- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Tactical Communication System Market Size, Share | CAGR of 6.6%

Global Tactical Communication System Market Size, Share, Analysis By Platform (Land, Airborne, Naval, Space), By Component (Hardware, Software, Services), By Comm Type (Voice, Data, Video), By End-User (Military, Homeland Security, Law Enforcement, Emergency) Region, Key Players – Dynamics, C4ISR Network Modernization & Secure Software-Defined Radio Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

| USD 22.75 Billion | USD 40.38 Billion | 6.6% | North America, 39.5% |

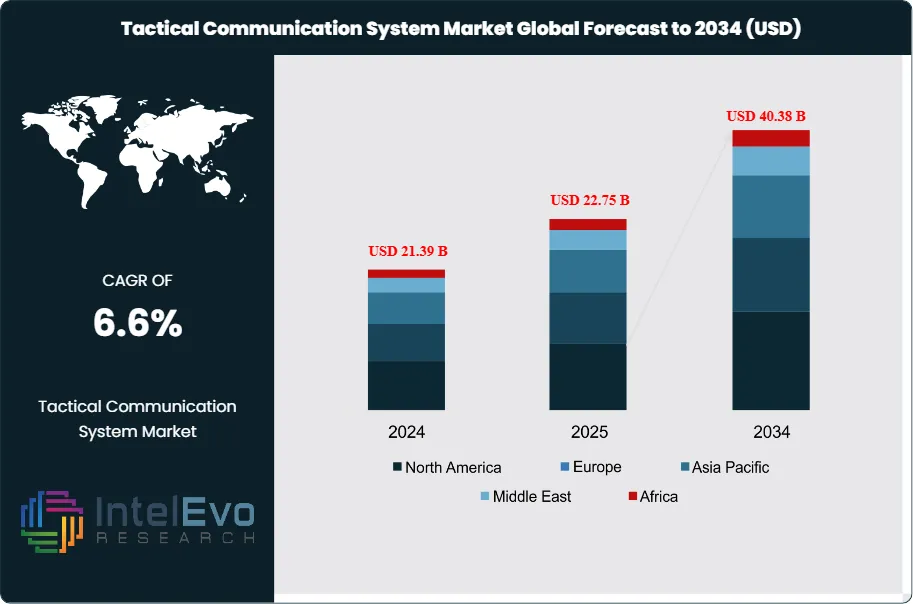

The Tactical Communication System Market was valued at approximately USD 21.39 billion in 2024 and reached USD 22.75 billion in 2025. The market is projected to grow to USD 40.38 billion by 2034, expanding at a CAGR of 6.6% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 17.63 billion over the analysis period, reflecting the rapid migration from platform-centric, voice-dominated architectures to data-driven, software-defined networks that connect dismounted soldiers, armored vehicles, aerial platforms, and space-based relay nodes into unified multi-domain operational grids.

Get More Information about this report -

Request Free Sample ReportThree forces are shaping market spending trajectories simultaneously. Defense budget expansion is the most direct driver: NATO member states committed at the June 2025 NATO Summit in The Hague to raise defense expenditure targets to 5% of GDP, and European Union member state outlays reached EUR 343 billion in 2024, advancing toward a projected EUR 381 billion in 2025. These commitments are translating directly into tactical communications procurement pipelines, particularly for software-defined radios (SDRs), mobile ad-hoc network (MANET) radios, satellite communication terminals, and command-and-control (C2) software platforms. In Asia Pacific, China, India, South Korea, and Japan are each accelerating modernization programs that include tactical communications infrastructure as a priority line item.

Technology displacement from legacy hardware-bound systems is the second major force. High-speed SDRs now operate across the 30–2,500 MHz spectrum range, simultaneously managing multiple waveforms—including SINCGARS, Link 16, Mobile User Objective System (MUOS), and high-capacity data networks—within a single manpack unit. The U.S. Army's Handheld, Manpack, Small Form Fit (HMS) program is procuring approximately 100,000 two-channel Leader Radios and 65,000 manpack radios under an IDIQ contract with a USD 16 billion ceiling, the largest tactical radio procurement in U.S. Army history. Simultaneously, the U.S. Army's Next Generation Command and Control (NGC2) program and the Joint All-Domain Command and Control (JADC2) initiative are driving integration of space-based and terrestrial communication layers to achieve seamless cross-domain data exchange.

The third force is geopolitical urgency, as lessons from conflicts in Ukraine, Gaza, and contested maritime regions demonstrate the decisive role of resilient, encrypted tactical communications in modern warfare. Anti-jamming waveforms, Low Probability of Intercept/Low Probability of Detection (LPI/LPD) technologies, and post-quantum encryption capabilities are shifting from advanced features to baseline procurement requirements. NATO interoperability mandates such as STANAG 4677 and Link 16 standardization shorten replacement cycles and create sustained demand from allied procurement offices, extending the market's primary customer base well beyond the United States to over 30 NATO and partner nations.

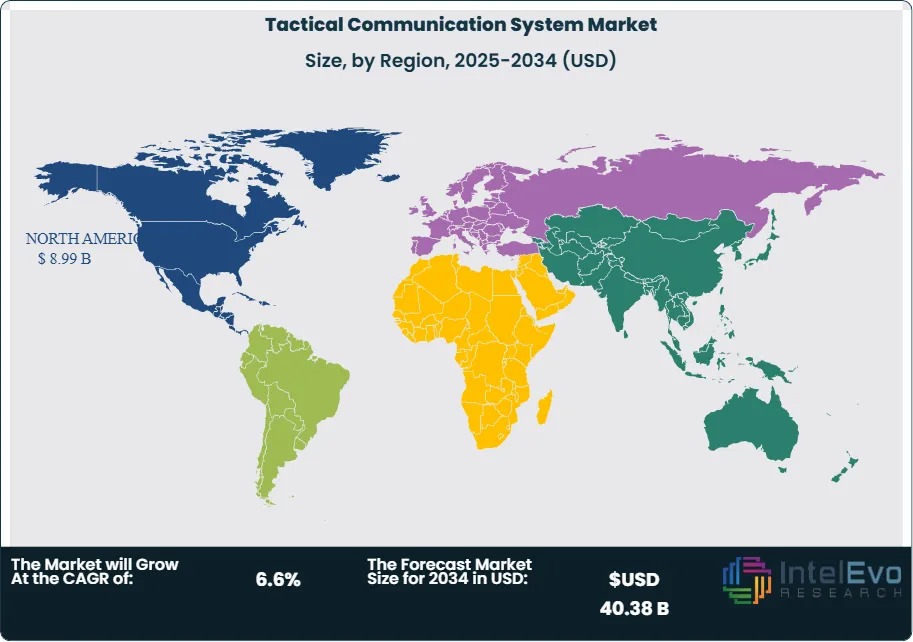

North America dominated the tactical communication system market in 2025 with a 39.5% revenue share valued at approximately USD 8.99 billion. Europe held the second-largest share at approximately 23.7%, valued at USD 5.39 billion, and is projected to grow at a 7.8% CAGR through 2034. Asia Pacific is the fastest-growing region, driven by defense modernization in India, South Korea, Japan, and Australia, alongside China's indigenous capability expansion under its military-civil fusion doctrine. The market's maturity period toward 2034 will be shaped by the commercial deployment of LEO satellite communication constellations, the integration of AI-driven spectrum management, and the transition from static encryption to post-quantum cryptographic standards mandated by the U.S. National Institute of Standards and Technology (NIST) through its PQC standardization process.

Market Definition & Scope

The tactical communication system market is defined as the commercial and government market for secure, interoperable communication equipment and software designed for real-time exchange of voice, data, imagery, and sensor telemetry among military and paramilitary units operating in contested, austere, or rapidly changing environments. The market encompasses software-defined radios (SDRs) across handheld, manpack, vehicular, airborne, and shipborne form factors; satellite communication (SATCOM) terminals and ultra-high-frequency links; mobile ad-hoc network (MANET) and mesh radio systems; tactical data links including Link 16 and Link 22; command-and-control (C2) software and battlefield management systems (BMS); encryption and cryptographic modules; and associated integration and sustainment services. Key system standards include MIL-STD-188, STANAG 4677, NSA Type 1 encryption certification, FIPS 140-3, and MUOS satellite architecture.

This analysis covers tactical communication systems deployed across military ground forces, naval vessels, airborne platforms, special operations forces, and homeland security agencies. Explicitly excluded are general-purpose commercial wireless infrastructure, public safety broadband networks (such as FirstNet), civilian VSAT deployments, and non-tactical military infrastructure communications such as fixed strategic satellite systems. The tactical communication system market represents a specialized sub-segment of the broader military communications sector, which was valued at USD 42.10 billion in 2025 when general military communication infrastructure is included. Tactical systems, by definition, serve the direct engagement layer—from battalion level downward to individual soldier—requiring ruggedization to MIL-STD-810, resistance to electronic warfare, and certification to classified cryptographic standards that commercial-grade systems cannot meet.

, By Component (Hardware, Software, Services), By Comm Type (Voice, Data, Video), By End-User (Military, Homeland Security, Law Enforcement, Emergency) Region, Key Players – Dynamics, C4ISR Network Modernization & Secure Software-Defined Radio Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The tactical communication system market expanded from an estimated USD 18.5 billion in 2020 to USD 22.75 billion in 2025 and is forecast to reach USD 40.38 billion by 2034, a 6.6% CAGR over the 2025–2034 forecast period, with an absolute opportunity of USD 17.63 billion.

- Segment Dominance (Platform): Land-based systems led the tactical communication system market with a 44.76% revenue share in 2025, valued at approximately USD 10.19 billion, anchored by the U.S. Army HMS procurement program and NATO vehicle-mounted radio upgrades.

- Segment Dominance (Component): Hardware held 57.68% of market revenue in 2025 at approximately USD 13.11 billion, while services are growing at a 7.61% CAGR, driven by software-defined platform sustainment contracts and over-the-air waveform update programs.

- Driver: NATO interoperability mandates and the U.S. DoD's JADC2 strategy are requiring allied forces to replace legacy voice-centric radios with dual-channel SDRs capable of simultaneously managing Link 16, MUOS SATCOM, and MANET waveforms, sustaining the most capital-intensive procurement wave in tactical radio history.

- Restraint: Spectrum congestion in the 225–400 MHz band and the high development cost of post-quantum encryption modules—estimated at 3–5× the cost of current NSA Type 1 cryptography—are constraining procurement timelines for the most advanced systems.

- Opportunity: Space-based tactical communication platforms represent the fastest-growing segment at a 9.91% CAGR through 2031, enabled by the U.S. Space Development Agency's Tranche 1 Transport Layer constellation and LEO integration into tactical architectures under the JADC2 framework.

- Trend: AI-driven cognitive spectrum management is transitioning from R&D to procurement, with Elbit Systems' cloud-based E-LynX portal demonstrating remote diagnostics and over-the-air patching across 14 nations, signaling a structural shift toward software-defined platform sustainment as a revenue model.

- Regional: North America held a 39.5% market share in 2025 valued at approximately USD 8.99 billion, anchored by the U.S. DoD's HMS, NGC2, and JADC2 investments, along with Foreign Military Sales (FMS) programs delivering L3Harris Falcon IV radios to NATO allies including the Netherlands, Germany, and Australia.

Key Insights Summary

- In April 2025, L3Harris Technologies finalized a USD 1.10 billion agreement with the Dutch Ministry of Defence under the FOXTROT program to supply Falcon IV SDRs—including the AN/PRC-117G, AN/PRC-152A, and AN/PRC-160—capable of interoperating with over one million tactical devices deployed across NATO forces worldwide.

- In January 2025, L3Harris received approximately USD 300 million in production orders for Army Manpack and Leader radios under the HMS program; the broader HMS IDIQ contract carries a USD 16 billion ceiling covering approximately 100,000 Leader Radios and 65,000 Manpack radios, representing the largest SDR procurement in U.S. Army history.

- Defense Innovation Unit (DIU) data from December 2025 confirms the StreamCaster 4400 Enhanced (SC4400E) MANET radio from Silvus Technologies—a Motorola Solutions company—was added to the Blue UAS Framework, validating its National Defense Authorization Act compliance and AES-256/FIPS 140-3 encryption for U.S. military drone command-and-control operations.

- In June 2025, Kongsberg Defence & Aerospace and Thales formed a 50/50 joint venture in Norway merging Kongsberg's software-defined tactical radio unit with Thales' cryptographic networks business; combined 2024 revenues were approximately EUR 130 million, with a projected doubling to EUR 254 million by 2030 on NATO interoperability demand.

- The U.S. Space Development Agency's 126-satellite Tranche 1 Transport Layer recorded 98% link availability during simulated jamming scenarios in 2025, demonstrating LEO constellation integration into tactical communication architectures and anchoring the space platform segment's 9.91% CAGR through 2031.

- In September 2025, the UK Ministry of Defence awarded a GBP 550 million (approximately USD 741 million) Tactical Communications Logistics Support contract spanning February 2028 to February 2033 under the TacCIS program, covering spares, repairs, stock management, and battlefield communications sustainment, while separately planning an eight-year tactical communications procurement program beginning June 2026.

Competitive Landscape Overview

The tactical communication system market is moderately consolidated, with the top five vendors—L3Harris Technologies, Inc.; RTX Corporation; General Dynamics Corporation; BAE Systems plc; and Northrop Grumman Corporation—capturing the majority of 2025 revenue concentrated within the United States and NATO markets. The top four together hold an estimated combined share of approximately 45–50% of global market revenue, a figure depressed relative to pure hardware markets because integration services, software maintenance, and government-specific cryptographic certification create specialized niches that specialized vendors such as Elbit Systems Ltd., ASELSAN A.S., Rohde & Schwarz GmbH & Co. KG, and Silvus Technologies can defend against tier-one incumbents. Competition is shifting from hardware specifications toward integrated platform propositions that bundle ruggedized SDR hardware with proprietary waveform portfolios, cloud-based sustainment portals, and AI-driven spectrum management software.

The competitive landscape is being reshaped by two structural forces. The first is NATO partner nation procurement, where FMS relationships allow U.S. vendors like L3Harris to extend platform standardization beyond DoD into 30+ allied military customers simultaneously, giving incumbents a compounding installed-base advantage that makes switching prohibitively expensive. L3Harris's Falcon IV systems interoperate with over one million previously fielded tactical devices, a network-effect moat that challengers cannot erode through technical superiority alone. The second force is European industrial sovereignty: the Thales-Kongsberg joint venture in Norway, Elbit's European expansion, and ASELSAN's indigenous SDR program are all responses to a growing European political preference for non-U.S. communication architecture in sensitive military networks—a trend that is not yet a procurement reality but is increasingly influencing long-cycle program planning in France, Germany, and Scandinavia.

Competitive Landscape Matrix

| Company | HQ | Position | Key Product | Geo Strength | Recent Strategic Move |

| L3Harris Technologies, Inc. | USA | Leader | Falcon IV AN/PRC-158, AN/PRC-163, AN/PRC-167 | Global | USD 1.10B Falcon IV contract with Dutch MOD, April 2025; USD 24M NGC2 Manpack contract, October 2025 |

| RTX Corporation (Raytheon) | USA | Leader | SINCGARS, RT-1523, Multifunctional Information Distribution System (MIDS JTRS) | N. America, NATO | Continued MIDS JTRS upgrades for NATO Link 16 interoperability under multiyear DoD contracts |

| General Dynamics Corporation | USA | Leader | Stryker vehicle comms, WIN-T systems, Bowman replacement | N. America, Europe | Integration work on UK Bowman replacement program valued at USD 85 million, 2025 |

| Thales Group | France | Leader | SYNAPS SDR, PR4G F@stnet VHSDR, SquadNet tactical radios | Europe, Middle East, Asia | Formed 50/50 JV with Kongsberg Defence & Aerospace in Norway for secure tactical comms, June 2025 |

| Northrop Grumman Corporation | USA | Challenger | JTIDS/MIDS terminals, AN/TSQ-179 HCDR, battlefield networks | N. America, NATO allies | SDA Tranche 1 Transport Layer milestones advancing LEO-enabled tactical link resilience, 2025 |

| BAE Systems plc | UK | Challenger | BOWMAN, MORPHEUS tactical comms, E-LYNX integration | UK, Europe, Five Eyes | USD 85M Bowman replacement integration contract awarded, 2025; TacCIS logistics support underpinned |

| Elbit Systems Ltd. | Israel | Challenger | E-LynX SDR, BMS C4ISR, TORCH-X battlefield OS | Europe, Asia Pacific, Middle East | USD 1.635B European defence contract including Network Combat Solution and C4ISR, August 2025 |

| Silvus Technologies (Motorola Solutions) | USA | Niche Player | StreamCaster 4400E MANET, StreamCaster LITE SL5200 | N. America, Five Eyes | SC4400E MANET radio added to DoD DIU Blue UAS Framework, December 2025 |

By Platform

Land-based platforms anchored the tactical communication system market in 2025 with a 44.76% share, generating approximately USD 10.19 billion, because ground force modernization—particularly under the U.S. Army's HMS, Integrated Tactical Network (ITN), and NGC2 programs—drives the highest-volume SDR procurements globally. Handheld and manpack radios account for the majority of land segment unit volume; the U.S. Army alone plans to procure approximately 165,000 units under HMS, while NATO allies in Germany, the Netherlands, Poland, and Australia are executing parallel vehicle-mounted radio upgrades. The ground segment's growth is moderated by the long program lifecycles inherent to platform-centric procurement and by budget reallocation toward unmanned systems and precision fires, but its sheer installed base size sustains an annualized replacement and upgrade demand that is structurally predictable across the forecast window.

Airborne platforms held the second-largest share, encompassing tactical radios and data links fitted to rotary- and fixed-wing aircraft and increasingly to unmanned aerial vehicles (UAVs). The F-35 Block 4 upgrade program illustrates how airborne communications enrich the multi-domain network, with its 274 Mbps data links enabling real-time sensor fusion across air, ground, and naval nodes. The expanding deployment of ISR UAVs—requiring MANET radios that meet DoD Blue UAS Framework certification, as validated for the Silvus SC4400E in December 2025—is creating a distinct high-growth sub-segment where size, weight, and power (SWaP) optimization, LPI/LPD waveforms, and anti-jamming capabilities are the primary purchase criteria rather than voice clarity or legacy waveform compatibility. The airborne segment is growing at an estimated 8–9% CAGR through 2034.

Naval platforms represent the third major segment, differentiated by their requirement for extreme ruggedization in salt-spray, high-humidity, and electromagnetic interference environments. Rohde & Schwarz's M3SR Series4400 radios—delivered to the German Navy with coatings extending mean time between failures to 15,000 hours at sea—illustrate the premium naval specifications command. Shipborne systems also integrate SATCOM terminals, HF skywave communications for beyond-line-of-sight (BLOS) scenarios, and UHF tactical data links connecting surface vessels with submarines, aircraft, and shore-based headquarters. Space-based tactical communication platforms are the fastest-growing segment at a projected 9.91% CAGR through 2031; the U.S. Space Development Agency's 126-satellite Tranche 1 Transport Layer constellation, achieving 98% link availability under simulated jamming in 2025, provides the architectural backbone for JADC2's cross-domain data routing ambitions.

By Component

Hardware commanded 57.68% of the tactical communication system market in 2025 at approximately USD 13.11 billion, driven by the volume of SDR units, SATCOM terminals, vehicular mounting kits, and antenna systems being procured under large-scale military modernization programs across the United States, NATO Europe, and Asia Pacific. Within the hardware tier, manpack and handheld radios account for the highest unit volume, while vehicular integration kits and maritime ruggedized systems generate higher per-unit revenue. The hardware share is gradually declining as software maintenance, over-the-air update subscriptions, and integration services capture a growing fraction of total customer expenditure; Elbit Systems' cloud-based diagnostic portal for E-LynX radios, operational across 14 nations in 2025, is a leading indicator of this structural shift.

Software and services together are growing at an aggregate rate that exceeds the market's overall CAGR, with services alone advancing at a 7.61% CAGR through 2031. The service revenue pool encompasses integration engineering—exemplified by BAE Systems' USD 85 million Bowman replacement integration contract in 2025—as well as depot-level and field maintenance, software-defined waveform licensing, cybersecurity services covering NSA cryptographic modernization compliance, and long-term logistics support such as the UK MoD's GBP 550 million TacCIS sustainment contract. The transition from hardware-centric to software-defined value capture is strategically significant: vendors who own the waveform intellectual property and the over-the-air update infrastructure gain recurring revenue streams and higher switching costs than hardware-only competitors.

By Communication Type

Data communication captured 41.26% of the tactical communication system market in 2025 at approximately USD 9.38 billion, reflecting the doctrinal shift from voice-centric coordination to network-centric warfare where blue-force tracking packets, targeting data, intelligence imagery, and logistics updates flow continuously across all echelons. High-throughput SDRs now push sensor telemetry from dismounted soldiers and armored vehicles to command posts, enabling real-time common operating picture generation without radio silence discipline that characterized legacy voice-centric protocols. The JADC2 architecture explicitly requires data dominance as its enabling condition, with data communication projected to grow at a 7–8% CAGR through 2034 as the single-largest category by revenue.

Voice communication remains indispensable at the dismounted soldier level, where radio discipline, simplicity of operation under stress, and minimal latency make digital push-to-talk the preferred mode for squad-level coordination. Video communication is the fastest-growing communication type at an 8.49% CAGR through 2031, driven by the proliferation of body-worn cameras, sensor-equipped UAVs, and vehicle optics that require live video transmission back to command elements for real-time situational awareness and target identification. Secure satellite communication is growing at an estimated 7–8% CAGR, underpinned by MUOS constellation maturation, LEO constellation integration, and the urgent need for BLOS communications in contested environments where terrestrial links can be severed by electronic warfare or physical disruption. Encryption and cybersecurity modules represent the fastest-growing embedded sub-category, as post-quantum cryptographic standards mandated under NIST's PQC process create a mandatory upgrade cycle across all fielded platforms.

By End-User

Defense forces commanded 79.23% of tactical communication system market revenue in 2025 at approximately USD 18.02 billion, reflecting the market's foundational character as a military procurement sector where budgetary allocation is driven by national security policy rather than commercial ROI calculations. Within the defense end-user tier, army ground forces represent the largest single buyer by unit volume, with air forces prioritizing high-bandwidth airborne data links and navies emphasizing ruggedization and SATCOM integration. Special operations forces—served by products like the Falcon IV AN/PRC-167 under the USSOCOM Next Generation Tactical Communications (NGTC) program—command the highest per-unit value due to the advanced capability requirements of covert, BLOS, and multi-environment missions.

Homeland security agencies are the fastest-growing end-user segment at an 8.54% CAGR through 2031, driven by growing border security investments in the United States, Middle East, and Asia Pacific, as well as the expansion of tactical radio use in counter-narcotics and counter-terrorism operations. Law enforcement tactical communication adoption is expanding in parallel as specialized units—including SWAT teams, federal agencies, and national police forces—procure militarized SDR systems with P25 Phase 2 or TETRA interoperability for coordinated multi-agency operations. Emergency services represent a nascent third end-user category, particularly in countries such as the United Arab Emirates, Saudi Arabia, and South Korea, where national disaster response frameworks specify military-grade communication standards for civilian emergency management infrastructure.

Regional Analysis

North America held the largest regional share of the tactical communication system market in 2025 at approximately 39.5%, generating USD 8.99 billion, anchored almost entirely by the United States, which contributes over 92% of the regional total. The U.S. DoD's sustained investment in HMS, JADC2, ITN, and the Space Development Agency's transport layer constellation creates a procurement environment unlike any other region in scale, contract certainty, and technology ambition. U.S. defense spending appropriated for communication modernization extends further through Foreign Military Sales (FMS) channels, with L3Harris Falcon IV contracts in the Netherlands, Australia, and Canada representing USD 1.1 billion in April 2025 FMS activity alone. Canada contributes through its own SDR modernization and through its role as a NORAD communications infrastructure partner. North America is projected to maintain its leadership with a CAGR of approximately 6.5% through 2034.

Europe held approximately 23.7% of market revenue in 2025 at USD 5.39 billion and is the second-largest region. The NATO defence spending increase—driven by the alliance's June 2025 Hague Summit commitment to 5% of GDP spending targets—is the single most consequential driver of European tactical communication demand over the forecast period. The UK's TacCIS program, including the GBP 550 million logistics support contract awarded in September 2025 and a planned eight-year procurement program beginning June 2026, illustrates the scale of structured recapitalization underway. Germany, Poland, France, and the Nordic states are simultaneously replacing legacy analogue and first-generation digital systems. The formation of the Kongsberg-Thales joint venture in Norway in June 2025—targeting EUR 254 million in combined revenue by 2030—signals a European industrial consolidation trend. Europe's market is projected to grow at 7.8% CAGR through 2034.

Asia Pacific generated approximately 20% of market revenue in 2025 at USD 4.55 billion and is the fastest-growing region by CAGR at approximately 7.15% through 2031. India's Tactical Communication System (TCS) program—with Bharat Electronics Limited (BEL) initiating mass production of Secure Manpack SDRs for the Indian Army—represents a dual driver of domestic manufacturing and operational capability. South Korea and Japan are investing in network-centric warfare architectures aligned with U.S. JADC2 concepts, with the Republic of Korea Ministry of Defense adopting Iridium satellite connectivity for military operations in February 2024. China's People's Liberation Army is developing indigenous tactical radio and data link systems under its military-civil fusion doctrine, creating a parallel procurement ecosystem that excludes Western vendors but stimulates competitive innovation globally.

The Middle East and Africa represented approximately 10.4% of the global tactical communication system market in 2025, valued at approximately USD 2.37 billion. Israel, Saudi Arabia, and the UAE are the primary demand centers, each investing in advanced SDR systems, SATCOM terminals, and C4ISR integration. The UAE's border security and its participation in regional coalition operations drive tactical radio procurement, while Saudi Arabia's Vision 2030 defense industrialization goals are creating domestic assembly opportunities for international vendors. In August 2025, Elbit Systems' USD 1.635 billion contract with an undisclosed European nation—including a military digitalization and Network Combat Solution—demonstrates the company's ability to win large-format platform deals. Latin America contributed approximately 6.4% of market revenue in 2025 at USD 1.46 billion, with Brazil, Mexico, and Colombia as primary markets driven by counter-narcotics operations and border security modernization programs.

Country Analysis

The United States tactical communication system market reached approximately USD 8.34 billion in 2025, growing at a country-level CAGR of approximately 6.5% through 2034. Three programs define the near-term demand trajectory. The HMS IDIQ contract with a USD 16 billion ceiling is the primary volume driver, covering approximately 165,000 SDR units for the U.S. Army. The NGC2 program—supporting the 4th Infantry Division's integration of the Falcon IV AN/PRC-158C Gateway Manpack ahead of Project Convergence 2026—is the primary network integration driver, embedding the tactical radio into the Army's transport layer data architecture. The JADC2 framework is the primary strategic driver, connecting all military branches—Army, Air Force, Navy, Space Force, and Marine Corps—into a unified data network and mandating interoperability standards that govern all future radio procurement. The DoD's adoption of NIST post-quantum cryptographic standards also mandates a forward cryptographic upgrade cycle, beginning with Special Operations Forces and extending to conventional units through 2030.

The United Kingdom's tactical communication system market was valued at approximately USD 1.18 billion in 2025, growing at an estimated 8.2% CAGR through 2034, reflecting a structured recapitalization program under TacCIS. In September 2025, the UK MoD formalized a GBP 550 million Tactical Communications Logistics Support contract spanning five years from February 2028, covering spares, repairs, and stock management for battlefield communications. Separately, in December 2025, the UK initiated planning for an eight-year tactical communications procurement program spanning June 2026 to June 2034. In August 2025, General Dynamics Mission Systems UK and supplier GRC were selected to incorporate eight Scytale SATCOM systems into the Bowman platform as Deployed Bearer of Opportunity technology, connecting headquarters to dispersed units in austere environments. BAE Systems' Bowman replacement integration work—valued at USD 85 million in 2025—positions the company as the primary systems integrator for the UK's next-generation tactical radio network.

India's tactical communication system market reached approximately USD 870 million in 2025, with BEL's indigenization of Secure Manpack SDRs under the Indian Army's TCS program representing a decisive shift from import dependency to domestic manufacturing. India's defense ministry allocated approximately 25% of its defense capital budget to communication and electronics modernization in fiscal year 2024–2025, reflecting the strategic priority placed on digital battlefield command and control following border tension with China. The German market reached approximately USD 680 million in 2025 and is accelerating under the Bundeswehr's EUR 100 billion Sondervermögen (special fund) established in 2022, with tactical communications comprising a structured modernization line for both land forces and the Luftwaffe's tactical data link upgrades. Germany's participation in NATO's CWIX25 interoperability exercises at Bydgoszcz, Poland, in June 2025 underscored the country's commitment to allied network compatibility and drove procurement requirements for STANAG-compliant SDR solutions.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Platform

- Land

- Airborne

- Naval

- Space

By Component

- Hardware

- Software

- Services

By Communication Type

- Voice Communication

- Data Communication

- Video Communication

By End-User

- Military

- Homeland Security

- Law Enforcement

- Emergency Response Services

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 22.75 B |

| Forecast Revenue (2034) | USD 40.38 B |

| CAGR (2025-2034) | 6.6% |

| Historical data | 2021-2025 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Platform, (Land, Airborne, Naval, Space), By Component, (Hardware, Software, Services), By Communication Type, (Voice Communication, Data Communication, Video Communication), By End-User, Military, (Homeland Security, Law Enforcement, Emergency Response Services), |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | L3HARRIS TECHNOLOGIES, INC., RTX CORPORATION (RAYTHEON INTELLIGENCE & SPACE), GENERAL DYNAMICS CORPORATION, THALES GROUP, NORTHROP GRUMMAN CORPORATION, BAE SYSTEMS PLC, ELBIT SYSTEMS LTD., ROHDE & SCHWARZ GMBH & CO. KG, ASELSAN A.S., LEONARDO S.P.A., BHARAT ELECTRONICS LIMITED, SILVUS TECHNOLOGIES (MOTOROLA SOLUTIONS), VIASAT, INC., IRIDIUM COMMUNICATIONS INC., CODAN LIMITED, BARRETT COMMUNICATIONS PTY LTD., KONGSBERG DEFENCE & AEROSPACE, BITTIUM CORPORATION, OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Component (Hardware, Software, Services), By Comm Type (Voice, Data, Video), By End-User (Military, Homeland Security, Law Enforcement, Emergency) Region, Key Players – Dynamics, C4ISR Network Modernization & Secure Software-Defined Radio Trends & Forecast 2026-2034")

, By Component (Hardware, Software, Services), By Comm Type (Voice, Data, Video), By End-User (Military, Homeland Security, Law Enforcement, Emergency) Region, Key Players – Dynamics, C4ISR Network Modernization & Secure Software-Defined Radio Trends & Forecast 2026-2034")

, By Component (Hardware, Software, Services), By Comm Type (Voice, Data, Video), By End-User (Military, Homeland Security, Law Enforcement, Emergency) Region, Key Players – Dynamics, C4ISR Network Modernization & Secure Software-Defined Radio Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Tactical Communication System Market?

Global Tactical Communication System Market was valued at USD 21.39 billion in 2024 and is projected to reach USD 40.38 billion by 2034, at a CAGR of 6.6% during 2026–2034.

Who are the major players in the Tactical Communication System Market?

L3HARRIS TECHNOLOGIES, INC., RTX CORPORATION (RAYTHEON INTELLIGENCE & SPACE), GENERAL DYNAMICS CORPORATION, THALES GROUP, NORTHROP GRUMMAN CORPORATION, BAE SYSTEMS PLC, ELBIT SYSTEMS LTD., ROHDE & SCHWARZ GMBH & CO. KG, ASELSAN A.S., LEONARDO S.P.A., BHARAT ELECTRONICS LIMITED, SILVUS TECHNOLOGIES (MOTOROLA SOLUTIONS), VIASAT, INC., IRIDIUM COMMUNICATIONS INC., CODAN LIMITED, BARRETT COMMUNICATIONS PTY LTD., KONGSBERG DEFENCE & AEROSPACE, BITTIUM CORPORATION, OTHERS

Which segments covered the Tactical Communication System Market?

By Platform, (Land, Airborne, Naval, Space), By Component, (Hardware, Software, Services), By Communication Type, (Voice Communication, Data Communication, Video Communication), By End-User, Military, (Homeland Security, Law Enforcement, Emergency Response Services),

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Tactical Communication System Market

Published Date : 17 Jul 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date