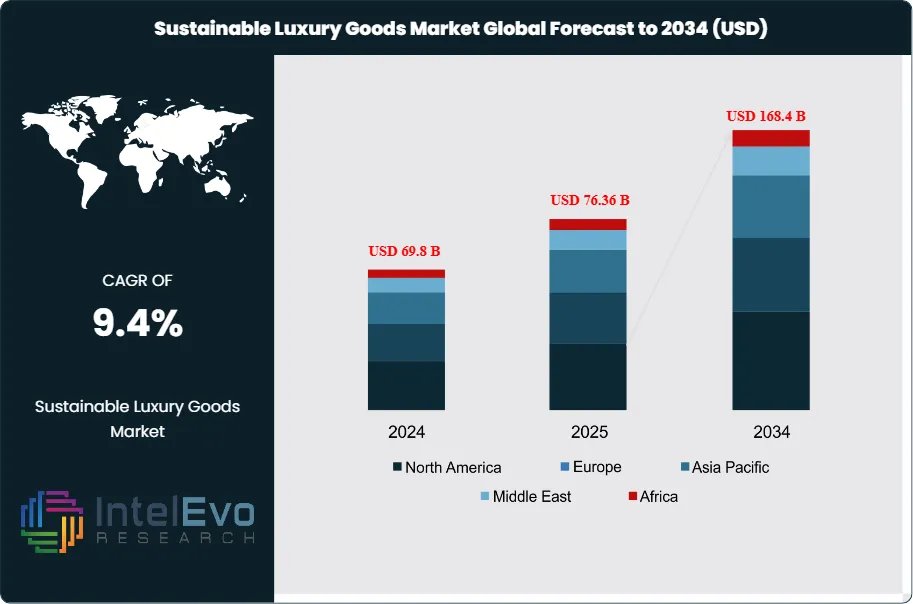

Sustainable Luxury Goods Market to Reach USD 168.4 Bn by 2034

Global Sustainable Luxury Goods Market Size, Share, Analysis Report By Product Type (Fashion, Beauty and Personal Care, Jewelry, Home Décor, Watches), Material (Organic Materials, Sustainable Leather, Vegan Materials), Distribution Channel (Online Retail, Offline Retail), End User (Men, Women, Children), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034

The Global Sustainable Luxury Goods Market size is projected to be worth around USD 168.4 billion by 2034, up from USD 69.8 billion in 2024, growing at a CAGR of 9.4% during the forecast period from 2025 to 2034. This growth reflects the rising consumer demand for eco-friendly, ethically sourced, and premium-quality products that combine luxury with sustainability. Increasing awareness of environmental impact, coupled with digital engagement and evolving fashion trends, is reshaping the luxury industry. Leading brands are investing in circular fashion, sustainable packaging, and carbon-neutral initiatives, making sustainability the new standard in global luxury markets.

The global sustainable luxury goods market encompasses high-end products made with environmentally friendly practices and materials, catering to eco-conscious consumers. This market includes fashion, accessories, cosmetics, and home decor items that prioritize sustainability in their production processes. Currently, it is driven by an increasing consumer awareness of environmental issues, leading brands to adopt sustainable practices to meet this demand. Major luxury brands are now focusing on ethical sourcing, responsible manufacturing, and transparency in their supply chains, further influencing market dynamics. As a result, the market has gained traction, with an increasing number of consumers prioritizing sustainability over brand prestige

The growth of the sustainable luxury goods market is fueled by several key drivers. A significant factor is the rising awareness of climate change and environmental sustainability, prompting consumers to seek out eco-friendly products. Additionally, millennials and Generation Z are leading this shift, as they are more likely to invest in brands that align with their values regarding sustainability. The growing availability of sustainable materials, such as organic cotton, recycled fabrics, and eco-friendly packaging, also contributes to market growth. Furthermore, brands that emphasize storytelling around their sustainability efforts create emotional connections with consumers, fostering loyalty and driving sales

Regionally, Europe currently dominates the sustainable luxury goods market, accounting for a substantial share due to a strong focus on sustainability among European consumers and a wealth of luxury brands committed to eco-friendly practices. The region's strict environmental regulations also play a significant role in promoting sustainable initiatives. However, the Asia-Pacific region is emerging as the fastest-growing market, driven by rising disposable incomes, changing consumer preferences, and increasing awareness of sustainability. Countries like China and Japan are witnessing a surge in demand for luxury goods that reflect sustainable practices, marking a shift in purchasing behavior

The COVID-19 pandemic has significantly impacted the sustainable luxury goods market. Initially, luxury goods experienced a downturn due to lockdowns and reduced consumer spending. However, the pandemic has led to an increased focus on sustainability and ethical consumption. Consumers have become more conscious of their purchasing decisions, preferring brands that prioritize social responsibility. This shift is expected to create lasting changes in the market, as luxury brands adapt to evolving consumer preferences by enhancing their sustainability initiatives and communicating their efforts more effectively.

Key Takeaways:

Market Growth: The global sustainable luxury goods market is projected to reach USD 420 billion by 2034, growing at a robust CAGR of 8.5%, reflecting increasing consumer preference for eco-friendly products and brands that prioritize sustainability.

Fashion Segment Dominance: The fashion segment is the largest within the sustainable luxury goods market, driven by high consumer demand for eco-friendly apparel and accessories. Luxury brands are increasingly incorporating sustainable materials, leading to significant market share and growth.

Beauty and Personal Care Focus: The beauty and personal care segment is rapidly growing, fueled by consumer interest in natural and ethically sourced products. Brands are launching sustainable cosmetics and skincare lines, emphasizing organic ingredients and eco-friendly packaging.

Driver: Rising awareness of environmental issues and consumer preference for sustainable products are driving market growth. Millennials and Generation Z are leading this trend, demanding transparency and ethical practices from luxury brands.

Restraint: The high cost of sustainable materials and production processes can limit the accessibility of luxury goods. Additionally, some consumers remain hesitant to pay a premium for sustainable products, impacting market adoption.

Opportunity: The increasing demand for sustainable luxury goods in emerging markets, particularly in Asia-Pacific, presents significant growth opportunities. Brands can tap into these markets by promoting eco-friendly initiatives and expanding their product offerings.

Trend: There is a growing trend of luxury brands investing in sustainability initiatives, from eco-friendly materials to transparent supply chains, aligning their business models with consumer values.

Regional Analysis: Europe currently holds the largest market share in sustainable luxury goods, driven by strong consumer awareness and regulatory support for sustainability. Meanwhile, the Asia-Pacific region is emerging as the fastest-growing market, fueled by rising disposable incomes and changing consumer preferences.

Product Type Analysis:

The product type segment is pivotal in the sustainable luxury goods market, encompassing various categories such as fashion, beauty and personal care, jewelry, home décor, and watches. Among these, sustainable fashion is gaining significant traction as consumers increasingly prioritize ethically sourced apparel, footwear, and accessories. Brands are responding by incorporating eco-friendly materials, such as organic cotton and recycled fibers, into their collections. The beauty and personal care sector is also evolving, with products utilizing natural ingredients and sustainable packaging. This shift reflects a broader trend toward responsible consumption and a growing awareness of environmental and ethical issues in the luxury sector.

Material Type Analysis:

The material type segment highlights the importance of eco-friendly resources in the production of sustainable luxury goods. Key materials include organic materials, such as organic cotton and bamboo, which are favored for their minimal environmental impact. Additionally, sustainable leather alternatives, including vegan materials made from plants or recycled products, are gaining popularity as consumers seek cruelty-free options. Brands are increasingly adopting these materials to enhance their sustainability credentials, catering to environmentally conscious consumers who are willing to invest in high-quality, ethically produced goods. This trend is not only beneficial for the planet but also helps brands differentiate themselves in a competitive market.

Distribution Channel Analysis:

Distribution channels play a crucial role in the accessibility and visibility of sustainable luxury goods. The market is characterized by a dual approach, with online retail and offline retail coexisting to meet consumer preferences. Online platforms are becoming increasingly popular due to their convenience and the ability to showcase a wider range of sustainable products. On the other hand, offline retail, including specialty stores and department stores, provides consumers with a tactile experience, allowing them to see and feel the quality of products before purchasing. This hybrid distribution strategy helps brands reach a broader audience while educating consumers about sustainability.

End Use Insights:

The end-user segment is diverse, comprising men, women, and children, reflecting the broad appeal of sustainable luxury goods across demographics. Women are traditionally the largest consumers of luxury fashion and beauty products, driving demand for sustainable options in these categories. However, there is a growing recognition of the importance of sustainable choices among men, particularly in fashion and grooming. Additionally, the market for children’s sustainable luxury goods is expanding, as parents increasingly prioritize eco-friendly and safe products for their children. This diversification of the end-user segment indicates a widespread shift toward sustainability in luxury consumption.

Region Analysis:

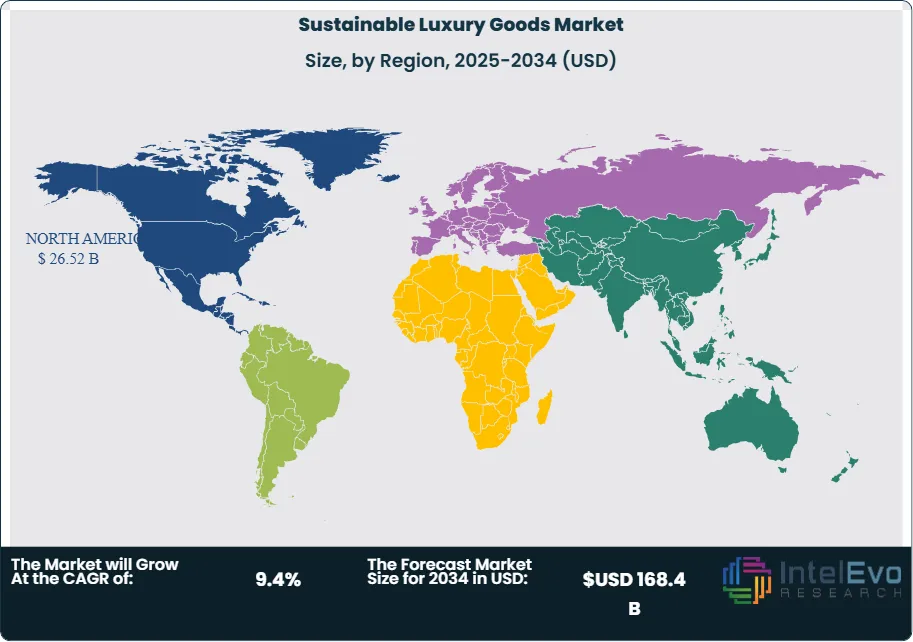

North America Dominates the Sustainable Luxury Goods Market with 38% Share: North America holds the largest market share in the sustainable luxury goods sector, accounting for approximately 38%. This dominance can be attributed to the increasing consumer awareness surrounding environmental issues and the growing demand for ethically produced products. Leading luxury brands are making significant investments in sustainable practices, with initiatives focusing on transparency in sourcing and production. Additionally, high disposable incomes among consumers in this region enable them to invest in premium sustainable products. The rise of eco-conscious millennials and Gen Z consumers further accelerates this trend, pushing brands to innovate and enhance their sustainability efforts.

The Asia-Pacific region is witnessing the fastest growth in the sustainable luxury goods market, projected to expand at a CAGR of over 10% through 2034. This rapid growth is driven by the increasing purchasing power of the middle class and a shift in consumer preferences towards sustainability, particularly in countries like China and India. Furthermore, heightened awareness of environmental issues and a desire for high-quality, ethically sourced products are shaping purchasing decisions. The rise of e-commerce platforms is also facilitating access to sustainable luxury goods, allowing brands to tap into a broader audience. As luxury consumption grows, the demand for sustainable options in this region will likely continue to increase.

By Product Type (Apparel & Footwear, Accessories (Handbags, Watches, Jewelry), Beauty & Personal Care, Home Décor & Lifestyle Goods, Others), By Material Type (Organic Cotton & Natural Fibers, Recycled & Upcycled Materials, Eco-Leather & Vegan Alternatives, Sustainable Metals & Precious Stones, Others), By Distribution Channel (Online/E-commerce Platforms, Specialty Stores, Department Stores, Luxury Brand Outlets, Others), By Consumer Demographics (Millennials, Gen Z, Baby Boomers, Others), By Price Range (Premium, Ultra-Premium, Affordable Luxury)

Research Methodology

Primary Research- 100 Interviews of Stakeholders

Secondary Research

Desk Research

Regional scope

North America (United States, Canada, Mexico)

Latin America (Brazil, Argentina, Columbia)

East Asia And Pacific (China, Japan, South Korea, Australia, Cambodia, Fiji, Indonesia)

Sea And South Asia (India, Singapore, Thailand, Taiwan, Malaysia)

Eastern Europe (Poland, Russia, Czech Republic, Romania)

Western Europe (Germany, U.K., France, Spain, Itlay)

Middle East & Africa (GCC Countries, Egypt, Nigeria, South Africa, Israel)

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements.

Pricing and Purchase Options

Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF).

TABLE OF CONTENTS

1. EXECUTIVE SUMMARY

1.1. MARKET SNAPSHOT

1.2. KEY FINDINGS & INSIGHTS

1.3. ANALYST RECOMMENDATIONS

1.4. FUTURE OUTLOOK

2. RESEARCH METHODOLOGY

2.1. MARKET DEFINITION & SCOPE

2.2. RESEARCH OBJECTIVES: PRIMARY & SECONDARY DATA SOURCES

2.3. DATA COLLECTION SOURCES

2.3.1. COVERAGE OF 100+ PRIMARY RESEARCH/CONSULTATION CALLS WITH INDUSTRY STAKEHOLDERS

FIGURE 17 NORTH AMERICA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 18 NORTH AMERICA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 19 MARKET SHARE BY COUNTRY

FIGURE 20 LATIN AMERICA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 21 LATIN AMERICA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 22 MARKET SHARE BY COUNTRY

FIGURE 23 EASTERN EUROPE SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 24 EASTERN EUROPE SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 25 MARKET SHARE BY COUNTRY

FIGURE 26 WESTERN EUROPE SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 27 WESTERN EUROPE SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 28 MARKET SHARE BY COUNTRY

FIGURE 29 EAST ASIA AND PACIFIC SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 30 EAST ASIA AND PACIFIC SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 31 MARKET SHARE BY COUNTRY

FIGURE 32 SEA AND SOUTH ASIA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 33 SEA AND SOUTH ASIA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 34 MARKET SHARE BY COUNTRY

FIGURE 35 MIDDLE EAST AND AFRICA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 36 MIDDLE EAST AND AFRICA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 37 NORTH AMERICA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 38 U.S. SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 39 U.S. SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 40 CANADA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 41 CANADA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 42 LATIN AMERICA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 43 MEXICO SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 44 MEXICO SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 45 BRAZIL SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 46 BRAZIL SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 47 ARGENTINA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 48 ARGENTINA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 49 COLUMBIA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 50 COLUMBIA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 51 REST OF LATIN AMERICA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 52 REST OF LATIN AMERICA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 53 EASTERN EUROPE SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 54 POLAND SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 55 POLAND SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 56 RUSSIA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 57 RUSSIA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 58 CZECH REPUBLIC SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 59 CZECH REPUBLIC SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 60 ROMANIA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 61 ROMANIA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 62 REST OF EASTERN EUROPE SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 63 REST OF EASTERN EUROPE SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 64 WESTERN EUROPE SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 65 GERMANY SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 66 GERMANY SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 67 FRANCE SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 68 FRANCE SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 69 UK SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 70 UK SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 71 SPAIN SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 72 SPAIN SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 73 ITALY SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 74 ITALY SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 75 REST OF WESTERN EUROPE SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 76 REST OF WESTERN EUROPE SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 77 EAST ASIA AND PACIFIC SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 78 CHINA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 79 CHINA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 80 JAPAN SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 81 JAPAN SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 82 AUSTRALIA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 83 AUSTRALIA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 84 CAMBODIA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 85 CAMBODIA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 86 FIJI SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 87 FIJI SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 88 INDONESIA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 89 INDONESIA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 90 SOUTH KOREA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 91 SOUTH KOREA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 92 REST OF EAST ASIA AND PACIFIC SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 93 REST OF EAST ASIA AND PACIFIC SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 94 SEA AND SOUTH ASIA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 95 BANGLADESH SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 96 BANGLADESH SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 97 NEW ZEALAND SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 98 NEW ZEALAND SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 99 INDIA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 100 INDIA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 101 SINGAPORE SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 102 SINGAPORE SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 103 THAILAND SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 104 THAILAND SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 105 TAIWAN SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 106 TAIWAN SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 107 MALAYSIA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 108 MALAYSIA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 109 REST OF SEA AND SOUTH ASIA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 110 REST OF SEA AND SOUTH ASIA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 111 MIDDLE EAST AND AFRICA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 112 GCC COUNTRIES SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 113 GCC COUNTRIES SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 114 SAUDI ARABIA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 115 SAUDI ARABIA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 116 UAE SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 117 UAE SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 118 BAHRAIN SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 119 BAHRAIN SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 120 KUWAIT SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 121 KUWAIT SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 122 OMAN SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 123 OMAN SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 124 QATAR SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 125 QATAR SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 126 EGYPT SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 127 EGYPT SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 128 NIGERIA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 129 NIGERIA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 130 SOUTH AFRICA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 131 SOUTH AFRICA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 132 ISRAEL SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 133 ISRAEL SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 134 REST OF MEA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 135 REST OF MEA SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 136 U. S. MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 137 U. S. MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 138 CANADA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 139 CANADA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 140 MEXICO MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 141 MEXICO MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 142 CHINA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 143 CHINA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 144 JAPAN MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 145 JAPAN MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 146 INDIA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 147 INDIA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 148 SOUTH KOREA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 149 SOUTH KOREA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 150 SAUDI ARABIA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 151 SAUDI ARABIA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 152 UAE MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 153 UAE MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 154 EGYPT MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 155 EGYPT MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 156 NIGERIA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 157 NIGERIA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 158 SOUTH AFRICA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 159 SOUTH AFRICA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 160 GERMANY MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 161 GERMANY MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 162 FRANCE MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 163 FRANCE MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 164 UK MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 165 UK MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 166 SPAIN MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 167 SPAIN MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 168 ITALY MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 169 ITALY MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 170 BRAZIL MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 171 BRAZIL MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 172 ARGENTINA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 173 ARGENTINA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 174 COLUMBIA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 175 COLUMBIA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 176 GLOBAL SUSTAINABLE LUXURY GOODS CURRENT AND FUTURE MARKET KEY COUNTRY LEVEL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 177 FINANCIAL OVERVIEW:

Key Players Analysis:

LVMH Moët Hennessy Louis Vuitton: LVMH is a global leader in luxury goods, based in Paris, France. The company produces high-end fashion, leather goods, perfumes, cosmetics, and wines. LVMH focuses on sustainability by investing in eco-friendly production methods and materials, aiming to reduce its carbon footprint across all its brands while maintaining craftsmanship and quality.

Kering: Kering, headquartered in Paris, France, owns renowned brands such as Gucci, Saint Laurent, and Bottega Veneta. The company emphasizes sustainable luxury by integrating environmental responsibility into its business model. Kering's “Environmental Profit and Loss” account tracks its ecological impact, driving efforts to promote circular fashion and ethical sourcing.

Richemont: Swiss-based Richemont owns prestigious brands like Cartier and Montblanc. The company focuses on luxury jewelry, watches, and writing instruments. Richemont's sustainability initiatives include using responsible materials and promoting artisanal craftsmanship. The group is committed to ethical sourcing and environmental sustainability, enhancing brand value while aligning with consumer expectations for responsible luxury.

Hermès: Hermès, based in France, is known for its handcrafted luxury products, including leather goods, silk scarves, and watches. The company emphasizes sustainability through its commitment to craftsmanship, sourcing quality materials responsibly, and minimizing waste. Hermès adopts a slow-fashion approach, valuing timeless designs over fast fashion trends.

Burberry: Burberry, a British luxury fashion house, focuses on outerwear, accessories, and fragrances. The company is committed to sustainability by aiming for carbon neutrality across its operations by 2022. Burberry uses innovative materials, such as recycled fabrics, and supports circular fashion initiatives to reduce environmental impact while enhancing its brand image.

Stella McCartney: Stella McCartney is a pioneering designer in sustainable luxury fashion. Based in London, the brand focuses on vegan and eco-friendly materials while avoiding leather and fur. McCartney advocates for ethical fashion practices and has partnered with organizations to promote sustainability in the fashion industry, emphasizing transparency and environmental responsibility.

Prada: The Italian luxury brand Prada emphasizes sustainability through its Re-Nylon collection, made from recycled plastics. Headquartered in Milan, Prada is committed to reducing waste and implementing eco-friendly practices across its supply chain. The brand's strategy includes collaborations with organizations focused on sustainability and environmental awareness.

Chanel: Chanel, a French luxury fashion house, is renowned for its timeless style and high-quality products, including couture, fragrances, and accessories. The company focuses on sustainability by committing to responsible sourcing and eco-friendly production methods. Chanel aims to integrate sustainable practices into its operations while maintaining its luxurious brand identity.

Gucci: Gucci, part of Kering Group, is a leading luxury brand known for its fashion and leather goods. The brand has launched initiatives like Gucci Equilibrium to promote sustainability and ethical practices. Gucci focuses on using sustainable materials and supports various environmental and social projects to enhance its brand reputation while addressing consumer demands for responsible luxury.

Tiffany & Co.: Tiffany & Co., an American luxury jewelry retailer, emphasizes sustainability through ethical sourcing of diamonds and precious metals. The company is committed to transparency and environmental stewardship, including responsible mining practices. Tiffany aims to create a positive impact by supporting local communities and promoting sustainable luxury practices within the jewelry industry.

Market Key Players

LVMH Moët Hennessy Louis Vuitton

Kering

Richemont

Hermès

Burberry

Stella McCartney

Prada

Chanel

Gucci

Tiffany & Co.

Valentino

Fendi

Coach

Moncler

Diesel

Nike

Adidas

Eileen Fisher

Patagonia

Ralph Lauren

Driver:

Growing Consumer Demand for Sustainable Products

The increasing awareness of environmental issues and ethical consumerism is driving the demand for sustainable luxury goods. Consumers are increasingly prioritizing sustainability, leading to a shift in purchasing behavior towards brands that demonstrate social responsibility and environmental stewardship. Luxury brands are responding by enhancing transparency in their supply chains and implementing sustainable practices in sourcing and production. This trend is especially prominent among millennials and Generation Z, who are willing to pay a premium for products that align with their values. As sustainability becomes a key consideration in luxury purchasing, the market for sustainable goods is expected to expand significantly.

Corporate Social Responsibility Initiatives

Luxury brands are increasingly adopting Corporate Social Responsibility (CSR) strategies to enhance their reputation and appeal to ethically-minded consumers. These initiatives often focus on sustainability in production, waste reduction, and fair labor practices. By investing in sustainable practices, brands not only contribute to environmental protection but also strengthen their brand identity and customer loyalty. Many companies are establishing partnerships with non-profits and engaging in community-based projects that promote sustainability, which helps build a positive brand image. As these CSR initiatives gain traction, they are expected to play a crucial role in driving growth in the sustainable luxury goods market.

Technological Advancements and Innovation

Technological advancements are facilitating the development of sustainable luxury goods by enabling brands to adopt more efficient and eco-friendly production methods. Innovations such as sustainable materials, circular production processes, and waste reduction technologies are helping companies reduce their environmental footprint. Additionally, technology is improving supply chain transparency, allowing consumers to trace the origins of products and understand their sustainability credentials. As brands leverage these advancements to create more sustainable offerings, the market for sustainable luxury goods is likely to grow, driven by increased consumer confidence in the authenticity and quality of these products.

Restrain:

High Production Costs

One significant restraint in the sustainable luxury goods market is the high cost associated with producing environmentally friendly products. Sustainable materials, ethical labor practices, and eco-friendly production methods often require more substantial investment compared to conventional practices. This can lead to higher retail prices, which may limit market accessibility for price-sensitive consumers. While affluent consumers are willing to pay a premium for sustainable luxury goods, brands still face challenges in maintaining competitive pricing while ensuring quality and sustainability. As a result, some companies may struggle to achieve profitability, which can hinder market growth.

Limited Consumer Awareness

Despite growing interest in sustainability, there remains a general lack of awareness among many consumers regarding sustainable luxury goods. This limited understanding can affect purchasing decisions, as consumers may not recognize the value or benefits of investing in sustainable products. Furthermore, misinformation regarding sustainability claims can lead to skepticism about the authenticity of brands' practices. To overcome this challenge, luxury brands must focus on educating consumers about the importance of sustainability and the specific benefits of their products. Without effective communication strategies, the market may face barriers to widespread adoption and growth.

Opportunities:

Expansion into Emerging Markets

The sustainable luxury goods market presents significant opportunities for growth in emerging markets, particularly in regions like Asia-Pacific and Latin America. As the middle class expands and purchasing power increases in these regions, consumers are becoming more inclined to invest in premium, sustainable products. Luxury brands can capitalize on this trend by tailoring their offerings to meet the specific cultural and economic needs of these markets. Establishing a strong presence in these areas can not only enhance brand visibility but also contribute to overall market growth as consumers seek high-quality, ethically produced luxury goods.

Increased Collaboration and Partnerships

Another opportunity lies in the potential for increased collaboration between luxury brands and sustainability-focused organizations, including non-profits and technology firms. By forming strategic partnerships, luxury brands can leverage expertise in sustainable practices, access innovative technologies, and enhance their product offerings. Collaborations can also help brands communicate their sustainability efforts more effectively, thereby building consumer trust and loyalty. As the industry moves toward a more sustainable future, these partnerships can play a crucial role in driving innovation, expanding market reach, and ultimately growing the sustainable luxury goods market.

Trends:

Increasing Investment in UAM Technologies

One notable trend in the UAM market is the surge in investment from both public and private sectors. Venture capital firms, aerospace manufacturers, and tech companies are allocating significant resources toward developing eVTOL aircraft and supporting infrastructure. This influx of capital is not only fostering innovation but also accelerating the pace of research and development, enabling companies to bring their products to market more quickly. As investors recognize the potential for high returns in this emerging industry, the competitive landscape is evolving, leading to collaborations and partnerships aimed at enhancing technological capabilities and operational efficiencies.

Recent Development:

In September 2024: Gucci and Ferragamo announced a strategic partnership to enhance their sustainability initiatives. This collaboration aims to integrate more eco-friendly practices into their supply chains, reflecting the growing consumer demand for ethical fashion. The companies plan to share resources and best practices in sustainable materials and production methods, demonstrating a collective effort to lead the industry towards greater environmental responsibility.

In July 2024: Kering announced the development of a new product line focused on circular fashion, utilizing recycled materials and sustainable production techniques. This initiative is part of the company's broader strategy to promote sustainability and respond to consumer trends favoring eco-conscious brands. Kering aims to redefine luxury by emphasizing quality, longevity, and ethical sourcing.

Frequently Asked Questions

How big is the Sustainable Luxury Goods Market?

The global sustainable luxury goods market is set to hit USD 168.4 Bn by 2034, driven by eco-conscious consumers, ethical fashion, and circular economy trends.

Who are the major players in the Sustainable Luxury Goods Market?

Which segments covered the Sustainable Luxury Goods Market?

By Product Type (Apparel & Footwear, Accessories (Handbags, Watches, Jewelry), Beauty & Personal Care, Home Décor & Lifestyle Goods, Others), By Material Type (Organic Cotton & Natural Fibers, Recycled & Upcycled Materials, Eco-Leather & Vegan Alternatives, Sustainable Metals & Precious Stones, Others), By Distribution Channel (Online/E-commerce Platforms, Specialty Stores, Department Stores, Luxury Brand Outlets, Others), By Consumer Demographics (Millennials, Gen Z, Baby Boomers, Others), By Price Range (Premium, Ultra-Premium, Affordable Luxury)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

, Material (Organic Materials, Sustainable Leather, Vegan Materials), Distribution Channel (Online Retail, Offline Retail), End User (Men, Women, Children), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

, Material (Organic Materials, Sustainable Leather, Vegan Materials), Distribution Channel (Online Retail, Offline Retail), End User (Men, Women, Children), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

, Material (Organic Materials, Sustainable Leather, Vegan Materials), Distribution Channel (Online Retail, Offline Retail), End User (Men, Women, Children), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

, Material (Organic Materials, Sustainable Leather, Vegan Materials), Distribution Channel (Online Retail, Offline Retail), End User (Men, Women, Children), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")