- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Supply Chain Finance Platform Market Size, Share | CAGR 9.9%

Global Supply Chain Finance Platform Market Size, Share, Analysis By Offering (Platforms & Software Solutions, Services), By Provider (Banks & Financial Institutions, Fintech Companies, Technology Platform Providers, Non-Bank Financial Institutions), By Deployment Mode (Cloud-Based, On-Premises, Hybrid), By Enterprise Size (Large Enterprises, SMEs), By End-User Vertical (Manufacturing, Retail & E-Commerce, Healthcare & Pharmaceuticals, Automotive, Transportation & Logistics, Energy & Utilities, IT & Telecommunications) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

|---|---|---|---|

| USD 8.45 Billion | USD 19.80 Billion | 9.9% | Asia Pacific, 41.5% |

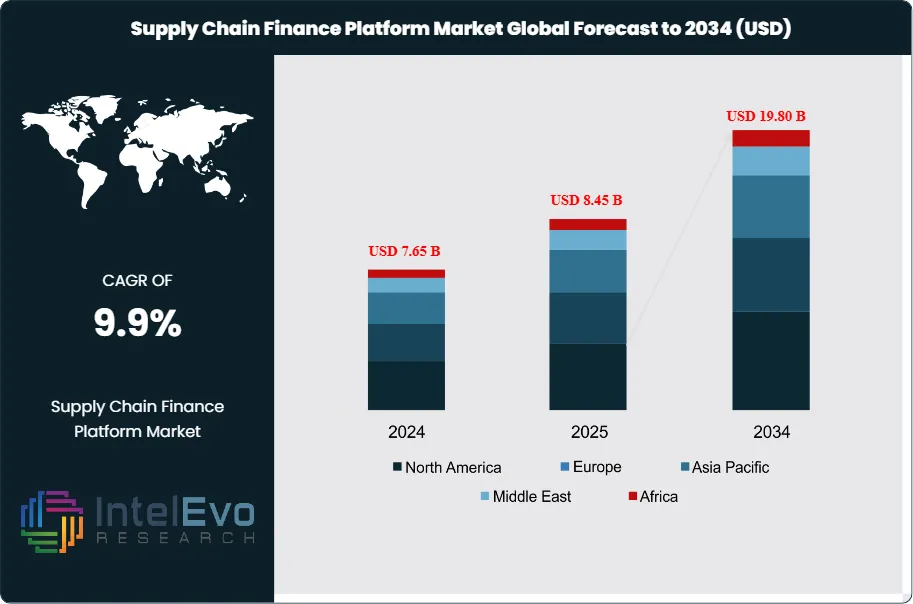

The Supply Chain Finance Platform Market was valued at approximately USD 7.65 Billion in 2024 and reached USD 8.45 Billion in 2025. The market is projected to grow to USD 19.80 Billion by 2034, expanding at a CAGR of 9.9% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 11.35 Billion over the analysis period.

Get More Information about this report -

Request Free Sample ReportGrowth in the supply chain finance platform market is anchored in three structural shifts. First, enterprise treasury teams moved from bank-led reverse factoring to multi-funder platforms, evidenced by SAP Taulia's rise in transaction volume from USD 500 Billion to USD 800 Billion over three years following SAP's March 2022 acquisition. Second, non-bank digital working capital networks scaled meaningfully, with C2FO surpassing USD 400 Billion in lifetime funding in December 2024 and recording its first USD 1 Billion day of funding, and PrimeRevenue facilitating more than USD 300 Billion in commerce across 16 million invoices totaling USD 80 Billion in 2025. Third, regulatory mandates accelerated SMB supplier enrollment, including India's March 2025 Central Public Sector Enterprise TReDS mandate requiring registration for corporations with annual revenues above Rs 250 Crores (approximately USD 29 Million).

The regulatory environment for supply chain finance platforms is consolidating around four frameworks. The International Chamber of Commerce (ICC) Standard Definitions for Techniques of Supply Chain Finance defines payables and receivables instrument categories that auditors apply under IFRS IAS 7. The UK Cabinet Office released a suppliers' guide to the Procurement Act 2023 in February 2025. The EU's Late Payment Regulation under negotiation through 2024-2025 constrains buyer payment terms across the 27-member bloc. In India, the Reserve Bank of India's Trade Receivables Discounting System (TReDS) mandate effective March 2025 requires Central Public Sector Enterprises and corporations above the Rs 250 Crore revenue threshold to onboard, supported by platforms including C2treds, RXIL, and M1xchange.

Demand is broadening across buyer, supplier, and funder counterparties. SAP Taulia released receivables and payables financing solutions on SAP Cloud ERP in February 2025, targeting the US, Canada, UK, DACH, and Singapore markets, and embedded SAP Taulia Virtual Cards inside SAP Ariba for pay-on-purchase-order transactions. C2FO signed 17 new dynamic supplier finance programs in 2024 and maintains 16 bank funding partners. PrimeRevenue operates across 90+ countries with 59,000+ suppliers and 105+ funding partners. Kyriba deployed the Bank of Africa working capital platform across 20 countries in July 2025, and Thales-NxtGen brought supply chain finance-adjacent sovereign cloud capabilities to India in May 2025 for regulated enterprise workloads.

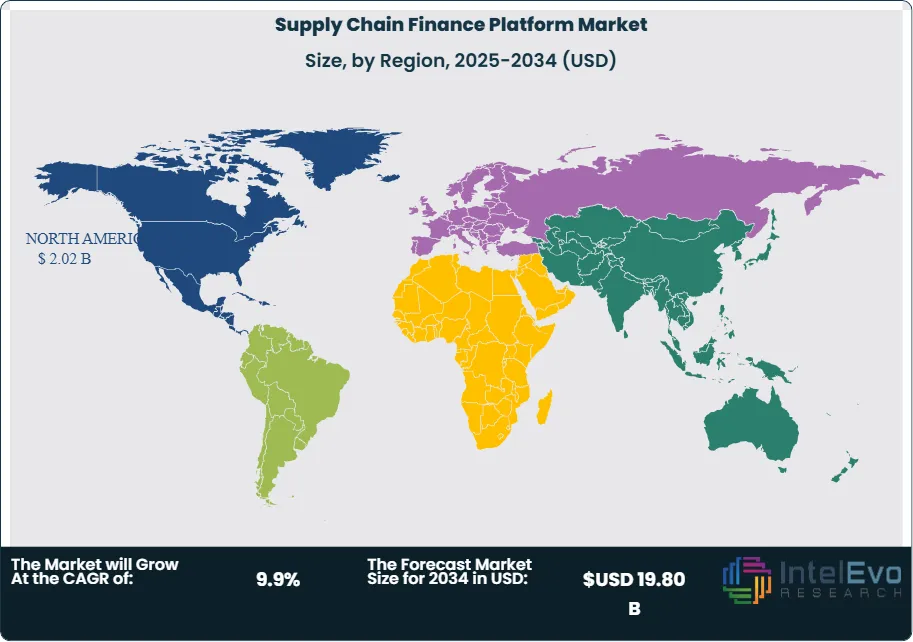

Asia Pacific held the largest supply chain finance platform market share at 41.5% in 2025, approximately USD 3.51 Billion, anchored by China's Industrial and Commercial Bank of China, Export-Import Bank of China, Bank of China, and Agricultural Bank of China, plus Japan's MUFG and DBS Bank in Singapore, and India's Vayana Network, C2treds, and M1xchange. Europe held 24.8% through HSBC, BNP Paribas, Deutsche Bank, Standard Chartered, Finastra, and Demica. North America held 23.9% through SAP Taulia, PrimeRevenue, C2FO, Kyriba, JPMorgan Chase, Citigroup, and Bank of America. The supply chain finance platform technology roadmap through 2034 tilts toward AI-driven credit assessment, agentic treasury coaching (exemplified by Kyriba's TAI launched May 2025), deep-tier financing extending beyond Tier 1 suppliers, and sustainability-linked pricing on ESG-compliant supplier invoices.

Market Definition & Scope

The supply chain finance platform market is defined as the global commercial activity in technology platforms, hardware, services, and cloud-based networks that enable buyers, suppliers, and funders to execute payables-led and receivables-led working capital finance programs. The market encompasses reverse factoring, dynamic discounting, receivables financing, purchase order financing, inventory financing, export and import financing, and letter-of-credit digitization delivered through platforms including SAP Taulia, PrimeRevenue, C2FO, Kyriba, Demica, Tradeshift, Finastra Fusion Trade Innovation, and Oracle Cash Management.

Included in the scope are platform license and subscription revenues, per-invoice transaction fees, bank funder API-integration fees, treasury-network access fees, and complementary treasury management system integrations with supply chain finance modules. Explicitly excluded are pure commercial lending balances funded by banks without platform technology delivery, retail consumer Buy Now Pay Later, pure payment-rail transactions without working-capital intermediation, and traditional factoring bureaus without digital onboarding. The supply chain finance platform market is a subset of the broader USD 13.4 Billion global trade finance category and sits adjacent to the larger global treasury management system category.

, By Provider (Banks & Financial Institutions, Fintech Companies, Technology Platform Providers, Non-Bank Financial Institutions), By Deployment Mode (Cloud-Based, On-Premises, Hybrid), By Enterprise Size (Large Enterprises, SMEs), By End-User Vertical (Manufacturing, Retail & E-Commerce, Healthcare & Pharmaceuticals, Automotive, Transportation & Logistics, Energy & Utilities, IT & Telecommunications) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The supply chain finance platform market expands from USD 8.45 Billion in 2025 to USD 19.80 Billion by 2034, a CAGR of 9.9% over the forecast period.

- Segment Dominance by Offering: Reverse factoring and payables-led supply chain finance led in 2025 with 42.8% share, anchored by SAP Taulia, PrimeRevenue, C2FO Dynamic Supplier Finance, and Demica programs.

- Segment Dominance by Provider: Banks represented 88.6% of 2025 provider share per IMARC Group, dominated by HSBC, Citigroup, Standard Chartered, BNP Paribas, Deutsche Bank, JPMorgan Chase, and DBS Bank funding platform programs.

- Driver: Non-bank working capital funding volumes scaled materially, with C2FO surpassing USD 400 Billion in lifetime funding and a USD 1 Billion daily funding milestone in December 2024 across 42 million invoices.

- Restraint: Post-Greensill Capital insolvency supervisory scrutiny continues to constrain buyer aggressive term-extension programs, and IFRS IAS 7 disclosure requirements introduced in 2024 raise transparency obligations.

- Opportunity: India's RBI TReDS mandate effective March 2025 requires Central Public Sector Enterprise and above-Rs 250 Crore corporate onboarding, creating a pipeline of 300+ MSMEs already onboarded via C2treds with USD 200 Million funded.

- Trend: Agentic AI embedded into treasury and working-capital platforms expanded in 2025, evidenced by Kyriba's TAI launched May 13, 2025 and SAP Taulia's AI-driven liquidity forecasting rollouts.

- Regional: Asia Pacific led the supply chain finance platform market with 41.5% share and approximately USD 3.51 Billion in revenue in 2025, followed by Europe at 24.8%.

Key Insights Summary

- SAP Taulia grew transaction volume from USD 500 Billion to USD 800 Billion over the three years following SAP's March 2022 majority-stake acquisition, per the SAP News Center's August 2025 interview with Thomas Mehlkopf, Global Chief Revenue Officer for Treasury and Working Capital Management at SAP, with one oil and gas enterprise customer saving nearly EUR 700,000 in a single month (annualizing to approximately EUR 8 Million).

- C2FO surpassed USD 400 Billion in lifetime funding to its customers in December 2024 and achieved its first USD 1 Billion day of daily funding, facilitating early payment on more than 42 million invoices in 2024 paid on average 32 days early to suppliers across 200 global enterprise clients including six of the Fortune 10, per the company's January 14, 2025 press release and April 14, 2025 USD 30 Million IFC-led funding round announcement.

- PrimeRevenue facilitated more than USD 300 Billion in commerce in 2025, accelerated payments on over 16 million invoices totaling USD 80 Billion, and enabled suppliers to receive payments on average 86 days earlier across 59,000 suppliers in 102 countries supported by 105+ funding partners, per the company's April 2026 GTR 2026 Leaders in Trade Awards finalist announcement.

- Kyriba launched TAI agentic AI for safe, compliant use of generative AI in finance operations on May 13, 2025, deployed the Bank of Africa Group working capital platform across 20 countries on July 23, 2025, reached its 1,000th French customer go-live with a new Paris office on April 1, 2025, and expanded Brazilian operations on November 12, 2025, per Business Wire releases.

- SAP released SAP Taulia receivables financing and payables financing solutions on SAP Cloud ERP in February 2025 targeting US, Canada, UK, DACH, and Singapore markets, and embedded SAP Taulia Virtual Cards into SAP Ariba for pay-on-purchase-order transactions to pre-fund supplier fulfilment, per SAP News Center August 2025 reporting.

- India's Reserve Bank of India TReDS mandate effective March 2025 required all Central Public Sector Enterprises and corporations with annual revenues above Rs 250 Crores (approximately USD 29 Million) to onboard trade receivables discounting platforms, with C2treds already facilitating USD 200 Million of funding to more than 300 MSMEs per C2FO's January 14, 2025 disclosure.

- The IFC's October 2024 partnership with C2FO to launch the first nationwide MSME working capital platform in Africa (starting in Nigeria in 2025) is estimated to unlock approximately USD 25 Billion in annual MSME financing, with an IFC estimate that every USD 1 Million of developing-country working capital creates 16 new jobs over two years.

Competitive Landscape Overview

The supply chain finance platform market is moderately consolidated across three distinct tiers. The top four technology platforms, SAP Taulia, PrimeRevenue, C2FO, and Demica, together processed over USD 1.5 Trillion in cumulative supplier working capital through 2025 and anchor an estimated 35.4% of combined platform-revenue share, with banks providing 88.6% of underlying funding liquidity per IMARC Group. Competition is platform-depth and multi-funder-breadth led rather than price-led, because ERP integration depth, funder network scale, and onboarding speed determine program adoption more than invoice-financing discount rates.

Competitive dynamics shifted materially through 2025. SAP Taulia grew transaction volume to USD 800 Billion, embedded Virtual Cards into SAP Ariba, and released cloud ERP-native SCF modules in February 2025. C2FO closed USD 30 Million from IFC on April 14, 2025 to scale African MSME lending, following its December 2024 USD 400 Billion lifetime-funding milestone. PrimeRevenue integrated Plaid ID verification in September 2025 and appointed Stefanie Nelsen as VP Payment Solutions in October 2025 after rehiring Eric Riddle as SVP Global Market Strategy in July 2025. Kyriba launched TAI agentic AI in May 2025 and deployed Bank of Africa's 20-country working capital platform in July 2025. Bank-led entrants including Mashreq partnered with Kyriba for LuLu Group in January 2025, demonstrating sustained bank-platform collaboration.

Competitive Landscape Matrix:

| Company | Headquarters | Position | Key Product | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| SAP Taulia (SAP SE) | United States / Germany | Leader | SAP Taulia Payables Financing; Dynamic Discounting; Virtual Cards | North America, Europe, APAC | Grew transaction volume from USD 500 Billion to USD 800 Billion over three years post-2022 SAP acquisition |

| PrimeRevenue, Inc. | United States | Leader | PrimeRevenue SCF platform; OpenSCi; Receivables Finance; B2B Payments | North America, Europe, APAC | Facilitated over USD 300 Billion in commerce and 16 million invoices totaling USD 80 Billion in 2025 |

| C2FO, Inc. | United States | Leader | C2FO Dynamic Supplier Finance; Name Your Rate; C2treds India | North America, EMEA, India | Closed USD 30 Million IFC-led round in April 2025 to expand African MSME platform for Nigeria launch |

| Demica Limited | United Kingdom | Leader | Demica SCF platform; white-labeled receivables finance | Europe, North America | Extended Mastercard SCF embed partnership to accelerate bank-funder working-capital deployments through 2025 |

| Kyriba Corp. (Bridgepoint Group) | United States | Challenger | Kyriba Liquidity Performance Platform; Supply Chain Finance; TAI agentic AI | North America, Europe, APAC, LatAm | Launched TAI agentic AI in May 2025; deployed Bank of Africa working capital platform across 20 countries in July 2025 |

| Tradeshift Holdings, Inc. | United States | Challenger | Tradeshift Pay; Tradeshift Go; Buy Now Pay Later for B2B | Europe, North America, APAC | Scaled embedded Tradeshift Pay working-capital modules via the HSBC joint venture through 2025 |

| Finastra International Limited | United Kingdom | Challenger | Fusion Trade Innovation; Fusion Corporate Channels; Fusion Essence | Europe, North America, APAC | Expanded Fusion Trade Innovation across more than 80 bank customers globally through 2025 |

| Oracle Corporation (NYSE: ORCL) | United States | Niche Player | Oracle Supply Chain Planning Cloud; Oracle Cash Management SCF | North America, Europe, APAC | Integrated AI Agents for Finance into Oracle Cloud ERP, supporting SCF workflows through 2025 |

| Incomlend Pte Ltd | Singapore | Niche Player | Incomlend invoice financing marketplace | APAC, Europe | Expanded Asia-Europe invoice-financing corridors for MSME suppliers through 2025 |

| Vayana Network | India | Niche Player | Vayana TradeXchange; Deep-Tier Financing | India, Southeast Asia | Scaled deep-tier supply chain finance programs for Indian corporates under TReDS framework through 2025 |

Segmentation Analysis

The supply chain finance platform market segments by offering type, provider, deployment mode, enterprise size, and end-user vertical. Each segmentation type maps to distinct buying criteria on a supply chain finance platform procurement checklist, including ERP integration depth, multi-funder breadth, regulatory alignment with IFRS IAS 7, and onboarding speed.

By Offering

Reverse factoring and payables-led supply chain finance led the supply chain finance platform market at 42.8% share in 2025, approximately USD 3.62 Billion, dominated by SAP Taulia, PrimeRevenue, C2FO Dynamic Supplier Finance, and Demica. Buyers use reverse factoring to extend payment terms from 45 to 90 days while allowing suppliers early payment through third-party funders, as illustrated in Taulia's Zanders case study where payment terms doubled without supplier liquidity impact. Receivables financing and invoice discounting held 24.6%, approximately USD 2.08 Billion, led by supplier-driven platforms including C2FO, C2treds, Vayana Network, and Incomlend.

Dynamic discounting held 13.2% of 2025 revenue, approximately USD 1.12 Billion, anchored by SAP Taulia's static and dynamic discounting, C2FO's patented Name Your Rate technology, and PrimeRevenue early-payment programs where buyers self-fund early payments from their own balance sheet in exchange for graduated discounts. Purchase order financing held 9.4%, inventory financing held 6.8%, and export-import financing and letter of credit digitization held 3.2%. The supply chain finance platform pricing benchmark typically reflects a 50 to 200 basis point spread over benchmark rates for bank-funded programs, with C2FO's Name Your Rate allowing suppliers to set their own acceptable discount through reverse auction.

By Provider

Banks held 88.6% of supply chain finance platform provider share in 2025 per IMARC Group, approximately USD 7.49 Billion of funded volume, led by HSBC, Citigroup, Standard Chartered, BNP Paribas, Deutsche Bank, JPMorgan Chase, DBS Bank, Mitsubishi UFJ Financial Group, and Industrial and Commercial Bank of China. Bank funder advantages include balance-sheet scale, cross-border currency expertise, and AML/KYC infrastructure. Fintech platforms and non-bank providers held 9.4% of 2025 funding share, approximately USD 794 Million, through dedicated working capital funds and institutional investors on C2FO, PrimeRevenue, Demica, and Incomlend.

Trade finance houses and specialist funders held 2.0%, approximately USD 169 Million, covering Allianz Trade (formerly Euler Hermes), Atradius, and specialized alternative credit firms. The fastest-growing provider sub-segment is non-bank digital platforms, which PrimeRevenue credited with accelerated adoption through its 2025 analyst commentary published on Martini.ai noting PrimeRevenue maintained an average credit spread of 6.167% from November 2021 to October 2025 despite macroeconomic volatility. Bank-platform joint ventures dominate a growing tier, with SAP inviting strategic banking partners to become Taulia equity partners, JPMorgan Chase maintaining its Taulia strategic alliance, and Mastercard-Demica extending SCF embeds.

By Deployment Mode

Cloud-based deployment led the supply chain finance platform market at 74.6% share in 2025, approximately USD 6.30 Billion, reflecting the migration of SAP Taulia onto SAP S/4HANA Cloud Public Edition, Kyriba's native SaaS treasury platform, PrimeRevenue's global cloud network, and C2FO's multi-tenant dynamic discounting engine. On-premises deployment held 25.4%, approximately USD 2.15 Billion, concentrated in large banks with legacy mainframe integrations and in government and defense buyers requiring sovereign-cloud or air-gapped architectures. The fastest-growing deployment sub-segment is hybrid cloud with sovereign-data-residency, exemplified by NxtGen-Thales post-quantum sovereign cloud partnerships announced May 2025 for India's regulated enterprise workloads, and by Bank of Africa's July 2025 Kyriba rollout across 20 African countries.

By Enterprise Size

Large enterprises held the largest share of the supply chain finance platform market at 76.8% in 2025, approximately USD 6.49 Billion, reflecting volume-driven pricing models and deep ERP integration requirements. Large enterprise anchor buyers include six Fortune 10 companies running C2FO programs, OTTO Group running PrimeRevenue, LuLu Group partnering with Mashreq on Kyriba, and BT Sourced running C2FO Dynamic Supplier Finance presented at TOLSON VDA Paris 2024. Small and medium-sized enterprises held 23.2%, approximately USD 1.96 Billion, with adoption accelerated by India's TReDS mandate effective March 2025 and by IFC's Africa MSME working capital platform launch planned for late 2025 in Nigeria.

The fastest-growing enterprise-size sub-segment is mid-market SMEs adopting deep-tier financing that extends beyond Tier 1 suppliers, exemplified by Vayana Network's Indian deep-tier programs and C2FO's prioritization of reaching beyond top-10% supplier concentrations. The supply chain finance platform ROI calculation for large enterprises typically compares days payable outstanding (DPO) extension against weighted average cost of capital (WACC) savings, generating payback inside 6 to 18 months for programs above USD 200 Million annual payables throughput per PrimeRevenue's 2025 public case study library.

By End-User Vertical

Manufacturing held the largest supply chain finance platform vertical share at 27.6% in 2025, approximately USD 2.33 Billion, covering automotive, industrial, aerospace, and heavy-machinery buyers running multi-tier supplier financing. Retail and consumer goods held 18.4%, projected to record the highest vertical CAGR of 12.0% through 2035 per Research Nester, driven by complex global supply chains, seasonality, and ESG-sourcing pressure. Pharmaceuticals and healthcare held 12.8%, led by programs across Senores Pharmaceuticals, which acquired 14 ANDAs from Dr. Reddy's Laboratories in March 2025 supporting working-capital-intensive generics programs.

Automotive held 10.6%, with tiered-supplier financing models pushed deep through OEM suppliers. Electronics and semiconductors held 8.4%, chemicals held 6.2%, food and beverages held 5.8%, logistics and transportation held 5.2%, and other verticals including energy held 5.0%. The supply chain finance platform compliance checklist by vertical includes EU MiFID II for financial-services end-users, FDA 21 CFR Part 11 for pharma electronic records, and automotive IATF 16949 for tier-one supplier program integrity.

Regional Analysis

The supply chain finance platform market is geographically led by Asia Pacific, Europe, and North America, together accounting for 90.2% of 2025 revenue. Regional dynamics differ on supplier-base concentration, bank-platform ecosystem maturity, and sovereign-cloud regulatory posture, with Asia Pacific leading on volume and North America leading on pricing power.

North America

North America held 23.9% of the supply chain finance platform market in 2025, approximately USD 2.02 Billion. The United States dominates with SAP Taulia headquartered in San Francisco, PrimeRevenue in Atlanta, C2FO in Kansas City, Kyriba in San Diego, JPMorgan Chase in New York, Citigroup, Bank of America, and Oracle. Canada contributes through Scotiabank and RBC trade finance platforms. Mexico is an emerging buyer market through automotive and consumer-goods supply chains with Tradeshift and Kyriba deployments. The US Federal Reserve's guidance on supply chain finance disclosures under IFRS IAS 7 (as endorsed by the IASB in 2023) and SEC Division of Corporation Finance's December 2020 dear-CFO letter frame North American supply chain finance platform compliance requirements. Post-Greensill regulatory scrutiny continues to shape buyer aggressive-payment-term programs.

Europe

Europe accounted for 24.8% of the supply chain finance platform market in 2025, approximately USD 2.10 Billion. The United Kingdom leads through Demica in London, Finastra, HSBC, and Standard Chartered; Germany hosts Deutsche Bank and SAP (as SAP Taulia's parent). France contributes through BNP Paribas, Kyriba's Paris office (which passed 1,000 French customer go-lives on April 1, 2025), and Societe Generale. Italy hosts UniCredit and Intesa Sanpaolo bank-led programs. The EU Late Payment Regulation under negotiation through 2024-2025 sets maximum payment terms across the 27-member bloc, and the UK Cabinet Office's February 2025 Procurement Act 2023 suppliers' guide reinforces payment-discipline frameworks. The European Banking Authority and European Central Bank oversee bank-funder prudential treatment of supply chain finance balances under CRR III and Basel III.1 finalization.

Asia Pacific

Asia Pacific held 41.5% of the supply chain finance platform market in 2025, approximately USD 3.51 Billion, the leading region by volume. China dominates with Industrial and Commercial Bank of China, Export-Import Bank of China, Bank of China, Agricultural Bank of China, Ant Group, and Alibaba running domestic SCF platforms at massive scale. Japan contributes through MUFG and Mizuho programs. Singapore hosts DBS Bank and Incomlend. India hosts Vayana Network, RXIL, M1xchange, C2treds, and Finastra's Fusion Trade Innovation deployments, with the RBI TReDS mandate effective March 2025 driving 300+ MSMEs onto C2treds and USD 200 Million of recorded MSME funding. Hong Kong, South Korea, Thailand, and Vietnam contribute through regional supplier bases to multinational programs. The Asian Development Bank's Trade and Supply Chain Finance Program funds underwriting gaps in Asian emerging markets.

Latin America

Latin America held 6.4% of the supply chain finance platform market in 2025, approximately USD 541 Million. Brazil leads through Itau Unibanco, Banco do Brasil, and Bradesco bank-led programs plus Kyriba's November 12, 2025 Brazil operations expansion. Mexico follows through BBVA Bancomer and Citibanamex, driven by automotive and consumer-goods supply chains. Chile, Colombia, and Argentina contribute emerging SCF platform deployments. The Banco Central do Brasil's PIX payment rail accelerates invoice-reconciliation automation, supporting supply chain finance platform onboarding for Brazilian SMEs. The Banco Central de la Republica Argentina's and Banco de la Republica Colombia's regulatory frameworks for receivables financing align with ICC Standard Definitions.

Middle East & Africa

Middle East & Africa accounted for 3.4% of the supply chain finance platform market in 2025, approximately USD 287 Million. The United Arab Emirates leads regional adoption through Mashreq Bank, Emirates NBD, and Abu Dhabi Commercial Bank, with Mashreq partnering with Kyriba to customize finance transactions for LuLu Group in January 2025. Saudi Arabia follows through Saudi National Bank and Al Rajhi Bank under Vision 2030 digital-finance programs. Egypt contributes through Commercial International Bank. Sub-Saharan Africa is anchored by Bank of Africa Group's July 23, 2025 Kyriba working capital platform rollout across 20 African countries and by C2FO's IFC-backed Nigeria nationwide MSME platform expected to unlock approximately USD 25 Billion in annual MSME financing. South Africa hosts Standard Bank and Absa bank-led programs.

Country Analysis

Four national supply chain finance platform markets, the United States, China, India, and the United Kingdom, collectively accounted for approximately 61.2% of 2025 revenue. These countries concentrate platform vendor headquarters, bank funder liquidity, and the regulatory frameworks that set supply chain finance platform procurement timelines.

United States

The United States represented approximately USD 1.82 Billion in 2025 supply chain finance platform revenue, with a country CAGR estimated at 10.4% through 2034. SAP Taulia in San Francisco, PrimeRevenue in Atlanta, C2FO in Kansas City, Kyriba in San Diego, and Oracle in Austin anchor the national platform supplier base. Major bank funders include JPMorgan Chase, Citigroup, and Bank of America. The SEC's December 2020 dear-CFO letter and subsequent IFRS IAS 7 amendments endorsed by the Financial Accounting Standards Board (FASB) through ASU 2022-04 require disclosure of supplier finance program outstanding obligations. The Office of the Comptroller of the Currency (OCC) and the Federal Reserve's joint 2023 supervisory letter on third-party risk management applies to bank-platform arrangements. US tariff implementation in 2025 reshaped supplier relationships and cash-flow dynamics, driving SCF platform adoption for liquidity optimization.

China

China represented approximately USD 1.68 Billion in 2025 supply chain finance platform revenue, with a country CAGR estimated at 10.8% through 2034. Industrial and Commercial Bank of China, Export-Import Bank of China, Bank of China, Agricultural Bank of China, and China Construction Bank dominate bank-led SCF programs. Ant Group, Alibaba, and JD.com anchor domestic fintech platform deployments. The People's Bank of China (PBoC) and the State Administration of Foreign Exchange (SAFE) govern cross-border supply chain finance flows, and China's Supply Chain Innovation and Application Pilot Program launched by eight ministries in 2018 continues to drive domestic adoption. China's e-invoicing mandate rolled out progressively through 2024-2025 supports digital reconciliation underlying SCF platform onboarding.

India

India represented approximately USD 658 Million in 2025 supply chain finance platform revenue, with a country CAGR estimated at 13.2% through 2034, the fastest among the four profiled countries. Vayana Network in Mumbai, RXIL, M1xchange, and C2treds anchor the domestic platform supplier base. DBS Bank India, HSBC India, and Standard Chartered India provide funder liquidity. The Reserve Bank of India's March 2025 TReDS mandate requires all Central Public Sector Enterprises and corporations above Rs 250 Crores annual revenue to onboard trade receivables discounting platforms, with C2treds alone facilitating USD 200 Million to 300+ MSMEs. The Goods and Services Tax Network (GSTN) e-invoice mandate from October 2020 (progressively extended through 2025 to cover taxpayers above Rs 5 Crore annual turnover) underpins invoice-integrity checks across SCF platforms.

United Kingdom

The United Kingdom represented approximately USD 517 Million in 2025 supply chain finance platform revenue, with a country CAGR estimated at 9.6% through 2034. Demica in London, Finastra, Orbian, and Tradeshift anchor UK platform suppliers, with HSBC, Standard Chartered, Barclays, Lloyds, and NatWest providing bank funder liquidity. The UK Cabinet Office released the February 2025 Procurement Act 2023 suppliers' guide including simpler SCF arrangements for public-sector buyer programs. The Financial Conduct Authority (FCA) and Prudential Regulation Authority (PRA) supervise bank SCF balances under PS10/24 and related prudential guidance. The UK Prompt Payment Code administered by the Small Business Commissioner reinforces payment-discipline obligations on large buyer signatories.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Offering

- Platforms & Software Solutions

- Services

By Provider

- Banks & Financial Institutions

- Fintech Companies

- Technology Platform Providers

- Non-Bank Financial Institutions (NBFIs)

By Deployment Mode

- Cloud-Based

- On-Premises

- Hybrid

By Enterprise Size

- Large Enterprises

- Small & Medium Enterprises (SMEs)

By End-User Vertical

- Manufacturing

- Retail & E-Commerce

- Healthcare & Pharmaceuticals

- Automotive

- Transportation & Logistics

- Energy & Utilities

- IT & Telecommunications

- Others (Food & Beverage, Consumer Goods, Chemicals)

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 8.45 B |

| Forecast Revenue (2034) | USD 19.80 B |

| CAGR (2025-2034) | 9.9% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Offering, (Platforms & Software Solutions, Services), By Provider, (Banks & Financial Institutions, Fintech Companies, Technology Platform Providers, Non-Bank Financial Institutions (NBFIs)), By Deployment Mode, (Cloud-Based, On-Premises, Hybrid), By Enterprise Size, (Large Enterprises, Small & Medium Enterprises (SMEs)), By End-User Vertical, (Manufacturing, Retail & E-Commerce, Healthcare & Pharmaceuticals, Automotive, Transportation & Logistics, Energy & Utilities, IT & Telecommunications, Others (Food & Beverage, Consumer Goods, Chemicals)) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | SAP TAULIA (SAP SE), PRIMEREVENUE, INC., C2FO, INC., DEMICA LIMITED, KYRIBA CORP. (BRIDGEPOINT GROUP), TRADESHIFT HOLDINGS, INC., FINASTRA INTERNATIONAL LIMITED, ORACLE CORPORATION (NYSE: ORCL), INCOMLEND PTE LTD, VAYANA NETWORK PVT LTD, ORBIAN FINANCIAL SERVICES III LLC, JPMORGAN CHASE & CO. (NYSE: JPM), CITIGROUP INC. (NYSE: C), HSBC HOLDINGS PLC (LON: HSBA), STANDARD CHARTERED PLC (LON: STAN), BNP PARIBAS (EPA: BNP), DEUTSCHE BANK AG (ETR: DBK), DBS BANK LTD, MITSUBISHI UFJ FINANCIAL GROUP, INC. (TYO: 8306), ANT GROUP CO., LTD., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Provider (Banks & Financial Institutions, Fintech Companies, Technology Platform Providers, Non-Bank Financial Institutions), By Deployment Mode (Cloud-Based, On-Premises, Hybrid), By Enterprise Size (Large Enterprises, SMEs), By End-User Vertical (Manufacturing, Retail & E-Commerce, Healthcare & Pharmaceuticals, Automotive, Transportation & Logistics, Energy & Utilities, IT & Telecommunications) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

, By Provider (Banks & Financial Institutions, Fintech Companies, Technology Platform Providers, Non-Bank Financial Institutions), By Deployment Mode (Cloud-Based, On-Premises, Hybrid), By Enterprise Size (Large Enterprises, SMEs), By End-User Vertical (Manufacturing, Retail & E-Commerce, Healthcare & Pharmaceuticals, Automotive, Transportation & Logistics, Energy & Utilities, IT & Telecommunications) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

, By Provider (Banks & Financial Institutions, Fintech Companies, Technology Platform Providers, Non-Bank Financial Institutions), By Deployment Mode (Cloud-Based, On-Premises, Hybrid), By Enterprise Size (Large Enterprises, SMEs), By End-User Vertical (Manufacturing, Retail & E-Commerce, Healthcare & Pharmaceuticals, Automotive, Transportation & Logistics, Energy & Utilities, IT & Telecommunications) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Supply Chain Finance Platform Market?

The Global Supply Chain Finance Platform Market was valued at USD 7.65 Billion in 2024 and is projected to reach USD 19.80 Billion by 2034, growing at a CAGR of 9.9% from 2026 to 2034. Growth is driven by increasing demand for working capital optimization, supplier financing, invoice automation, trade finance digitalization, blockchain-enabled finance platforms, AI-powered analytics, cloud-based financial solutions, and expanding global supply chain networks.

Who are the major players in the Supply Chain Finance Platform Market?

SAP TAULIA (SAP SE), PRIMEREVENUE, INC., C2FO, INC., DEMICA LIMITED, KYRIBA CORP. (BRIDGEPOINT GROUP), TRADESHIFT HOLDINGS, INC., FINASTRA INTERNATIONAL LIMITED, ORACLE CORPORATION (NYSE: ORCL), INCOMLEND PTE LTD, VAYANA NETWORK PVT LTD, ORBIAN FINANCIAL SERVICES III LLC, JPMORGAN CHASE & CO. (NYSE: JPM), CITIGROUP INC. (NYSE: C), HSBC HOLDINGS PLC (LON: HSBA), STANDARD CHARTERED PLC (LON: STAN), BNP PARIBAS (EPA: BNP), DEUTSCHE BANK AG (ETR: DBK), DBS BANK LTD, MITSUBISHI UFJ FINANCIAL GROUP, INC. (TYO: 8306), ANT GROUP CO., LTD., Others

Which segments covered the Supply Chain Finance Platform Market?

By Offering, (Platforms & Software Solutions, Services), By Provider, (Banks & Financial Institutions, Fintech Companies, Technology Platform Providers, Non-Bank Financial Institutions (NBFIs)), By Deployment Mode, (Cloud-Based, On-Premises, Hybrid), By Enterprise Size, (Large Enterprises, Small & Medium Enterprises (SMEs)), By End-User Vertical, (Manufacturing, Retail & E-Commerce, Healthcare & Pharmaceuticals, Automotive, Transportation & Logistics, Energy & Utilities, IT & Telecommunications, Others (Food & Beverage, Consumer Goods, Chemicals))

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Supply Chain Finance Platform Market

Published Date : 03 Jun 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date