- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Surgical Robotics Software Market Size, Share | CAGR 19.1%

Global Surgical Robotics Software Market Size, Share & Industry Analysis By Software Type (Surgical Planning and Simulation, Navigation and Guidance, Robotic Control, Imaging and Visualization, AI-Enabled Surgical, Data Analytics and Performance Monitoring, Training and Education, Workflow Management), By Application (General Surgery, Orthopedic Surgery, Neurosurgery, Urology, Gynecology, Cardiothoracic Surgery, Gastrointestinal Surgery, ENT Surgery, Oncology and Ophthalmic Surgery), By Deployment (On-Premises, Cloud-Based and Hybrid) Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Strategies, Emerging Trends and Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

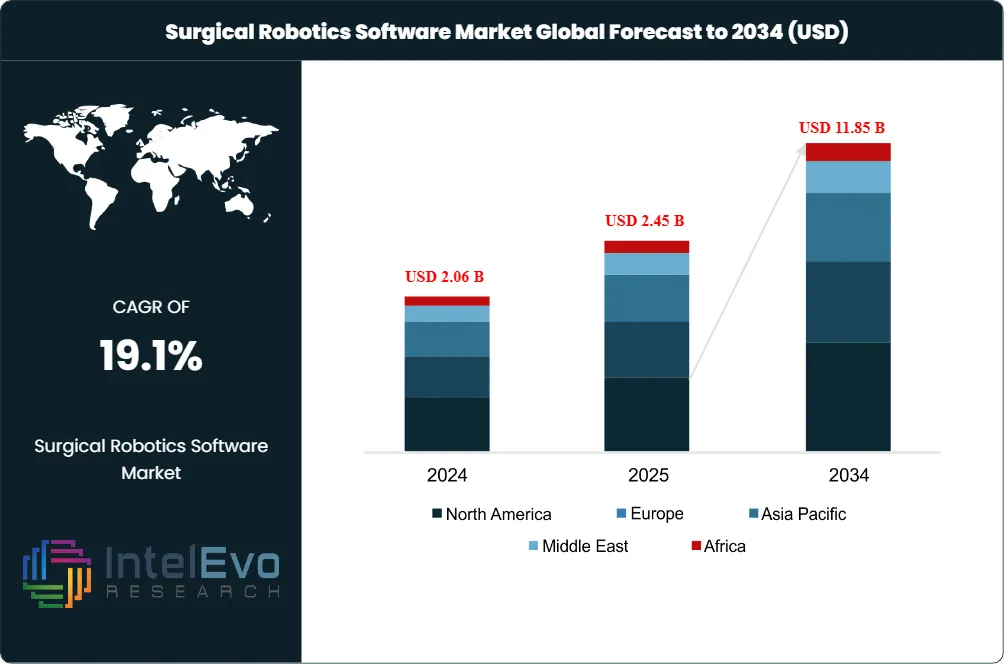

| USD 2.45 Billion | USD 11.85 Billion | 19.1% | North America, 51.4% |

The Surgical Robotics Software Market was valued at USD 2.06 Billion in 2024 and USD 2.45 Billion in 2025. The market is projected to reach USD 11.85 Billion by 2034, expanding at a CAGR of 19.1% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 9.40 Billion over the analysis period. Surgical robotics software is the digital intelligence layer that controls, navigates, and augments robotic surgical systems, encompassing preoperative 3D planning platforms, AI-driven intraoperative navigation, computer-vision tissue recognition, surgical video analytics, digital-twin simulation environments, fleet-management cloud platforms, and postoperative outcome analytics tied to electronic health record systems.

Get More Information about this report -

Request Free Sample ReportThe software category is the fastest-growing segment of the broader surgical robotics market (USD 12.49 Billion in 2025 per industry analysis), expanding at nearly twice the rate of the underlying hardware platforms because manufacturers are shifting revenue from upfront system pricing toward recurring software subscriptions, AI feature unlocks, and procedure-level licensing. A 2025 peer-reviewed meta-analysis published in PMC synthesizing 25 studies on AI-driven robotic surgery (2024–2025) found that AI-powered surgical planning produced a 30% decrease in intraoperative complications across orthopedic, urologic, and general surgery procedures. Johns Hopkins researchers reported in 2025 that machine-learning algorithms based on convolutional neural networks now predict tissue motion and guide suture plans with accuracy approaching skilled human surgeons, validating the clinical foundation for autonomous and semi-autonomous software modules.

Regulatory clearances accelerated through 2025 across the surgical robotics software category. In April 2025, Intuitive Surgical received FDA clearance for the SureForm 45 stapler with SmartFire technology that monitors tissue compression in real time during single-port robotic urology procedures. In July 2025, Intuitive Surgical secured CE-mark clearance for the da Vinci 5, enabling European rollout of force-feedback-enabled fifth-generation software. In April 2025, Medtronic submitted its Hugo robotic-assisted surgery system to the FDA after the IDE study reported a 98.5% clinical success rate. In May 2024, Anaut Inc. received Japanese Ministry of Health approval for Eureka alpha, the first AI-driven software device that analyzes real-time video from laparoscopic and robotic surgery to enhance intraoperative decision support. In July 2025, Toumai (MicroPort/MedBot) received the Groundbreaking Technology award at the Surgical Robotics Industry Awards 2025 and holds regulatory clearance in over 30 countries as the first surgical robot approved globally for remote surgery applications across multiple specialties.

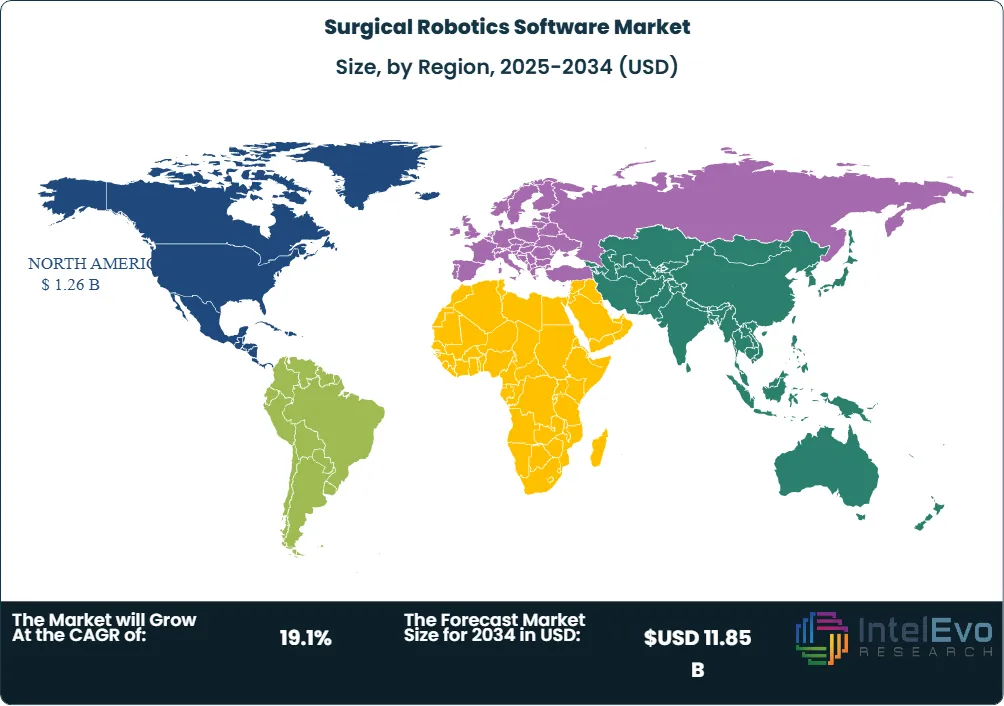

North America held 51.4% of the surgical robotics software market in 2025 at approximately USD 1.26 Billion, anchored by the United States where over 7,500 da Vinci surgical systems are installed and more than 11 million procedures have been performed using these platforms. Roughly 75% of U.S. prostate cancer surgeries are performed using da Vinci systems, generating substantial software-license and services revenue. Europe accounted for 23.6% at USD 578 million, supported by EU MDR-compliant device certification and the July 2025 CE-mark approval of da Vinci 5 across urologic, gynecologic, and general laparoscopic specialties. Asia Pacific represented 18.2% at USD 446 million and is projected to grow at the fastest regional CAGR of 22.4%, accelerated by India's January 2025 SSI Mantra telesurgery milestone covering 286 km with 40-millisecond latency.

Market Definition & Scope

The surgical robotics software market is defined as the global commercial segment for software platforms, AI modules, and digital intelligence services that enable, control, augment, or analyze robotic-assisted surgical procedures. The market encompasses preoperative planning software (3D anatomical reconstruction, surgical simulation, digital twins); intraoperative navigation and guidance software (image-guided surgery, augmented reality overlays, real-time tissue recognition); AI-driven decision support (computer vision, anatomical landmark detection, complication prediction); surgical video analytics platforms (case review, quality assurance, training); fleet-management and predictive-maintenance cloud platforms; and postoperative outcome analytics integrated with electronic health record systems.

This analysis includes both the proprietary software embedded in robotic surgical systems sold by hardware manufacturers and the standalone software platforms sold by independent vendors to hospitals operating multi-vendor robotic fleets. The report explicitly excludes the underlying robotic hardware and instruments, manual surgical instruments without robotic actuation, hospital electronic health record systems not specifically integrated with surgical robotics, and general medical imaging platforms without surgical workflow integration. The surgical robotics software market is the digital-intelligence subset of the broader surgical robotics market (USD 12.49 Billion in 2025) and intersects with the next-generation surgical robotics segment (USD 4.54 Billion in 2024) where AI capabilities are the primary differentiator.

, By Application (General Surgery, Orthopedic Surgery, Neurosurgery, Urology, Gynecology, Cardiothoracic Surgery, Gastrointestinal Surgery, ENT Surgery, Oncology and Ophthalmic Surgery), By Deployment (On-Premises, Cloud-Based and Hybrid) Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Strategies, Emerging Trends and Forecast 2026-2034")

Key Takeaways

- Market Growth: The surgical robotics software market grew from USD 2.45 Billion in 2025 to a projected USD 11.85 Billion by 2034, at a 19.1% CAGR, representing USD 9.40 Billion in absolute dollar opportunity.

- Segment Dominance (By Software Type): Intraoperative navigation and guidance software held the largest share at 38.4% in 2025 at approximately USD 941 million, anchored by Intuitive Surgical's da Vinci visualization platform that supports more than 11 million procedures performed globally on over 7,500 installed systems.

- Segment Dominance (By Application): Urology was the largest application segment in 2025 at 27.4% share and approximately USD 671 million, because roughly 75% of U.S. prostate cancer surgeries are performed using da Vinci systems with their integrated software suite.

- Driver: Recurring software revenue is reshaping vendor economics, with manufacturers bundling AI dashboards, fleet optimization consulting, and education portals to shift the income mix toward subscription streams. AI-powered surgical planning has demonstrated a 30% decrease in intraoperative complications per a 2025 PMC meta-analysis of 25 peer-reviewed studies.

- Restraint: Cybersecurity vulnerabilities and data ownership ambiguity create legal and reputational risk as robotic platforms become more software-driven and connected. Software glitches, integration challenges with existing hospital infrastructure, and the operational learning curve for surgeons remain primary adoption barriers.

- Opportunity: Telesurgery represents the largest expansion frontier, with India's SSI Mantra completing two world-first telesurgeries in January 2025 over 286 km with 40-millisecond latency, and MicroPort/MedBot's Toumai becoming the first surgical robot globally approved for remote surgery applications across multiple specialties in 2025.

- Trend: Open-architecture challengers including CMR Surgical's Versius are pressuring market leaders with 30 to 40% lower acquisition cost, forcing incumbents to defend margins through software bundling, fleet optimization consulting, and AI dashboard subscriptions that build recurring software revenue.

- Regional: North America led the surgical robotics software market with 51.4% share valued at USD 1.26 Billion in 2025, supported by the U.S. installed base of 7,500+ da Vinci systems and the April 2025 FDA submission of Medtronic's Hugo system following a 98.5% clinical success rate.

Key Insights Summary

- AI-powered surgical planning produced a 30% decrease in intraoperative complications according to a 2025 PMC meta-analysis synthesizing 25 peer-reviewed studies on AI-driven robotic surgery published between 2024 and 2025.

- More than 7,500 da Vinci surgical systems are installed worldwide as of early 2023, with over 11 million procedures performed using these platforms globally, generating the largest software-license and service revenue base in the category (industry analysis based on company filings).

- In April 2025, Medtronic submitted its Hugo robotic-assisted surgery system to the U.S. FDA after meeting primary safety and effectiveness endpoints in an IDE study, with the system reporting a 98.5% clinical success rate that supports the integrated software platform's regulatory pathway.

- In January 2025, India's SSI Mantra performed two world-first telesurgeries over a distance of 286 kilometers with a latency of only 40 milliseconds, validating the network-mediated software architecture that enables remote surgical capability.

- In July 2025, Intuitive Surgical's da Vinci 5 received CE-mark approval for adult and pediatric use across urologic, gynecologic, and general laparoscopic minimally invasive procedures in Europe, with force-feedback-enabled software representing the platform's primary differentiator.

- In May 2024, Anaut Inc. received Japanese Ministry of Health approval for Eureka alpha, the first AI-driven software device that analyzes real-time video from laparoscopic and robotic surgery to enhance surgeon accuracy, establishing a regulatory precedent for standalone surgical AI software in Japan.

Competitive Landscape Overview

The surgical robotics software market operates across three competitive tiers: integrated hardware-software platform manufacturers (Intuitive Surgical, Medtronic, Stryker, Zimmer Biomet, Smith & Nephew) that bundle proprietary software with their robotic systems; specialty software vendors (Brainlab, Theator, Caresyntax, Activ Surgical, Proprio, Proximie) that develop standalone platforms for navigation, video analytics, telesurgery, and AI-driven decision support; and emerging open-architecture challengers (CMR Surgical, Asensus Surgical, SS Innovations) that compete on cost-efficient platforms with progressively expanding software ecosystems. The top four integrated platform vendors collectively hold approximately 67% of the surgical robotics software market in 2025, with Intuitive Surgical's da Vinci ecosystem representing the largest single share. Open-architecture challengers promise 30 to 40% lower acquisition cost, forcing leaders to bundle AI dashboards, fleet optimization consulting, and education portals to shift revenue toward recurring software streams. Strategic M&A continues to reshape the landscape: Zimmer Biomet's USD 177 million acquisition of Monogram Technologies in July 2025 added autonomous orthopedic planning capabilities to the ROSA franchise; KARL STORZ acquired Asensus Surgical to integrate visualization heritage with sensor-rich instrumentation; Johnson & Johnson continues development of the OTTAVA platform integrating stapling and energy devices within a single arm architecture.

Competitive Landscape Matrix

| Company | HQ | Position | Key Software Platform | Geo Strength | Founded | Recent Strategic Move |

| Intuitive Surgical | US | Leader | da Vinci 5, Iris, Intuitive Hub | Global | 1995 | CE-mark da Vinci 5 (Jul 2025) |

| Medtronic | Ireland/US | Leader | Hugo console, Touch Surgery | Global | 1949 | Hugo FDA submission, 98.5% IDE success (Apr 2025) |

| Stryker | US | Leader | Mako SmartRobotics planning | Global | 1941 | Mako spine and shoulder expansion (2025) |

| Zimmer Biomet | US | Leader | ROSA Knee, ROSA Brain, Monogram | Global | 1927 | Monogram Technologies acquisition (Jul 2025) |

| Johnson & Johnson | US | Challenger | VELYS, OTTAVA, Monarch | Global | 1886 | VELYS knee global rollout, OTTAVA development |

| Brainlab | Germany | Challenger | Curve, Loop-X navigation | Global | 1989 | AI-driven cranial navigation expansion |

| CMR Surgical | UK | Challenger | Versius, Aportal cloud platform | UK, EU, Asia | 2014 | Aportal cloud analytics expansion (2025) |

| Smith & Nephew | UK | Challenger | CORI, Real Intelligence | Global | 1856 | CORI software platform updates (2025) |

By Software Type

Intraoperative navigation and guidance software dominated the surgical robotics software market with 38.4% share in 2025 at approximately USD 941 million. This segment includes image-guided surgery overlays, augmented reality visualization, real-time tissue recognition powered by computer vision, and force-feedback systems such as the haptic capabilities introduced in Intuitive Surgical's da Vinci 5 (CE-marked in July 2025). Brainlab's Curve and Loop-X platforms anchor the cranial navigation subsegment. Stryker's Mako SmartRobotics platform integrates real-time intraoperative guidance with preoperative planning for orthopedic procedures. The intraoperative software category has captured the highest software value because it is the regulatory-cleared decision-support layer that surgeons interact with continuously during cases.

Preoperative planning software held 22.6% of the surgical robotics software market at approximately USD 554 million in 2025. This segment includes 3D anatomical reconstruction, surgical simulation, and digital twin platforms that allow surgeons to rehearse procedures on patient-specific models before entering the operating room. Zimmer Biomet's July 2025 USD 177 million acquisition of Monogram Technologies added autonomous orthopedic planning for shoulder and knee arthroplasty to the ROSA franchise. Stryker's Mako planning module and Smith & Nephew's CORI Real Intelligence platform compete in orthopedic-focused planning. AI-powered digital twins now enable predictive modeling that customizes surgical strategies, with continued development through 2025 across hepato-biliary, neurosurgery, and reconstructive surgery applications.

Surgical video analytics platforms held 14.8% at approximately USD 363 million. Theator transforms surgical video into structured clinical data across 9 specialties and 180+ procedure types. Caresyntax provides AI-enabled surgical workflow analytics. Activ Surgical develops real-time computer vision overlays for intraoperative decision support. Medtronic's Touch Surgery platform delivers AI-driven case analysis. The category is gaining institutional purchase as hospitals seek quality analytics, operative report automation, and surgeon training data infrastructure.

Telesurgery and remote-assistance software accounted for 9.7% at approximately USD 238 million in 2025, including Proximie's collaborative platform and SSI Mantra's telesurgery infrastructure that achieved 286 km transmission with 40-millisecond latency in January 2025. Fleet management and predictive maintenance cloud software comprised 8.3% at USD 203 million, dominated by manufacturer-proprietary platforms such as Intuitive Hub. Postoperative analytics and outcome-tracking software made up the remaining 6.2% at USD 152 million, with EHR integration and quality reporting as primary use cases.

By Application

Urology represented the largest application segment of the surgical robotics software market in 2025 at 27.4% share and approximately USD 671 million, because roughly 75% of U.S. prostate cancer surgeries are performed using da Vinci systems and their integrated software suite. Intuitive Surgical's April 2025 FDA clearance of the SureForm 45 stapler with SmartFire technology specifically targets single-port robotic urology procedures. Orthopedic surgery held 24.1% at USD 590 million, with knee and hip replacement (over 790,000 knee and 544,000 hip replacements annually in the U.S. per the American College of Rheumatology, March 2025) as the highest-volume use cases for software-driven planning and intraoperative guidance. Gynecology accounted for 18.6% at USD 456 million; neurosurgery 11.4% at USD 279 million; general surgery 10.2% at USD 250 million; and cardiovascular and other specialties comprised the remaining 8.3% at USD 203 million.

By Deployment

Cloud-based and hybrid-cloud surgical robotics software accounted for 56.8% of the surgical robotics software market in 2025 at approximately USD 1.39 Billion, advancing at a 22.7% CAGR through 2034. Cloud deployment enables centralized AI model updates, fleet-wide performance analytics, and remote case proctoring. CMR Surgical's Aportal cloud platform demonstrates the open-architecture deployment model. On-premises deployment held 43.2% at USD 1.06 Billion, predominantly among large academic medical centers with strict data sovereignty requirements and existing investment in private surgical data infrastructure.

Regional Analysis

North America held the largest share of the surgical robotics software market at 51.4% in 2025, valued at approximately USD 1.26 Billion. The United States dominates regional demand through the installed base of more than 7,500 da Vinci surgical systems and the broader robotic platforms operated by Stryker (Mako), Zimmer Biomet (ROSA), Smith & Nephew (CORI), and Johnson & Johnson (VELYS). The April 2025 FDA submission of Medtronic's Hugo system following a 98.5% clinical success rate creates near-term demand expansion for integrated software. The U.S. surgical robotics market alone reached USD 4.46 Billion in 2025 with a 15.4% projected CAGR. Canada contributes approximately USD 95 million to regional software demand.

Europe accounted for 23.6% of the surgical robotics software market at approximately USD 578 million in 2025. Germany leads regional demand through high-quality healthcare infrastructure and favorable reimbursement policies. The July 2025 CE-mark approval of da Vinci 5 for adult and pediatric use across urologic, gynecologic, and general laparoscopic procedures expands the European software-licensing base. Brainlab, headquartered in Munich, anchors the European specialty software segment with cranial navigation, image-guided surgery, and AI-driven planning platforms. CMR Surgical, headquartered in Cambridge, UK, competes through Versius and the Aportal cloud platform. EU MDR (Medical Device Regulation) compliance requirements shape software certification timelines and create regulatory barriers to entry for new vendors.

Asia Pacific represented 18.2% of the surgical robotics software market at approximately USD 446 million in 2025 and is projected to grow at the fastest regional CAGR of 22.4% through 2034. India is leading regional innovation through SSI Mantra's January 2025 telesurgery milestone (286 km, 40-millisecond latency) and Krishna Institute of Medical Sciences' partnership with Intuitive (October 2024) to launch 25 robotic surgery programs across Maharashtra, Karnataka, Andhra Pradesh, and Telangana. Japan validated regulatory pathways for AI surgical software with Anaut Inc.'s Eureka alpha approval in May 2024. China's MicroPort/MedBot Toumai platform achieved regulatory clearance in over 30 countries by 2025. Ronovo Surgical announced a strategic partnership with Johnson & Johnson Medical Shanghai in September 2025 to expand surgical technology offerings to Chinese hospitals.

Latin America held 4.2% of the surgical robotics software market at approximately USD 103 million in 2025, with Brazil and Mexico as primary national markets. Middle East and Africa accounted for 2.6% at approximately USD 64 million. Both regions face capital constraints on robotic system procurement that limit software penetration despite growing surgical demand.

Country Analysis

The United States dominates the surgical robotics software market with an estimated value of USD 1.16 Billion in 2025 and a country-level CAGR of 19.8% through 2034. The country's installed base of more than 7,500 da Vinci systems generates the largest software-license and services revenue base globally. Roughly 75% of U.S. prostate cancer surgeries are performed using da Vinci systems. American hospitals conduct over 790,000 knee and 544,000 hip replacements annually per the American College of Rheumatology (March 2025), with software-driven planning and intraoperative guidance increasingly central to procedural workflows. April 2025 FDA milestones included Intuitive's SureForm 45 SmartFire clearance and Medtronic's Hugo IDE submission. Major U.S. headquarters include Intuitive Surgical (Sunnyvale, California), Stryker (Portage, Michigan), Johnson & Johnson MedTech (New Brunswick, New Jersey), and Zimmer Biomet (Warsaw, Indiana).

Germany represents Europe's largest national market for surgical robotics software at approximately USD 195 million in 2025 with a CAGR of 16.4%. Brainlab AG, headquartered in Munich, is one of the world's leading specialty software vendors for cranial navigation and image-guided surgery. Johnson & Johnson MedTech launched VELYS Robotic-Assisted Solution in the European market starting with successful Total Knee surgeries in Germany in October 2023, expanding software demand throughout 2024 and 2025. Germany's statutory health insurance system provides reimbursement coverage for robotic-assisted procedures, supporting hospital procurement of software-bundled robotic platforms.

Japan is a strategic national market valued at approximately USD 142 million in 2025 with a CAGR of 18.7%. The May 2024 approval of Anaut Inc.'s Eureka alpha by the Ministry of Health, Labour, and Welfare established the world's first regulatory clearance for AI-driven real-time video analysis software in laparoscopic and robotic surgery. Japanese academic medical centers maintain high-volume robotic surgery programs, and domestic device manufacturers including Kawasaki Medical and Sysmex compete in select software niches. The country's aging population (29% over age 65) drives sustained surgical procedure volumes.

India contributes approximately USD 108 million to the surgical robotics software market in 2025 with the highest country-level CAGR of 24.6%. SSI Mantra's January 2025 telesurgery milestone, performing two world-first procedures over 286 kilometers with 40-millisecond latency, established India as the global leader in network-mediated surgical software. Krishna Institute of Medical Sciences (KIMS) partnered with Intuitive in October 2024 to launch 25 robotic surgery programs across Maharashtra, Karnataka, Andhra Pradesh, and Telangana, expanding software demand in Tier 2 and Tier 3 cities. In June 2025, CTS Hospital launched Anna Nagar's first robotic-assisted knee replacement using the Johnson & Johnson VELYS platform with integrated planning and guidance software.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Software Type

- Surgical Planning and Simulation Software

- Navigation and Guidance Software

- Robotic Control Software

- Imaging and Visualization Software

- Data Analytics and Performance Monitoring Software

- Artificial Intelligence (AI)-Enabled Surgical Software

- Training and Education Software

- Workflow and Operating Room Management Software

- Cybersecurity and Compliance Software

- Others

By Application

- General Surgery

- Orthopedic Surgery

- Neurosurgery

- Urology Surgery

- Gynecological Surgery

- Cardiothoracic Surgery

- Gastrointestinal Surgery

- Ear, Nose, and Throat (ENT) Surgery

- Plastic and Reconstructive Surgery

- Oncology Surgery

- Pediatric Surgery

- Ophthalmic Surgery

- Others

By Deployment

- On-Premises Deployment

- Cloud-Based Deployment

- Hybrid Deployment

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 2.45 B |

| Forecast Revenue (2034) | USD 11.85 B |

| CAGR (2025-2034) | 19.1% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Software Type, (Surgical Planning and Simulation Software, Navigation and Guidance Software, Robotic Control Software, Imaging and Visualization Software, Data Analytics and Performance Monitoring Software, Artificial Intelligence (AI)-Enabled Surgical Software, Training and Education Software, Workflow and Operating Room Management Software, Cybersecurity and Compliance Software, Others), By Application, (General Surgery, Orthopedic Surgery, Neurosurgery, Urology Surgery, Gynecological Surgery, Cardiothoracic Surgery, Gastrointestinal Surgery, Ear, Nose, and Throat (ENT) Surgery, Plastic and Reconstructive Surgery, Oncology Surgery, Pediatric Surgery, Ophthalmic Surgery, Others), By Deployment, (On-Premises Deployment, Cloud-Based Deployment, Hybrid Deployment) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | INTUITIVE SURGICAL, INC., MEDTRONIC PLC, STRYKER CORPORATION, ZIMMER BIOMET HOLDINGS, INC., JOHNSON & JOHNSON MEDTECH, BRAINLAB AG, CMR SURGICAL, SMITH & NEPHEW PLC, ASENSUS SURGICAL (KARL STORZ), THINK SURGICAL, INC., THEATOR INC., CARESYNTAX, ACTIV SURGICAL, INC., PROPRIO INC., PROXIMIE LTD., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (General Surgery, Orthopedic Surgery, Neurosurgery, Urology, Gynecology, Cardiothoracic Surgery, Gastrointestinal Surgery, ENT Surgery, Oncology and Ophthalmic Surgery), By Deployment (On-Premises, Cloud-Based and Hybrid) Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Strategies, Emerging Trends and Forecast 2026-2034")

, By Application (General Surgery, Orthopedic Surgery, Neurosurgery, Urology, Gynecology, Cardiothoracic Surgery, Gastrointestinal Surgery, ENT Surgery, Oncology and Ophthalmic Surgery), By Deployment (On-Premises, Cloud-Based and Hybrid) Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Strategies, Emerging Trends and Forecast 2026-2034")

, By Application (General Surgery, Orthopedic Surgery, Neurosurgery, Urology, Gynecology, Cardiothoracic Surgery, Gastrointestinal Surgery, ENT Surgery, Oncology and Ophthalmic Surgery), By Deployment (On-Premises, Cloud-Based and Hybrid) Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Strategies, Emerging Trends and Forecast 2026-2034")

Frequently Asked Questions

How big is the Surgical Robotics Software Market?

The Global Surgical Robotics Software Market was valued at USD 2.06 Billion in 2024 and USD 2.45 Billion in 2025, and is projected to reach USD 11.85 Billion by 2034, growing at a CAGR of 19.1% from 2026 to 2034. Market growth is driven by the increasing adoption of robotic-assisted surgeries, rising demand for minimally invasive procedures, and advancements in AI-powered surgical technologies.

Who are the major players in the Surgical Robotics Software Market?

INTUITIVE SURGICAL, INC., MEDTRONIC PLC, STRYKER CORPORATION, ZIMMER BIOMET HOLDINGS, INC., JOHNSON & JOHNSON MEDTECH, BRAINLAB AG, CMR SURGICAL, SMITH & NEPHEW PLC, ASENSUS SURGICAL (KARL STORZ), THINK SURGICAL, INC., THEATOR INC., CARESYNTAX, ACTIV SURGICAL, INC., PROPRIO INC., PROXIMIE LTD., Others

Which segments covered the Surgical Robotics Software Market?

By Software Type, (Surgical Planning and Simulation Software, Navigation and Guidance Software, Robotic Control Software, Imaging and Visualization Software, Data Analytics and Performance Monitoring Software, Artificial Intelligence (AI)-Enabled Surgical Software, Training and Education Software, Workflow and Operating Room Management Software, Cybersecurity and Compliance Software, Others), By Application, (General Surgery, Orthopedic Surgery, Neurosurgery, Urology Surgery, Gynecological Surgery, Cardiothoracic Surgery, Gastrointestinal Surgery, Ear, Nose, and Throat (ENT) Surgery, Plastic and Reconstructive Surgery, Oncology Surgery, Pediatric Surgery, Ophthalmic Surgery, Others), By Deployment, (On-Premises Deployment, Cloud-Based Deployment, Hybrid Deployment)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Surgical Robotics Software Market

Published Date : 12 Jun 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date