- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Ultra Fine Grinding Equipment Market Size, Share & Forecast | 5.4% CAGR

Global Ultra Fine Grinding Equipment Market Size, Share, Analysis By Product Type (Jet Mill, Hammer Mill, Agitated Mill, Cryogenic Mill, Others), By Operation Mode (Automated, Manual), By Process (Batch Process, Continuous Process), By Grinding Material (Dry Material, Wet Material), By Application (Mining, Pharmaceuticals, Cement, Chemicals & Materials, Food Processing, Institutional Laboratory, Others) Industry Regional Outlook, Market Dynamics, Technology Trends, Competitive Landscape & Forecast 2026–2034

Report Overview

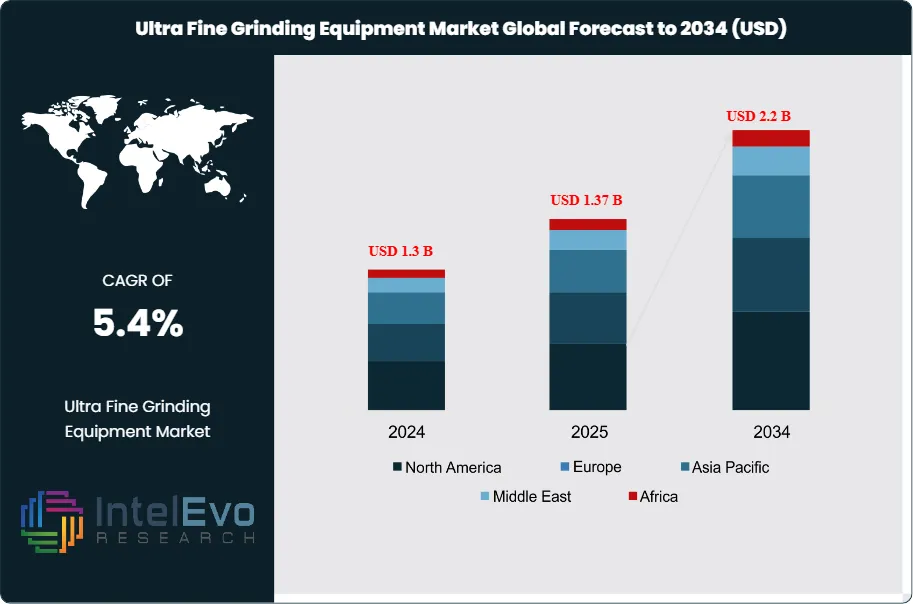

The Ultra Fine Grinding Equipment Market was valued at USD 1.3 billion in 2024 and is projected to reach approximately USD 1.37 billion in 2025. The market is further expected to expand to nearly USD 2.2 billion by 2034, registering a compound annual growth rate (CAGR) of about 5.4% during the forecast period from 2026 to 2034. Growth in the market is driven by increasing demand for high-precision particle size reduction across cement, pharmaceuticals, specialty chemicals, and advanced materials industries. Ultra-fine grinding equipment plays a critical role in improving material reactivity, product consistency, and processing efficiency, particularly in high-performance industrial and chemical applications. Additionally, continuous advancements in automation, digital monitoring systems, and energy-efficient grinding technologies are supporting broader adoption of ultra-fine grinding systems across modern manufacturing environments.

Get More Information about this report -

Request Free Sample ReportUltra-fine grinding equipment reduces solids to very small particle sizes through compression, shear, and friction. Demand concentrates in applications where particle-size distribution directly drives product performance and yield. Cement producers use ultra-fine milling to optimize blended formulations and improve strength development. Pharmaceutical and specialty chemical manufacturers rely on tight size control to improve dissolution, stability, and dispersion in high-value formulations. Mining and minerals processing also sustain baseline demand, particularly where liberation at finer sizes improves recovery rates and downstream separation efficiency.

The market’s near-term growth reflects a shift toward automation and continuous grinding circuits that raise throughput and reduce unit processing costs. Buyers increasingly specify integrated systems with advanced sensors, automated feed control, and closed-loop particle classification. AI-enabled analytics support predictive maintenance, energy optimization, and real-time quality control, which lowers unplanned downtime and stabilizes output. Digitalization also accelerates adoption of remote monitoring and commissioning, reducing reliance on scarce field specialists. These technology upgrades matter as energy intensity and wear-part consumption remain key cost drivers, and operators push for higher availability under tighter operating budgets.

Regulatory and compliance requirements reinforce this trajectory, especially in pharmaceuticals where GMP expectations and validation discipline favor controlled, traceable, and repeatable milling performance. In 2025, the U.S. Food and Drug Administration approved 44 novel drugs, following 50 approvals in 2024, supporting sustained investment in API processing and particle engineering. This trend increases interest in nanoparticle-enabled formulations and fine milling solutions that can meet stringent specification limits. At the same time, geopolitical uncertainty, supply-chain disruptions for precision components, and skilled labor shortages elevate delivery and commissioning risk, particularly for complex lines with high automation content.

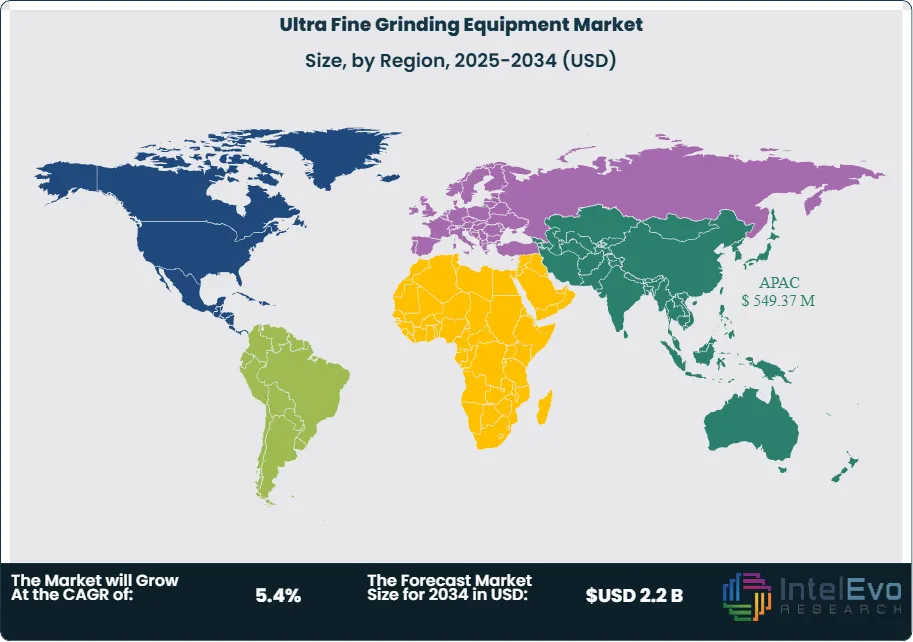

Regionally, Asia-Pacific held more than a 40.1% share in 2024, supported by capacity additions in cement, rapid growth in specialty chemicals, and expanding pharmaceutical production. Based on the 2024 global market size, this share implies approximately USD 0.52 billion in regional revenue. China and India remain primary demand centers, while Vietnam, Indonesia, and Thailand attract incremental investment in downstream processing and export-oriented manufacturing. North America and Europe continue to anchor high-spec installations in pharmaceuticals and specialty chemicals, where compliance and process control requirements support premium system configurations.

, By Operation Mode (Automated, Manual), By Process (Batch Process, Continuous Process), By Grinding Material (Dry Material, Wet Material), By Application (Mining, Pharmaceuticals, Cement, Chemicals & Materials, Food Processing, Institutional Laboratory, Others) Industry Regional Outlook, Market Dynamics, Technology Trends, Competitive Landscape & Forecast 2026–2034")

Key Takeaways

- Market Growth: The market totals 1.3 billion USD, 2024 and reaches 2.2 billion USD, 2034, reflecting 5.4% CAGR, 2026-2034.

- Segment Dominance : Agitated mills lead by type at 33.5%, 2024.

- Segment Dominance: Automated equipment leads by operation mode at 52.9%, 2024.

- Driver: High-volume end-use demand anchors growth, with cement holding 26.9%, 2024.

- Restraint: The market faces adoption friction from upfront system costs at estimated: 0.2 billion USD, 2024.

- Opportunity: Suppliers expand into high-value applications through capacity additions at estimated: 0.6 billion USD, 2030.

- Trend: Continuous processes set the operating standard at 68.9%, 2024.

- Regional Analysis: Asia Pacific leads global consumption at 40.1%, 2024.

By Type

Ultra fine grinding equipment spans jet mills, hammer mills, agitated mills, cryogenic mills, and other niche systems designed for specialized materials. As of 2025, agitated mills account for the largest share of installed capacity, representing about 33.5 percent of global demand. Their adoption reflects consistent performance in achieving sub-micron particle sizes while maintaining lower specific energy consumption compared with alternative technologies. This balance positions agitated mills as the preferred choice across high-volume and precision-driven industries.

Agitated mills rely on high-speed stirring mechanisms that maintain constant contact between grinding media and feed material. This configuration delivers uniform particle size distribution and stable throughput under continuous operation. Jet mills remain relevant in high-purity and contamination-sensitive applications, although their reliance on compressed gases raises operating costs at scale. Hammer mills continue to serve coarse and intermediate grinding needs, while cryogenic mills support temperature-sensitive materials despite higher capital and energy requirements. The type mix increasingly favors agitated systems as producers seek cost control and repeatable quality.

By Application

Application demand remains concentrated in cement, which accounts for approximately 26.9 percent of total equipment consumption in 2025. Cement producers require ultra fine grinding to support blended formulations, improve hydration efficiency, and enhance mechanical strength. Continuous kiln operations and large production volumes sustain steady replacement and upgrade cycles for grinding systems.

Mining, pharmaceuticals, chemicals, and food processing represent smaller but steadily growing segments. Pharmaceutical manufacturers deploy ultra fine grinding for active ingredient production where particle size directly affects bioavailability and formulation stability. Chemical and materials processors use these systems for pigments, fillers, and advanced compounds. Food processing applications focus on texture control and solubility, while institutional laboratories operate compact units primarily for testing and formulation development rather than commercial-scale output.

By End-Use

Industrial buildings represent the largest end-use category due to the concentration of cement plants, mineral processing sites, and chemical facilities. These environments favor automated and continuous grinding configurations to support uninterrupted production and consistent output quality. Capital allocation in this segment remains tied to infrastructure development, materials demand, and industrial expansion programs.

Commercial buildings follow, supported by pharmaceutical, specialty chemical, and food manufacturing facilities that require validated and reproducible processing. Residential building end-use remains indirect, driven mainly through upstream demand for cement and construction materials. Across all end-use categories, automation penetration continues to rise, with automated systems accounting for roughly 52.9 percent of total installations in 2025.

By Region

Asia Pacific remains the largest regional market, accounting for about 40.1 percent of global consumption in 2025. Rapid industrialization, large-scale cement production, and expanding pharmaceutical manufacturing underpin sustained demand. China leads global cement output with approximately 51 percent of worldwide production, reinforcing strong equipment utilization. India ranks second with close to 9 percent of global cement output and maintains a dominant role in generic drug manufacturing, producing over 500 active pharmaceutical ingredients and holding 57 percent of WHO-prequalified APIs.

North America and Europe maintain stable demand driven by pharmaceuticals, specialty chemicals, and materials research, with emphasis on compliance and process control. Latin America and the Middle East and Africa show emerging momentum as infrastructure investment and localized manufacturing capacity increase. These regions present longer-term growth potential as industrial output and processing sophistication continue to advance beyond 2025.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Product Type

- Jet Mill

- Hammer Mill

- Agitated Mill

- Cryogenic Mill

- Others

By Operation Mode

- Automated

- Manual

By Process

- Batch Process

- Continuous Process

By Grinding Material

- Dry Material

- Wet Material

By Application

- Mining

- Pharmaceuticals

- Cement

- Chemicals & Materials

- Food Processing

- Institutional Laboratory

- Others

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 1.37 B |

| Forecast Revenue (2034) | USD 2.2 B |

| CAGR (2025-2034) | 5.4% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product Type (Jet Mill, Hammer Mill, Agitated Mill, Cryogenic Mill, Others), By Operation Mode (Automated, Manual), By Process (Batch Process, Continuous Process), By Grinding Material (Dry Material, Wet Material), By Application (Mining, Pharmaceuticals, Cement, Chemicals & Materials, Food Processing, Institutional Laboratory, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Metso Corporation, Hosokawa Alpine AG, Retsch GmbH, Bepex International LLC, United Grinding Group, Promas Engineers Private Limited, Quadro, Atritor Limited, Pulva, Erich NETZSCH GmbH & Co. Holding KG, Fritsch GmbH, The Jet Pulverizer Company, Schutte Hammermill, HORIBA, Air Products and Chemicals, Inc., Hosokawa Micron Group, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Operation Mode (Automated, Manual), By Process (Batch Process, Continuous Process), By Grinding Material (Dry Material, Wet Material), By Application (Mining, Pharmaceuticals, Cement, Chemicals & Materials, Food Processing, Institutional Laboratory, Others) Industry Regional Outlook, Market Dynamics, Technology Trends, Competitive Landscape & Forecast 2026–2034")

, By Operation Mode (Automated, Manual), By Process (Batch Process, Continuous Process), By Grinding Material (Dry Material, Wet Material), By Application (Mining, Pharmaceuticals, Cement, Chemicals & Materials, Food Processing, Institutional Laboratory, Others) Industry Regional Outlook, Market Dynamics, Technology Trends, Competitive Landscape & Forecast 2026–2034")

, By Operation Mode (Automated, Manual), By Process (Batch Process, Continuous Process), By Grinding Material (Dry Material, Wet Material), By Application (Mining, Pharmaceuticals, Cement, Chemicals & Materials, Food Processing, Institutional Laboratory, Others) Industry Regional Outlook, Market Dynamics, Technology Trends, Competitive Landscape & Forecast 2026–2034")

Frequently Asked Questions

How big is the Ultra Fine Grinding Equipment Market?

Global Ultra Fine Grinding Equipment Market was valued at USD 1.3 billion in 2024 and is projected to reach USD 2.2 billion by 2034, growing at a CAGR of 5.4%. Discover key industry trends, drivers, and growth opportunities.

Who are the major players in the Ultra Fine Grinding Equipment Market?

Metso Corporation, Hosokawa Alpine AG, Retsch GmbH, Bepex International LLC, United Grinding Group, Promas Engineers Private Limited, Quadro, Atritor Limited, Pulva, Erich NETZSCH GmbH & Co. Holding KG, Fritsch GmbH, The Jet Pulverizer Company, Schutte Hammermill, HORIBA, Air Products and Chemicals, Inc., Hosokawa Micron Group, Other Key Players

Which segments covered the Ultra Fine Grinding Equipment Market?

By Product Type (Jet Mill, Hammer Mill, Agitated Mill, Cryogenic Mill, Others), By Operation Mode (Automated, Manual), By Process (Batch Process, Continuous Process), By Grinding Material (Dry Material, Wet Material), By Application (Mining, Pharmaceuticals, Cement, Chemicals & Materials, Food Processing, Institutional Laboratory, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Ultra Fine Grinding Equipment Market

Published Date : 09 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date