control systems, form the critical hardware infrastructure that enables hydrocarbon extraction from seabed reservoirs at water depths ranging from 300 meters to over 3,000 meters.

Get More Information about this report -

Request Free Sample ReportDemand forces driving the subsea production system market include the depletion of shallow-water reserves that is compelling operators to develop increasingly deep and remote offshore fields, the strong price environment supporting deepwater project economics, and the growing backlog of final investment decisions across pre-salt basins in Brazil, deepwater West Africa, and ultra-deepwater Gulf of Mexico developments. Supply-side dynamics reflect competitive pressure among the major subsea equipment manufacturers, with SLB, TechnipFMC, Baker Hughes, and Aker Solutions competing intensively on system integration capability, delivery lead times, and total lifecycle cost propositions. The subsea production system market benefits from the multi-year project development timelines that create sustained order backlog visibility for established equipment vendors.

Regulatory frameworks across major offshore producing regions are influencing subsea production system design requirements and certification standards. The Bureau of Safety and Environmental Enforcement in the United States mandates rigorous blowout preventer and well control equipment standards for deepwater Gulf of Mexico operations, driving demand for advanced subsea control and safety systems. The Norwegian Petroleum Directorate maintains some of the world's most demanding technical standards for subsea equipment qualification, which has historically driven Norwegian-based vendors including Aker Solutions and Equinor to develop market-leading engineering capabilities. Brazil's National Agency of Petroleum regulates local content requirements for subsea equipment procurement, incentivizing international vendors to establish Brazilian manufacturing presence.

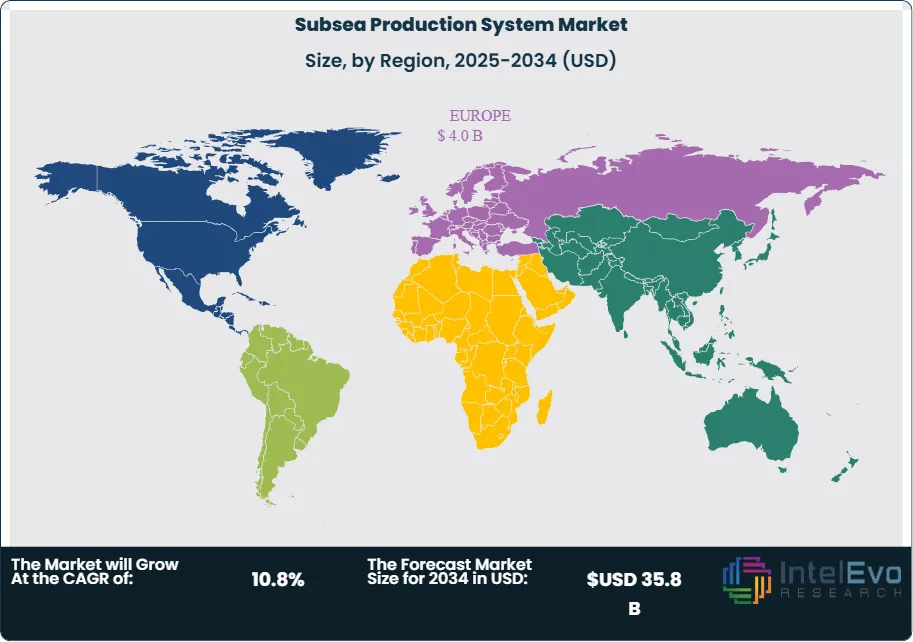

Risk factors in the subsea production system market include oil price volatility that can delay or cancel deepwater final investment decisions, the long lead times for complex subsea system fabrication that create schedule and cost risk, and supply chain constraints for specialized subsea materials including high-grade duplex stainless steel and subsea-rated electrical components. The market is also navigating the energy transition, with operators requiring subsea systems designed for carbon capture and storage applications alongside conventional hydrocarbon production. Europe leads regional market share with 28.4% of global subsea production system revenue in 2025 at USD 4.0 Billion, anchored by North Sea activity. Latin America follows closely at 26.8% of market revenue at USD 3.8 Billion, driven by Brazilian pre-salt developments. By 2034, autonomous and all-electric subsea production systems are projected to define the technological frontier of the market, reshaping vendor competitive positioning across the global subsea production system landscape.

, By Water Depth (Shallow Water, Deepwater, Ultra-Deepwater), By Application (Oil Production, Gas Production, Subsea Processing Including Boosting, Separation & Compression), By End-User (International Oil Companies, National Oil Companies, Independent Operators, EPC & Oilfield Services) Industry Region & Key Players – Market Dynamics, Competitive Strategies, Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The global subsea production system market was valued at USD 14.2 Billion in 2025 and is projected to reach USD 35.8 Billion by 2034, registering a CAGR of 10.8% during the forecast period 2025–2034, driven by rising deepwater capital investment and expanding all-electric subsea system adoption.

- Segment Dominance (By Equipment): Subsea trees are the dominant equipment segment in the subsea production system market, accounting for 31.4% of revenue in 2025 at USD 4.5 Billion, underpinned by steady deepwater well completions across the Gulf of Mexico, Brazilian pre-salt basins, and West African deepwater blocks.

- Segment Dominance (By Application): Deepwater applications lead the subsea production system market by water depth category, commanding 58.6% of revenue in 2025 at USD 8.3 Billion, as operators concentrate capital investment in reservoirs located between 300 and 1,500 meters water depth across the Atlantic basin.

- Driver: The accelerating global deepwater exploration and production investment cycle, with offshore upstream capital expenditure growing at 14.2% annually in 2025 and projected to reach USD 142 Billion by 2028, is creating sustained demand for subsea trees, manifolds, and integrated production control systems across frontier deepwater basins.

- Restraint: Extended equipment lead times of 18–36 months for complex subsea tree and manifold fabrication create project schedule risk and limit the ability of the subsea production system market to respond rapidly to accelerating operator demand, with supply chain bottlenecks estimated to constrain market growth by 1.2–1.8 percentage points annually.

- Opportunity: All-electric subsea production system architectures represent a USD 6.4 Billion addressable opportunity within the market by 2034. Current all-electric system installations cover less than 7% of global active subsea production infrastructure as of 2025, with the majority of technically viable conversion candidates remaining on conventional hydraulic control architectures.

- Trend: Subsea processing technology adoption, encompassing seabed boosting, separation, and compression systems, is growing at 22.8% annually in 2025 as operators deploy in-field boosting to arrest production decline and extend economic field life without expensive topside facility modifications.

- Regional Analysis: Europe leads the global subsea production system market with a 28.4% share in 2025, equivalent to USD 4.0 Billion, anchored by North Sea and Norwegian Continental Shelf deepwater activity and the presence of world-leading subsea technology vendors including Aker Solutions and TechnipFMC.

Competitive Landscape

The Global Subsea Production System Market is moderately consolidated. The top four companies accounted for an estimated 42–45% of global market revenue in 2025. Competition is technology-driven and execution-focused, with strength in subsea trees, SURF systems (umbilicals, risers, and flowlines), integrated EPC delivery, and all-electric subsea solutions shaping competitive positioning more than pricing alone. Competitive intensity increased through 2025 and early 2026 as operators favored integrated subsea packages and long-term framework agreements, while consolidation and strategic partnerships continued across the offshore value chain.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| TECHNIPFMC | UK | Leader | iEPCI integrated subsea production systems, SURF solutions | Brazil, Guyana, West Africa, global deepwater | Secured multiple Petrobras and ExxonMobil Guyana subsea EPC awards in 2025, strengthening backlog visibility. |

| SLB (OneSubsea) | US | Leader | Integrated subsea production systems, subsea boosting & processing | North America, Middle East, Southeast Asia | Expanded subsea boosting projects and deepwater contracts in Gulf of Mexico and Asia in 2025. |

| BAKER HUGHES | US | Leader | Subsea trees, control systems, integrated well systems | Brazil, North America, Africa | Won subsea tree and control system contracts with Petrobras and other offshore operators in 2025. |

| AKER SOLUTIONS | Norway | Leader | Subsea production systems, all-electric subsea technology | North Sea, Brazil, global offshore | Advanced all-electric subsea tree deployments with Equinor and secured multiple North Sea contracts. |

| SUBSEA7 | Luxembourg | Challenger | SURF installation and subsea engineering services | Europe, Africa, Middle East | Continued strategic combination efforts with Saipem and expanded offshore installation backlog in 2026. |

| SAIPEM | Italy | Challenger | Offshore EPC and subsea system integration | Middle East, Mediterranean, Africa | Won major offshore EPC contracts in Middle East and expanded subsea project portfolio in 2025. |

| OCEANEERING INTERNATIONAL | US | Challenger | ROV services, subsea intervention, control systems | North America, global deepwater | Expanded vessel-based subsea services and secured long-term offshore support agreements in 2025. |

| DRIL-QUIP | US | Niche Player | Subsea wellheads, connectors, production systems | North America, Asia-Pacific | Strengthened subsea equipment portfolio and secured new deepwater wellhead contracts in 2025. |

| EXPRO GROUP | UK | Niche Player | Subsea well access, intervention, and flow management | Europe, Middle East, Africa | Expanded subsea intervention services and integrated well access offerings in 2025. |

| NEXANS / PRYSMIAN | France / Italy | Niche Player | Subsea cables, umbilicals, power transmission systems | Europe, offshore wind & oilfields | Secured long-term subsea cable and umbilical supply agreements for offshore energy projects in 2025. |

Segmentation Analysis

The subsea production system market segmentation analysis examines the market across four key dimensions: By Equipment Type, By Water Depth, By Application, and By Region. Each dimension reveals distinct demand patterns, technology requirements, and competitive dynamics that collectively define the global subsea production system market structure through 2034.

By Equipment Type

Subsea trees constitute the largest equipment segment within the subsea production system market, holding a 31.4% share in 2025 at USD 4.5 Billion. Subsea trees, comprising horizontal and vertical tree configurations, provide the primary well control and flow management interface between the wellbore and the subsea production manifold. Horizontal trees dominate new deepwater well completions due to their installation efficiency and compatibility with subsea intervention tooling, while vertical trees maintain relevance in shallower water applications and well workovers. The subsea tree segment benefits from steady deepwater drilling activity across the Gulf of Mexico, pre-salt Brazil, and deepwater West Africa, with major tree vendors SLB, TechnipFMC, and Baker Hughes investing in all-electric tree designs that eliminate hydraulic fluid dependency and reduce maintenance intervention frequency.

Umbilicals, risers, and flowlines collectively represent 27.8% of the subsea production system market in 2025 at USD 3.9 Billion. Umbilicals provide the critical electrical, hydraulic, and chemical injection connectivity between topside facilities and seabed production equipment, while risers and flowlines transport produced fluids from the seabed to surface processing facilities. The segment is driven by the lengthening tiebacks associated with remote field developments, where flow assurance challenges require more sophisticated insulated and heated flowline systems to prevent hydrate and wax deposition. Subsea manifolds account for 18.6% of market revenue at USD 2.6 Billion, serving as subsea flow network hubs that consolidate production from multiple wells. Subsea control systems represent 13.2% of revenue at USD 1.9 Billion, while subsea processing equipment including pumps, separators, and compressors accounts for 9.0% at USD 1.3 Billion in 2025.

By Water Depth

Deepwater applications, defined as water depths between 300 and 1,500 meters, dominate the subsea production system market by water depth with a 58.6% share in 2025 at USD 8.3 Billion. The deepwater segment encompasses the majority of active subsea production infrastructure globally, concentrated in the Gulf of Mexico, Brazilian Santos and Campos Basins, West African deepwater blocks, and the Norwegian Continental Shelf. Deepwater field economics have improved significantly through design standardization, long-distance tieback development strategies, and advancing subsea processing technologies that extend plateau production rates and reduce topside infrastructure requirements. The segment benefits from a well-established technology base and proven contractor capabilities that reduce execution risk compared to ultra-deepwater developments.

Ultra-deepwater applications, covering water depths exceeding 1,500 meters, hold a 28.4% share of the subsea production system market in 2025 at USD 4.0 Billion. Ultra-deepwater developments including the Brazilian pre-salt Santos Basin fields at 2,000–3,000 meters water depth, the Mozambique Area 1 LNG development, and Gulf of Mexico Paleogene discoveries represent the growth frontier for subsea production system technology. These developments require advanced high-pressure high-temperature rated subsea trees, dynamic riser systems capable of withstanding extreme ocean current environments, and sophisticated flow assurance strategies for long-distance tieback architectures. Shallow water applications at depths below 300 meters account for 13.0% of market revenue at USD 1.8 Billion in 2025, representing predominantly brownfield activity in mature offshore basins.

By Application

Oil production is the dominant application within the subsea production system market, accounting for 62.4% of revenue in 2025 at USD 8.9 Billion. Oil-focused subsea production systems encompass the full range of equipment deployed across conventional and pre-salt deepwater oil fields, including single-phase and multiphase subsea trees, oil export flowlines, and production control systems calibrated for reservoir pressure and fluid characteristics. The application is particularly concentrated in the Atlantic-facing deepwater basins where major pre-salt and post-salt oil discoveries continue to drive new subsea infrastructure investment. Major oil-producing operators including Petrobras, ExxonMobil, Shell, and TotalEnergies are the primary demand drivers, with combined subsea capital expenditure estimated at over USD 8 Billion annually in 2025.

Gas production applications represent 24.8% of the subsea production system market in 2025 at USD 3.5 Billion, driven by deepwater gas field developments in East Africa, the Mediterranean, and Southeast Asia where LNG project economics justify the capital intensity of long-distance subsea tieback architectures. Gas-focused subsea systems require specialized flow assurance solutions for hydrate prevention over long seabed flowline distances, driving demand for chemical injection umbilicals and heated pipeline systems. Subsea processing applications covering boosting, separation, and gas compression represent 12.8% of market revenue at USD 1.8 Billion in 2025, growing at above-market rates as operators deploy seabed processing to arrest production decline in mature deepwater fields without costly platform modifications.

By End-User

International oil companies constitute the largest end-user segment in the subsea production system market, accounting for 48.6% of revenue in 2025 at USD 6.9 Billion. Entities including ExxonMobil, Shell, BP, TotalEnergies, Chevron, and Equinor operate the largest deepwater asset portfolios globally and drive the procurement decisions that define subsea equipment market dynamics. These operators typically manage long-term framework agreements with major subsea system suppliers, securing preferential pricing and delivery commitments across multi-project portfolios. National oil companies represent 38.4% of market revenue in 2025 at USD 5.5 Billion, with Petrobras, ADNOC, ONGC, and Malaysia's Petronas committing substantial subsea capital programs across their respective deepwater development pipelines.

Independent oil companies account for 13.0% of the subsea production system market in 2025 at USD 1.8 Billion. Independents including Kosmos Energy, Tullow Oil, and Harbour Energy operate deepwater assets primarily in West Africa, the North Sea, and Latin America, typically relying on leased FPSO vessels and standardized subsea equipment to manage capital efficiency. The independent segment is particularly sensitive to oil price movements and financing conditions, making it the most cyclically variable end-user category. Oilfield services companies and engineering procurement construction firms account for the remaining 0.8% as direct equipment procurers for service-operated subsea installations.

Regional Analysis

Europe Subsea Production System Market

Europe leads the global subsea production system market with a 28.4% share in 2025, equivalent to USD 4.0 Billion in revenue. Norway is the dominant country market, with Equinor, Aker BP, and Vår Energi collectively operating the world's most advanced subsea production infrastructure across the Norwegian Continental Shelf. Norway's Johan Sverdrup Phase 2, Kristin South, and Yggdrasil field developments represent active subsea system procurement programs in 2025, with combined subsea hardware investment estimated at over USD 1.2 Billion. The Norwegian market benefits from the world's highest concentration of subsea technology expertise, with Aker Solutions, Kongsberg, and Nexans headquartered in Norway and operating globally from their Norwegian development centers.

The United Kingdom contributes approximately 28% of European subsea production system market revenue in 2025, driven by North Sea subsea tieback developments and brownfield life extension programs across mature fields including Clair, Culzean, and Rosebank. The UK North Sea Transition Deal includes commitments to maintain offshore production capacity through digital and subsea technology investment, providing policy support for continued subsea system procurement. Scotland's subsea engineering services ecosystem, concentrated in Aberdeen and Wick, provides a deep talent pool for subsea project execution. The United Kingdom's Offshore Petroleum Regulator for Environment and Decommissioning is developing subsea equipment standards that align with net-zero emissions goals, influencing design requirements for new subsea system installations. Europe is projected to grow at a CAGR of 9.8% through 2034.

Latin America Subsea Production System Market

Latin America holds a 26.8% share of the global subsea production system market in 2025, valued at USD 3.8 Billion, ranking as the second-largest regional market. Brazil is the overwhelmingly dominant country market, accounting for approximately 88% of Latin American subsea production system revenue, driven by Petrobras's massive pre-salt Santos and Campos Basin development program. Petrobras's Strategic Plan 2024–2028 allocates USD 51.6 Billion to upstream oil and gas investment, with deepwater pre-salt developments representing the core capital program. The pre-salt reservoirs located at water depths of 2,000–3,000 meters below reservoirs covered by thick salt layers require specialized subsea tree configurations, high-pressure rated flowlines, and advanced flow assurance systems capable of managing reservoir fluids at extreme temperature and pressure conditions.

Brazil's National Agency of Petroleum local content regulations require that a defined percentage of subsea equipment value be manufactured within Brazil, incentivizing major international vendors including TechnipFMC, SLB, and Baker Hughes to establish Brazilian manufacturing facilities. TechnipFMC operates a large subsea equipment manufacturing facility in Vitoria, Brazil, which supplies a significant proportion of the subsea trees and manifolds deployed in Santos Basin pre-salt developments. Guyana is emerging as a significant secondary market within Latin America, with ExxonMobil, Hess, and CNOOC deploying multiple FPSO-based subsea production systems across the Stabroek block that contains recoverable resources estimated at over 11 Billion barrels. Latin America is projected to grow at a CAGR of 11.8% through 2034.

Asia Pacific Subsea Production System Market

Asia Pacific accounts for 20.4% of the global subsea production system market in 2025, generating USD 2.9 Billion in revenue. Australia is the dominant country market within the region, driven by subsea tieback developments associated with LNG operations in the Carnarvon Basin, including Woodside Energy's Scarborough and Browse developments which require extensive deepwater subsea infrastructure to connect remote wellheads to existing LNG processing facilities. Australia's offshore regulator, NOPSEMA, enforces rigorous subsea equipment integrity standards that align with North Sea best practices, supporting the deployment of premium-specification subsea systems across Australian deepwater operations.

Malaysia is the second-largest Asia Pacific market, with Petronas deploying subsea production systems across its deepwater Sabah and Sarawak offshore blocks, including the Kasawari gas field development at approximately 1,400 meters water depth. Indonesia represents a growing opportunity as Pertamina and its production-sharing partners develop subsea tieback solutions for deepwater blocks in the Makassar Strait and Banda Sea. India's ONGC is pursuing deepwater subsea developments in the Bay of Bengal and along the eastern continental shelf, with the KG-DWN-98/2 block requiring significant subsea hardware investment. China's CNOOC is expanding deepwater activity in the South China Sea, deploying subsea production systems at the Lingshui 17-2 and related deepwater gas fields. Asia Pacific is projected to grow at a CAGR of 11.4% through 2034.

North America Subsea Production System Market

North America holds a 16.2% share of the global subsea production system market in 2025, equivalent to USD 2.3 Billion in revenue. The United States Gulf of Mexico deepwater basin is the dominant North American market, with operators including Shell, BP, Chevron, and Murphy Oil deploying subsea production systems across Paleogene and Miocene oil developments. The Gulf of Mexico deepwater market is characterized by high-value, technically complex projects requiring advanced subsea tree designs capable of handling high-pressure high-temperature reservoir conditions. The BSEE's well control regulations enacted following the 2010 Deepwater Horizon incident have driven significant upgrades to subsea blowout preventer and control system specifications across the Gulf of Mexico operating environment.

Canada's East Coast offshore market, centered on Newfoundland's Jeanne d'Arc Basin, hosts established FPSO-based subsea production developments including Hibernia, Terra Nova, and White Rose fields, with life extension programs driving continued subsea equipment investment. Mexico's deepwater Gulf development ambitions under Pemex and private operator licenses represent a longer-term growth opportunity, with water depth capabilities increasing as regulatory frameworks and contractor ecosystems mature. The United States market benefits from world-class deepwater project execution capabilities concentrated in Houston, where the majority of deepwater project management and engineering activities for Gulf of Mexico developments are conducted. North America is projected to grow at a CAGR of 9.6% through 2034.

Middle East & Africa Subsea Production System Market

The Middle East and Africa segment accounts for 8.2% of global subsea production system market revenue in 2025, totaling USD 1.2 Billion. West Africa is the dominant sub-region, with Nigeria, Angola, and Senegal hosting active deepwater subsea production development programs. Nigeria's deepwater blocks operated by Shell, TotalEnergies, ExxonMobil, and Chevron contain producing subsea fields in the Bonga, Erha, and Agbami developments, with next-generation deepwater projects including Bonga North and Zabazaba requiring significant subsea system investment. Angola's Total-operated Cameia and Golfinho developments in Block 20/11 and Block 15/06 represent active subsea hardware procurement programs, with the Angolan government's oil company Sonangol mandating local content provisions for offshore equipment supply.

Senegal and Mauritania's Greater Tortue Ahmeyim LNG development, operated by BP and Kosmos Energy, represents a major subsea production system deployment in West Africa, with floating LNG processing connected to deepwater subsea wells via long-distance tieback flowlines. South Africa's deepwater potential is being assessed through exploration programs in the Orange Basin, where significant gas discoveries have been made, with subsea development feasibility studies underway. The Middle East itself contributes modestly to the subsea production system market, with UAE and Saudi Arabian offshore developments primarily in shallower water depths that require less complex subsea architectures. East Africa's Mozambique LNG developments, though experiencing execution delays, represent a significant pending subsea equipment procurement opportunity. The Middle East and Africa region is projected to grow at a CAGR of 12.6% through 2034.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Equipment Type

- Subsea Trees

- Umbilicals, Risers, and Flowlines

- Subsea Manifolds

- Subsea Control Systems

- Subsea Processing Equipment

By Water Depth

- Deepwater (300–1,500 meters)

- Ultra-Deepwater (above 1,500 meters)

- Shallow Water (below 300 meters)

By Application

- Oil Production

- Gas Production

- Subsea Processing (Boosting, Separation, Compression)

By End-User

- International Oil Companies

- National Oil Companies

- Independent Oil Companies

- Oilfield Services and EPC Companies

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 14.2 B |

| Forecast Revenue (2034) | USD 35.8 B |

| CAGR (2025-2034) | 10.8% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Equipment Type (Subsea Trees, Umbilicals, Risers, and Flowlines, Subsea Manifolds, Subsea Control Systems, Subsea Processing Equipment), By Water Depth (Deepwater (300–1,500 meters), Ultra-Deepwater (above 1,500 meters), Shallow Water (below 300 meters)), By Application (Oil Production, Gas Production, Subsea Processing (Boosting, Separation, Compression)), By End-User (International Oil Companies, National Oil Companies, Independent Oil Companies, Oilfield Services and EPC Companies) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | TECHNIPFMC PLC, SLB (SCHLUMBERGER LIMITED), BAKER HUGHES COMPANY, AKER SOLUTIONS ASA, SUBSEA 7 S.A., SAIPEM S.P.A., OCEANEERING INTERNATIONAL INC., EQUINOR ASA, PETROBRAS (PETROLEO BRASILEIRO S.A.), KONGSBERG GRUPPEN ASA, NEXANS S.A., PRYSMIAN GROUP, DRIL-QUIP INC., EXPRO GROUP HOLDINGS N.V., PROSERV GROUP, APHION SUBSEA, VAULT SUBSEA, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Water Depth (Shallow Water, Deepwater, Ultra-Deepwater), By Application (Oil Production, Gas Production, Subsea Processing Including Boosting, Separation & Compression), By End-User (International Oil Companies, National Oil Companies, Independent Operators, EPC & Oilfield Services) Industry Region & Key Players – Market Dynamics, Competitive Strategies, Trends & Forecast 2026–2034")

, By Water Depth (Shallow Water, Deepwater, Ultra-Deepwater), By Application (Oil Production, Gas Production, Subsea Processing Including Boosting, Separation & Compression), By End-User (International Oil Companies, National Oil Companies, Independent Operators, EPC & Oilfield Services) Industry Region & Key Players – Market Dynamics, Competitive Strategies, Trends & Forecast 2026–2034")

, By Water Depth (Shallow Water, Deepwater, Ultra-Deepwater), By Application (Oil Production, Gas Production, Subsea Processing Including Boosting, Separation & Compression), By End-User (International Oil Companies, National Oil Companies, Independent Operators, EPC & Oilfield Services) Industry Region & Key Players – Market Dynamics, Competitive Strategies, Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Subsea Production System Market?

The Global Subsea Production System Market was valued at USD 14.2 Billion in 2025, projected to reach USD 35.8 Billion by 2034 at a CAGR of 10.8% (2026–2034). Growth is driven by increasing deepwater exploration, rising offshore investments, and adoption of advanced subsea technologies including all-electric systems and subsea processing solutions.

Who are the major players in the Subsea Production System Market?

TECHNIPFMC PLC, SLB (SCHLUMBERGER LIMITED), BAKER HUGHES COMPANY, AKER SOLUTIONS ASA, SUBSEA 7 S.A., SAIPEM S.P.A., OCEANEERING INTERNATIONAL INC., EQUINOR ASA, PETROBRAS (PETROLEO BRASILEIRO S.A.), KONGSBERG GRUPPEN ASA, NEXANS S.A., PRYSMIAN GROUP, DRIL-QUIP INC., EXPRO GROUP HOLDINGS N.V., PROSERV GROUP, APHION SUBSEA, VAULT SUBSEA, Others

Which segments covered the Subsea Production System Market?

By Equipment Type (Subsea Trees, Umbilicals, Risers, and Flowlines, Subsea Manifolds, Subsea Control Systems, Subsea Processing Equipment), By Water Depth (Deepwater (300–1,500 meters), Ultra-Deepwater (above 1,500 meters), Shallow Water (below 300 meters)), By Application (Oil Production, Gas Production, Subsea Processing (Boosting, Separation, Compression)), By End-User (International Oil Companies, National Oil Companies, Independent Oil Companies, Oilfield Services and EPC Companies)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Subsea Production System Market

Published Date : 18 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date