- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Sustainable Aviation Fuel Market Size, Share | CAGR 25.8%

Global Sustainable Aviation Fuel Market Size, Share, Growth Analysis By Production Pathway (HEFA, Alcohol-to-Jet, Power-to-Liquid, Fischer-Tropsch), By Feedstock (Waste Oils, Agricultural Residues, Municipal Waste, CO2 & Green Hydrogen), By End-User (Commercial Aviation, Military Aviation, Business Aviation), By Blend Ratio, Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

| USD 7.43 Billion | USD 58.62 Billion | 25.8% | Europe, 37.6% |

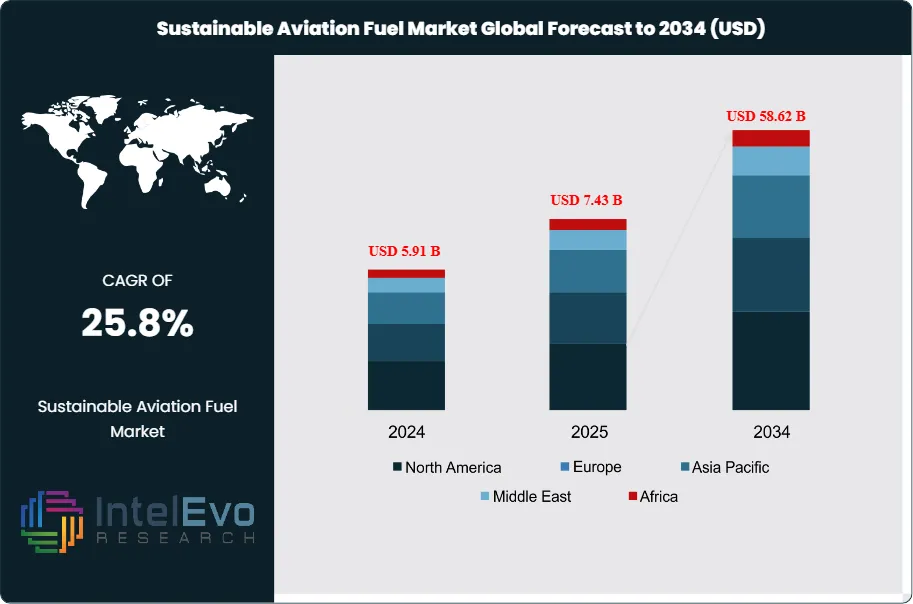

The Sustainable Aviation Fuel Market was valued at approximately USD 5.91 Billion in 2024 and reached USD 7.43 Billion in 2025. The market is projected to grow to USD 58.62 Billion by 2034, expanding at a CAGR of 25.8% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 51.19 Billion over the analysis period, establishing Sustainable Aviation Fuel as the single largest near-term decarbonization investment within the commercial aviation industry.

Get More Information about this report -

Request Free Sample ReportSustainable Aviation Fuel encompasses a broad class of aviation fuels produced from non-petroleum feedstocks, including agricultural residues, municipal solid waste, used cooking oil, woody biomass, and, increasingly, captured CO2 combined with green hydrogen via power-to-liquid synthesis. All commercially certified SAF pathways must demonstrate lifecycle greenhouse gas emissions reductions of at least 50% versus conventional Jet-A fuel under ASTM D7566 certification standards, and leading pathways including Hydroprocessed Esters and Fatty Acids (HEFA) achieve reductions of 60–85%. SAF is fully drop-in compatible with existing jet engines and airport fuel infrastructure when blended at up to 50% concentration as certified by ASTM, eliminating the need for engine modification or new distribution infrastructure that characterizes alternative propulsion pathways.

Market growth is driven by the convergence of mandatory blending mandates, airline corporate net-zero commitments, and a rapidly expanding producer ecosystem. The International Civil Aviation Organization's Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) entered its mandatory phase in 2027, compelling airlines on international routes to offset or reduce carbon emissions relative to a 2019–2020 baseline. The EU's ReFuelEU Aviation regulation, effective from January 2025, mandates a 2% SAF blending requirement at EU airports rising to 70% by 2050, creating the world's most prescriptive demand-side policy framework. The U.S. Inflation Reduction Act's Section 40B SAF blender tax credit, providing USD 1.25–USD 1.75 per gallon based on lifecycle carbon intensity, is the most significant single financial incentive in the global SAF supply build-out.

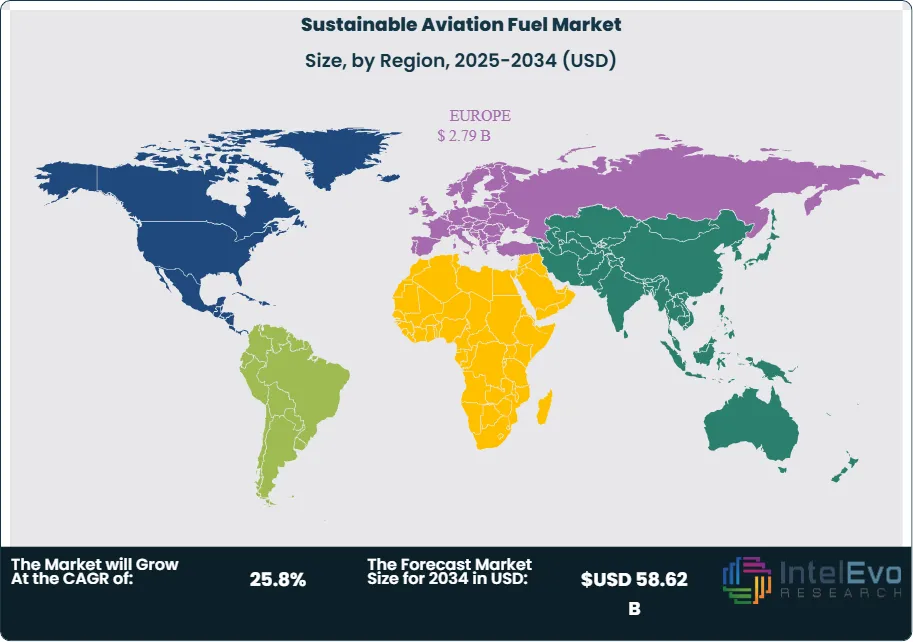

Europe leads global market revenue at 37.6% in 2025, approximately USD 2.79 Billion, driven by ReFuelEU mandate compliance requirements and strong airline sustainability purchasing commitments from Lufthansa Group, Air France-KLM, and International Airlines Group. North America holds a 31.4% share, supported by the IRA tax credit and California's Low Carbon Fuel Standard, which provides additional SAF credits for in-state production. Asia Pacific accounted for 22.3% of the global Sustainable Aviation Fuel market in 2025, with Japan's Green Growth Strategy targeting 10% SAF penetration in domestic aviation by 2030 and Singapore's Civil Aviation Authority mandating 1% SAF blending from 2026.

The Sustainable Aviation Fuel market is transitioning from a demonstration-scale, premium-priced specialty product into a volume commodity as production capacity scales and feedstock economics improve. Total global SAF production capacity reached approximately 1.5 billion liters in 2025, compared to global aviation fuel consumption of approximately 370 billion liters, placing SAF penetration below 0.5% of jet fuel supply. The supply gap between mandate-driven demand and production capacity is the defining commercial tension of the market through 2034, and it is attracting capital from energy majors, agricultural commodity processors, industrial gas companies, and technology developers at a pace that is reshaping the competitive landscape across all production pathways.

, By Feedstock (Waste Oils, Agricultural Residues, Municipal Waste, CO2 & Green Hydrogen), By End-User (Commercial Aviation, Military Aviation, Business Aviation), By Blend Ratio, Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global Sustainable Aviation Fuel market reached USD 7.43 Billion in 2025 and is forecast to reach USD 58.62 Billion by 2034, expanding at a CAGR of 25.8% over the 2026–2034 forecast period.

- Segment Dominance: By production pathway, Hydroprocessed Esters and Fatty Acids (HEFA) held the largest share at 71.4% of global SAF production volume in 2025, reflecting its commercial maturity, established feedstock supply chains, and ASTM certification across the broadest range of feedstocks.

- Segment Dominance: By end-user, commercial aviation accounted for 82.6% of global Sustainable Aviation Fuel demand in 2025, with passenger airlines representing the largest single buyer category, driven by CORSIA compliance obligations and corporate sustainability purchasing commitments.

- Driver: Binding regulatory mandates across the EU, UK, Japan, Singapore, and the United States are converting voluntary SAF purchasing into compliance-driven procurement, with the EU's ReFuelEU Aviation regulation alone projected to require approximately 700,000 tonnes of SAF annually at EU airports by 2026, creating a structurally guaranteed demand floor.

- Restraint: SAF production costs remain 3–5 times higher than conventional Jet-A fuel at approximately USD 1,500–USD 3,500 per tonne versus USD 600–USD 800 per tonne for petroleum jet fuel in 2025, limiting unsubsidized adoption to airlines with explicit sustainability mandates and constraining penetration in price-sensitive markets.

- Opportunity: Power-to-Liquid (PtL) SAF, produced by combining green hydrogen with captured CO2 via Fischer-Tropsch or methanol synthesis, represents the largest long-term production expansion pathway, with addressable capacity estimated at USD 18.7 Billion by 2034 as electrolysis costs decline and renewable electricity prices fall below USD 30 per MWh in high-irradiance regions.

- Trend: Vertical integration by energy majors into SAF production, with BP, Shell, TotalEnergies, and Neste each committing multi-billion-dollar capital expenditure to dedicated SAF refining capacity, is reshaping the supply landscape from specialist niche producers toward large-scale commodity production, with combined announced capacity additions exceeding 10 billion liters annually by 2030.

- Regional Analysis: Europe leads the global Sustainable Aviation Fuel market with a 37.6% share in 2025, representing approximately USD 2.79 Billion in revenue, driven by ReFuelEU Aviation mandate compliance and Lufthansa Group, Air France-KLM, and IAG SAF offtake commitments.

Competitive Landscape Overview

The global Sustainable Aviation Fuel market is moderately fragmented at the production level, with the top four producers, Neste, World Energy, LanzaTech, and TotalEnergies, collectively accounting for approximately 38.2% of global SAF production capacity in 2025. Competition is pathway-driven: HEFA producers compete primarily on feedstock cost and processing efficiency, while emerging Alcohol-to-Jet and Power-to-Liquid producers compete on technology differentiation and carbon intensity certification. The entry of oil majors including BP, Shell, and TotalEnergies with multi-billion-dollar capital commitments is rapidly consolidating the production tier, while the feedstock aggregation and logistics layer is attracting specialist commodity traders including Vitol and Trafigura. M&A activity has been intense since 2023, with refiners acquiring biofuel technology licenses, agricultural processors securing SAF production rights, and airlines signing multi-decade offtake agreements that provide the demand certainty needed for project financing.

Competitive Landscape Matrix

| Company | HQ Country | Market Position | Key Product / Platform | Geographic Strength | Recent Strategic Move (2024–2026) |

| Neste | Finland | Leader | Neste MY Sustainable Aviation Fuel (HEFA) | Europe / Asia Pacific | Expanded Singapore HEFA refinery to 1 billion liters SAF annual capacity; signed 10-year offtake with American Airlines for 300M liters (Jan 2025). |

| World Energy | USA | Leader | World Energy SAF (HEFA) | North America | Commissioned Paramount, California HEFA facility at 200M liters/year; secured USD 1.4B DOE loan guarantee for capacity expansion (Mar 2025). |

| LanzaTech | USA | Leader | LanzaJet Freedom Pines Fuels (AtJ) | North America / Europe | Freedom Pines Fuels Georgia facility reached commercial production of 10M gallons/year Alcohol-to-Jet SAF; signed offtake with United Airlines (Dec 2024). |

| TotalEnergies | France | Leader | TotalEnergies SAF (HEFA + PtL) | Europe / MEA | Announced EUR 500M investment in dedicated SAF production units at La Mede and Grandpuits refineries targeting 285,000 tonnes/year by 2030 (Apr 2025). |

| Neste / Shell JV (Air bp) | UK | Challenger | Air bp SAF supply platform | Europe / North America | Air bp extended SAF supply agreements to 20 airports across 12 countries, including first SAF supply to Istanbul Ataturk (Sep 2025). |

| Gevo | USA | Challenger | Net-Zero 1 (Alcohol-to-Jet) | North America | Net-Zero 1 South Dakota facility broke ground with 65M gallon annual capacity; backed by USD 1.6B DOE loan conditional commitment (Jun 2025). |

| Aemetis | USA | Challenger | Aemetis Carbon Zero SAF | North America | Completed feedstock diversification to 100% waste oils at Keyes California plant; delivered first SAF blend to Delta Air Lines (Feb 2026). |

| Repsol | Spain | Niche Player | Repsol Ecoplants SAF (HEFA) | Europe | Commissioned co-processing SAF production at Cartagena refinery; signed SAF supply agreement with Iberia for 2026–2031 (Jan 2026). |

| SkyNRG | Netherlands | Niche Player | SkyNRG SAF (HEFA) | Europe | Expanded DSL-01 Netherlands facility to 100,000 tonnes/year with KLM as anchor offtake partner; certified under ISCC PLUS (Oct 2025). |

By Production Pathway:

The Hydroprocessed Esters and Fatty Acids pathway commands the dominant share of the global Sustainable Aviation Fuel market at 71.4% of production volume in 2025, valued at approximately USD 5.30 Billion. HEFA is the only SAF pathway currently operating at commercial refinery scale, using waste oils, animal fats, and vegetable oils as feedstocks that are hydroprocessed in modified or dedicated refinery units to produce a drop-in aviation fuel blend stock. Neste's Singapore facility, expanded to 1 billion liters of SAF annual capacity, and World Energy's California plant are the two largest single-site HEFA installations globally. The HEFA pathway benefits from established ASTM D7566 Annex 2 certification, proven refinery technology from hydrotreatment operations, and an existing waste oil and agricultural lipid supply chain. HEFA SAF achieves lifecycle GHG reductions of 60–85% versus conventional Jet-A when derived from waste fats and used cooking oil, and 50–65% from non-food crop oils, meeting CORSIA and ReFuelEU eligibility thresholds. The pathway's primary constraint is feedstock competition: waste cooking oil and animal fats face simultaneous demand from the road transport biodiesel sector, and global supply of these feedstocks is estimated to be sufficient for only 30–40 billion liters of SAF annually, well below long-term aviation sector demand.

The Alcohol-to-Jet pathway represented 12.3% of the global Sustainable Aviation Fuel market in 2025, approximately USD 914 Million, and is the fastest-scaling alternative to HEFA with multiple commercial-scale facilities reaching production milestones in 2024–2025. AtJ processes ethanol or isobutanol, typically derived from cellulosic biomass, agricultural residues, or industrial waste gases, through dehydration, oligomerization, and hydrogenation steps to produce a certified jet fuel blend stock. LanzaTech's Freedom Pines Fuels facility in Georgia, using ethanol derived from captured industrial off-gases, and Gevo's Net-Zero 1 South Dakota project, using corn-derived isobutanol, represent the two most advanced commercial AtJ developments. AtJ feedstocks are more diverse and scalable than HEFA lipid feedstocks, providing a longer-term supply runway. The Power-to-Liquid pathway held a 6.8% share in 2025, representing the early-commercial stage of e-SAF production from green hydrogen and CO2. Fischer-Tropsch and other certified pathways accounted for the remaining 9.5%.

By Feedstock:

Waste oils and fats, encompassing used cooking oil, animal processing fats, and trap grease, held a 48.7% share of global SAF feedstock supply in 2025, valued at approximately USD 3.62 Billion. This feedstock category dominates because it is the primary input for the HEFA pathway, the market-leading production technology, and because waste-derived feedstocks carry the highest lifecycle GHG reduction credits under CORSIA and the EU's Renewable Energy Directive. Used cooking oil prices have been volatile, reaching USD 800–USD 1,100 per tonne in European markets in 2024–2025, driven by competing demand from road transport biodiesel and rising Asian import competition. Agricultural residues, including corn stover, wheat straw, and sugarcane bagasse, accounted for 19.4% of feedstock supply in 2025, primarily channeled into cellulosic ethanol production for AtJ pathways. Municipal solid waste represented 14.2% of the feedstock mix, processed through gasification and Fischer-Tropsch or AtJ routes. CO2 and green hydrogen for PtL pathways accounted for 8.1% of the feedstock value in 2025, with the balance from other certified biomass and feedstock categories.

By End-User:

Commercial aviation dominated Sustainable Aviation Fuel demand at 82.6% of global market revenue in 2025, approximately USD 6.14 Billion, reflecting the sector's exposure to CORSIA obligations and the concentration of airline sustainability purchasing power. Within commercial aviation, passenger airlines represent the largest buyer segment, with IATA member airlines having collectively signed SAF offtake agreements covering an estimated 8 billion liters of forward supply as of mid-2025. United Airlines, Delta Air Lines, Lufthansa Group, Air France-KLM, and British Airways are among the highest-volume SAF purchasers, with multi-year agreements providing revenue certainty that underpins SAF producer project financing. Air freight operators, including FedEx, UPS, and DHL Aviation, represent a growing commercial aviation sub-segment, with logistics operators facing supply chain decarbonization pressure from corporate shipper clients. Military aviation accounted for 10.8% of SAF demand in 2025, with the U.S. Department of Defense having committed to net-zero emissions by 2050 and initiating SAF procurement under the Defense Production Act provisions for domestic clean fuel supply. Business and general aviation represented the remaining 6.6%.

By Blend Ratio:

The below 10% blend ratio segment, reflecting the predominant operational SAF blending practice at most airports in 2025, accounted for 63.2% of global SAF volume consumed in 2025. At this blend level, SAF is fully interchangeable with conventional Jet-A without any aircraft or fueling system modification, and single-airport infrastructure investments for SAF delivery are minimized. The 10–30% blend segment held 27.4% of volume in 2025, primarily reflecting dedicated fleet agreements where airlines have negotiated SAF supply directly at hub airports with sufficient storage infrastructure. Above 30% blends accounted for 9.4% of volume, concentrated in military trials and advanced airline sustainability demonstration flights, including the first 100% SAF transatlantic demonstration flights completed by Virgin Atlantic and Airbus in 2023–2024 using research-grade certification exemptions.

Regional Analysis

Europe

Europe leads the global Sustainable Aviation Fuel market with a 37.6% share in 2025, representing approximately USD 2.79 Billion in revenue, driven by the world's most comprehensive and prescriptive SAF policy framework. The EU's ReFuelEU Aviation Regulation, effective from January 2025, mandates 2% SAF blending at all EU airports in 2025, rising through 6% in 2030, 20% in 2035, and 70% by 2050, creating a legally binding demand escalator that is the primary driver of European SAF investment. Critically, ReFuelEU reserves a specific sub-mandate for synthetic PtL-SAF, requiring 1.2% by 2030 and 35% by 2050, directing investment toward electrolysis-based pathways that address feedstock limitations of HEFA. Germany is Europe's largest single SAF market, reflecting Lufthansa Group's procurement leadership, with the airline group having committed to using 10% SAF by 2030 across its entire fleet. The Netherlands is the second-largest market, driven by KLM's long-standing SAF program operating since 2011 and Schiphol Airport's central position in European SAF supply logistics. The UK's SAF mandate, separate from the EU framework post-Brexit, requires 2% blending in 2025 rising to 10% by 2030 and 22% by 2040, with British Airways and Virgin Atlantic as the primary compliance buyers. France's SAF mandate, reinforced by national airline sustainability reporting requirements under the Loi Climat et Resilience, and Scandinavian markets with high environmental consciousness and renewable energy resources further strengthen European production investment.

North America

North America accounted for 31.4% of the global Sustainable Aviation Fuel market in 2025, approximately USD 2.33 Billion, with the United States generating approximately 91% of regional revenue. The IRA Section 40B SAF blender tax credit, providing USD 1.25 per gallon for SAF with a 50% lifecycle GHG reduction and an additional USD 0.01 per gallon for each percentage point of additional reduction above 50%, is the most financially impactful single SAF policy instrument globally. This credit, combined with California's Low Carbon Fuel Standard, which provides tradeable LCFS credits for SAF produced and used in California, creates a stacked incentive environment that has attracted major capital commitments. The DOE Loan Programs Office has conditionally committed over USD 4.5 Billion in loan guarantees to SAF production projects including Gevo, World Energy, and LanzaTech expansions. The FAA's Sustainable Aviation Fuel Grand Challenge, targeting 3 billion gallons of SAF production annually by 2030, provides interagency coordination across USDA, DOE, and FAA to accelerate feedstock development, technology scale-up, and infrastructure investment. United Airlines is the largest single airline SAF buyer in North America, with offtake agreements covering over 1 billion liters of annual forward supply. Canada's Clean Fuel Regulations and British Columbia's Low Carbon Fuel Standard create a secondary policy environment for SAF investment in western Canada.

Asia Pacific

Asia Pacific represented 22.3% of the global Sustainable Aviation Fuel market in 2025, approximately USD 1.66 Billion, with the region's policy frameworks and airline purchasing commitments accelerating sharply from 2024 onward. Japan is the most advanced Asia Pacific SAF market, with the Ministry of Economy, Trade and Industry targeting 10% SAF penetration in domestic aviation by 2030 under the Green Growth Strategy and committing JPY 300 Billion toward SAF production infrastructure. Japan Airlines and ANA Holdings are the leading Asian airline SAF buyers, with both carriers having signed multi-year purchase agreements with Neste's Singapore facility. Singapore's Civil Aviation Authority announced a 1% SAF blending mandate from 2026 and a 3–5% target by 2030, with Changi Airport serving as the regional SAF supply hub for Southeast Asian carriers. China's Civil Aviation Administration has initiated SAF certification trials and pilot blending programs, with Sinopec and China Eastern Airlines collaborating on domestic HEFA production using palm oil derivatives and waste cooking oil. India's Ministry of Civil Aviation has outlined a 1% SAF blending aspiration by 2025–2026 under its National Air Sports Policy, though near-term capacity investment remains limited. South Korea's SAF development is driven by SK Innovation's biofuel refining capabilities and Korean Air's sustainability commitments.

Latin America

Latin America held a 4.2% share of the global Sustainable Aviation Fuel market in 2025, approximately USD 312 Million, with Brazil representing the dominant regional market. Brazil's position as the world's largest sugarcane ethanol producer creates a structurally advantaged feedstock base for Alcohol-to-Jet SAF production, with sugarcane ethanol achieving lifecycle GHG reductions of 70–85% under CORSIA Sustainability Criteria. Raízen, the joint venture between Shell and Cosan, operates the first commercial-scale cellulosic ethanol facility in Brazil and is advancing SAF production from sugarcane bagasse residues, targeting 200 million liters of AtJ-SAF annually by 2028. EMBRAER has partnered with Brazilian biofuel producers to develop regional aviation SAF supply chains for its E-Jet fleet operators. Chile's copper mining sector aviation operations and Colombia's domestic airline sector are secondary SAF demand nodes, with Avianca having signed a small-scale SAF supply agreement in 2024. Regional feedstock competitiveness and the potential for low-cost green hydrogen from Chilean and Patagonian wind resources position Latin America as a significant long-term SAF export region.

Middle East & Africa

The Middle East and Africa region accounted for 4.5% of the global Sustainable Aviation Fuel market in 2025, approximately USD 334 Million, with activity concentrated in the UAE and South Africa. The UAE's position as a global aviation hub, with Dubai International and Abu Dhabi International among the world's busiest airports by passenger volume, creates substantial SAF demand from Emirates, Etihad, and flydubai. Emirates has committed to 10% SAF usage by 2030 and has signed supply agreements with bp and Air bp for European-sourced SAF on inbound international routes. The UAE government's net-zero 2050 strategy includes aviation decarbonization components, and Masdar is evaluating green hydrogen-based PtL-SAF production using Abu Dhabi's substantial solar energy resources. South Africa's potential as a SAF feedstock exporter, leveraging its agricultural residue base and emerging green hydrogen production from wind and solar resources, has attracted interest from European SAF producers seeking to diversify feedstock supply chains. Kenya's aviation sector, through the Kenya Airports Authority, has initiated SAF supply chain feasibility studies supported by the International Air Transport Association's SAF incentive framework for developing country carriers.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Production Pathway

- Hydroprocessed Esters and Fatty Acids (HEFA)

- Alcohol-to-Jet (AtJ)

- Power-to-Liquid (PtL / e-SAF)

- Fischer-Tropsch (FT-SPK)

- Others (DSHC, CHJ, Co-processing)

By Feedstock

- Waste Oils and Fats (Used Cooking Oil, Animal Fats)

- Agricultural Residues (Corn Stover, Wheat Straw, Sugarcane Bagasse)

- Municipal Solid Waste

- CO2 and Green Hydrogen (Power-to-Liquid)

- Others (Energy Crops, Woody Biomass)

By End-User

- Commercial Aviation

- Military Aviation

- Business and General Aviation

By Blend Ratio

- Below 10%

- 10–30%

- Above 30%

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 7.43 B |

| Forecast Revenue (2034) | USD 58.62 B |

| CAGR (2025-2034) | 25.8% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Production Pathway, (Hydroprocessed Esters and Fatty Acids (HEFA), Alcohol-to-Jet (AtJ), Power-to-Liquid (PtL / e-SAF), Fischer-Tropsch (FT-SPK), Others (DSHC, CHJ, Co-processing)), By Feedstock, (Waste Oils and Fats (Used Cooking Oil, Animal Fats), Agricultural Residues (Corn Stover, Wheat Straw, Sugarcane Bagasse), Municipal Solid Waste, CO2 and Green Hydrogen (Power-to-Liquid), Others (Energy Crops, Woody Biomass)), By End-User, (Commercial Aviation, Military Aviation, Business and General Aviation), By Blend Ratio, (Below 10%, 10–30%, Above 30%) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | NESTE, WORLD ENERGY, LANZATECH / LANZAJET, TOTALENERGIES, BP / AIR BP, SHELL AVIATION, GEVO, AEMETIS, SKYNYG, REPSOL, FULCRUM BIOENERGY, RED ROCK BIOFUELS, ENI (VERSALIS), SINOPEC (CHINA PETROLEUM), RAIZEN (SHELL / COSAN JV), VELOCYS, TWELVE BENEFIT CORPORATION, ARCADIA E-FUELS, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Feedstock (Waste Oils, Agricultural Residues, Municipal Waste, CO2 & Green Hydrogen), By End-User (Commercial Aviation, Military Aviation, Business Aviation), By Blend Ratio, Industry Trends & Forecast 2026-2034")

, By Feedstock (Waste Oils, Agricultural Residues, Municipal Waste, CO2 & Green Hydrogen), By End-User (Commercial Aviation, Military Aviation, Business Aviation), By Blend Ratio, Industry Trends & Forecast 2026-2034")

, By Feedstock (Waste Oils, Agricultural Residues, Municipal Waste, CO2 & Green Hydrogen), By End-User (Commercial Aviation, Military Aviation, Business Aviation), By Blend Ratio, Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Sustainable Aviation Fuel Market?

The Global Sustainable Aviation Fuel Market was valued at USD 5.91 Billion in 2024 and is projected to reach USD 58.62 Billion by 2034, growing at a CAGR of 25.8% from 2026 to 2034, driven by rising demand for low-carbon aviation fuels, increasing airline decarbonization initiatives, supportive government regulations, advancements in biofuel production technologies, and expanding investments in sustainable aviation infrastructure worldwide.

Who are the major players in the Sustainable Aviation Fuel Market?

NESTE, WORLD ENERGY, LANZATECH / LANZAJET, TOTALENERGIES, BP / AIR BP, SHELL AVIATION, GEVO, AEMETIS, SKYNYG, REPSOL, FULCRUM BIOENERGY, RED ROCK BIOFUELS, ENI (VERSALIS), SINOPEC (CHINA PETROLEUM), RAIZEN (SHELL / COSAN JV), VELOCYS, TWELVE BENEFIT CORPORATION, ARCADIA E-FUELS, Others

Which segments covered the Sustainable Aviation Fuel Market?

By Production Pathway, (Hydroprocessed Esters and Fatty Acids (HEFA), Alcohol-to-Jet (AtJ), Power-to-Liquid (PtL / e-SAF), Fischer-Tropsch (FT-SPK), Others (DSHC, CHJ, Co-processing)), By Feedstock, (Waste Oils and Fats (Used Cooking Oil, Animal Fats), Agricultural Residues (Corn Stover, Wheat Straw, Sugarcane Bagasse), Municipal Solid Waste, CO2 and Green Hydrogen (Power-to-Liquid), Others (Energy Crops, Woody Biomass)), By End-User, (Commercial Aviation, Military Aviation, Business and General Aviation), By Blend Ratio, (Below 10%, 10–30%, Above 30%)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Sustainable Aviation Fuel Market

Published Date : 23 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date