- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Tea Capsules Market Size & Forecast 2025–2034 | 7.0% CAGR

Global Tea Capsules Market Size, Share & Trends – By Type (Black Tea Capsules, Green Tea Capsules, Herbal Tea Capsules, Specialty Blends), By Distribution Channel (Supermarkets/Hypermarkets, Specialty Stores, Online Retail, Other Channels), By End-Use (Herbs & Spices, Chamomile, Berries, Hibiscus, Pomegranate), By Application (HoReCa, Residential, Commercial), Regional Analysis, Competitive Landscape & Industry & Forecast 2025–2034

Report Overview

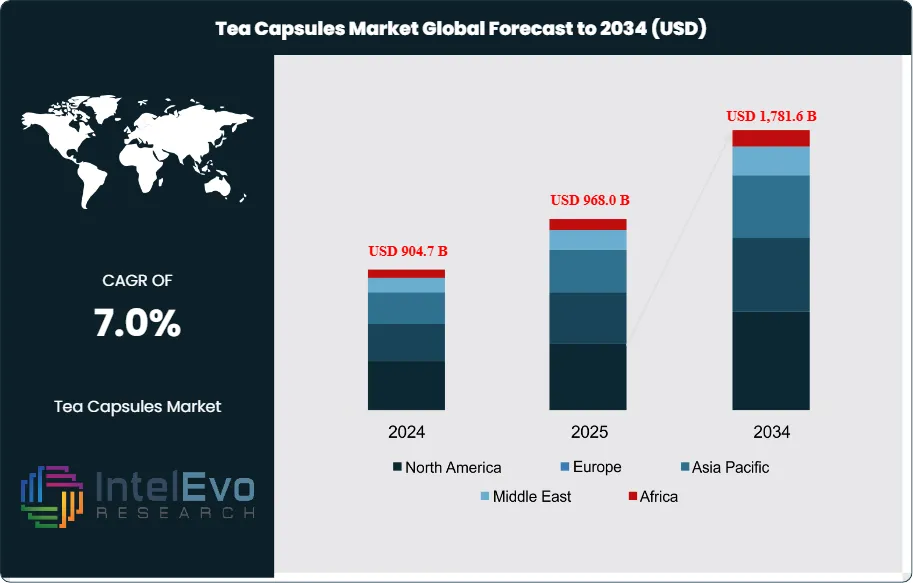

The Global Tea Capsules Market was valued at approximately USD 904.7 million in 2024 and is projected to reach nearly USD 1,781.6 million by 2034, supported by rising demand for convenient single-serve beverages and premium tea consumption trends. Based on the stated growth trajectory, the market size for 2025 is estimated at approximately USD 968.0 million. From 2026 onward, the market is expected to expand at a compound annual growth rate (CAGR) of approximately 7.0% during 2026–2034, ultimately reaching around USD 1,781.6 million by 2034.

Get More Information about this report -

Request Free Sample ReportGrowth reflects the convergence of convenience, premiumization, and health-focused consumption within the broader hot beverages category. Tea capsules extend the installed base of single-serve coffee systems into tea drinking occasions, allowing brands to capture share from traditional loose and bagged formats. In 2024, single-serve formats already account for an estimated 18–20% of global at-home specialty tea spending, with capsules projected to exceed 25% by 2034 as adoption deepens in urban households and offices.

Demand-side momentum stems from rising preference for portion-controlled, consistently brewed beverages and expanding interest in green, herbal, and functional blends. Health-aware consumers increasingly favor teas positioned for antioxidant support, relaxation, and metabolic wellness, lifting the share of specialty and wellness-focused capsules to nearly 40% of segment revenue in 2024. On the supply side, leading manufacturers and private labels invest in capsule-compatible blends, origin-specific teas, and organic-certified offerings, while large tea producers integrate downstream into branded capsule portfolios. E-commerce and direct-to-consumer channels now contribute close to 30–32% of tea capsule sales, supported by subscription models and curated assortments.

Technology and automation reshape the value chain. Producers deploy automated filling and sealing lines to improve throughput and quality consistency, while AI-enabled demand forecasting optimizes inventory and reduces waste. Digital platforms use recommendation engines to personalize flavor discovery and cross-sell higher-margin specialty ranges. At the same time, regulators tighten oversight on food safety, labeling, and packaging waste. Extended producer responsibility rules and restrictions on non-recyclable materials accelerate innovation in compostable, biodegradable, and aluminum-recycling capsule formats. Key risks include volatile tea leaf prices, machine-compatibility constraints, increasing scrutiny of single-use packaging, and intensifying rivalry from both coffee capsules and ready-to-drink teas.

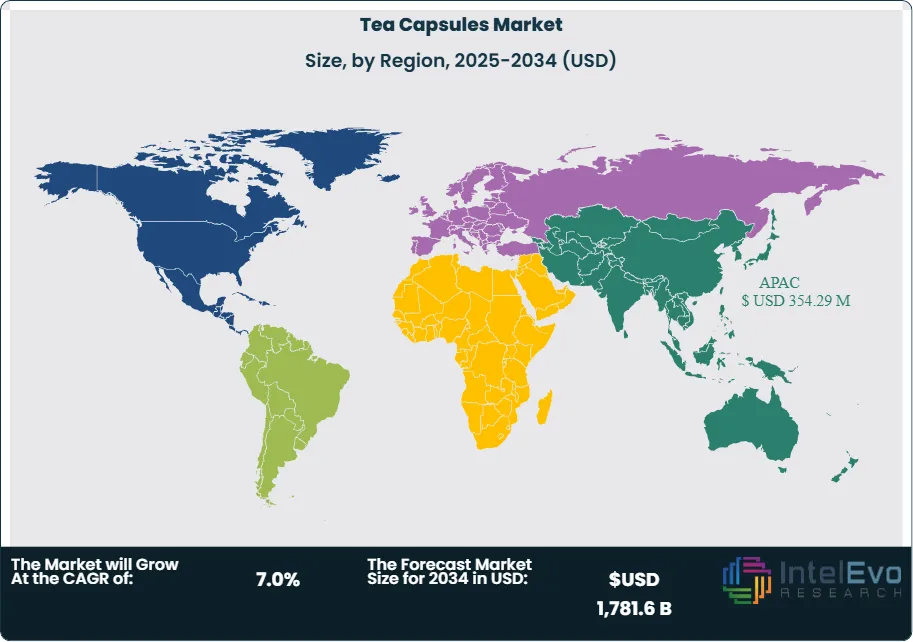

Regionally, Asia Pacific represents the largest tea consumption base, with India recognized as the leading tea-drinking nation in absolute terms and Turkey ranking among the highest in per capita intake. However, Europe currently leads in capsule penetration, accounting for roughly 35% of global tea capsule revenue in 2024, followed by North America at about 30% and Asia Pacific at nearly 25%. Expansion of modern retail, rapid growth of middle-income households, and strong tea-drinking traditions position Asia Pacific and parts of the Middle East as priority investment hotspots over the coming decade, particularly for brands that combine sustainable packaging, wellness-led formulations, and omnichannel distribution.

, By Distribution Channel (Supermarkets/Hypermarkets, Specialty Stores, Online Retail, Other Channels), By End-Use (Herbs & Spices, Chamomile, Berries, Hibiscus, Pomegranate), By Application (HoReCa, Residential, Commercial), Regional Analysis, Competitive Landscape & Industry & Forecast 2025–2034")

Key Takeaways

- Market Growth: The global tea capsules market records revenue of 904.7 million USD, 2024 and will reach 1,781.6 million USD, 2034, growing at a 7.0% CAGR, 2024-2034.

- Segment Dominance: Green tea capsules lead the product mix with a 42.6% share of global tea capsule revenue, 2024, reflecting strong preference for wellness-oriented formats.

- Segment Dominance: Supermarkets and hypermarkets command 48.7% of distribution revenue, 2024, while the HoReCa application segment contributes 34.7% of global demand, 2024, anchoring volumes in organized retail and foodservice.

- Driver: Convenience-led single-serve consumption and consistent brew quality support the 7.0% CAGR, 2024-2034, as households shift spending from loose and bagged tea formats. Growth in at-home machine installations gains momentum, supported by estimated: 60.0% household penetration of capsule-compatible brewers, 2034.

- Restraint: Packaging waste concerns and price sensitivity limit faster adoption, as capsule products carry estimated: 15.0% price premium per cup versus conventional tea formats, 2024. Regulatory scrutiny on single-use materials in key markets could moderate volume expansion to an estimated: 6.0% annual growth in more restrictive jurisdictions, 2024-2034.

- Opportunity: Manufacturers can capture incremental value by expanding herbal and functional blends, where herbs and spices already generate a 38.8% revenue share in end-use terms, 2024. Digital and direct-to-consumer models open new routes to market, with estimated: 35.0% of tea capsule sales transacting online, 2034.

- Trend: Retailers and brands increasingly focus on sustainable and premium packaging, driving estimated: 50.0% of new product launches to feature recyclable or compostable capsules, 2030. Automation and data-driven inventory planning improve supply efficiency, cutting out-of-stock rates by an estimated: 20.0% in modern trade outlets, 2024-2034.

- Regional Analysis: Asia-Pacific holds the largest regional share at 36.6% of global revenue, 2024, while Europe follows with a 28.8% share, 2024 and progresses at a 7.1% CAGR, 2024-2034. North America emerges as the fastest-growing region with an 8.2% CAGR, 2024-2034, lifting its contribution to an estimated: 30.0% of global market revenue, 2034.

By Type

The tea capsule market continues to diversify as consumers expect precision, consistency, and convenience in daily beverage routines. Green tea capsules gained the highest share in 2024 at 42.6 percent. This reflects rising interest in beverages linked to wellness, metabolism balance, and antioxidant intake. You see stronger demand in markets where health awareness is accelerating, including Asia Pacific, Europe, and North America. These capsules also benefit from steady adoption among first-time buyers who shift from loose-leaf formats to portioned servings.

Growth across other categories remains steady. Black tea capsules retain a strong base in regions where black tea is traditionally preferred. Herbal tea capsules attract buyers seeking caffeine-free alternatives with functional attributes. The category labelled “others” includes fruit blends and specialty teas that appeal to niche buyers looking for distinct flavors. As capsule machine penetration increases globally, all segments are expected to expand at rates between 6 and 9 percent annually through 2028.

The outlook suggests sustained interest in green and herbal formats as consumers prioritize predictable taste and reduced preparation time. Brands that introduce origin-specific teas or certified organic blends are expected to capture additional share in higher-income urban markets.

By Application

The HoReCa segment led global demand in 2024 with a 34.7 percent share. Hotels, restaurants, and cafes prefer tea capsules because they reduce preparation time and support consistent service quality. Capsule systems also help staff manage peak-hour demand without compromising flavor or presentation. These features have made capsules a preferred option in establishments that handle high turnover and require predictable beverage output.

Residential adoption has risen as machine prices decline and online retail expands. You see households adopting capsules for convenience, portion control, and flavor variety. Commercial offices also contribute to demand as employers install beverage stations to support staff preferences for quick tea options. Together, residential and commercial channels show an annual growth trend of 7 to 10 percent through 2029.

The overall application outlook remains positive. HoReCa is expected to maintain its lead as hospitality groups update service models, while residential demand expands with broader machine availability and subscription-based capsule purchases.

By End-Use

Residential buildings represent the fastest-expanding end-use category due to rising machine ownership and broader awareness of capsule-based beverages. Households view capsules as a clean and consistent brewing method that minimizes waste and reduces preparation steps. This segment is projected to grow at an annual rate of approximately 9 percent from 2025 to 2030.

Commercial buildings, including offices and coworking spaces, continue to integrate capsule systems to meet employee beverage expectations. These installations help reduce wait times and improve service reliability. Industrial facilities show slower adoption, although demand increases in locations offering staff cafeterias with automated beverage systems.

The market structure indicates that residential and commercial buildings will account for more than 60 percent of total volume by 2030. Retailers and machine manufacturers increasingly target these segments with bundled offerings and curated flavor options.

By Region

Asia Pacific held 36.6 percent of global revenue in 2024. The region’s long-standing tea culture, combined with rising urban spending power, supports rapid adoption of capsule formats. China, India, and Japan lead consumption due to growing interest in premium beverages and greater acceptance of automated brewing systems. Retail expansion and strong e-commerce penetration make capsules widely accessible.

Europe accounts for a substantial share as well, supported by established single-serve habits and growing demand for specialty teas. Europe posted a 2024 share of 28.8 percent and is projected to grow at a 7.1 percent annual rate through 2034. North America remains the fastest-expanding region with an expected CAGR of 8.2 percent as households shift from coffee-only capsule use to mixed beverage capsules.

Latin America and the Middle East & Africa show emerging potential as capsule machine prices fall and modern retail expands. These regions are expected to grow at annual rates between 6 and 9 percent, driven by urban population growth and rising interest in premium beverages.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Type

- Black Tea Capsules

- Green Tea Capsule

- Herbal Tea Capsule

- Others

By Distribution Channel

- Supermarkets/Hypermarkets

- Specialty Stores

- Online Retail

- Other Distribution Channels

By End-Use

- Herbs & Spices

- Chamomile

- Berries

- Hibiscus

- Pomegranate

- Others

By Application

- HoReCa

- Residential

- Commercial

- Others

By Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 968.0 B |

| Forecast Revenue (2034) | USD 1,781.6 B |

| CAGR (2025-2034) | 7.0% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Type (Black Tea Capsules, Green Tea Capsule, Herbal Tea Capsule, Others), By Distribution Channel (Supermarkets/Hypermarkets, Specialty Stores, Online Retail, Other Distribution Channels), By End-Use (Herbs & Spices (Chamomile, Berries, Hibiscus, Pomegranate, Others)), By Application (HoReCa, Residential, Commercial, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Rene Coffee Pads Magmar, Plants Med Laboratories Pvt. Ltd., Bonhomia World, Italytrade SRL, LIPTON Teas and Infusions, Zoic Pharmaceuticals, Melitta Single Portions, T. Ronnefeldt KG, Nestlé S.A., Tea Château, Lexicare Pharma Pvt. Ltd., Red Espresso, AdvaCare Pharma, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Distribution Channel (Supermarkets/Hypermarkets, Specialty Stores, Online Retail, Other Channels), By End-Use (Herbs & Spices, Chamomile, Berries, Hibiscus, Pomegranate), By Application (HoReCa, Residential, Commercial), Regional Analysis, Competitive Landscape & Industry & Forecast 2025–2034")

, By Distribution Channel (Supermarkets/Hypermarkets, Specialty Stores, Online Retail, Other Channels), By End-Use (Herbs & Spices, Chamomile, Berries, Hibiscus, Pomegranate), By Application (HoReCa, Residential, Commercial), Regional Analysis, Competitive Landscape & Industry & Forecast 2025–2034")

, By Distribution Channel (Supermarkets/Hypermarkets, Specialty Stores, Online Retail, Other Channels), By End-Use (Herbs & Spices, Chamomile, Berries, Hibiscus, Pomegranate), By Application (HoReCa, Residential, Commercial), Regional Analysis, Competitive Landscape & Industry & Forecast 2025–2034")

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date