- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Superconducting Quantum Processor Market Size, Share | CAGR 17.2%

Global Superconducting Quantum Processor Market Size, Share Analysis By Qubit (Transmon, Flux, Charge, Phase, Xmon, Tunable, Fixed), By Application (Simulation, Optimization, ML/AI, Cryptography, Drug Discovery, Financial, Chemistry), By End-User (IT & Telecom, Healthcare, BFSI, Defense, Automotive, Manufacturing), By Access Model, By Qubit Count Tier Region & Key Players-Industry Segment Overview, Dynamics, Strategies, Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

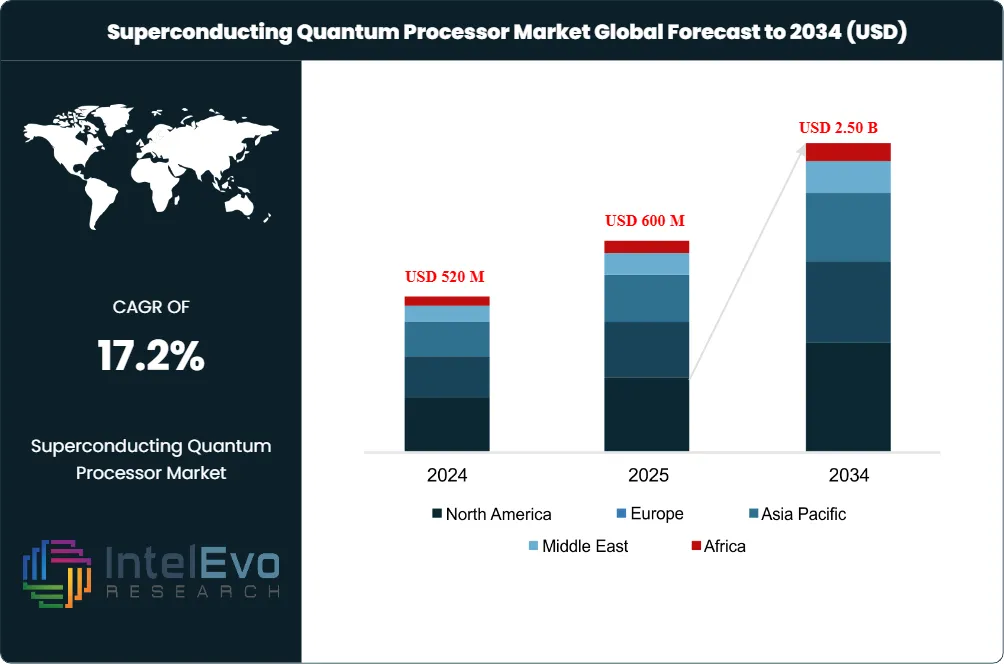

| USD 600 Million | USD 2.50 Billion | 17.2% | North America, 40.0% |

The Superconducting Quantum Processor Market was valued at USD 520 Million in 2024 and USD 600 Million in 2025. The market is projected to reach USD 2.50 Billion by 2034, expanding at a CAGR of 17.2% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 1.90 Billion over the analysis period. Demand is driven by enterprise pilots in quantum simulation, financial modeling, and combinatorial problem solving on IBM Heron R2 156-qubit, Google Willow 105-qubit, Rigetti Ankaa-2 84-qubit, and Fujitsu-RIKEN 256-qubit systems.

Get More Information about this report -

Request Free Sample ReportSuperconducting quantum processors hold approximately 40% share of the broader quantum computing hardware market because the architecture combines mature cryogenic infrastructure, fast gate operations measured in nanoseconds, and direct compatibility with existing semiconductor fabrication techniques. Transmon qubit designs captured 65% of superconducting quantum processor market revenue in 2025, dominating the qubit-type mix at IBM, Google, Rigetti, and AWS. Flux qubits held the second-largest share at approximately 17%, with the segment forecast to grow at an 18.7% CAGR through 2034 supported by D-Wave annealing systems and specialized fast-gate research applications.

Quantum simulation captured 34% of superconducting quantum processor market revenue in 2025, the largest application segment, addressing materials discovery, battery chemistry, drug development, and protein folding workloads at Pfizer, Roche, BMW, and BASF. Cloud-based deployment dominates customer access because superconducting systems require dilution refrigerators operating below 20 millikelvin, conditions impractical for enterprise on-premise installation. Google's Willow chip demonstrated exponential error reduction as qubit counts increased, achieving the below-threshold milestone in December 2024 and completing benchmark calculations in five minutes that classical supercomputers would require 10^25 years to perform.

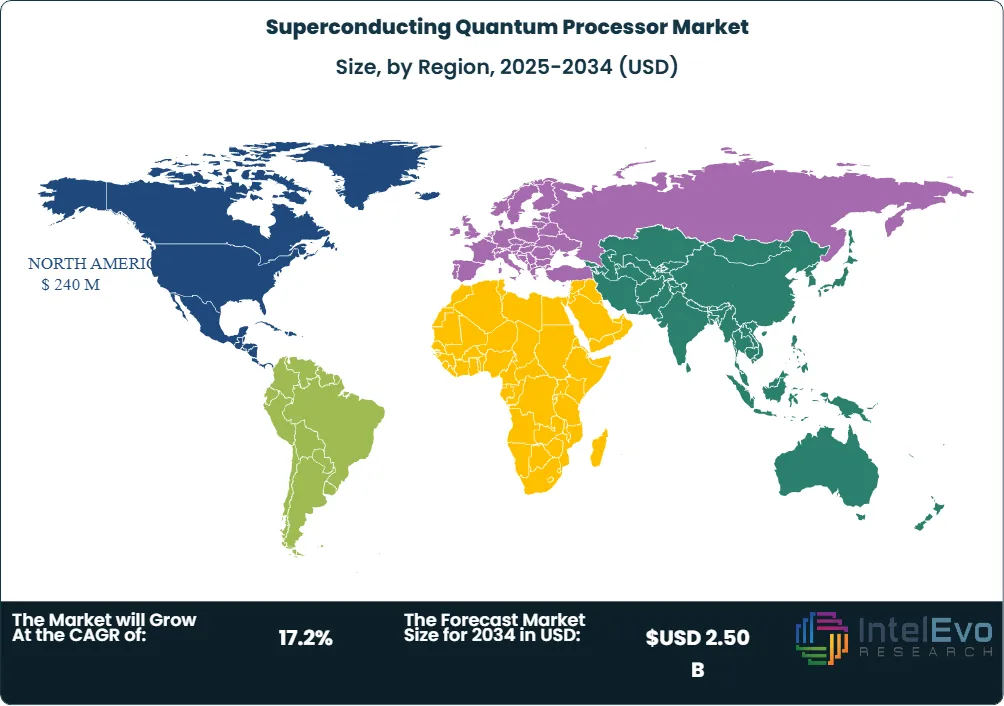

North America led the superconducting quantum processor market with 40.0% revenue share in 2025, equivalent to approximately USD 240 Million in regional revenue, anchored by IBM (Yorktown Heights), Google Quantum AI (Santa Barbara), Rigetti Computing (Berkeley), and AWS Center for Quantum Computing at Caltech. Asia Pacific captured 31% share led by Fujitsu-RIKEN, Origin Quantum (Hefei), and Bangalore-based QpiAI's April 2025 25-qubit launch. Europe held 24% share through IQM Quantum (Espoo), QuantWare (Delft), and Oxford Quantum Circuits (Reading). Through 2034, IBM's Kookaburra roadmap targeting 1,386 qubits per chip and Google's Quantum Echoes algorithm demonstrating 13,000-times classical speedup are reshaping competitive positioning.

Market Definition & Scope

The superconducting quantum processor market is defined as the global commercial activity covering quantum processing units (QPUs) built from Josephson-junction-based superconducting circuits, cooled to millikelvin temperatures in dilution refrigerators, and operated through microwave control electronics. The market includes transmon qubits (IBM, Google, Rigetti), flux qubits (D-Wave annealing), phase qubits, fluxonium qubits, and cat qubits (AWS Ocelot). Processors covered span 5-qubit research devices through 1,121-qubit IBM Condor scale and roadmap commitments to 4,158-qubit multi-chip configurations through 2027.

This analysis includes superconducting QPUs sold or accessed through cloud services, associated control electronics, dilution refrigerator-integrated systems, and bespoke fabrication services from foundries including QuantWare, SEEQC, and Origin Quantum. Excluded are trapped-ion systems (IonQ, Quantinuum), neutral-atom systems (QuEra, Atom Computing, Pasqal), photonic quantum systems (Xanadu, PsiQuantum), silicon-spin qubits (Intel, Quantum Motion), topological qubits (Microsoft Majorana 1), diamond-defect systems, and post-quantum cryptography software. The superconducting quantum processor market sits within the broader quantum computing hardware parent market, accounting for approximately 40% of cumulative hardware revenue in 2025.

, By Application (Simulation, Optimization, ML/AI, Cryptography, Drug Discovery, Financial, Chemistry), By End-User (IT & Telecom, Healthcare, BFSI, Defense, Automotive, Manufacturing), By Access Model, By Qubit Count Tier Region & Key Players-Industry Segment Overview, Dynamics, Strategies, Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The superconducting quantum processor market grew from USD 600 Million in 2025 toward a forecast value of USD 2.50 Billion by 2034 at a 17.2% CAGR.

- Segment Dominance: Transmon qubits captured approximately 65% revenue share in 2025, anchored by IBM Heron R2, Google Willow, Rigetti Ankaa-2, and AWS Emerald deployments.

- Segment Dominance: Quantum simulation held 34% of 2025 application revenue, addressing materials discovery, battery chemistry, and drug development at Pfizer, BASF, and BMW.

- Driver: Government and private quantum investment exceeded USD 30 Billion cumulatively through 2025, including USD 1.2 Billion from the U.S. National Quantum Initiative and EUR 1 Billion from the EU Quantum Flagship.

- Restraint: Cryogenic cooling requirements at 20 millikelvin operating temperature constrain deployment to specialized data centers, with dilution refrigerator capital costs running USD 500,000 to USD 1.5 Million per unit.

- Opportunity: Multi-chip quantum communication links represent the largest forecast-period opportunity, with IBM's Kookaburra roadmap targeting a 4,158-qubit system through three connected 1,386-qubit chips.

- Trend: Below-threshold quantum error correction is now demonstrated, with Google Willow showing exponential error reduction in December 2024 and IBM targeting the Quantum Starling system with 200 logical qubits by 2029.

- Regional: North America led with 40.0% share in 2025 equivalent to roughly USD 240 Million, while Asia Pacific captured 31% led by Fujitsu-RIKEN's 256-qubit system unveiled in April 2025.

Key Insights Summary

- Fujitsu and RIKEN announced a 256-qubit superconducting quantum computer in April 2025, four times larger than their 2023 system, with plans for a 1,000-qubit machine by 2026 per company disclosure.

- Google Willow demonstrated exponential error reduction as qubit counts increased in December 2024, completing benchmark calculations in five minutes that classical supercomputers would require 10^25 years to perform.

- IBM Heron R2 156-qubit processor supports up to 5,000 two-qubit gates per circuit and now powers cloud systems in the United States and European Union per IBM Research disclosure.

- Google announced the Quantum Echoes algorithm in October 2025, demonstrating the first verifiable quantum advantage with the out-of-time-order correlator running 13,000 times faster on Willow than classical supercomputers.

- AWS Braket launched the 54-qubit Emerald superconducting quantum processor in July 2025, providing higher-fidelity gates and full square-lattice connectivity per AWS announcement.

- NIST research through the SQMS Nanofabrication Taskforce achieved coherence times up to 0.6 milliseconds for the best-performing superconducting qubits, a significant advance for the technology.

- QpiAI launched a 25-qubit superconducting quantum computer in April 2025, positioning India among the most powerful quantum systems built domestically and supporting the National Quantum Mission.

Competitive Landscape Overview

The superconducting quantum processor market is moderately consolidated, with the top four vendors (IBM Corporation, Google LLC, Rigetti Computing, and Fujitsu Limited) collectively representing an estimated 65 to 72% of 2025 revenue. IBM holds the leading position through the Heron R2 156-qubit processor, the Condor 1,121-qubit system, and the Kookaburra roadmap targeting 1,386 qubits per chip with a 4,158-qubit multi-chip configuration. Google's Willow 105-qubit chip demonstrated below-threshold error correction in December 2024, the most consequential technical milestone of the period. Rigetti Computing operates the Ankaa-2 84-qubit and Novera 9-qubit systems through Rigetti Quantum Cloud Services and AWS Braket distribution.

Competitive evolution centers on three axes: qubit count and connectivity geometry, gate fidelity and coherence time, and error-correction efficiency. AWS revealed its Ocelot quantum chip in 2025, designed with cat qubits to improve quantum error correction by up to 90% versus prior architectures. SEEQC operates Single Flux Quantum (SFQ) digital control electronics co-located with the QPU at cryogenic temperatures, reducing wiring heat load. QuantWare provides Soprano-D 25-qubit and Contralto-A processors through a fab service model serving global vendors. Strategic moves through 2025 included IBM's June 2025 fault-tolerant data center announcement at Poughkeepsie, AWS's July 2025 Emerald 54-qubit launch, the May 2025 QphoX-Rigetti-NQCC optical-readout collaboration, and Google's October 2025 Quantum Echoes algorithm demonstration.

Competitive Landscape Matrix

| Company | HQ | Position | Key Product / Solution | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| IBM Corporation | USA | Leader | Heron R2 156-qubit, Condor 1121-qubit, Kookaburra | North America, Europe | Jun 2025 announced fault-tolerant quantum at Poughkeepsie |

| Google LLC | USA | Leader | Willow 105-qubit, Quantum AI Sycamore | North America | Oct 2025 demonstrated Quantum Echoes 13,000x speedup |

| Rigetti Computing Inc. | USA | Leader | Ankaa-2 84-qubit, Novera 9-qubit, QCS platform | North America, Europe | May 2025 partnered with QphoX and NQCC on optical readout |

| Fujitsu Limited | Japan | Leader | 256-qubit RIKEN system, Digital Annealer | Asia Pacific, Europe | Apr 2025 unveiled 256-qubit system, 1000-qubit plan for 2026 |

| Amazon Web Services | USA | Challenger | Ocelot cat-qubit chip, Emerald 54-qubit | North America | Jul 2025 launched Emerald superconducting processor |

| IQM Quantum Computers | Finland | Challenger | IQM Spark 5-qubit, IQM Garnet 20-qubit | Europe | 2025 expanded full-stack quantum installations across EU |

| Origin Quantum Computing | China | Challenger | Origin Wukong 72-qubit, Tianyan platform | Asia Pacific | 2025 expanded Wuyuan superconducting cloud access |

| SEEQC Inc. | USA | Niche Player | Digital quantum readout, SFQ control electronics | North America, Europe | 2025 advanced single flux quantum control deployments |

| QuantWare BV | Netherlands | Niche Player | Soprano-D 25-qubit, Contralto-A processor | Europe | 2025 expanded fab service offering for global vendors |

| Oxford Quantum Circuits | UK | Niche Player | Lucy 8-qubit, Toshiko 32-qubit, OQC Cloud | Europe | 2024 secured GBP 100M Series B for AWS deployment |

Segmentation Analysis

The superconducting quantum processor market is segmented by qubit type, application, end-use industry, deployment access model, and qubit count tier, each producing distinct competitive and adoption patterns across the forecast period.

By Qubit Type

Transmon qubits dominated the superconducting quantum processor market with approximately 65% revenue share in 2025, anchored by IBM Heron R2, Google Willow, Rigetti Ankaa-2, and AWS Emerald deployments. Transmons offer reduced charge-noise sensitivity and well-characterized two-qubit gate physics through cross-resonance and tunable-coupler designs. Flux qubits captured 17% revenue share, dominated by D-Wave annealing systems for combinatorial workloads, with the segment forecast to grow at an 18.7% CAGR through 2034. Fluxonium and 0-pi qubits represent the emerging high-coherence research segment with NIST coherence times reaching 0.6 milliseconds. AWS Ocelot cat qubits represent a separate engineering bet on hardware-level error correction. Phase qubits hold a small legacy share concentrated in academic research.

By Application

Quantum simulation captured 34% of superconducting quantum processor market revenue in 2025, the largest application segment, with the category forecast to reach USD 1.11 Billion by 2034. Materials discovery, battery electrolyte chemistry, drug-target binding, and protein folding workloads anchor demand at Pfizer, Roche, BMW, BASF, and Mitsubishi Chemical. Combinatorial problem solving represented the second-largest application share at 26%, anchored by D-Wave annealing systems for vehicle routing, production scheduling, and portfolio rebalancing. Machine learning and AI captured 22% share through quantum kernel methods, variational quantum classifiers, and Google's quantum-enhanced random circuit sampling. Cryptography and security held the remaining 18% share, driven by post-quantum cryptography assessment and quantum key distribution research.

By End-Use Industry

IT and telecommunications captured approximately 28% of superconducting quantum processor market revenue in 2025, anchored by hyperscaler internal use and telecommunications-carrier 6G research. BFSI held 22% share through JPMorgan Chase, Goldman Sachs, HSBC, and Mitsubishi UFJ portfolio-rebalancing and risk-modeling pilots. Aerospace and defense captured 17% share through DARPA programs, the U.S. Department of Defense, and European defense agencies. Healthcare and pharmaceutical end-users represented 15% share at Pfizer, Roche, Boehringer Ingelheim, and Moderna for drug-discovery workloads. Energy and utilities held 11% share, with the remaining 7% covering automotive (BMW, Volkswagen, Toyota), academia, and government civilian agencies.

By Deployment Access Model

Cloud access dominated the superconducting quantum processor market with approximately 78% revenue share in 2025 because dilution-refrigerator infrastructure constrains on-premises deployment to specialized data centers. IBM Quantum Network, AWS Braket, Microsoft Azure Quantum, and Google Cloud Quantum Engine anchor cloud-access revenue. Direct hardware sales captured 14% share, primarily covering national laboratory installations including Forschungszentrum Julich (IBM Quantum System Two), RIKEN (Fujitsu 256-qubit), and the U.K. National Quantum Computing Centre. Bespoke fab and contract manufacturing held 8% share through QuantWare, SEEQC, and Origin Quantum service offerings. Cloud access is forecast to grow at a 19% CAGR through 2030 versus 12% for direct sales.

By Qubit Count Tier

Mid-scale processors covering 50 to 200 qubits captured approximately 47% of superconducting quantum processor market revenue in 2025, anchored by IBM Heron R2 156-qubit, Google Willow 105-qubit, Rigetti Ankaa-2 84-qubit, and AWS Emerald 54-qubit cloud deployments. Small-scale research devices below 50 qubits held 21% share through OQC Lucy 8-qubit, Rigetti Novera 9-qubit, IQM Spark 5-qubit, and academic-laboratory installations. Large-scale processors above 200 qubits captured 32% revenue share following IBM Condor 1,121-qubit deployment and the April 2025 Fujitsu-RIKEN 256-qubit unveiling. The large-scale tier is forecast to lead growth through 2030 as IBM Kookaburra 1,386-qubit and Fujitsu 1,000-qubit roadmaps reach commercial availability.

Regional Analysis

The global superconducting quantum processor market shows distinct regional revenue and growth profiles across North America, Europe, Asia Pacific, Latin America, and Middle East and Africa, with North American hyperscaler concentration and Asia Pacific national-program investment driving the geographic mix.

North America

North America led the superconducting quantum processor market with 40.0% share in 2025, equivalent to approximately USD 240 Million in regional revenue. The United States anchors regional supply through IBM Yorktown Heights, Google Quantum AI Santa Barbara, Rigetti Computing Berkeley, AWS Center for Quantum Computing at Caltech, and SEEQC Elmsford. The U.S. National Quantum Initiative Act, the CHIPS and Science Act quantum allocations, and Department of Energy National Quantum Information Science Research Centers committed more than USD 1.2 Billion through fiscal year 2025. Canada anchors regional supply through Photonic Inc. and Anyon Systems. JPMorgan Chase's October 2025 USD 1.5 Trillion Security and Resiliency Initiative committed up to USD 10 Billion across 27 sub-areas including quantum computing.

Europe

Europe held approximately 24% of superconducting quantum processor market revenue in 2025, valued near USD 144 Million. Germany leads regional demand through IBM Quantum System Two installation at Forschungszentrum Julich, BMW and Volkswagen materials-simulation pilots, and the Munich Quantum Valley initiative. The United Kingdom anchors regional vendor supply through Oxford Quantum Circuits (Reading) and the National Quantum Computing Centre, supported by the GBP 2.5 Billion National Quantum Strategy. Finland hosts IQM Quantum Computers (Espoo), the Netherlands hosts QuantWare (Delft), and France contributes through the EUR 1.8 Billion Plan Quantique. The European Union Quantum Flagship committed EUR 1 Billion over ten years.

Asia Pacific

Asia Pacific captured approximately 31% of superconducting quantum processor market revenue in 2025, valued near USD 186 Million, and is forecast as the fastest-growing region at a 19% CAGR through 2030. Japan leads regional supply through Fujitsu-RIKEN's April 2025 256-qubit announcement and roadmap to 1,000 qubits by 2026, supported by the METI Q-LEAP program and Cabinet Office Moonshot Goal 6. China leads regional demand through Origin Quantum (Hefei) operating the Wukong 72-qubit and Wuyuan superconducting cloud, supported by an estimated USD 15 Billion in cumulative quantum investment through 2025. India anchors emerging supply through QpiAI's April 2025 25-qubit launch and the National Quantum Mission INR 6,003 Crore allocation.

Latin America

Latin America accounted for approximately 3% of superconducting quantum processor market revenue in 2025. Brazil leads regional adoption through Embraer aerospace simulation, Petrobras energy modeling, and the SENAI Innovation Institute research programs. Mexico contributes through CINVESTAV academic collaborations with U.S. quantum vendors. Argentina, Chile, and Colombia represent emerging demand pockets supported by university research grants. Regional growth is constrained by limited cryogenic infrastructure and dilution-refrigerator-import logistics, although AWS Sao Paulo and Azure Brazil South cloud regions provide remote access for enterprise pilots.

Middle East & Africa

Middle East and Africa held approximately 2% of superconducting quantum processor market revenue in 2025. The United Arab Emirates anchors regional demand through the Quantum Research Center at Technology Innovation Institute (Abu Dhabi) and Masdar City quantum-research investments. Saudi Arabia's KAUST quantum initiative and Vision 2030 sustainability mandates drive secondary demand. Israel contributes through Quantum Machines and Classiq Technologies commercial offerings supporting QPU control infrastructure. South Africa's national quantum technology initiative supports African demand, although growth is constrained by limited specialized-talent depth.

Country Analysis

United States

The United States superconducting quantum processor market reached approximately USD 220 Million in 2025, with country CAGR tracking near 17.5% through 2034. Demand concentrates at JPMorgan Chase, Goldman Sachs, BlackRock, ExxonMobil, Pfizer, and the Department of Defense pilot programs. Domestic supply concentrates at IBM (Yorktown Heights), Google Quantum AI (Santa Barbara), Rigetti Computing (Berkeley), AWS Center for Quantum Computing (Pasadena), and SEEQC (Elmsford). The U.S. National Quantum Initiative Act funded more than USD 1.2 Billion through fiscal year 2025. June 2025's IBM announcement of a fault-tolerant quantum computer at the Poughkeepsie data center marks the largest single-site superconducting quantum capacity commitment to date.

Japan

Japan's superconducting quantum processor market reached approximately USD 95 Million in 2025, the largest single-country market within Asia Pacific with country CAGR near 19% through 2034. April 2025's Fujitsu-RIKEN 256-qubit superconducting quantum computer announcement marks the largest non-U.S. installation, four times larger than the 2023 system, with plans for a 1,000-qubit machine by 2026. Toyota anchors automotive supply-chain pilots, while Hitachi, NEC, and Mitsubishi Chemical Holdings drive industrial demand. The METI Q-LEAP program and Cabinet Office Moonshot Goal 6 target fault-tolerant quantum computing by 2050, with the Green Innovation Fund allocating JPY 2 Trillion through 2030.

China

China's superconducting quantum processor market reached approximately USD 65 Million in 2025, with country CAGR near 22% through 2034, the highest among major economies. Domestic supply concentrates at Origin Quantum (Hefei) operating the Wukong 72-qubit superconducting system through the Tianyan cloud platform, alongside Beijing Yike, SpinQ Technology, and QuantumCTek. The 14th Five-Year Plan prioritizes quantum-information science as a strategic priority, with the Hefei National Laboratory anchoring research infrastructure. China's estimated USD 15 Billion in cumulative quantum investment funds both research and commercial pilots. Demand concentrates at Industrial and Commercial Bank of China, China Construction Bank, Sinopec, BYD, and Huawei for financial-modeling and battery-chemistry workloads.

Germany

Germany's superconducting quantum processor market reached approximately USD 55 Million in 2025, the largest single-country market within Europe with country CAGR near 18% through 2034. The Federal Ministry of Education and Research (BMBF) committed EUR 3 Billion through 2026 for quantum technology, with the Munich Quantum Valley initiative anchoring regional infrastructure. The IBM Quantum System Two installation at Forschungszentrum Julich anchors regional cloud access. BMW, Volkswagen, Mercedes-Benz, BASF, Siemens, and Deutsche Bank drive demand-side adoption. ParityQC and Quantum Brilliance contribute regional vendor supply, while the European Chips Act extends quantum-supply-chain investment commitments through 2030.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Qubit Type

- Transmon Qubits

- Flux Qubits

- Charge Qubits

- Phase Qubits

- Xmon Qubits

- Tunable Coupler Qubits

- Fixed-Frequency Qubits

- Hybrid Superconducting Qubits

- Others

By Application

- Quantum Simulation

- Optimization Problems

- Machine Learning and Artificial Intelligence

- Cryptography and Cybersecurity

- Drug Discovery and Molecular Modeling

- Financial Modeling and Risk Analysis

- Materials Science Research

- Supply Chain and Logistics Optimization

- Climate and Weather Modeling

- Quantum Chemistry

- Scientific Research and Academic Studies

- Others

By End-Use Industry

- Information Technology and Telecommunications

- Healthcare and Life Sciences

- Pharmaceuticals and Biotechnology

- Banking, Financial Services, and Insurance (BFSI)

- Government and Defense

- Aerospace and Defense

- Automotive

- Energy and Utilities

- Manufacturing

- Academic and Research Institutions

- Chemicals and Materials

- Others

By Deployment Access Model

- Cloud-Based Access

- On-Premises Deployment

- Hybrid Access Model

- Quantum Computing as a Service (QCaaS)

- Research Consortium Access

- Dedicated Enterprise Access

- Others

By Qubit Count Tier

- Below 100 Qubits

- 100–500 Qubits

- 501–1,000 Qubits

- 1,001–5,000 Qubits

- Above 5,000 Qubits

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 600 M |

| Forecast Revenue (2034) | USD 2.50 B |

| CAGR (2025-2034) | 17.2% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Qubit Type, (Transmon Qubits, Flux Qubits, Charge Qubits, Phase Qubits, Xmon Qubits, Tunable Coupler Qubits, Fixed-Frequency Qubits, Hybrid Superconducting Qubits, Others), By Application, (Quantum Simulation, Optimization Problems, Machine Learning and Artificial Intelligence, Cryptography and Cybersecurity, Drug Discovery and Molecular Modeling, Financial Modeling and Risk Analysis, Materials Science Research, Supply Chain and Logistics Optimization, Climate and Weather Modeling, Quantum Chemistry, Scientific Research and Academic Studies, Others), By End-Use Industry, (Information Technology and Telecommunications, Healthcare and Life Sciences, Pharmaceuticals and Biotechnology, Banking, Financial Services, and Insurance (BFSI), Government and Defense, Aerospace and Defense, Automotive, Energy and Utilities, Manufacturing, Academic and Research Institutions, Chemicals and Materials, Others), By Deployment Access Model, (Cloud-Based Access, On-Premises Deployment, Hybrid Access Model, Quantum Computing as a Service (QCaaS), Research Consortium Access, Dedicated Enterprise Access, Others), By Qubit Count Tier, Below 100 Qubits, 100–500 Qubits, 501–1,000 Qubits, 1,001–5,000 Qubits, Above 5,000 Qubits) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | IBM CORPORATION, GOOGLE LLC (ALPHABET INC.), RIGETTI COMPUTING INC., FUJITSU LIMITED, AMAZON WEB SERVICES INC., IQM QUANTUM COMPUTERS, ORIGIN QUANTUM COMPUTING, SEEQC INC., QUANTWARE BV, OXFORD QUANTUM CIRCUITS LTD., D-WAVE QUANTUM INC., INTEL CORPORATION, ALIBABA QUANTUM LABORATORY, TOSHIBA CORPORATION, NEC CORPORATION, NORTHROP GRUMMAN CORPORATION, QUANTINUUM LTD., ANYON SYSTEMS INC., QPIAI INC., QUANDELA SAS, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Simulation, Optimization, ML/AI, Cryptography, Drug Discovery, Financial, Chemistry), By End-User (IT & Telecom, Healthcare, BFSI, Defense, Automotive, Manufacturing), By Access Model, By Qubit Count Tier Region & Key Players-Industry Segment Overview, Dynamics, Strategies, Trends & Forecast 2026-2034")

, By Application (Simulation, Optimization, ML/AI, Cryptography, Drug Discovery, Financial, Chemistry), By End-User (IT & Telecom, Healthcare, BFSI, Defense, Automotive, Manufacturing), By Access Model, By Qubit Count Tier Region & Key Players-Industry Segment Overview, Dynamics, Strategies, Trends & Forecast 2026-2034")

, By Application (Simulation, Optimization, ML/AI, Cryptography, Drug Discovery, Financial, Chemistry), By End-User (IT & Telecom, Healthcare, BFSI, Defense, Automotive, Manufacturing), By Access Model, By Qubit Count Tier Region & Key Players-Industry Segment Overview, Dynamics, Strategies, Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Superconducting Quantum Processor Market?

The Global Superconducting Quantum Processor Market was valued at USD 520 Million in 2024 and USD 600 Million in 2025, and is projected to reach USD 2.50 Billion by 2034, growing at a CAGR of 17.2% from 2026 to 2034. Market growth is driven by advancements in superconducting qubits, quantum computing infrastructure, and cloud-based quantum services.

Who are the major players in the Superconducting Quantum Processor Market?

IBM CORPORATION, GOOGLE LLC (ALPHABET INC.), RIGETTI COMPUTING INC., FUJITSU LIMITED, AMAZON WEB SERVICES INC., IQM QUANTUM COMPUTERS, ORIGIN QUANTUM COMPUTING, SEEQC INC., QUANTWARE BV, OXFORD QUANTUM CIRCUITS LTD., D-WAVE QUANTUM INC., INTEL CORPORATION, ALIBABA QUANTUM LABORATORY, TOSHIBA CORPORATION, NEC CORPORATION, NORTHROP GRUMMAN CORPORATION, QUANTINUUM LTD., ANYON SYSTEMS INC., QPIAI INC., QUANDELA SAS, Others

Which segments covered the Superconducting Quantum Processor Market?

By Qubit Type, (Transmon Qubits, Flux Qubits, Charge Qubits, Phase Qubits, Xmon Qubits, Tunable Coupler Qubits, Fixed-Frequency Qubits, Hybrid Superconducting Qubits, Others), By Application, (Quantum Simulation, Optimization Problems, Machine Learning and Artificial Intelligence, Cryptography and Cybersecurity, Drug Discovery and Molecular Modeling, Financial Modeling and Risk Analysis, Materials Science Research, Supply Chain and Logistics Optimization, Climate and Weather Modeling, Quantum Chemistry, Scientific Research and Academic Studies, Others), By End-Use Industry, (Information Technology and Telecommunications, Healthcare and Life Sciences, Pharmaceuticals and Biotechnology, Banking, Financial Services, and Insurance (BFSI), Government and Defense, Aerospace and Defense, Automotive, Energy and Utilities, Manufacturing, Academic and Research Institutions, Chemicals and Materials, Others), By Deployment Access Model, (Cloud-Based Access, On-Premises Deployment, Hybrid Access Model, Quantum Computing as a Service (QCaaS), Research Consortium Access, Dedicated Enterprise Access, Others), By Qubit Count Tier, Below 100 Qubits, 100–500 Qubits, 501–1,000 Qubits, 1,001–5,000 Qubits, Above 5,000 Qubits)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Superconducting Quantum Processor Market

Published Date : 19 Jun 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date