- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Thin Insulation Market Size | Growth to USD 10.1 Billion at 6.9% CAGR

Global Thin Insulation Market Size, Share & Analysis By Type (Sheets and Films, Vacuum Insulation Panels (VIP), Coatings, Foils, Foams), By Materials (Aerogels, Silica Aerogels, Metals, Plastic Foams, Fiberglass), By Thickness Range (Less Than 1 Inch, 1 Inch to 2 Inches, 2 Inches to 4 Inches, More Than 4 Inches), By Installation Method, By Application , By End User, Energy Efficiency Regulations, Thermal Performance Trends & Forecast 2025–2034

Report Overview

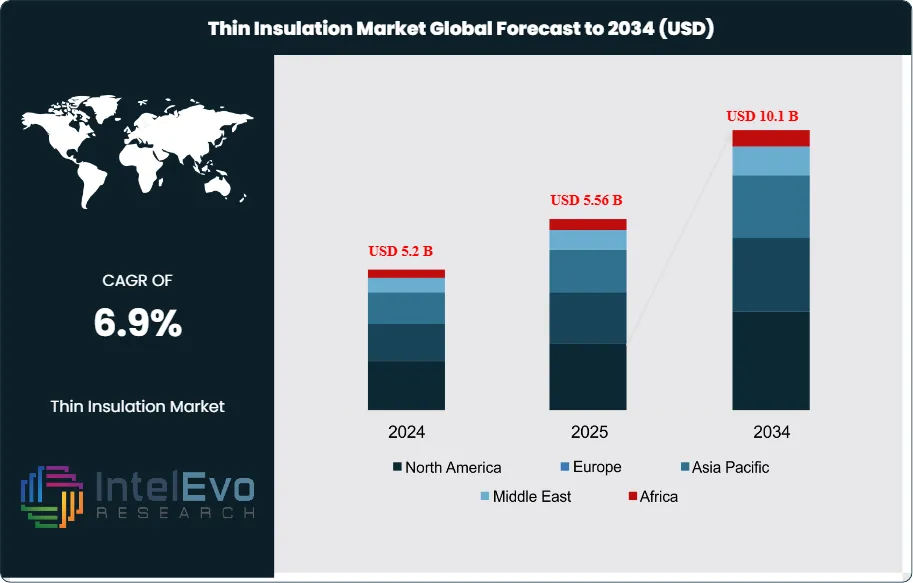

The Thin Insulation Market is estimated at USD 5.2 billion in 2024 and is on track to reach roughly USD 10.1 billion by 2034, implying a compound annual growth rate (CAGR) of 6.9% over 2025–2034. This trajectory reflects the sector’s pivotal role in addressing rising energy efficiency demands and space optimization challenges across industries such as construction, automotive, and electronics. Historically valued at USD 7.3 billion in 2021 and projected to hit USD 9.1 billion by 2026 at a CAGR of 4.5%, the market has transitioned from steady growth into a phase of accelerated adoption fueled by regulatory pressure, technological advancements, and sustainability imperatives.

Get More Information about this report -

Request Free Sample ReportDemand-side momentum is strongest in the construction industry, which accounted for nearly 45% of global thin insulation consumption in 2022, as building developers prioritize solutions that balance energy conservation with spatial efficiency. Automotive manufacturers, representing approximately 20% of market share, are increasingly deploying thin insulation for both thermal management and noise reduction in next-generation electric and hybrid vehicles. Supply-side dynamics further highlight the significance of China and Germany as key production hubs, with China alone exporting thin insulation materials valued at over USD 200 million to North America in 2022, underscoring the strategic role of global trade flows in meeting regional demand.

Regulatory frameworks have been instrumental in shaping adoption patterns. The European Union’s Energy Performance of Buildings Directive (EPBD) and the U.S. Department of Energy’s insulation standards are compelling both private and public stakeholders to invest in advanced insulation technologies. Complementing these mandates, policy-driven funding, such as the USD 500 million allocation under the U.S. Infrastructure Investment and Jobs Act for sustainable building solutions, is providing a tailwind for innovation and deployment.

Technological advancements are rapidly redefining product performance, with AI-driven design tools, nanomaterials, and advanced composites enabling thinner, more effective insulation with superior durability. Strategic collaborations and investments amplify this trend, as evidenced by the 2023 partnership between DuPont and Honeywell targeting next-generation automotive and aerospace applications, and Kingspan’s USD 100 million acquisition to strengthen market positioning.

Regionally, Western Europe and North America remain the largest consumers, while Asia-Pacific is emerging as a high-growth hotspot, driven by rapid urbanization and green infrastructure investments. For investors, opportunities lie in targeting markets where tightened building codes, electric vehicle penetration, and industrial automation converge to accelerate adoption, solidifying thin insulation’s status as a critical enabler of energy efficiency and sustainable growth.

, Coatings, Foils, Foams), By Materials (Aerogels, Silica Aerogels, Metals, Plastic Foams, Fiberglass), By Thickness Range (Less Than 1 Inch, 1 Inch to 2 Inches, 2 Inches to 4 Inches, More Than 4 Inches), By Installation Method, By Application , By End User, Energy Efficiency Regulations, Thermal Performance Trends & Forecast 2025–2034")

Key Takeaways

- Market Growth: The global Thin Insulation Market was valued at USD 5.2 billion in 2024 and is projected to reach USD 10.1 billion by 2034, expanding at a 6.9% CAGR (2025–2034). Growth is fueled by stricter building energy codes, demand for space-efficient insulation, and rising adoption in automotive and electronics sectors.

- Product Type: Sheets and Films accounted for 34.4% of the market in 2023, benefiting from cost-effectiveness, easy installation, and adaptability across construction and industrial applications.

- Material: Aerogels led the materials segment with a 28.7% share in 2023, driven by superior thermal resistance and adoption in aerospace, automotive, and oil & gas industries.

- Thickness Range: The “Less Than 1 Inch” category represented 27.7% of global demand, underscoring its importance in space-constrained applications such as retrofitted buildings, vehicles, and consumer electronics.

- Installation Method: Spray Insulation captured 34.5% share, offering enhanced energy efficiency and versatility for both residential and commercial construction projects.

- Application: Building Thermal Insulation remained the leading application with a 37.5% share, reflecting tightening building energy standards and the growing push for nearly zero-energy buildings in the EU and North America.

- End User: Building and Construction was the largest end-user segment, holding 35.6% share in 2023, as governments and private developers prioritize energy-efficient urban infrastructure.

- Driver: Regulatory frameworks such as the EU Energy Performance of Buildings Directive (EPBD) and the U.S. DOE insulation standards are accelerating adoption, complemented by USD 500 million in U.S. federal funding for sustainable building materials.

- Restraint: High production costs of advanced insulation materials, particularly aerogels, limit adoption in cost-sensitive markets, constraining penetration in low- and middle-income regions.

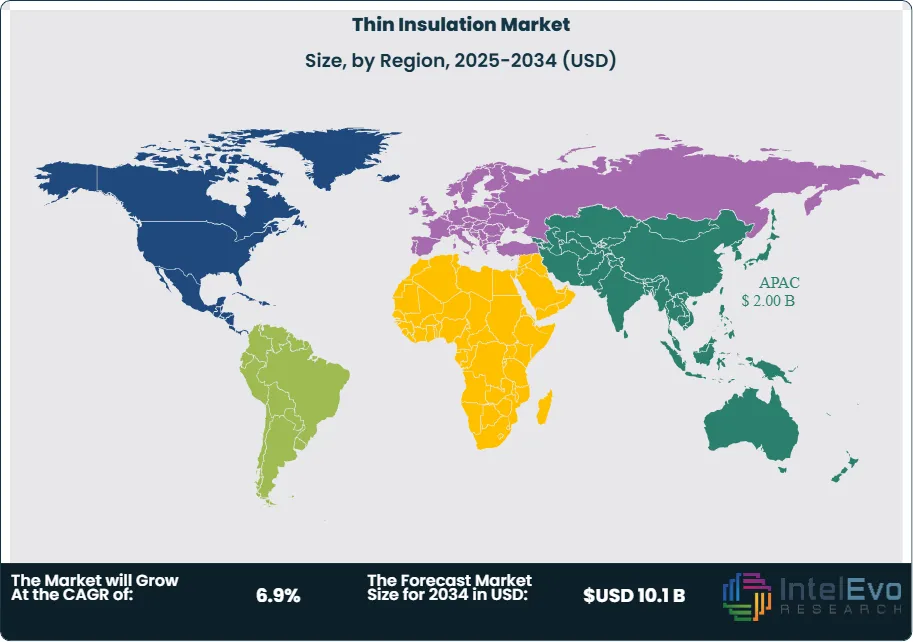

- Opportunity: The Asia-Pacific market, valued at USD 1.1 billion in 2023 (38.5% share), is set for accelerated growth due to rapid urbanization, green building initiatives, and increasing EV adoption—making it a prime investment hotspot.

- Trend: Ongoing R&D in nanomaterials, AI-driven insulation design, and lightweight composites is reshaping the market. Notable moves include the 2023 DuPont-Honeywell partnership targeting automotive insulation solutions and Kingspan’s USD 100 million acquisition to expand product portfolios.

- Regional Analysis: Asia-Pacific leads the global market with 38.5% share, supported by infrastructure expansion and government-led energy efficiency mandates. Meanwhile, North America and Western Europe remain mature markets driven by regulatory compliance, while Latin America and the Middle East emerge as new demand frontiers due to industrial growth and construction investments.

Type Analysis

Sheets and Films remain the anchor of the thin insulation landscape, accounting for 34.4% of global revenues in 2023. Their dominance into 2025 and beyond is underpinned by broad use in building envelopes, HVAC duct wraps, and industrial equipment where millimeter-level build-up is critical. Performance improvements—multi-layer laminates, infrared (IR) modifiers, and low-emissivity surfaces—are extending service life and improving R-values per millimeter, supporting code compliance without structural redesign.

Vacuum Insulation Panels (VIP) are the fastest-rising type, used in high-efficiency façades, commercial refrigeration, and cold-chain packaging. While still a smaller revenue base than Sheets and Films, VIP adoption is expected to outpace the overall market growth through 2033 thanks to ultra-low thermal conductivity (λ ≈ 0.004–0.008 W/m·K) and shrinking total cost of ownership. Coatings and Foils continue to gain share in retrofit settings; reflective foils boost thermal resistance in hot climates, while sprayable thin-film coatings enable coverage on irregular substrates. Foams (including advanced rigid and flexible formats) retain relevance where structural rigidity and acoustic damping are required, with hybrid systems (foam + foil) increasingly specified to balance thermal and moisture performance.

Materials Analysis

Aerogels led the materials mix with a 28.7% share in 2023, reflecting their superior thermal resistance at minimal thickness and favorable weight-to-performance ratio. From 2025 onward, continued price rationalization and process yields in silica aerogels are widening use in façades, process piping, EV battery packs, and aerospace cabins. Silica Aerogels, the largest aerogel sub-class, are benefiting from improved hydrophobicity and dust-suppression treatments, enhancing installation productivity and safety.

Metals (foils) are entrenched in radiant barrier applications and as facer layers that augment vapor control. Plastic Foams—notably XPS/EPS variants and emerging low-GWP formulations—remain pivotal in cost-sensitive builds and logistics, while Fiberglass persists as a workhorse where fire performance and acoustic attenuation are prioritized. Across materials, formulation shifts toward low-emission binders and circular inputs (recycled content, solvent-free coatings) are becoming specification requirements in public tenders and green-building certifications.

Thickness Range Analysis

The “Less Than 1 Inch” category led with 27.7% share in 2023, reflecting its suitability for space-constrained retrofits and assemblies where cladding depth, mass, or door/window clearances cannot be compromised. This range is central to urban refurbishments and transport platforms (rolling stock, EVs) where every millimeter affects weight and aerodynamics.

Thickness bands from “1 Inch to 2 Inches” and “2 Inches to 4 Inches” are widely used in commercial envelopes and industrial assets to meet stricter U-values without redesigning wall sections. “More Than 4 Inches” remains a smaller niche but is essential for deep-cold environments—cold rooms, LNG handling, and certain pharmaceutical logistics—where peak thermal performance and condensation control trump footprint concerns.

Installation Method Analysis

Spray Insulation held the lead with a 34.5% share in 2023, driven by its ability to eliminate thermal bypass via continuous coverage and gap filling. In 2025+, building codes that emphasize airtightness and moisture management sustain spray systems in both new build and complex retrofits, especially where geometric complexity penalizes board-based solutions.

Board Insulation retains strong traction in façades, roofs, and equipment housings due to consistent thickness, dimensional stability, and faster QA/QC on site. Batts and Rolls remain competitive in cost-controlled residential projects and selective commercial interiors, especially when installers seek familiar methods with predictable labor times. Blown-In Insulation continues to rise in occupied retrofits, filling cavities and attics with minimal disruption while immediately improving energy intensity per square meter.

Application Analysis

Building Thermal Insulation was the largest application at 37.5% share in 2023, supported by tightening energy performance standards and net-zero pathways. From 2025 onward, thin solutions are increasingly specified in envelope upgrades (over-cladding, interior retrofits) where maintaining usable floor area and façade lines is critical. Performance stack-ups—combining thin reflective layers, aerogel blankets, and vapor control—are becoming standard in high-performance retrofits.

Thermal Packaging is a notable growth pocket, propelled by cold-chain expansion in pharmaceuticals and perishables, along with last-mile delivery. VIP and aerogel-lined shippers are used to meet hold-time targets while reducing package weight. Wires and Cables leverage thin insulation for heat resistance and dielectric performance in EVs and data centers, while Pipe Coatings in oil, gas, and chemicals support process efficiency and personnel protection, with thin formats enabling rapid maintenance cycles and reduced downtime.

End User Analysis

Building and Construction remained the top end user with 35.6% share in 2023, as developers pursue energy-use intensity reductions and green certifications across commercial offices, healthcare, and multifamily. The 2025+ outlook points to accelerated retrofit demand in aging building stock, where thin assemblies enable compliance without major structural rework.

Automotive is growing on the back of EV platform proliferation, using thin insulation for battery thermal management, cabin NVH, and occupant comfort—areas where grams and millimeters matter. Aerospace specifies aerogel and advanced foils for cabin comfort and systems protection while preserving range through weight savings. In Oil and Gas, thin, high-performance wraps and coatings mitigate heat loss and corrosion under insulation (CUI), improving asset life and process stability, especially in brownfield upgrades where space is constrained.

Regional Analysis

Asia Pacific leads the global market with 38.5% share (≈USD 1.1 billion in 2023) and is poised to widen its lead through 2030+ as China, India, and Southeast Asia intensify urban housing programs and industrial capacity additions. Local manufacturing of films, foils, and aerogel blankets, combined with rising green-building mandates, underpins sustained demand.

North America remains a high-value market driven by deep retrofit programs, building code convergence toward lower U-values, and cold-chain investments. Europe sustains premium specifications via the Energy Performance of Buildings framework and decarbonization funding, with Northern and Western Europe emphasizing envelope upgrades in social housing and public buildings. Latin America and the Middle East & Africa are emerging growth corridors: Latin America benefits from modernization of commercial stock and cold-chain build-out, while GCC countries deploy thin, reflective, and hybrid systems to combat high solar loads and advance national energy-efficiency agendas.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Type

- Sheets and Films

- Vacuum Insulation Panels (VIP)

- Coatings

- Foils

- Foams

- Others

By Materials

- Aerogels

- Silica Aerogels

- Metals

- Plastic Foams

- Fiberglass

- Others

By Thickness Range

- Less Than 1 Inch

- 1 Inch to 2 Inches

- 2 Inches to 4 Inches

- More Than 4 Inches

By Installation Method

- Spray Insulation

- Board Insulation

- Batts and Rolls

- Blown-In Insulation

By Application

- Building Thermal Insulation

- Thermal Packaging

- Wires and Cables

- Pipe Coatings

- Others

By End User

- Automotive

- Aerospace

- Building and Construction

- Oil and Gas

- Others

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2024) | USD 5.2 B |

| Forecast Revenue (2034) | USD 10.1 B |

| CAGR (2024-2034) | 6.9% |

| Historical data | 2020-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Type (Sheets and Films, Vacuum Insulation Panels (VIP), Coatings, Foils, Foams, Others), By Materials (Aerogels, Silica Aerogels, Metals, Plastic Foams, Fiberglass, Others), By Thickness Range (Less Than 1 Inch, 1 Inch to 2 Inches, 2 Inches to 4 Inches, More Than 4 Inches), By Installation Method (Spray Insulation, Board Insulation, Batts and Rolls, Blown-In Insulation), By Application (Building Thermal Insulation, Thermal Packaging, Wires and Cables, Pipe Coatings, Others), By End User (Automotive, Aerospace, Building and Construction, Oil and Gas, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Kingspan Group, ContiTech AG, Rockwool Group, 3M, BNZ Materials, Inc., UNILIN Insulation, Owens Corning, Actis Insulation Ltd., Dow Chemical Company, Armacell International S.A., Huntsman International LLC, Saint-Gobain, BASF SE, Cabot Corporation, Celotax Saint Gobain, Johns Manville, A Berkshire Hathaway Company, Xtratherm |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, Coatings, Foils, Foams), By Materials (Aerogels, Silica Aerogels, Metals, Plastic Foams, Fiberglass), By Thickness Range (Less Than 1 Inch, 1 Inch to 2 Inches, 2 Inches to 4 Inches, More Than 4 Inches), By Installation Method, By Application , By End User, Energy Efficiency Regulations, Thermal Performance Trends & Forecast 2025–2034")

, Coatings, Foils, Foams), By Materials (Aerogels, Silica Aerogels, Metals, Plastic Foams, Fiberglass), By Thickness Range (Less Than 1 Inch, 1 Inch to 2 Inches, 2 Inches to 4 Inches, More Than 4 Inches), By Installation Method, By Application , By End User, Energy Efficiency Regulations, Thermal Performance Trends & Forecast 2025–2034")

, Coatings, Foils, Foams), By Materials (Aerogels, Silica Aerogels, Metals, Plastic Foams, Fiberglass), By Thickness Range (Less Than 1 Inch, 1 Inch to 2 Inches, 2 Inches to 4 Inches, More Than 4 Inches), By Installation Method, By Application , By End User, Energy Efficiency Regulations, Thermal Performance Trends & Forecast 2025–2034")

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date