- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Tokenized Real-World Assets Market Size, Share | CAGR 30.5%

Global Tokenized Real-World Assets Market Size, Share, Growth Analysis By Asset Class (Private Credit & Fixed Income, Real Estate, Equities & Funds, Commodities, Infrastructure Assets), By Blockchain Infrastructure (Public Permissioned, Private Permissioned, Hybrid, Layer 2 Networks), By Service Type (Issuance, Custody, Trading, Compliance), Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

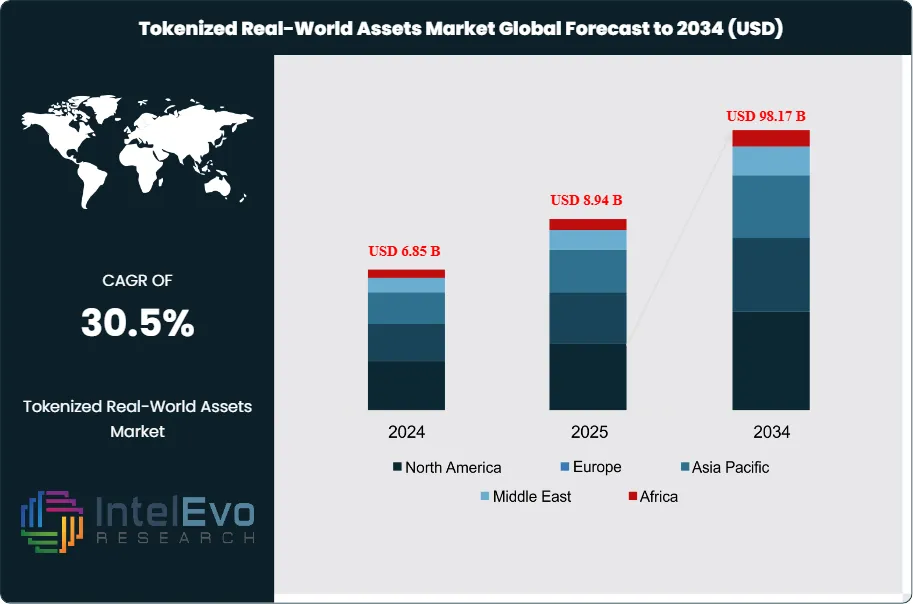

| USD 8.94 Billion | USD 98.17 Billion | 30.5% | North America, 41.3% |

The Tokenized Real-World Assets Market was valued at approximately USD 6.85 Billion in 2024 and reached USD 8.94 Billion in 2025. The market is projected to grow to USD 98.17 Billion by 2034, expanding at a CAGR of 30.5% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 89.23 Billion over the analysis period, establishing Tokenized Real-World Assets as one of the most transformative and rapidly scaling categories within the global financial technology and digital asset ecosystem.

Get More Information about this report -

Request Free Sample ReportTokenized Real-World Assets refers to the process of representing ownership rights to tangible and traditional financial assets, including real estate, private credit, government and corporate bonds, commodities, private equity, and infrastructure, as digital tokens issued on public or permissioned blockchain networks. Each token embeds ownership data, transfer rules, compliance logic, and economic rights directly in programmable smart contracts, enabling assets that historically required days, weeks, or months to settle, transfer, and administer to be managed with near-instant settlement finality, automated dividend and coupon distributions, and 24-hour global secondary market accessibility. The addressable asset universe for tokenization is vast: global real estate alone is estimated at USD 330 Trillion by the Bank for International Settlements, global bond markets exceed USD 130 Trillion, and private markets including private equity, private credit, and infrastructure represent a further USD 15 Trillion in assets under management as of 2025. Even fractional penetration of these markets generates enormous tokenization platform revenue.

Three structural shifts are accelerating market growth across the forecast period. First, institutional capital is entering the tokenized asset market at scale following years of regulatory uncertainty. BlackRock's BUIDL tokenized money market fund, launched on Ethereum in March 2024 and reaching USD 520 Million in assets within six months, demonstrated that the world's largest asset manager views blockchain settlement as a viable and superior operational infrastructure for fund administration. Franklin Templeton, Fidelity, and State Street have each launched tokenized fund products, signaling institutional validation that is accelerating adoption across the asset management industry. Second, regulatory clarity is improving in key jurisdictions. The European Union's Markets in Crypto-Assets Regulation (MiCA) and the EU's DLT Pilot Regime, which allows securities settlement on blockchain infrastructure, are providing the legal framework for institutional tokenized asset issuance and trading. The SEC's evolving guidance on digital asset securities and the OCC's interpretive letters permitting national banks to use blockchain for asset settlement are creating comparable clarity in the U.S. market. Third, blockchain infrastructure has matured sufficiently to support institutional settlement requirements, with Ethereum Layer 2 networks achieving transaction throughput exceeding 10,000 transactions per second, Ethereum mainnet settlement finality below 15 seconds, and enterprise-grade KYC and AML compliance modules embedded directly in permissioned token smart contracts.

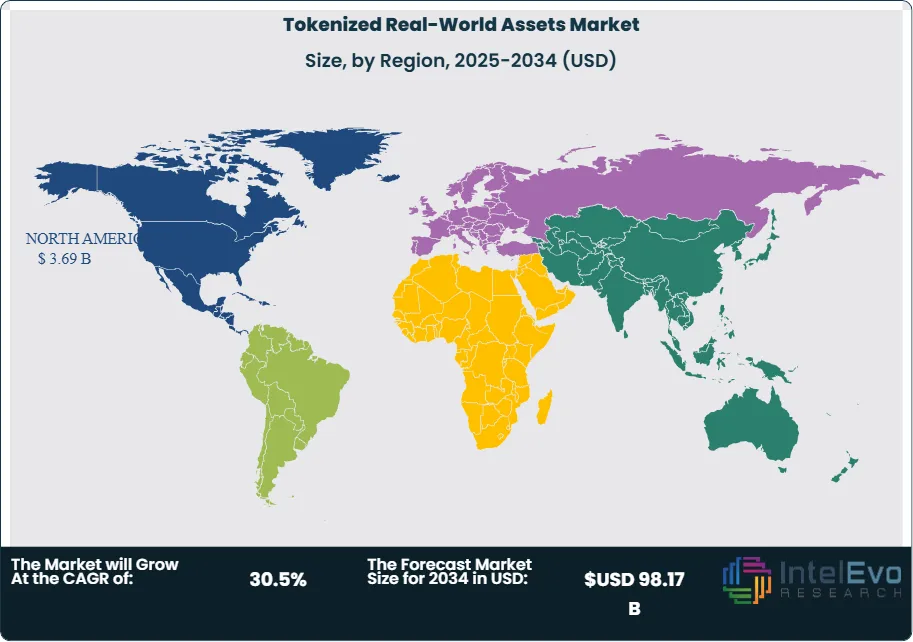

North America leads global market revenue at 41.3% in 2025, approximately USD 3.69 Billion, driven by the concentration of global asset management, capital markets infrastructure, and blockchain technology development in the United States. Europe holds a 28.6% share, supported by MiCA regulatory clarity, the DLT Pilot Regime, and active tokenized bond issuance by the European Investment Bank and major German and French financial institutions. Asia Pacific accounted for 20.4% of global Tokenized Real-World Assets revenue in 2025, with Singapore's MAS Project Guardian, Japan's FSA digital securities framework, and Hong Kong's tokenized green bond program as leading institutional market developments. Competitive intensity is rising sharply as traditional financial institutions, blockchain infrastructure providers, and specialized tokenization platforms compete for control of the issuance, custody, and secondary market trading layers of the tokenized asset value chain.

, By Blockchain Infrastructure (Public Permissioned, Private Permissioned, Hybrid, Layer 2 Networks), By Service Type (Issuance, Custody, Trading, Compliance), Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global Tokenized Real-World Assets market reached USD 8.94 Billion in 2025 and is forecast to reach USD 98.17 Billion by 2034, expanding at a CAGR of 30.5% over the 2026–2034 forecast period.

- Segment Dominance: By asset class, tokenized private credit and fixed income held the largest segment share at 38.4% of global market revenue in 2025, driven by institutional demand for yield-bearing on-chain assets, the operational efficiency of automated coupon payments via smart contracts, and the rapid growth of on-chain lending protocols secured by tokenized loan portfolios.

- Segment Dominance: By end-user, institutional investors including asset managers, banks, insurance companies, and sovereign wealth funds represented the largest demand segment at 61.7% of global market revenue in 2025, reflecting the concentration of tokenization activity in wholesale capital markets and regulated fund structures ahead of retail investor market development.

- Driver: Institutional adoption by BlackRock, Franklin Templeton, Fidelity, and JPMorgan Chase is the primary demand-side catalyst, with the combined AUM of tokenized fund products from major asset managers surpassing USD 2.3 Billion by mid-2025 and demonstrating that blockchain-based fund administration reduces operational costs by 30–50% versus traditional transfer agent and custodian infrastructure.

- Restraint: Regulatory fragmentation across jurisdictions, with materially different legal treatments of tokenized securities under U.S. securities law, EU MiCA, Singapore MAS frameworks, and the laws of 140-plus other countries, creates cross-border issuance complexity that increases legal and compliance costs by an estimated 20–35% versus single-jurisdiction tokenized asset programs.

- Opportunity: Tokenization of private market assets, including private equity fund interests, infrastructure debt, and real estate limited partnership stakes, represents the largest near-term addressable expansion, with the USD 15 Trillion private markets universe currently accessible only to institutional investors due to high minimum investment sizes and illiquid secondary markets that tokenization directly addresses.

- Trend: The convergence of tokenized assets with decentralized finance (DeFi) protocols, enabling institutional-grade real-world asset collateral to support on-chain lending, yield generation, and structured product creation, is the dominant 2025 market trend, with tokenized U.S. Treasury products deployed as DeFi collateral exceeding USD 1.8 Billion in total value locked by mid-2025.

- Regional Analysis: North America leads the global Tokenized Real-World Assets market with a 41.3% share in 2025, representing approximately USD 3.69 Billion, anchored by BlackRock BUIDL, Franklin Templeton FOBXX, and JPMorgan's Onyx digital assets platform driving institutional tokenized fund and bond adoption.

Competitive Landscape Overview

The global Tokenized Real-World Assets market is moderately fragmented across its issuance, custody, and trading layers, with no single vendor holding dominant positions across all three. At the issuance layer, the top four platform providers, Securitize, Tokeny Solutions, Polymath, and Fireblocks, collectively account for approximately 34.2% of tokenized asset issuance platform revenue in 2025. Traditional financial institutions including BlackRock, JPMorgan (Onyx), and Citigroup have built proprietary tokenization infrastructure for internal and client use, competing with specialist platforms at the institutional tier. Competition is driven by regulatory compliance coverage, supported blockchain network breadth, integration with traditional financial system custodians and transfer agents, and the depth of secondary liquidity provision. M&A activity accelerated sharply in 2024–2025, with digital asset custodians acquiring compliance technology firms, traditional prime brokers acquiring tokenized asset marketplace operators, and blockchain infrastructure companies purchasing regulatory technology specialists to assemble end-to-end tokenization stacks.

Competitive Landscape Matrix

| Company | HQ Country | Market Position | Key Product / Platform | Geographic Strength | Recent Strategic Move (2024–2026) |

| Securitize | USA | Leader | Securitize Capital Tokenization Platform | North America / Europe | Acquired Onramp Invest digital asset portfolio platform; processed USD 1.1B in tokenized security issuance including BlackRock BUIDL custody (Jan 2025). |

| Fireblocks | USA | Leader | Fireblocks Digital Asset Platform | North America / Europe | Launched Fireblocks Tokenization Suite with MiCA-compliant issuance templates; onboarded 30 European bank clients for tokenized bond settlement (Mar 2025). |

| Tokeny Solutions | Luxembourg | Leader | Tokeny T-REX Protocol | Europe | Deployed T-REX ERC-3643 compliance layer for 18 EU tokenized securities issuances; certified as MiCA-compliant issuance infrastructure by BaFin (Dec 2024). |

| Ondo Finance | USA | Leader | Ondo USDY / OUSG Tokenized Treasuries | North America / Asia Pacific | OUSG tokenized U.S. Treasury product surpassed USD 600M AUM; launched Ondo Global Markets for cross-chain tokenized security distribution (Sep 2025). |

| JPMorgan (Onyx) | USA | Challenger | JPMorgan Onyx Digital Assets | North America / Asia Pacific | Processed USD 1.5T in repo transactions on Onyx blockchain; launched tokenized collateral network with Goldman Sachs and BNP Paribas (Apr 2025). |

| Franklin Templeton | USA | Challenger | FOBXX Tokenized Money Market Fund | North America / Europe | FOBXX reached USD 420M AUM on Stellar and Polygon networks; launched tokenized fixed income fund for European institutional investors (Jun 2025). |

| Centrifuge | USA | Challenger | Centrifuge RWA Protocol | North America / Europe | Surpassed USD 500M in tokenized real-world asset pools including trade receivables and real estate debt; integrated with MakerDAO and Aave (Oct 2025). |

| Backed Finance | Switzerland | Niche Player | bTokens Tokenized Securities | Europe / Asia Pacific | Launched tokenized equity products covering S&P 500 and EURO STOXX components under Swiss DLT Act framework; distributed via 8 digital asset exchanges (Jan 2026). |

| RealT | USA | Niche Player | RealT Tokenized Real Estate | North America | Expanded tokenized U.S. residential real estate portfolio to 1,200 properties with USD 120M total tokenized value; launched secondary market on Gnosis Chain (Feb 2026). |

By Asset Class:

Private credit and fixed income represent the dominant asset class in the global Tokenized Real-World Assets market, accounting for 38.4% of revenue in 2025, approximately USD 3.43 Billion. This category encompasses tokenized government bonds, corporate bonds, money market funds, private credit loan pools, and trade receivables. Tokenized fixed income has achieved the fastest institutional adoption of any real-world asset class because bond cash flows, including coupon payments and principal repayment, map cleanly onto smart contract automation without the legal complexity of representing physical asset ownership on-chain. The European Investment Bank has issued multiple tokenized bonds on public blockchain infrastructure since 2021, including a EUR 100 Million digital bond on Ethereum in 2023, demonstrating sovereign-grade institutional comfort with DLT settlement for fixed income. Tokenized money market funds from BlackRock (BUIDL) and Franklin Templeton (FOBXX) have attracted the largest institutional AUM in the tokenized fund category, with combined assets exceeding USD 940 Million by mid-2025. On-chain private credit, where loan portfolios originated by specialist credit managers are tokenized and funded by DeFi protocol liquidity, represents the fastest-growing sub-segment within fixed income, with platforms including Centrifuge, Maple Finance, and Goldfinch processing over USD 2.8 Billion in cumulative tokenized loan origination by 2025.

Real estate tokenization accounted for 26.7% of the Tokenized Real-World Assets in 2025, approximately USD 2.39 Billion, encompassing fractional ownership tokens in commercial and residential properties, tokenized real estate investment trust interests, and tokenized mortgage-backed debt instruments. Real estate is the most intuitive asset class for tokenization from a democratization perspective, as fractionalization allows investors to acquire USD 50–USD 500 fractional interests in properties that would otherwise require USD 100,000-plus minimum investments, opening the asset class to retail and semi-institutional investor segments. Platforms including RealT, Lofty AI, and Propertize operate retail-facing real estate tokenization marketplaces in the United States, while institutional platforms including Paxos and Securitize manage larger commercial real estate tokenization programs. Equities and fund interests held a 17.8% share, covering tokenized private equity fund LP interests, tokenized public equity exposure through products like Backed Finance's bTokens, and tokenized hedge fund shares. Commodities represented 10.2% of the market, primarily tokenized gold, silver, and oil, with Paxos Gold (PAXG) and Tether Gold (XAUT) the leading tokenized commodity products. Infrastructure and other alternatives accounted for the remaining 6.9%.

By Blockchain Infrastructure:

Public permissioned blockchain networks, where the underlying blockchain is publicly verifiable but token transfers require KYC and compliance approvals embedded in smart contract logic, represent the dominant infrastructure choice for institutional Tokenized Real-World Assets implementations at 44.6% of platform revenue in 2025. Ethereum's ERC-3643 (T-REX) standard, developed by Tokeny Solutions and adopted by the EU's DLT Pilot Regime as a reference implementation, embeds investor identity verification and transfer restriction logic directly into the token contract, enabling regulatory-compliant secondary market trading on public blockchain infrastructure while maintaining investor access controls. Tokenized assets on Ethereum have the broadest DeFi integration potential, enabling institutional tokenized bonds to be used as collateral in lending protocols and as liquidity in automated market makers. Private permissioned blockchains, including Hyperledger Fabric, R3 Corda, and Quorum, held a 28.3% share in 2025, primarily used by banking consortia and central bank digital currency pilots where transaction privacy between participants is a regulatory requirement. Hybrid architectures, where assets are issued on private chains with settlement finality anchored to public blockchains, accounted for 16.4%, and Layer 2 networks including Polygon, Arbitrum, and Base held the remaining 10.7%, growing rapidly as gas cost reductions make high-frequency token transfers economically viable.

By End-User:

Institutional investors including asset managers, banks, insurance companies, pension funds, and sovereign wealth funds represented the dominant end-user category in the Tokenized Real-World Assets at 61.7% of global revenue in 2025, approximately USD 5.52 Billion. Institutional adoption is concentrated in tokenized money market funds and fixed income, where operational cost reductions from blockchain settlement are most quantifiable, and in private market asset tokenization where improved secondary liquidity creates portfolio management value. BlackRock's BUIDL fund, which uses tokenized fund shares for real-time institutional settlement at USD 1 minimum share size versus T+1 conventional fund settlement, has demonstrated that blockchain-based fund administration reduces NAV calculation and transfer agent costs by an estimated 30–50% at scale. Retail and wealth management end-users accounted for 24.8% of market revenue, concentrated in real estate tokenization platforms and tokenized commodities where retail investor democratization of alternative assets is the primary value proposition. Issuers and corporates, including companies tokenizing their own equity or debt and real estate operators tokenizing property portfolios, represented the remaining 13.5%.

By Service Type:

Issuance and tokenization services held the largest revenue share at 35.2% of the Tokenized Real-World Assets in 2025, approximately USD 3.15 Billion, encompassing the technical and legal services required to structure, create, and distribute tokenized asset smart contracts. Issuance platform providers including Securitize, Fireblocks, and Tokeny charge issuers platform fees of 0.5–1.5% of issuance value for primary tokenization services, plus ongoing annual administration fees. Custody and settlement services accounted for 27.4% of revenue, reflecting the critical role of digital asset custodians including Anchorage Digital, BitGo, and Coinbase Custody in providing qualified custody for tokenized securities under SEC and OCC regulatory frameworks. Trading and liquidity services, covering tokenized asset secondary market exchanges, OTC desks, and automated market maker liquidity provision, held a 22.8% share. Compliance and regulatory technology, including KYC/AML token compliance modules, securities law mapping engines, and cross-border regulatory reporting, represented 14.6% and is growing at the highest rate within the service mix at approximately 38% annually as multi-jurisdiction tokenized asset programs generate complex compliance requirements.

Regional Analysis

North America

North America leads the global Tokenized Real-World Assets market with a 41.3% share in 2025, representing approximately USD 3.69 Billion, anchored by the concentration of global asset management, capital markets infrastructure, and blockchain technology development in the United States. The U.S. market has been defined by institutional adoption from major asset managers: BlackRock's BUIDL tokenized money market fund reached USD 520 Million in AUM within six months of its March 2024 launch, Franklin Templeton's FOBXX money market fund on Stellar and Polygon exceeded USD 420 Million in AUM, and JPMorgan's Onyx blockchain platform processed USD 1.5 Trillion in cumulative repo transactions by early 2025. The Securities and Exchange Commission's evolving approach to digital asset securities, including the withdrawal of Staff Accounting Bulletin 121 in 2025 allowing banks to custody digital assets without punitive capital treatment, has materially improved the institutional feasibility of tokenized securities programs. The Office of the Comptroller of the Currency's interpretive letters confirming that national banks may use blockchain infrastructure for payment and settlement functions provide regulatory legitimacy for bank-operated tokenization platforms. The Depository Trust and Clearing Corporation has initiated a blockchain settlement pilot for U.S. equity tokenization under its DTCC Digital Launchpad program, with the potential to bring blockchain settlement to the USD 85 Trillion annual U.S. equity settlement market. Canada's tokenized asset market is developing through the Ontario Securities Commission's regulatory sandbox, with tokenized real estate and private equity fund platforms gaining regulatory approvals in Toronto's financial district.

Europe

Europe accounted for 28.6% of the global Tokenized Real-World Assets market in 2025, approximately USD 2.56 Billion, benefiting from the world's most advanced regulatory framework for tokenized securities through the EU's DLT Pilot Regime and MiCA regulation. The DLT Pilot Regime, operational from March 2023, allows securities settlement on distributed ledger technology infrastructure under a structured exemption from traditional securities law requirements, with a EUR 6 Billion per security and EUR 9 Billion total AUM cap for pilot participants. European Investment Bank digital bond issuances on Ethereum have been the most prominent institutional tokenized fixed income transactions in the EU, each demonstrating seamless cross-border settlement between French and German institutional investors. Germany's BaFin has approved multiple tokenized securities issuers under the Electronic Securities Act (eWpG), which came into effect in 2021 and allows fully electronic, registration-free securities issuance on DLT infrastructure, creating the legal foundation for Germany's growing tokenized bond and fund market. Luxembourg's fund domicile infrastructure, which serves 28% of global UCITS fund assets, is being adapted for tokenized fund share classes, with ALFI (Association of the Luxembourg Fund Industry) publishing tokenized fund operational guidelines. Switzerland's DLT Act, effective January 2021, provides the most permissive regulatory environment for tokenized securities in Europe, enabling Backed Finance and other Swiss-based issuers to tokenize traditional securities for global distribution under a coherent legal framework. The UK's Financial Conduct Authority's Digital Securities Sandbox provides a structured path for tokenized securities innovation within the UK regulatory perimeter post-Brexit.

Asia Pacific

Asia Pacific represented 20.4% of the global Tokenized Real-World Assets market in 2025, approximately USD 1.82 Billion, with Singapore, Japan, Hong Kong, and Australia as the primary institutional tokenized asset markets. Singapore's Monetary Authority of Singapore Project Guardian, a public-private industry initiative, has produced the most comprehensive institutional tokenization pilots globally, covering tokenized bonds, tokenized fund distribution, FX settlement on-chain, and tokenized trade finance across 24 financial institution participants including DBS Bank, Standard Chartered, Citibank, and HSBC. MAS's Variable Capital Company structure, purpose-designed for digital fund vehicles, and MAS's recognized market operator license for digital securities exchanges provide Singapore's tokenized asset market with institutional-grade regulatory infrastructure. Japan's Financial Services Agency digital securities framework, operating under the Financial Instruments and Exchange Act amendments that recognize blockchain-recorded securities as legally valid, has enabled Nomura Holdings' Laser Digital subsidiary and SBI Digital Asset Holdings to issue and trade tokenized bonds and funds within Japan's regulated financial system. Hong Kong's Securities and Futures Commission issued tokenized green bonds for the Hong Kong government in 2023 and 2024 and approved virtual asset trading platform licenses for tokenized security secondary markets, positioning Hong Kong as the primary institutional tokenized asset hub in Chinese-speaking markets. Australia's ASX digital asset infrastructure project and Reserve Bank of Australia CBDC pilot have laid groundwork for tokenized securities settlement integration with Australia's national equity market infrastructure.

Latin America

Latin America held a 5.2% share of the global Tokenized Real-World Assets market in 2025, approximately USD 465 Million, with Brazil emerging as the most active regional market due to its large capital market, fintech-friendly regulatory environment, and high retail investor participation in digital assets. Brazil's Comissao de Valores Mobiliarios (CVM) issued Resolution 175 in 2022 establishing a regulatory framework for investment fund tokenization, and Brazilian asset managers including XP Investimentos, BTG Pactual, and Itau Unibanco have launched tokenized real estate funds, private credit funds, and commodity-backed tokens accessible to retail investors through digital platforms. BTG Pactual's tokenized gold product and XP's tokenized real estate certificates have collectively attracted over USD 180 Million in retail investment by 2025, demonstrating the appetite for tokenized alternatives among Brazilian retail investors who hold USD 1.1 Trillion in financial assets. Mexico's CNBV and Colombia's Superfinanciera are at earlier regulatory development stages for tokenized securities, with sandbox programs underway. Argentina's macro-economic instability has paradoxically accelerated adoption of tokenized USD-denominated assets as a store of value and capital preservation instrument among high-net-worth investors.

Middle East & Africa

The Middle East and Africa region accounted for 4.5% of the global Tokenized Real-World Assets market in 2025, approximately USD 402 Million, with the UAE, Saudi Arabia, and South Africa as the primary active markets. The UAE's financial free zones, particularly the Abu Dhabi Global Market (ADGM) and Dubai International Financial Centre (DIFC), have established tokenized securities regulatory frameworks that attract global issuers seeking Middle East distribution access. ADGM's Digital Securities framework and DFSA's digital asset token regime in DIFC provide regulated pathways for tokenized fund and bond issuance, and the Abu Dhabi Investment Authority has disclosed exploratory interest in tokenized private market asset holdings for portfolio liquidity management. Saudi Arabia's Capital Market Authority has initiated a fintech regulatory sandbox that includes digital asset securities provisions, aligned with Vision 2030's financial sector modernization objectives. South Africa's Financial Sector Conduct Authority and Prudential Authority have jointly published guidance on digital asset securities that creates a pathway for tokenized securities issuance, with Johannesburg Stock Exchange initiating a blockchain settlement pilot for domestic equity transactions. The broader African market opportunity in tokenized assets is concentrated in remittance-backed tokenized instruments and agricultural commodity tokens that address capital market access gaps for smallholder producers and SME borrowers.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Asset Class

- Private Credit and Fixed Income (Government Bonds, Corporate Bonds, Money Market Funds, Private Credit)

- Real Estate (Commercial, Residential, REITs, Mortgage-Backed Instruments)

- Equities and Funds (Private Equity LP Interests, Tokenized Public Equity, Hedge Fund Shares)

- Commodities (Gold, Silver, Oil, Agricultural Commodities)

- Infrastructure and Other Alternatives

By Blockchain Infrastructure

- Public Permissioned (Ethereum ERC-3643, Stellar, Polygon)

- Private Permissioned (Hyperledger Fabric, R3 Corda, Quorum)

- Hybrid (Private Issuance with Public Anchoring)

- Layer 2 Networks (Arbitrum, Base, Optimism)

By End-User

- Institutional Investors (Asset Managers, Banks, Insurance, Pension, Sovereign Wealth Funds)

- Retail and Wealth Management

- Issuers and Corporates

By Service Type

- Issuance and Tokenization

- Custody and Settlement

- Trading and Liquidity

- Compliance and Regulatory Technology

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 8.94 B |

| Forecast Revenue (2034) | USD 98.17 B |

| CAGR (2025-2034) | 30.5% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Asset Class, (Private Credit and Fixed Income (Government Bonds, Corporate Bonds, Money Market Funds, Private Credit), Real Estate (Commercial, Residential, REITs, Mortgage-Backed Instruments), Equities and Funds (Private Equity LP Interests, Tokenized Public Equity, Hedge Fund Shares), Commodities (Gold, Silver, Oil, Agricultural Commodities), Infrastructure and Other Alternatives), By Blockchain Infrastructure, (Public Permissioned (Ethereum ERC-3643, Stellar, Polygon), Private Permissioned (Hyperledger Fabric, R3 Corda, Quorum), Hybrid (Private Issuance with Public Anchoring), Layer 2 Networks (Arbitrum, Base, Optimism)), By End-User, (Institutional Investors (Asset Managers, Banks, Insurance, Pension, Sovereign Wealth Funds), Retail and Wealth Management, Issuers and Corporates), By Service Type, (Issuance and Tokenization, Custody and Settlement, Trading and Liquidity, Compliance and Regulatory Technology) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | SECURITIZE, FIREBLOCKS, ONDO FINANCE, JPMORGAN (ONYX DIGITAL ASSETS), TOKENY SOLUTIONS, FRANKLIN TEMPLETON (FOBXX), BLACKROCK (BUIDL), CENTRIFUGE, BACKED FINANCE, REALTOKEN (REALT), POLYMATH NETWORK, MAPLE FINANCE, GOLDFINCH PROTOCOL, ANCHORAGE DIGITAL, BITGO (INSTITUTIONAL TOKENIZATION), PAXOS (PAXG, TOKENIZED COMMODITIES), SUPERSTATE, HAMILTON LANE (TOKENIZED PRIVATE EQUITY), Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Blockchain Infrastructure (Public Permissioned, Private Permissioned, Hybrid, Layer 2 Networks), By Service Type (Issuance, Custody, Trading, Compliance), Industry Trends & Forecast 2026-2034")

, By Blockchain Infrastructure (Public Permissioned, Private Permissioned, Hybrid, Layer 2 Networks), By Service Type (Issuance, Custody, Trading, Compliance), Industry Trends & Forecast 2026-2034")

, By Blockchain Infrastructure (Public Permissioned, Private Permissioned, Hybrid, Layer 2 Networks), By Service Type (Issuance, Custody, Trading, Compliance), Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Tokenized Real-World Assets Market?

The Global Tokenized Real-World Assets Market was valued at USD 6.85 Billion in 2024 and is projected to reach USD 98.17 Billion by 2034, growing at a CAGR of 30.5% from 2026 to 2034, driven by rising adoption of blockchain-based asset tokenization platforms, increasing demand for fractional ownership, expanding institutional participation in digital assets, and growing integration of tokenized securities across banking, wealth management, and decentralized finance ecosystems worldwide.

Who are the major players in the Tokenized Real-World Assets Market?

SECURITIZE, FIREBLOCKS, ONDO FINANCE, JPMORGAN (ONYX DIGITAL ASSETS), TOKENY SOLUTIONS, FRANKLIN TEMPLETON (FOBXX), BLACKROCK (BUIDL), CENTRIFUGE, BACKED FINANCE, REALTOKEN (REALT), POLYMATH NETWORK, MAPLE FINANCE, GOLDFINCH PROTOCOL, ANCHORAGE DIGITAL, BITGO (INSTITUTIONAL TOKENIZATION), PAXOS (PAXG, TOKENIZED COMMODITIES), SUPERSTATE, HAMILTON LANE (TOKENIZED PRIVATE EQUITY), Others

Which segments covered the Tokenized Real-World Assets Market?

By Asset Class, (Private Credit and Fixed Income (Government Bonds, Corporate Bonds, Money Market Funds, Private Credit), Real Estate (Commercial, Residential, REITs, Mortgage-Backed Instruments), Equities and Funds (Private Equity LP Interests, Tokenized Public Equity, Hedge Fund Shares), Commodities (Gold, Silver, Oil, Agricultural Commodities), Infrastructure and Other Alternatives), By Blockchain Infrastructure, (Public Permissioned (Ethereum ERC-3643, Stellar, Polygon), Private Permissioned (Hyperledger Fabric, R3 Corda, Quorum), Hybrid (Private Issuance with Public Anchoring), Layer 2 Networks (Arbitrum, Base, Optimism)), By End-User, (Institutional Investors (Asset Managers, Banks, Insurance, Pension, Sovereign Wealth Funds), Retail and Wealth Management, Issuers and Corporates), By Service Type, (Issuance and Tokenization, Custody and Settlement, Trading and Liquidity, Compliance and Regulatory Technology)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Tokenized Real-World Assets Market

Published Date : 25 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date