- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Subsea Umbilical Riser and Flowline Market Size, Share & Growth | CAGR 7.2%

Global Subsea Umbilical Riser and Flowline Market Size, Share & Growth Analysis By Product Type (Flowlines, Risers, Umbilicals, Ancillary Jumpers and Connection Hardware), By Water Depth (Deepwater and Ultra-Deepwater Projects, Shallow-Water Developments, Mature-Field Tiebacks & Brownfield Expansions), By Installation Type (EPCI Integrated Delivery, Standalone Installation & Fabrication, Supply-Only Contracts), By End Use (Oilfield Developments, Gas Developments, Carbon Transport Infrastructure) Industry Regional Outlook, Competitive Landscape, Key Players, Market Dynamics, Strategic Insights, Technology Trends & Forecast 2026–2034

Report Overview

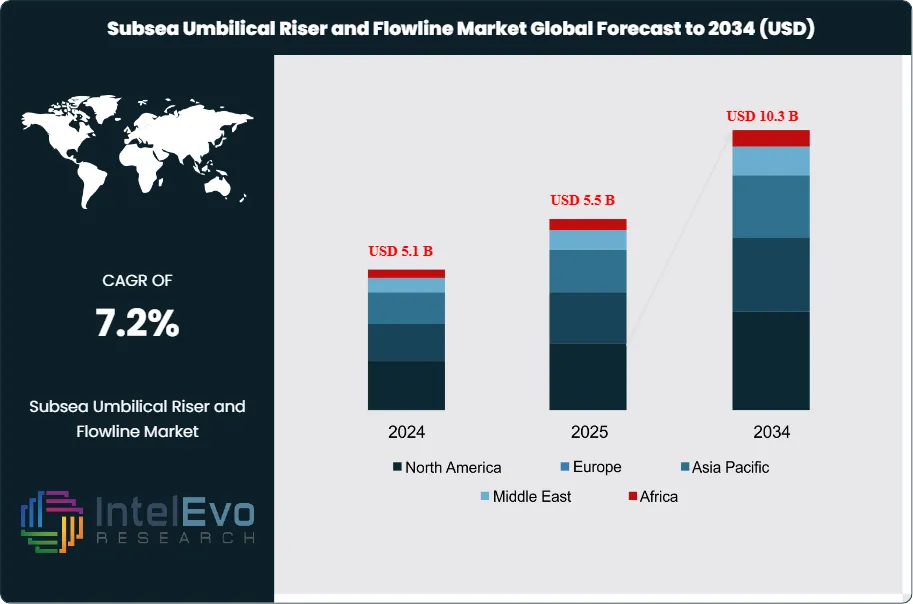

| Market Size, 2025 | Forecast Value, 2034 | CAGR, 2026-2034 | Leading Region, 2025 |

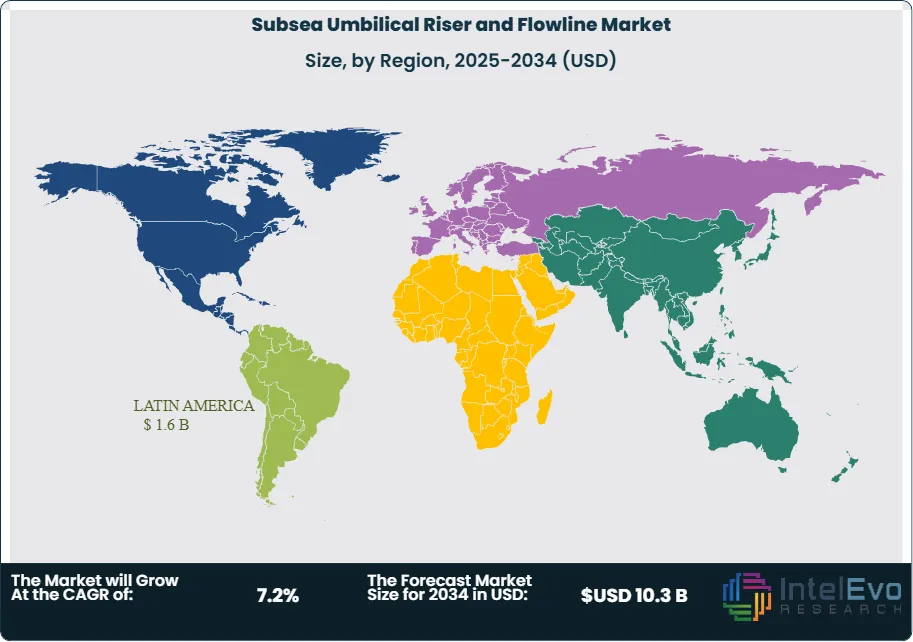

| USD 5.5 Billion | USD 10.3 Billion | 7.2% | Latin America, 29.0% |

The Subsea Umbilical Riser and Flowline Market was valued at USD 5.5 Billion in 2025 and is expected to reach USD 10.3 Billion by 2034, growing at a CAGR of 7.2% during the forecast period 2025–2034. This Subsea Umbilical Riser and Flowline Market view sits close to current public benchmarks. Recent market references place the market at about USD 5.1 Billion in 2024 with a 7.3% CAGR to 2034, around USD 5.5 Billion in 2025 with a 7.3% CAGR to 2035, and a broader premium estimate at USD 11.3 Billion in 2025 under a different market framing. The 2025–2034 figures used here reflect a conservative global SURF capital-spend view and are mathematically consistent.

Get More Information about this report -

Request Free Sample ReportThe Subsea Umbilical Riser and Flowline Market is growing because offshore operators are sanctioning more deepwater tiebacks, longer step-outs, and brownfield expansions that require integrated transport, control, and connection infrastructure. Demand is strongest where field architecture depends on long-distance flow assurance and subsea production control. Brazil remains a major investment hotspot. Subsea7 won a super-major Petrobras contract for the Búzios 11 field in May 2025 in about 2,000 meters of water. Petrobras also awarded SLB an USD 800 million offshore services contract in December 2024 tied to more than 100 deepwater wells, supporting a larger offshore development pipeline. TechnipFMC added a Petrobras subsea production systems award in September 2025, confirming that Brazil remains one of the most active subsea markets globally.

The Subsea Umbilical Riser and Flowline Market is also being shaped by supplier concentration, vessel availability, and integration models. The most important supply-side shift came from the proposed Saipem and Subsea7 merger, first announced in February 2025 and formalized in July 2025. Reuters reported the combined group would have about EUR 43 Billion in backlog, around EUR 20 billion in annual revenue, and more than EUR 2 billion in EBITDA, while customers in Brazil later argued the deal could reduce competition in SURF. That concentration risk matters because SURF execution depends on a limited set of global contractors with reel-lay assets, flexible-pipe manufacturing, installation vessels, and engineering depth.

Technology is lifting the market’s value per project. Integrated EPCI models now combine subsea production systems, umbilicals, rigid and flexible flowlines, risers, and boosting into one delivery frame. SLB OneSubsea and Subsea7 won the Ginger EPCI contract from bp in May 2025. SLB OneSubsea later won a subsea boosting contract for bp’s Tiber project in November 2025. TechnipFMC’s 2025 and early 2026 awards also show strong demand for flexible flowlines, risers, and subsea production integration in Brazil, Norway, Indonesia, and Mozambique. These shifts favor suppliers with full-system engineering capability rather than stand-alone component manufacturers.

Regional capital allocation supports the growth profile. The IEA expects the Middle East to invest about USD 130 Billion in oil and gas supply in 2025, while Equinor and other North Sea operators continued placing major contracts in Norway through late 2025 and early 2026. The main risks remain project deferrals, steel and vessel cost pressure, and competition concerns in concentrated offshore service corridors. Even so, the Subsea Umbilical Riser and Flowline Market should maintain a strong growth path because SURF hardware remains essential to deepwater field development and long-distance subsea tieback economics.

, By Water Depth (Deepwater and Ultra-Deepwater Projects, Shallow-Water Developments, Mature-Field Tiebacks & Brownfield Expansions), By Installation Type (EPCI Integrated Delivery, Standalone Installation & Fabrication, Supply-Only Contracts), By End Use (Oilfield Developments, Gas Developments, Carbon Transport Infrastructure) Industry Regional Outlook, Competitive Landscape, Key Players, Market Dynamics, Strategic Insights, Technology Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The Subsea Umbilical Riser and Flowline Market was valued at USD 5.5 Billion, 2025 and is projected to reach USD 10.3 Billion, 2034, at a 7.2% CAGR during 2025–2034.

- Segment Dominance: By product type, flowlines held the largest share at 39.0%, 2025, equal to USD 2.1 Billion, 2025.

- Segment Dominance: By application, deepwater and ultra-deepwater field developments accounted for 56.0% share, 2025, equal to USD 3.1 Billion, 2025.

- Driver: The main driver is rising offshore project sanctioning. Petrobras’ Búzios 11 award to Subsea7 in May 2025 and bp’s Ginger EPCI award in May 2025 both reinforce the scale of current deepwater demand.

- Restraint: The main restraint is supplier concentration and fleet-capacity risk. Customers argued in 2025 that the planned Saipem-Subsea7 merger could reduce competition in SURF, especially in Brazil.

- Opportunity: The biggest opportunity is integrated EPCI delivery that combines subsea trees, umbilicals, risers, flowlines, and boosting into one bundled model.

- Trend: The clearest trend is stronger alignment between subsea production systems and SURF execution. TechnipFMC recorded USD 10.1 Billion in full-year 2025 subsea orders, highlighting how integrated backlogs are lifting SURF demand.

- Regional Analysis: Latin America led the market with 29.0% share, 2025, equal to USD 1.6 Billion, 2025, with Brazil as the anchor market.

Competitive Landscape

The Subsea Umbilical Riser and Flowline Market is moderately consolidated. The top four companies, TechnipFMC, Subsea7, Saipem, and SLB OneSubsea, held an estimated 58.0% of global revenue in 2025. Competition is technology-driven and vessel-driven, with reel-lay capacity, flexible-pipe manufacturing, integrated EPCI capability, and offshore engineering depth deciding most awards. Competitive intensity increased sharply in 2025 as Subsea7 won Búzios 11, TechnipFMC expanded Petrobras and Indonesia subsea awards, SLB OneSubsea won Ginger and Tiber, and Saipem and Subsea7 formalized their merger agreement.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| TECHNIPFMC | UK | Leader | Subsea 2.0 integrated SURF and subsea systems | Latin America, Europe, Asia Pacific | Won Petrobras subsea systems contract in Sep 2025 and Eni Maha project award in Nov 2025. |

| SUBSEA7 | Luxembourg / UK | Leader | SURF EPCI portfolio | Latin America, Europe | Won Búzios 11 contract in May 2025 and signed merger agreement with Saipem in Jul 2025. |

| SAIPEM | Italy | Leader | Offshore EPCI and SURF installation fleet | Europe, Middle East, Africa | Signed binding merger agreement with Subsea7 in Jul 2025 to create Saipem7. |

| SLB ONESUBSEA | US / Norway JV | Leader | Integrated subsea production and EPCI alliance model | Gulf of America, Caribbean, global offshore | Won Ginger EPCI contract in May 2025 and Tiber boosting contract in Nov 2025. |

| AKER SOLUTIONS | Norway | Challenger | Umbilicals and subsea production systems | Europe, Latin America | Continued multi-region subsea and life-cycle contract execution through late 2025 and early 2026. |

| NOV | US | Challenger | Flexible pipe and offshore systems | North America, Middle East | Maintained offshore project exposure through adjacent subsea and marine system activity in 2025. |

| OCEANEERING | US | Challenger | Umbilical hardware, subsea distribution, installation support | North America, Brazil | Continued subsea hardware and service participation across offshore projects through 2025. |

| PRYSMIAN | Italy | Niche Player | Dynamic and static umbilical systems | Europe, Latin America | Remained active in global umbilicals supply into 2025. |

| JDR CABLE SYSTEMS | UK | Niche Player | Subsea umbilicals | Europe, Asia Pacific | Continued subsea umbilical manufacturing participation in offshore energy projects in 2025. |

| MCS KENNEDY | US | Niche Player | Steel catenary riser and flowline components | Gulf of America | Continued component supply into offshore deepwater developments through 2025. |

By Product Type

Flowlines held the largest share of the Subsea Umbilical Riser and Flowline Market at 39.0%, 2025, equal to USD 2.1 Billion, 2025. This segment leads because every subsea development needs reliable hydrocarbon transport from wells to manifolds, host facilities, or export systems. Risers accounted for 28.0%, 2025, equal to USD 1.5 Billion, 2025, supported by floating production systems and deeper water depths where vertical transport complexity rises sharply. Umbilicals represented 23.0%, 2025, or USD 1.3 Billion, 2025, driven by subsea control, power, and chemical injection needs. Ancillary jumpers and associated SURF connection hardware made up the remaining 10.0%, 2025, equal to USD 0.6 Billion, 2025. Competition in flowlines and risers is centered on fabrication capability, installation vessels, metallurgy, and flow assurance engineering. Umbilicals reward manufacturing precision, delivery timing, and long-life reliability. That is why TechnipFMC, Subsea7, Saipem, OneSubsea, Aker Solutions, and a smaller group of specialist umbilical suppliers dominate the high-value end of the market.

By Water Depth

Deepwater and ultra-deepwater projects led with 56.0% share, 2025, equal to USD 3.1 Billion, 2025. This segment dominates because longer tiebacks, floating production, harsher thermal conditions, and more difficult installation windows drive larger SURF scope per project. Brazil’s Búzios 11 development, Petrobras’ broader offshore portfolio, bp’s Tiber project, and Eni’s Coral North development all reinforce the weight of deepwater capital in the current market. Shallow-water developments accounted for 27.0%, 2025, or USD 1.5 Billion, 2025, supported by lower-cost regional projects and tie-ins. Mature-field tiebacks and brownfield expansion projects made up 17.0%, 2025, equal to USD 0.9 Billion, 2025. While smaller in absolute size, brownfield work remains attractive because tiebacks can generate strong returns using existing host infrastructure.

By Installation Type

EPCI-led integrated delivery accounted for 62.0% share, 2025, equal to USD 3.4 Billion, 2025. This segment leads because operators increasingly prefer bundled execution that joins subsea production systems, control infrastructure, SURF installation, and life-of-field support into one commercial model. Standalone installation and fabrication contracts represented 24.0%, 2025, or USD 1.3 Billion, 2025, still relevant where operators separate component purchasing from offshore execution. Umbilical and connection-system supply-only contracts made up 14.0%, 2025, equal to USD 0.8 Billion, 2025. The installation-type split explains why the market is concentrating around fewer global players. Integrated EPCI reduces interface risk, shortens schedules, and improves technical accountability, especially in deepwater developments.

By End Use

Oilfield developments held 68.0% share, 2025, equal to USD 3.7 Billion, 2025. This segment leads because most current SURF spending is still tied to deepwater oil developments in Brazil, the Gulf of America, West Africa, and selected North Sea projects. Gas-focused developments represented 25.0%, 2025, or USD 1.4 Billion, 2025, with major support from offshore gas and FLNG-linked projects such as Coral North offshore Mozambique and Indonesia’s Maha project. Carbon transport, adjacent offshore energy infrastructure, and other non-traditional uses represented 7.0%, 2025, equal to USD 0.4 Billion, 2025. The end-use mix matters because gas and adjacent applications often require different materials, thermal design, and long-distance flow assurance models, while oil developments still dominate installation complexity and project value.

By Regional Analysis

Latin America Subsea Umbilical Riser and Flowline Market

Latin America held 29.0% share, 2025, equal to USD 1.6 Billion, 2025. Brazil dominates the region, followed by Mexico, Guyana, and the Rest of Latin America. Brazil is the clear anchor because Petrobras continues to drive deepwater field development at scale. Subsea7’s Búzios 11 award in May 2025, TechnipFMC’s Petrobras subsea systems contract in September 2025, and Petrobras’ earlier USD 800 million integrated offshore services award to SLB all point to a sustained multi-year SURF pipeline. Guyana adds strong strategic relevance because large Stabroek developments continue to require umbilicals and associated subsea systems, while Mexico contributes selected offshore demand. Latin America remains the most commercially important region for premium SURF work because project sizes are large, water depths are demanding, and operators still need both greenfield and brownfield expansion infrastructure.

Europe Subsea Umbilical Riser and Flowline Market

Europe accounted for 24.0% share, 2025, equal to USD 1.3 Billion, 2025. Norway, the UK, Germany, and Italy are the most relevant countries, though Norway and the UK drive most actual offshore SURF demand. Europe remains a high-value region because the North Sea continues to support subsea tiebacks, brownfield redevelopment, and platform-linked subsea expansion. TechnipFMC’s Halten East award from Equinor and Subsea7’s Norway contracts in January and December 2025 confirm continued project flow. Italy matters strongly from a supplier standpoint because Saipem is one of the market’s largest contractors, and its planned merger with Subsea7 would further concentrate the regional vendor landscape. Europe’s growth is steadier than Latin America’s, but its commercial importance remains high because subsea tieback economics, harsh-environment engineering, and mature offshore infrastructure all favor SURF spending.

Asia Pacific Subsea Umbilical Riser and Flowline Market

Asia Pacific captured 18.0% share, 2025, equal to USD 1.0 Billion, 2025. China, Japan, India, and South Korea are the most relevant countries, with the Rest of Asia Pacific also important through Southeast Asian offshore developments. Australia, Indonesia, and broader offshore Southeast Asia remain especially material from a project standpoint, even if the user-requested country list prioritizes the four countries above. Asia Pacific’s growth case rests on offshore gas, FLNG-linked developments, and long-distance tiebacks that need flexible risers, control umbilicals, and advanced flow assurance. TechnipFMC’s substantial iEPCI contract for Eni’s Maha project in Indonesia and the earlier Scarborough project structure off Australia illustrate the region’s value profile.

Middle East & Africa Subsea Umbilical Riser and Flowline Market

Middle East & Africa represented 17.0% share, 2025, equal to USD 0.9 Billion, 2025. UAE, Saudi Arabia, South Africa, and the Rest of MEA define the regional structure, though Angola and Mozambique are commercially vital from a subsea project standpoint. The IEA expects the Middle East to invest about USD 130 Billion in oil and gas supply in 2025, which supports the region’s longer-term offshore infrastructure outlook. Africa’s contribution is increasingly important because offshore Angola and Mozambique remain linked to major subsea developments. TechnipFMC’s Coral North award offshore Mozambique in December 2025 is especially significant because it includes flexible flowlines, risers, manifolds, and umbilicals in about 2,000 meters of water.

North America Subsea Umbilical Riser and Flowline Market

North America held 12.0% share, 2025, equal to USD 0.7 Billion, 2025. The United States dominates the region, followed by Canada, Mexico, and the Rest of North America. The market is smaller than Latin America and Europe because offshore project concentration is lower, but the Gulf of America remains a premium deepwater SURF market. SLB OneSubsea’s boosting award for bp’s Tiber project in November 2025 confirms that the Gulf is still producing high-value subsea opportunities. The U.S. also matters as a manufacturing base for offshore systems and umbilicals, including Aker Solutions’ earlier Alabama-linked umbilicals work for Guyana developments.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Product Type

- Flowlines

- Risers

- Umbilicals

- Ancillary Jumpers and Connection Hardware

By Water Depth

- Deepwater and Ultra-Deepwater Projects

- Shallow-Water Developments

- Mature-Field Tiebacks and Brownfield Expansions

By Installation Type

- EPCI-Led Integrated Delivery

- Standalone Installation and Fabrication Contracts

- Umbilical and Connection-System Supply-Only Contracts

By End Use

- Oilfield Developments

- Gas-Focused Developments

- Carbon Transport and Other Offshore Infrastructure

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 5.5 B |

| Forecast Revenue (2034) | USD 10.3 B |

| CAGR (2025-2034) | 7.2% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product Type (Flowlines, Risers, Umbilicals, Ancillary Jumpers and Connection Hardware), By Water Depth (Deepwater and Ultra-Deepwater Projects, Shallow-Water Developments, Mature-Field Tiebacks and Brownfield Expansions), By Installation Type (EPCI-Led Integrated Delivery, Standalone Installation and Fabrication Contracts, Umbilical and Connection-System Supply-Only Contracts), By End Use (Oilfield Developments, Gas-Focused Developments, Carbon Transport and Other Offshore Infrastructure) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | TECHNIPFMC, SUBSEA7, SAIPEM, SLB ONESUBSEA, AKER SOLUTIONS, NOV, OCEANEERING, PRYSMIAN, JDR CABLE SYSTEMS, MCS KENNEDY, TENARIS, BOSKALIS SUBSEA, DOF SUBSEA, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Water Depth (Deepwater and Ultra-Deepwater Projects, Shallow-Water Developments, Mature-Field Tiebacks & Brownfield Expansions), By Installation Type (EPCI Integrated Delivery, Standalone Installation & Fabrication, Supply-Only Contracts), By End Use (Oilfield Developments, Gas Developments, Carbon Transport Infrastructure) Industry Regional Outlook, Competitive Landscape, Key Players, Market Dynamics, Strategic Insights, Technology Trends & Forecast 2026–2034")

, By Water Depth (Deepwater and Ultra-Deepwater Projects, Shallow-Water Developments, Mature-Field Tiebacks & Brownfield Expansions), By Installation Type (EPCI Integrated Delivery, Standalone Installation & Fabrication, Supply-Only Contracts), By End Use (Oilfield Developments, Gas Developments, Carbon Transport Infrastructure) Industry Regional Outlook, Competitive Landscape, Key Players, Market Dynamics, Strategic Insights, Technology Trends & Forecast 2026–2034")

, By Water Depth (Deepwater and Ultra-Deepwater Projects, Shallow-Water Developments, Mature-Field Tiebacks & Brownfield Expansions), By Installation Type (EPCI Integrated Delivery, Standalone Installation & Fabrication, Supply-Only Contracts), By End Use (Oilfield Developments, Gas Developments, Carbon Transport Infrastructure) Industry Regional Outlook, Competitive Landscape, Key Players, Market Dynamics, Strategic Insights, Technology Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Subsea Umbilical Riser and Flowline Market?

The Global Subsea Umbilical, Riser, and Flowline Market was valued at USD 5.1 Billion in 2024 and reached USD 5.5 Billion in 2025, projected to grow to USD 10.3 Billion by 2034 at a CAGR of 7.2%. The market is driven by increasing deepwater and ultra-deepwater oil & gas exploration, offshore infrastructure investments, and technological advancements in subsea production systems.

Who are the major players in the Subsea Umbilical Riser and Flowline Market?

TECHNIPFMC, SUBSEA7, SAIPEM, SLB ONESUBSEA, AKER SOLUTIONS, NOV, OCEANEERING, PRYSMIAN, JDR CABLE SYSTEMS, MCS KENNEDY, TENARIS, BOSKALIS SUBSEA, DOF SUBSEA, Others

Which segments covered the Subsea Umbilical Riser and Flowline Market?

By Product Type (Flowlines, Risers, Umbilicals, Ancillary Jumpers and Connection Hardware), By Water Depth (Deepwater and Ultra-Deepwater Projects, Shallow-Water Developments, Mature-Field Tiebacks and Brownfield Expansions), By Installation Type (EPCI-Led Integrated Delivery, Standalone Installation and Fabrication Contracts, Umbilical and Connection-System Supply-Only Contracts), By End Use (Oilfield Developments, Gas-Focused Developments, Carbon Transport and Other Offshore Infrastructure)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Subsea Umbilical Riser and Flowline Market

Published Date : 12 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date