- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Subsea Valve Market Size & Forecast 2034 | CAGR 5.8%

Global Subsea Valve Market Size, Share, Growth & Industry Analysis By Valve Type (Gate Valves, Ball Valves, Check Valves, Choke & Control Valves, Others), By Water Depth (Shallow Water, Deepwater, Ultra-Deepwater), By Application (Production Trees, Manifolds & Distribution Systems, Pipelines & Flowlines, Well Intervention & Abandonment Systems), By Actuation (Hydraulic, Electro-Hydraulic, Electric) Industry Trends, Competitive Landscape & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

| USD 2.48 Billion | USD 4.12 Billion | 5.8% | Latin America, 27.0% |

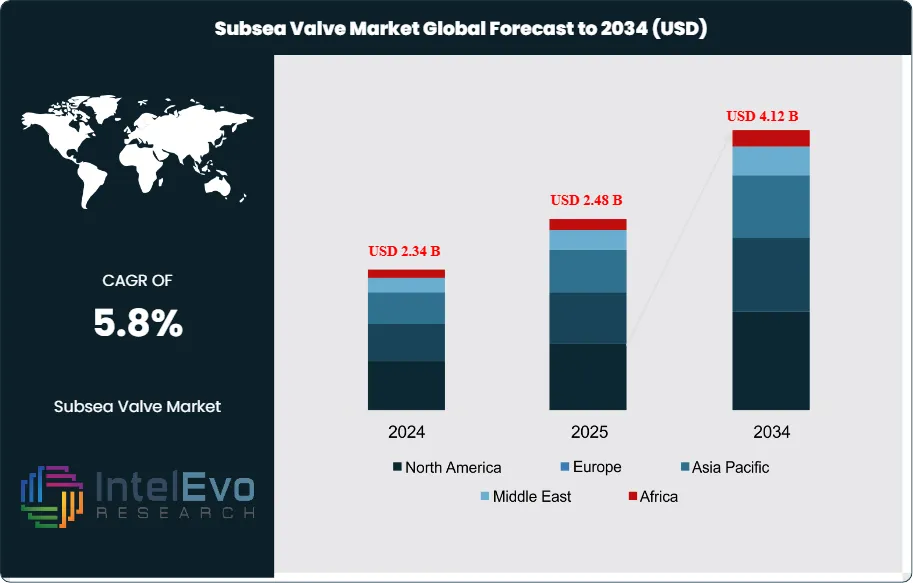

The Subsea Valve Market was valued at approximately USD 2.34 Billion in 2024 and reached USD 2.48 Billion in 2025. The market is projected to grow to USD 4.12 Billion by 2034, expanding at a CAGR of 5.8% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 1.64 Billion over the analysis period. The subsea valve market sits inside a larger offshore equipment cycle that has strengthened since 2022 as deepwater project sanctions, subsea tree awards, and operator spending shifted upward in Brazil, Guyana, Norway, the U.S. Gulf of Mexico, and selected African gas basins. Rystad data published by Offshore showed deepwater investment rising from about USD 90 Billion in 2023 toward almost USD 130 Billion by 2027, while more than 1,000 subsea trees had been awarded by the end of 2024, including 216 awards in 2024 alone.

Get More Information about this report -

Request Free Sample ReportThe subsea valve market draws demand from production trees, manifolds, subsea isolation systems, flowlines, and intervention packages. Gate valves, ball valves, check valves, and choke or control valves remain the core revenue pools. Demand stays highest where operators prefer long-life subsea production systems with low intervention frequency and high integrity sealing under corrosive, high-pressure, and deepwater service conditions. API Spec 17D remains a critical technical benchmark because it governs subsea wellhead and tree equipment, while API RP 17A, API RP 17N, and BSEE offshore production safety rules continue to shape qualification, testing, and reliability requirements. These standards raise entry barriers and keep pricing power concentrated among qualified suppliers with proven metallurgy, sealing performance, and long installed histories.

The subsea valve market also benefits from lower deepwater development costs, higher standardization, and digital condition monitoring. Offshore reported that average development cost for new deepwater fields fell from about USD 14 per boe to about USD 8 per boe over the last decade, which improved project economics and helped revive sanction activity. At the same time, suppliers have expanded manufacturing capacity in Brazil, Malaysia, Indonesia, the UK, and the U.S., yet labor tightness and long lead times still threaten delivery schedules. This cost-pressure mix supports demand for service-less valves, compact block designs, and electric or electro-hydraulic actuation that cut intervention cost over field life.

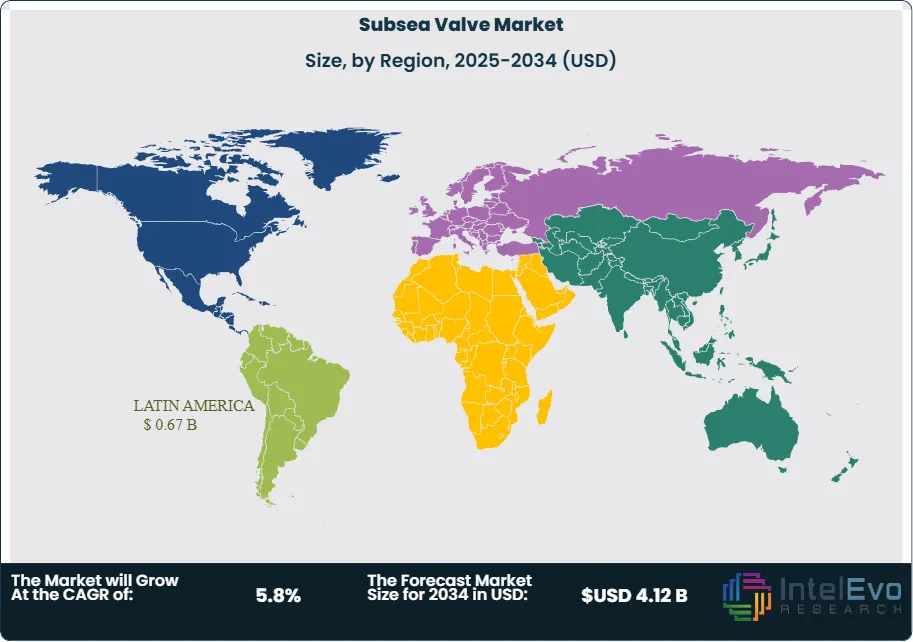

Regional demand remains strongest in Latin America, which accounted for 27.0% of global subsea valve revenue in 2025, or USD 0.67 Billion. Brazil anchors this position through pre-salt developments, while Guyana adds one of the fastest order pipelines for tree and manifold systems. North America followed with 25.0%, supported by a U.S. Gulf of Mexico production forecast of 1.9 million b/d in 2025. Europe held 21.0%, backed by Norway's project wave and UK brownfield subsea tiebacks. Asia Pacific captured 15.0% on Malaysia, Australia, Indonesia, and China activity, while the Middle East & Africa reached 12.0% on Mozambique, Angola, Nigeria, and new gas-led developments. The subsea valve market will keep tracking offshore CAPEX discipline, project approval timing, and the ability of suppliers to meet higher qualification and delivery demands.

, By Water Depth (Shallow Water, Deepwater, Ultra-Deepwater), By Application (Production Trees, Manifolds & Distribution Systems, Pipelines & Flowlines, Well Intervention & Abandonment Systems), By Actuation (Hydraulic, Electro-Hydraulic, Electric) Industry Trends, Competitive Landscape & Forecast 2026–2034")

Key Takeaways

- Market Growth: The subsea valve market stood at USD 2.48 Billion in 2025 and is projected to reach USD 4.12 Billion by 2034 at a CAGR of 5.8%. The market adds USD 1.64 Billion in new revenue over 2025-2034 as deepwater and ultra-deepwater projects move from sanction to installation.

- Segment Dominance: By valve type, gate valves led the subsea valve market with a 34.0% share in 2025, equal to USD 0.84 Billion. Operators still favor gate designs in tree and manifold duty because they handle high pressure, abrasive service, and shutoff isolation with long field life.

- Segment Dominance: By application, production trees held the largest share at 38.0% in 2025, or USD 0.94 Billion. Tree programs remain the main demand center because each new deepwater well architecture pulls multiple qualified valve sets into the bill of materials.

- Driver: Offshore project approvals are the main growth driver. Deepwater spending is on track to rise from about USD 90 Billion in 2023 to almost USD 130 Billion in 2027, while 216 subsea tree awards were recorded in 2024, lifting valve demand across trees, manifolds, and tiebacks.

- Restraint: Qualification cost and lead-time pressure hold the market back. API 17D compliance, metallurgy validation, and BSEE-linked safety requirements keep supplier entry tight, while workforce and factory bottlenecks can delay project delivery.

- Opportunity: Electrified subsea architecture is the clearest upside. Electric and electro-hydraulic valves represented 51.0% of 2025 revenue, and their share is set to expand as operators pursue lower intervention cost, lower fluid usage, and tighter digital diagnostics.

- Trend: Standardized subsea production systems are reshaping procurement. TechnipFMC, OneSubsea, Baker Hughes, and Innovex are pushing standardized tree and wellhead platforms, which reduces engineering hours and lifts repeat valve content across multi-well campaigns.

- Regional Analysis: Latin America led the subsea valve market with 27.0% share and USD 0.67 Billion in 2025. Brazil pre-salt developments and Guyana's Stabroek-led project pipeline kept the region ahead of North America and Europe.

Competitive Landscape Overview

The subsea valve market is moderately consolidated. The top four suppliers held an estimated 58.0% of global revenue in 2025. Competition is technology-driven and qualification-driven, not purely price-driven, because operators prefer suppliers with proven field history, API compliance, and installed-base service capability. Competitive intensity increased through 2025 as tree awards rose, Petrobras and ExxonMobil accelerated offshore programs, and suppliers expanded regional manufacturing to avoid capacity bottlenecks. Rystad identified OneSubsea and TechnipFMC as the dominant subsea tree suppliers since 2020, followed by Baker Hughes and Innovex, which aligns closely with valve purchasing patterns in integrated subsea production systems.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

|---|---|---|---|---|---|

| TechnipFMC | United Kingdom | Leader | Subsea 2.0 tree and valve systems | Latin America | Awarded substantial subsea contract for ExxonMobil's Hammerhead project in Guyana in Sep 2025. |

| SLB OneSubsea | United States | Leader | Subsea boosting and processing systems | Europe and Latin America | Secured a deepwater project contract offshore Malaysia in Mar 2026 after winning Northern Lights expansion work in Jun 2025. |

| Baker Hughes | United States | Leader | Deepwater horizontal tree and valve packages | Brazil and Eastern Mediterranean | Won Petrobras subsea tree systems work in Sep 2025 and Sakarya Phase 3 work in Turkey in Sep 2025. |

| Innovex International | United States | Challenger | Subsea wellhead and related valve interfaces | North America | Became exclusive wellhead partner for OneSubsea in Sep 2025 after a frame agreement signed in Feb 2025. |

| Oceaneering International | United States | Challenger | Subsea valves and intervention tooling | Latin America | Announced USD 180 Million of Petrobras-linked subsea robotics contracts in Aug 2025, strengthening installed-base service pull. |

| NOV | United States | Challenger | Subsea isolation valves | North America and Middle East | Continued commercial push of subsea isolation valve systems across offshore brownfield safety upgrades in 2025. |

| Hunting PLC | United Kingdom | Niche Player | Subsea valves and couplings | Europe and Middle East | Acquired Flexible Engineering Solutions for USD 64.8 Million in Jun 2025 to build out subsea capability. |

| Expro Group | United States | Niche Player | Solus single-valve subsea well access system | North Sea and Gulf of Mexico | Launched Solus in Feb 2026 as a single-valve subsea access system qualified to API Std 17G. |

| KOIL Energy | United States | Niche Player | SSIV control equipment | North America | Reported a 2025 contract for control equipment tied to a subsea isolation valve system, with delivery into 2026. |

| Neway Valve | China | Niche Player | Large-bore subsea valves | Asia Pacific | Expanded subsea valve delivery footprint in China and Southeast Asia through 2025 production scale-up. |

By Valve Type:

The subsea valve market generated its largest revenue from gate valves, which held 34.0% share in 2025, equal to USD 0.84 Billion. Gate valves dominate because they remain the preferred shutoff design inside subsea trees, manifolds, and high-pressure isolation duties where full-bore flow and tight sealing matter. Ball valves ranked second with 26.0%, or USD 0.64 Billion, supported by intervention systems, subsea well access packages, and compact layouts that value fast quarter-turn operation. Check valves accounted for 18.0%, or USD 0.45 Billion, mainly in backflow prevention on flowlines, injection systems, and process protection loops. Choke and control valves represented 14.0%, or USD 0.35 Billion, where operators need pressure management, flow control, and gas-lift handling in complex field architectures. Other specialty subsea valves, including relief and custom intervention designs, made up the remaining 8.0%. The share pattern reflects conservative operator purchasing behavior. Qualified shutoff valves with long field history still win the largest budgets, while more advanced control-oriented designs rise with digital production management and subsea processing growth.

By Water Depth:

The subsea valve market by water depth shows where field economics have improved most. Deepwater projects led with 43.0% share in 2025, or USD 1.07 Billion. These projects carry high valve content because each development uses multiple tree, manifold, jumper, and isolation packages and often demands corrosion-resistant alloys for long tieback life. Ultra-deepwater followed with 31.0%, or USD 0.77 Billion, and posted the strongest forward pace because Brazil pre-salt, Guyana, and selected African gas projects continue to move into deeper waters where reliability is worth a premium. Shallow-water subsea installations still contributed 26.0%, or USD 0.64 Billion, driven by brownfield extensions, compact tiebacks, and intervention-led replacement demand. The mix favors deeper water because development cost has fallen sharply and project sanctions have recovered. Offshore reported deepwater development cost dropping from about USD 14 per boe to about USD 8 per boe over the past decade, which improved break-even economics and widened the economic case for durable subsea hardware. Suppliers therefore keep directing capacity toward high-value deepwater and ultra-deepwater projects rather than lower-margin shallow-water packages.

By Application:

The subsea valve market by application remained centered on production trees, which accounted for 38.0% of 2025 revenue, or USD 0.94 Billion. This segment stays dominant because tree systems are valve-dense and every new well completion in deepwater requires qualified shutoff, control, and safety functions. Manifolds and distribution systems held 24.0%, or USD 0.60 Billion, because operators continue to standardize hub-and-spoke architectures that reduce umbilical length and simplify tiebacks. Pipelines and flowlines represented 21.0%, or USD 0.52 Billion, supported by subsea isolation valves and line protection equipment used to contain failures and support maintenance without shutting broader systems. Well intervention and abandonment systems contributed 17.0%, or USD 0.42 Billion, and this share is rising as mature offshore basins seek safer access for intervention, plug and abandonment, and late-life remediation. This application mix tracks the broader offshore project cycle. First, new field developments pull demand into tree and manifold packages. Later, the installed base creates aftermarket and intervention demand, which protects suppliers during slower sanction periods. That installed-base service pull is a major reason suppliers with field-proven valves and control packages keep share even when EPC cycles soften.

By Actuation and Control System:

The subsea valve market by actuation and control system still leaned toward hydraulic architectures, which held 49.0% share in 2025, or USD 1.22 Billion. Hydraulic systems dominate legacy installed bases because they are field-proven, widely supported, and accepted by operators in high-pressure applications. Electro-hydraulic systems captured 33.0%, or USD 0.82 Billion, and now sit in the strategic middle ground. They preserve proven hydraulic force while adding better diagnostics, faster control response, and lower topside complexity. Fully electric systems accounted for 18.0%, or USD 0.45 Billion, but they posted the strongest projected growth through 2034 because operators want lower fluid management, fewer leak paths, and tighter integration with remote monitoring. The shift matters for valve suppliers because electric and electro-hydraulic designs raise demand for smart actuators, sensor-rich assemblies, and software-linked condition monitoring. This transition also aligns with broader offshore moves toward standardized subsea production systems and lower intervention frequency. Suppliers that can validate electric reliability under API-linked qualification frameworks should gain share fastest in greenfield projects sanctioned after 2027.

Regional Analysis

North America

The subsea valve market in North America accounted for 25.0% of global revenue in 2025, equal to USD 0.62 Billion. The United States dominated regional demand because the Gulf of Mexico remained one of the world's most capital-efficient deepwater provinces. EIA projected federal Gulf crude production at 1.9 million b/d in 2025, which kept replacement, brownfield, and new-project demand firm for subsea trees, manifolds, and isolation systems. Canada contributed a smaller but technically important share through Atlantic offshore work and engineering demand tied to harsh-environment equipment. Mexico added project-based demand as operators pursued offshore field maintenance and selective redevelopment. North America remains strong in high-spec qualification, aftermarket service, and operator spending discipline. BSEE oversight and U.S. operator preference for high-integrity equipment keep barriers to entry high. This region also benefits from a large installed base, which supports intervention and retrofit demand even when new-field sanctioning pauses.

Europe

The subsea valve market in Europe represented 21.0% of global revenue in 2025, or USD 0.52 Billion. Norway led the region as tax-driven project approvals and subsea tieback activity kept equipment demand strong. The United Kingdom remained the second-largest regional market, helped by mature North Sea fields where subsea intervention, flow assurance, and well reactivation programs extend asset life. France and Italy matter more through OEM engineering, manufacturing, and EPC integration than through domestic offshore production. Europe stands out for its engineering depth, subsea technology development, and early movement into subsea electrification and CO2 injection. Norway sits among the key countries driving deepwater growth and project approval momentum, and Northern Lights contract activity shows how valve capability is starting to extend into subsea carbon storage systems. European buyers also place heavy weight on reliability documentation, life-cycle testing, and lower-emission field design, which favors suppliers with strong qualification records and digital diagnostics.

Asia Pacific

The subsea valve market in Asia Pacific reached 15.0% of global revenue in 2025, equal to USD 0.37 Billion. Malaysia led regional demand through deepwater developments and strong manufacturing relevance, while Australia supported high-spec gas and subsea tieback projects. China added capacity on the supply side and a rising domestic market for offshore flow-control hardware. India contributed through offshore redevelopment in the western offshore basin, though demand remained smaller than in Southeast Asia. Indonesia stayed relevant on both fabrication and project execution, with Baker Hughes expanding workforce at Batam and regional manufacturing becoming a bigger factor in supply-chain resilience. Asia Pacific is less concentrated than Latin America or North America, but it offers strong growth for standardized valve packages, electro-hydraulic controls, and service hubs. Regional demand should climb as gas monetization, floating production systems, and brownfield tiebacks gain pace across Malaysia, Australia, Indonesia, and China.

Latin America

The subsea valve market in Latin America led the world with 27.0% share in 2025, or USD 0.67 Billion. Brazil accounted for the bulk of regional revenue because pre-salt output continues to dominate national production and drives repeat orders for tree, manifold, and associated valve hardware. Guyana ranked second in regional growth intensity as Stabroek developments keep pulling new subsea awards. Mexico remained a smaller but still relevant market through offshore maintenance and redevelopment work. The region's strength comes from multi-year project visibility, high tree counts, and large installed subsea networks that require both greenfield hardware and life-of-field service. South America secured more than 40% of total subsea tree awards between 2020 and 2024, which explains why valve suppliers continue to prioritize Brazil and Guyana for factory capacity, local content, and field service.

Middle East & Africa

The subsea valve market in Middle East & Africa held 12.0% of global revenue in 2025, equal to USD 0.30 Billion. Angola and Nigeria remained the main oil-led demand centers in Africa, while Mozambique emerged as a gas-led equipment market tied to long-cycle subsea production systems. Baker Hughes highlighted Eni's Coral North LNG scope offshore Mozambique in early 2026, covering subsea trees, controls, manifolds, distribution, and topsides, which signals fresh demand for qualified valve assemblies. Saudi Arabia and the UAE are smaller subsea valve consumers than the Atlantic Basin, but they remain relevant through offshore field expansions and high-spec procurement standards. South Africa contributes more through regional service and logistics than direct demand. This region offers strong upside where gas export projects, floating LNG, and deepwater redevelopment proceed, but timing risk remains higher because project approvals can shift with commodity prices, financing conditions, and operator capital discipline.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Valve Type

- Gate Valves

- Ball Valves

- Check Valves

- Choke and Control Valves

- Others

By Water Depth

- Shallow Water

- Deepwater

- Ultra-Deepwater

By Application

- Production Trees

- Manifolds and Distribution Systems

- Pipelines and Flowlines

- Well Intervention and Abandonment Systems

By Actuation and Control System

- Hydraulic

- Electro-Hydraulic

- Electric

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 2.48 B |

| Forecast Revenue (2034) | USD 4.12 B |

| CAGR (2025-2034) | 5.8% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Valve Type, (Gate Valves, Ball Valves, Check Valves, Choke and Control Valves, Others), By Water Depth, (Shallow Water, Deepwater, Ultra-Deepwater), By Application, (Production Trees, Manifolds and Distribution Systems, Pipelines and Flowlines, Well Intervention and Abandonment Systems), By Actuation and Control System,(Hydraulic, Electro-Hydraulic, Electric) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | TECHNIPFMC, SLB ONESUBSEA, BAKER HUGHES, INNOVEX INTERNATIONAL, OCEANEERING INTERNATIONAL, NOV, HUNTING PLC, EXPRO GROUP, KOIL ENERGY, CURTISS-WRIGHT, IMI, NEWAY VALVE, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Water Depth (Shallow Water, Deepwater, Ultra-Deepwater), By Application (Production Trees, Manifolds & Distribution Systems, Pipelines & Flowlines, Well Intervention & Abandonment Systems), By Actuation (Hydraulic, Electro-Hydraulic, Electric) Industry Trends, Competitive Landscape & Forecast 2026–2034")

, By Water Depth (Shallow Water, Deepwater, Ultra-Deepwater), By Application (Production Trees, Manifolds & Distribution Systems, Pipelines & Flowlines, Well Intervention & Abandonment Systems), By Actuation (Hydraulic, Electro-Hydraulic, Electric) Industry Trends, Competitive Landscape & Forecast 2026–2034")

, By Water Depth (Shallow Water, Deepwater, Ultra-Deepwater), By Application (Production Trees, Manifolds & Distribution Systems, Pipelines & Flowlines, Well Intervention & Abandonment Systems), By Actuation (Hydraulic, Electro-Hydraulic, Electric) Industry Trends, Competitive Landscape & Forecast 2026–2034")

Frequently Asked Questions

How big is the Subsea Valve Market?

Global subsea valve market valued at USD 2.34B in 2024, reaching USD 4.12B by 2034, growing at a CAGR of 5.8% from 2026–2034.

Who are the major players in the Subsea Valve Market?

TECHNIPFMC, SLB ONESUBSEA, BAKER HUGHES, INNOVEX INTERNATIONAL, OCEANEERING INTERNATIONAL, NOV, HUNTING PLC, EXPRO GROUP, KOIL ENERGY, CURTISS-WRIGHT, IMI, NEWAY VALVE, Others

Which segments covered the Subsea Valve Market?

By Valve Type, (Gate Valves, Ball Valves, Check Valves, Choke and Control Valves, Others), By Water Depth, (Shallow Water, Deepwater, Ultra-Deepwater), By Application, (Production Trees, Manifolds and Distribution Systems, Pipelines and Flowlines, Well Intervention and Abandonment Systems), By Actuation and Control System,(Hydraulic, Electro-Hydraulic, Electric)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date