- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

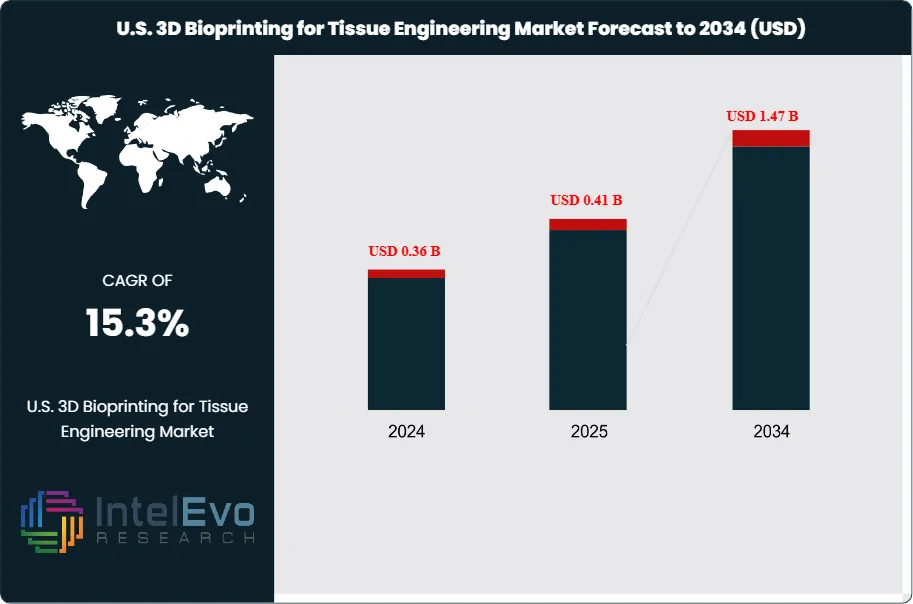

U.S. 3D Bioprinting for Tissue Engineering Market Size | CAGR of 15.3%

U.S. 3D Bioprinting for Tissue Engineering Market Size, Share, Analysis By Technology (Extrusion, Inkjet, Laser-Assisted, SLA, DLP), By Bioink (Natural, Synthetic, Hybrid, dECM-Based), By Application (Regenerative Medicine, Drug Discovery, Organ Transplantation, Disease Modeling), By End-User (Research, Pharma & Biotech, Hospitals, CROs) Region, Key Players – Dynamics, Advanced Regenerative Medicine & Biomaterials Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

| USD 0.41 Billion | USD 1.47 Billion | 15.3% | Northeast U.S., 38.5% |

The U.S. 3D Bioprinting for Tissue Engineering Market was valued at USD 0.36 Billion in 2024 and USD 0.41 Billion in 2025, and is expected to reach USD 1.47 Billion by 2034, growing at a CAGR of 15.3% during the forecast period from 2026 to 2034. The increasing adoption of regenerative medicine, rising demand for advanced tissue models, and growing investments in biotechnology research are driving the expansion of the U.S. 3D bioprinting for tissue engineering market. The market is witnessing rapid innovation in bioink materials, bioprinting technologies, and personalized healthcare solutions, creating significant opportunities across drug discovery, tissue regeneration, precision medicine, and organ engineering applications.

Get More Information about this report -

Request Free Sample ReportThe 3D bioprinting for tissue engineering market sits at the intersection of additive manufacturing, regenerative medicine, and biomaterials science. The market encompasses bioprinters, bioinks (hydrogels, decellularized extracellular matrix, recombinant collagen), software, and contract bioprinting services applied to fabricate functional tissue constructs for transplantation, drug screening, disease modeling, and surgical planning. Clinical translation accelerated when the FDA approved Humacyte's Symvess (acellular tissue engineered vessel) on December 19, 2024 for extremity arterial injury, with commercial launch on February 26, 2025 at USD 29,500 per unit. Symvess became the first FDA-approved bioengineered human tissue conduit and validated regulatory pathways for engineered tissue products.

Regulatory anchors are concentrated under the FDA's Center for Biologics Evaluation and Research (CBER), which administers Regenerative Medicine Advanced Therapy (RMAT) designation under Section 3033 of the 21st Century Cures Act. Symvess received RMAT designation in May 2023 prior to BLA filing in December 2023 and Priority Review in February 2024. The European Medicines Agency reviews bioprinted tissue products under the Advanced Therapy Medicinal Products (ATMP) framework. Japan's PMDA, China's NMPA, India's CDSCO, and the UK's MHRA align with ICH guidelines on cell and tissue therapy quality. ISO 23556 governs additive manufacturing of medical devices. The FDA Modernization Act 2.0 increasing acceptance of non-animal models supports adoption of bioprinted tissues for preclinical toxicology.

Technology innovation is bifurcating between extrusion-based platforms and light-based platforms. Extrusion-based bioprinting (CELLINK BIO X, BIO X6, Aspect Biosystems RX1) offers material versatility and cost-effectiveness, while light-based DLP and stereolithography systems (CELLINK BIONOVA X, 3D Systems' Print to Perfusion, Readily3D volumetric printing) deliver 10 to 50 micrometer resolution suited for vascularized constructs. Aspect Biosystems' microfluidic bioprinting and Wyss Institute's SWIFT technology enable perfusable channels essential for thick-tissue viability. AI-driven process control entered the field with the September 2025 MIT-Polimi monitoring platform for embedded bioprinting and the Wyss Institute's January 30, 2026 publication on engineering kidney collecting duct systems.

Regionally, North America held 41.5% revenue share in the 3D bioprinting for tissue engineering market in 2025, anchored by FDA approvals, NIH and ARPA-H funding (the University of Texas Southwestern Medical Center received a USD 25 Million ARPA-H grant for the VITAL project in January 2026 to develop bioprinted artificial livers), and concentrated venture activity in Vancouver, Boston, San Diego, and Cambridge. Asia Pacific captured 26.8% share with Japan, China, South Korea, and India as principal innovation centers. Outlook through 2034 hinges on additional RMAT approvals for tissue-engineered grafts, GMP-scale bioprinter deployment in hospital settings, and the maturation of vascularized organoid programs at the Wyss Institute, Wake Forest Institute for Regenerative Medicine, and academic medical centers.

Market Definition and Scope

The 3D bioprinting for tissue engineering market is defined as the segment of additive manufacturing dedicated to the layer-by-layer fabrication of functional tissue constructs using cells, biomaterials, and bioinks for clinical, preclinical, and research applications. The market encompasses bioprinter hardware (extrusion, inkjet, laser-assisted, stereolithography, DLP, and microfluidic platforms), bioinks (hydrogels, decellularized extracellular matrix, recombinant collagen, alginate, GelMA), bioprinting software, and contract bioprinting services applied to skin, cartilage, bone, vascular, hepatic, renal, neural, and pancreatic tissue construction.

This analysis covers tissue-engineering applications including regenerative medicine implants, in vitro disease models, drug toxicity screening, organ-on-chip systems, surgical training models, and pre-transplantation tissue conditioning. It includes products from CELLINK (BICO Group), 3D Systems Corporation, Aspect Biosystems, Humacyte, Organovo, Stratasys, ROKIT Healthcare, Poietis, and CollPlant Biotechnologies. Excluded from this scope are non-bioprinting tissue engineering scaffolds (electrospun, freeze-dried), pure cell therapy without printing, traditional 3D printed surgical guides without living cells, and food technology applications such as cultured meat. The parent global 3D bioprinting market, including non-tissue applications, reached approximately USD 2.91 Billion in 2025; tissue engineering represented approximately 37.8% of that parent.

, By Bioink (Natural, Synthetic, Hybrid, dECM-Based), By Application (Regenerative Medicine, Drug Discovery, Organ Transplantation, Disease Modeling), By End-User (Research, Pharma & Biotech, Hospitals, CROs) Region, Key Players – Dynamics, Advanced Regenerative Medicine & Biomaterials Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The 3D bioprinting for tissue engineering market expanded from USD 1.10 Billion in 2025 toward a projected USD 3.95 Billion by 2034, registering a CAGR of 15.3% during the forecast period.

- Segment Dominance by Technology: Extrusion-based bioprinting captured approximately 42.8% share in 2025 due to its compatibility with diverse bioinks and cost-effectiveness, while DLP and stereolithography systems (such as CELLINK BIONOVA X) grew at 20.0% CAGR.

- Segment Dominance by Application: Regenerative medicine and tissue regeneration represented 32.0% of platform value in 2025, while drug testing and disease modeling applications grew at 17.9% CAGR projected through 2030.

- Driver: The FDA approval of Humacyte's Symvess on December 19, 2024 for extremity arterial injury, priced at USD 29,500 per unit, established the first commercial regulatory pathway for engineered tissue conduits and validated long-cycle BLA review economics.

- Restraint: Vascularization of constructs thicker than 200 micrometers remains technically constrained, with cell viability dropping below 60% in non-perfused thick tissues, requiring SWIFT-class perfusion or microfluidic channel printing that adds USD 50,000 to USD 150,000 to per-construct manufacturing cost.

- Opportunity: Bioprinted islet tissue therapeutics for Type 1 diabetes represent an addressable opportunity exceeding USD 8 Billion in source-injectable insulin economics, validated by Aspect Biosystems' USD 280 Million Government of Canada project announced April 2, 2026.

- Trend: AI-enabled real-time process monitoring entered standard practice in September 2025 through the MIT-Polimi modular monitoring platform published in journal Device, supporting reproducibility for clinical-grade bioprinting.

- Regional: North America held the largest regional share at 41.5%, equating to approximately USD 457 Million in 2025, with the United States contributing the bulk via FDA RMAT designations and concentrated NIH and ARPA-H funding.

Key Insights Summary

- Symvess (acellular tissue engineered vessel-tyod) from Humacyte became the first engineered vascular conduit to receive FDA approval, with the agency clearing the product for extremity arterial injury on December 19, 2024; commercial sales opened on February 26, 2025 at a per-unit list price of USD 29,500, and a New Technology Add-on Payment application was filed with CMS in October 2024.

- Aspect Biosystems disclosed on April 2, 2026 a USD 79 Million Government of Canada investment via the Strategic Response Fund, with the funding anchoring a USD 280 Million multi-year initiative aimed at advancing bioprinted cellular therapeutics for metabolic and endocrine indications including Type 1 diabetes.

- In January 2026 the University of Texas Southwestern Medical Center secured USD 25 Million in ARPA-H funding under the VITAL project to engineer functional 3D bioprinted livers, representing the single largest ARPA-H allocation toward bioprinting research recorded to date.

- CollPlant Biotechnologies introduced BioFlex during February 2026 as a turnkey recombinant human collagen kit designed for DLP-based 3D bioprinting, enabling reproducible scaffold output for regenerative medicine and meeting requirements for commercial GMP workflows.

- BICO Group AB reports an installed footprint exceeding 32,000 bioprinting and lab automation instruments deployed across more than 3,500 laboratories spanning 65 countries, with citations in over 11,000 peer-reviewed publications, the largest research-grade bioprinting base in the world.

- In September 2025 the MIT-Polimi monitoring system was published in the journal Device, validating AI-guided layer-by-layer imaging during embedded bioprinting and supporting reproducibility, real-time quality inspection, and adaptive process correction for clinical-grade tissue construct production.

Competitive Landscape Overview

The 3D bioprinting for tissue engineering market is moderately consolidated at the top tier and fragmented across niche specialists. The combined share of the top four players, BICO Group AB (CELLINK), 3D Systems Corporation, Aspect Biosystems Ltd., and Humacyte Inc., reached approximately 54% of platform-attributable value in 2025. Competition is technology-led rather than price-led, with three distinct architectures competing: research-grade benchtop bioprinters (CELLINK, Allevi/3D Systems, RegenHU), clinical-grade tissue therapeutics platforms (Aspect Biosystems, Humacyte, Organovo), and specialty hardware (Stratasys for medical models, Cyfuse for needle-array, Poietis for laser-assisted). The competitive frontier is shifting from hardware sales toward integrated tissue therapeutic platforms with embedded AI, computational design, and GMP manufacturing capabilities. New entrants include TissueLabs (Switzerland), CollPlant Biotechnologies (Israel), Foldink (Armenia), Cellbricks (Germany), and Pandorum Technologies (India). BICO Group's installed base of over 32,000 instruments across 3,500 laboratories anchors the research market, while Aspect Biosystems and Humacyte lead clinical translation.

Competitive Landscape Matrix

| Company Name | Headquarters | Market Position | Key Product / Solution | Geographic Strength | Recent Strategic Move |

| BICO Group AB (CELLINK) | Gothenburg, Sweden | Leader | BIO X, BIO X6, BIONOVA X bioprinters; bioinks | Europe, North America, Global | Over 32,000 instruments installed across 3,500 laboratories worldwide |

| 3D Systems Corporation | Rock Hill, USA | Leader | Print to Perfusion bioprinter; GenesisTissue spinout | North America, Europe | GenesisTissue Inc. spinout launched February 2025 |

| Aspect Biosystems Ltd. | Vancouver, Canada | Leader | Microfluidic 3D bioprinting; pancreatic tissue therapeutics | North America, Europe | USD 280 Million project with Government of Canada announced April 2, 2026 |

| Humacyte, Inc. | Durham, USA | Leader | ATEV (acellular tissue engineered vessel); Symvess | North America | Symvess (FDA approved December 19, 2024) commercial launch February 26, 2025 |

| Organovo Holdings, Inc. | San Diego, USA | Challenger | ExVive 3D liver and kidney tissue platform | North America | Phase 1 IBD program advancing 2025-2026 |

| Stratasys Ltd. | Rehovot, Israel | Challenger | P3 DLP technology; J5 MediJet | Global | Materialise partnership for medical 3D printing |

| ROKIT Healthcare | Seoul, South Korea | Challenger | INVIVO bioprinter; autologous regeneration | Asia, Global | Korean Won 21.7 Billion in cumulative funding to date |

| Poietis | Pessac, France | Niche Player | NGB-R laser-assisted bioprinter; Poieskin | Europe | Cosmetic skin model commercial expansion 2025 |

| CollPlant Biotechnologies | Rehovot, Israel | Niche Player | rhCollagen bioink; BioFlex DLP kit | Israel, Global | BioFlex rhCollagen DLP kit launched February 2026 |

| Cyfuse Biomedical K.K. | Tokyo, Japan | Niche Player | Regenova Kenzan needle-array bioprinter | Asia | Clinical pilots in cartilage tissue engineering |

By Technology

The 3D bioprinting for tissue engineering market by technology is led by extrusion-based bioprinting, which captured approximately 42.8% share in 2025. Extrusion-based platforms, exemplified by CELLINK BIO X and BIO X6, Aspect Biosystems' RX1, and 3D Systems' BioAssemblyBot, dispense bioinks ranging from 100 to 500 micrometers in continuous filaments through pneumatic or mechanical mechanisms. The technology offers cost-effectiveness, broad bioink compatibility, and surgical-grade load-bearing properties suitable for skeletal muscle, cartilage, and bone tissue engineering. Manufacturing scale advantages and ISO 9001 quality systems support segment leadership.

Inkjet-based bioprinting represented approximately 21.6% of segment value in 2025, anchored by drop-on-demand thermal and piezoelectric platforms suited for high-resolution skin and hepatic tissue printing at 50 to 200 micrometer feature sizes. Light-based bioprinting (DLP, stereolithography, two-photon) captured 18.4% share, anchored by CELLINK BIONOVA X (10 micrometer resolution), Readily3D volumetric printing, and 3D Systems' Print to Perfusion. Light-based platforms enable vascular network printing and grew at the fastest segment CAGR of 20.0% projected through 2034, driven by demand for perfusable thick tissues.

Microfluidic bioprinting accounted for 9.2% share in 2025, led by Aspect Biosystems' proprietary microfluidic printhead enabling cell encapsulation in immune-protective materials. Laser-assisted bioprinting captured 5.4% share, dominated by Poietis NGB-R systems used in cosmetic skin testing. Magnetic levitation and other emerging modalities held the residual 2.6% share. Comparison: light-based DLP platforms hold a 1.4x revenue advantage over inkjet for vascular tissue applications because volumetric curing enables sub-50 micrometer microvascular geometries unachievable with droplet-based methods.

By Bioink Material

The 3D bioprinting for tissue engineering market by bioink material is dominated by hydrogels, which accounted for approximately 38.4% share in 2025. GelMA (gelatin methacryloyl), alginate, hyaluronic acid, and PEG-based hydrogels anchor this segment with broad cell compatibility and tunable mechanical properties. Decellularized extracellular matrix (dECM) bioinks captured 22.1% share, growing fastest as native tissue mimicry becomes critical for clinical-grade constructs. Recombinant collagen and fibrin bioinks represented 16.8% share, anchored by CollPlant's rhCollagen platform and the February 2026 BioFlex launch. Living cell suspensions held 14.2% share, with the segment dominant for clinical-grade applications. Synthetic polymers (PLGA, PCL) held 6.1%, while ceramics and composite bioinks made up 2.4%. Procurement leads at NCI-designated Comprehensive Cancer Centers and academic medical centers should evaluate bioink selection against three criteria: cell viability above 90%, printability index, and ICH-aligned quality release specifications.

By Application

The 3D bioprinting for tissue engineering market by application is led by regenerative medicine implants at 32.0% share in 2025, encompassing vascular grafts, cartilage and bone scaffolds, skin substitutes, and tracheal repair constructs. Humacyte's Symvess and Aspect Biosystems' pancreatic islet tissue programs anchor clinical translation. Drug testing and disease modeling captured 25.4% share, projected to reach approximately USD 858 Million by 2030 across organoid and organ-on-chip applications, supported by FDA Modernization Act 2.0 acceptance of non-animal models. Skin tissue engineering represented 18.7% share led by Poietis Poieskin and Wake Forest Institute for Regenerative Medicine programs.

Bone and cartilage tissue engineering captured 12.4% share, with orthopedic implants accounting for approximately 33.9% of the broader segment in 2025 driven by patient-specific scaffold design. Vascular and cardiac applications held 6.8% share, anchored by Wyss Institute SWIFT and co-SWIFT vascular channel technology. Other tissue applications (liver, kidney, neural, pancreatic) made up 4.7% share, with the University of Texas Southwestern's USD 25 Million ARPA-H VITAL project (January 2026) and Wyss Institute's January 30, 2026 kidney collecting duct system anchoring R&D pipelines.

By End-User

The 3D bioprinting for tissue engineering market by end-user is led by academic and research institutes at 41.7% share in 2025, including Wyss Institute at Harvard, MIT, Wake Forest Institute for Regenerative Medicine, Memorial Sloan Kettering, and Polimi (Polytechnic University of Milan). Pharmaceutical and biotechnology companies captured 26.5% share, with the segment growing at 18.4% CAGR through 2034 as Roche, Novartis, Pfizer, Merck, and Eli Lilly integrate bioprinted toxicology models into preclinical workflows. Hospitals and surgical centers held 18.4% share, anchored by University Hospital Basel's March 2025 point-of-care facial implant printing. Medical device manufacturers and contract research organizations made up the residual 13.4% share. ROI calculation for hospital-based GMP bioprinting deployment must account for facility classification (ISO 7 cleanroom minimum), bioink supply chain validation, regulatory submission timelines (typically 24 to 36 months for RMAT-eligible products), and reimbursement coding strategy.

Regional Analysis

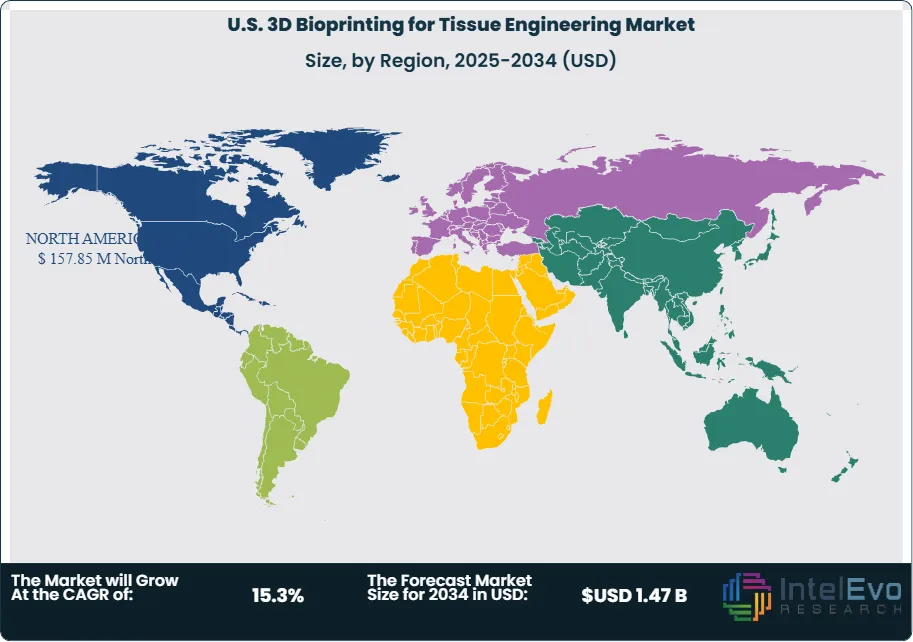

Northeast U.S. – Largest Regional Market

The Northeast U.S. accounted for the largest share of the U.S. 3D Bioprinting for Tissue Engineering Market in 2024, representing an estimated 38.5% of the total market. The region's leadership is driven by its strong concentration of biotechnology companies, globally recognized research universities, academic medical centers, and extensive government funding for regenerative medicine and tissue engineering research. States such as Massachusetts, New York, and Pennsylvania continue to lead innovation through collaborations between universities, hospitals, and biotechnology firms.

The region also benefits from a well-established life sciences ecosystem, access to venture capital, and the presence of leading pharmaceutical companies investing in personalized medicine, organ-on-chip technologies, and advanced biofabrication. Continuous research grants and commercialization activities are expected to maintain the Northeast's dominant position throughout the forecast period.

West U.S. – Fastest-Growing Regional Market

The West U.S. is projected to be the fastest-growing regional market during the forecast period, accounting for approximately 31.0% of the U.S. market in 2024. Growth is primarily supported by California's thriving biotechnology industry, strong venture capital investments, and increasing research in stem cell biology, regenerative medicine, and 3D bioprinting technologies. The presence of leading medical research institutions and technology startups further accelerates market expansion.

Rising adoption of AI-integrated bioprinting platforms, increasing demand for personalized healthcare solutions, and collaborations between biotechnology companies and healthcare providers are expected to drive sustained growth across the region. Continuous innovation and commercialization activities position the West as a key hub for next-generation tissue engineering technologies.

South U.S. – Expanding Biotechnology Infrastructure

The South U.S. held an estimated 19.5% share of the market in 2024, supported by growing investments in biotechnology research, healthcare infrastructure, and pharmaceutical manufacturing. States including Texas, North Carolina, Florida, and Georgia are witnessing increased establishment of life sciences research centers and biomanufacturing facilities.

Government support, expanding clinical research activities, and increasing partnerships between universities and biotechnology companies are contributing to regional growth. Rising demand for advanced tissue models in drug discovery and regenerative therapies is expected to further strengthen the South's market position over the forecast period.

Midwest U.S. – Emerging Research and Innovation Hub

The Midwest U.S. accounted for an estimated 11.0% of the market in 2024. The region benefits from strong biomedical engineering programs, university-led research initiatives, and growing collaborations between healthcare institutions and biotechnology companies. States such as Illinois, Ohio, Michigan, and Minnesota are increasingly investing in tissue engineering research and advanced medical technologies.

Although smaller in market size compared to other regions, the Midwest continues to expand through public-private partnerships, increased R&D funding, and advancements in biomaterials and bioink development. These factors are expected to create steady growth opportunities and enhance the region's role in the U.S. 3D bioprinting for tissue engineering market.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Technology

- Extrusion-Based Bioprinting

- Inkjet-Based Bioprinting

- Laser-Assisted Bioprinting

- Stereolithography (SLA)

- Digital Light Processing (DLP)

By Bioink Material

- Natural Bioinks

- Synthetic Bioinks

- Hybrid Bioinks

- Decellularized Extracellular Matrix (dECM)-Based Bioinks

By Application

- Regenerative Medicine

- Drug Discovery & Development

- Tissue & Organ Transplantation

- Disease Modeling

- Personalized Medicine

By End-User

- Research Institutes & Universities

- Pharmaceutical & Biotechnology Companies

- Hospitals & Clinics

- Contract Research Organizations (CROs)

- Medical Device Companies

By Regional Coverage

- U.S.A.

| Report Attribute | Details |

| Market size (2026) | USD 0.41 B |

| Forecast Revenue (2034) | USD 1.47 B |

| CAGR (2026-2034) | 15.3% |

| Historical data | 2021-2025 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Technology, (Extrusion-Based Bioprinting, Inkjet-Based Bioprinting, Laser-Assisted Bioprinting, Stereolithography (SLA), Digital Light Processing (DLP)), By Bioink Material, (Natural Bioinks, Synthetic Bioinks, Hybrid Bioinks, Decellularized Extracellular Matrix (dECM)-Based Bioinks), By Application, (Regenerative Medicine, Drug Discovery & Development, Tissue & Organ Transplantation, Disease Modeling, Personalized Medicine), By End-User, (Research Institutes & Universities, Pharmaceutical & Biotechnology Companies, Hospitals & Clinics, Contract Research Organizations (CROs), Medical Device Companies), |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | BICO GROUP AB (CELLINK), 3D SYSTEMS CORPORATION, ASPECT BIOSYSTEMS LTD., HUMACYTE, INC., ORGANOVO HOLDINGS, INC., STRATASYS LTD., ROKIT HEALTHCARE, POIETIS, COLLPLANT BIOTECHNOLOGIES LTD., CYFUSE BIOMEDICAL K.K., ADVANCED SOLUTIONS LIFE SCIENCES, LLC, REGENHU SA, MATERIALISE NV, TISSUELABS, ENVISIONTEC GMBH, INVENTIA LIFE SCIENCE PTY LTD, PANDORUM TECHNOLOGIES, CELLBRICKS GMBH, FOLDINK LIFE SCIENCE TECHNOLOGIES, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Bioink (Natural, Synthetic, Hybrid, dECM-Based), By Application (Regenerative Medicine, Drug Discovery, Organ Transplantation, Disease Modeling), By End-User (Research, Pharma & Biotech, Hospitals, CROs) Region, Key Players – Dynamics, Advanced Regenerative Medicine & Biomaterials Trends & Forecast 2026-2034")

, By Bioink (Natural, Synthetic, Hybrid, dECM-Based), By Application (Regenerative Medicine, Drug Discovery, Organ Transplantation, Disease Modeling), By End-User (Research, Pharma & Biotech, Hospitals, CROs) Region, Key Players – Dynamics, Advanced Regenerative Medicine & Biomaterials Trends & Forecast 2026-2034")

, By Bioink (Natural, Synthetic, Hybrid, dECM-Based), By Application (Regenerative Medicine, Drug Discovery, Organ Transplantation, Disease Modeling), By End-User (Research, Pharma & Biotech, Hospitals, CROs) Region, Key Players – Dynamics, Advanced Regenerative Medicine & Biomaterials Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the U.S. 3D Bioprinting for Tissue Engineering Market?

U.S. 3D Bioprinting for Tissue Engineering Market was valued at USD 0.36 Billion in 2024 and USD 0.41 Billion in 2025 and is projected to reach USD 1.47 Billion by 2034, growing at a CAGR of 15.3% during the forecast period 2026–2034.

Who are the major players in the U.S. 3D Bioprinting for Tissue Engineering Market?

BICO GROUP AB (CELLINK), 3D SYSTEMS CORPORATION, ASPECT BIOSYSTEMS LTD., HUMACYTE, INC., ORGANOVO HOLDINGS, INC., STRATASYS LTD., ROKIT HEALTHCARE, POIETIS, COLLPLANT BIOTECHNOLOGIES LTD., CYFUSE BIOMEDICAL K.K., ADVANCED SOLUTIONS LIFE SCIENCES, LLC, REGENHU SA, MATERIALISE NV, TISSUELABS, ENVISIONTEC GMBH, INVENTIA LIFE SCIENCE PTY LTD, PANDORUM TECHNOLOGIES, CELLBRICKS GMBH, FOLDINK LIFE SCIENCE TECHNOLOGIES, Others

Which segments covered the U.S. 3D Bioprinting for Tissue Engineering Market?

By Technology, (Extrusion-Based Bioprinting, Inkjet-Based Bioprinting, Laser-Assisted Bioprinting, Stereolithography (SLA), Digital Light Processing (DLP)), By Bioink Material, (Natural Bioinks, Synthetic Bioinks, Hybrid Bioinks, Decellularized Extracellular Matrix (dECM)-Based Bioinks), By Application, (Regenerative Medicine, Drug Discovery & Development, Tissue & Organ Transplantation, Disease Modeling, Personalized Medicine), By End-User, (Research Institutes & Universities, Pharmaceutical & Biotechnology Companies, Hospitals & Clinics, Contract Research Organizations (CROs), Medical Device Companies),

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

U.S. 3D Bioprinting for Tissue Engineering Market

Published Date : 14 Jul 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date