- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Unconventional Gas Treatment Market Size, Share & Forecast | CAGR 6.0%

Global Unconventional Gas Treatment Market Size, Share, Analysis By Treatment Process (Gas Sweetening, Dehydration, Sulfur Recovery & Tail Gas Treatment, NGL Recovery, Produced Water Treatment), By Source Application (Shale Gas, Tight Gas, Coalbed Methane, Other Unconventional Sources), By Technology (Amine Systems, Membrane Separation, Adsorption, Cryogenic Processes), By Facility Type, Industry Trends, Competitive Landscape & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

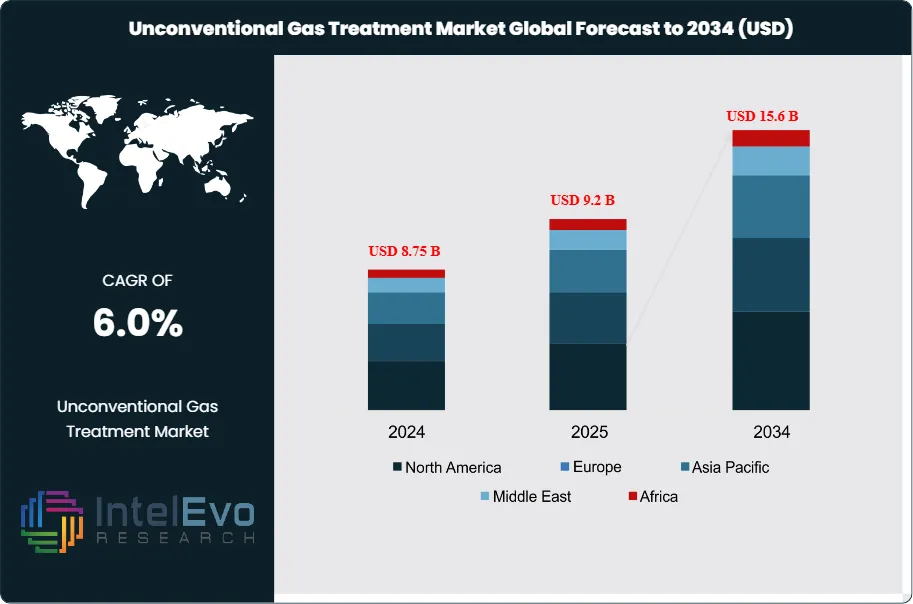

| USD 9.2 Billion | USD 15.6 Billion | 6.0% | North America, 35.0% |

The Unconventional Gas Treatment Market was valued at approximately USD 8.75 Billion in 2024 and increased to USD 9.2 Billion in 2025. The market is projected to reach nearly USD 15.6 Billion by 2034, expanding at a compound annual growth rate (CAGR) of around 6.0% during the forecast period from 2026 to 2034. This market estimate is a modeled view based on unconventional gas output growth, gas-processing equipment demand, methane-control regulation, LNG pretreatment expansion, and project activity across shale gas, tight gas, and coalbed methane value chains. U.S. dry natural gas production remained near record levels in 2024, with shale and tight resources still forming the backbone of supply growth, while Argentina’s Vaca Muerta and deeper shale development in China continued to widen the addressable base for gas sweetening, dehydration, sulfur recovery, membrane separation, and produced-water treatment systems.

Get More Information about this report -

Request Free Sample ReportThe unconventional gas treatment market sits at the intersection of upstream development and midstream quality compliance. Demand comes from rising sour-gas handling, higher water cuts in mature unconventional wells, stricter pipeline specifications, and larger NGL extraction and LNG pretreatment programs. Supply remains led by established technology houses and modular plant integrators with strong positions in amine systems, adsorption, membranes, cryogenic recovery, and packaged processing skids. Honeywell UOP, Technip Energies, SLB, Baker Hughes, Enerflex, and Chart Industries remain central because they combine process know-how with equipment, packaged systems, digital monitoring, or field services. Honeywell UOP continues to market broad gas-treating and LNG pretreatment systems. Technip Energies remains strong in sulfur recovery, tail-gas treatment, and NGL recovery. Enerflex entered 2025 with USD 1.5 Billion in energy-infrastructure backlog and a processing-heavy engineered-systems book.

Regulation is shifting the unconventional gas treatment market from a capacity story to a compliance-and-efficiency story. The EU methane regulation adopted in 2024 set measurement, monitoring, verification, and importer requirements for oil, gas, and coal, while U.S. OOOOb/c implementation and later deadline adjustments kept methane control at the center of facility design decisions. The IEA estimates fossil fuels account for nearly one-third of methane emissions from human activity, and energy-sector methane emissions stayed above 120 Mt annually, which keeps treatment, vapor recovery, sulfur cleanup, and digital leak management on capital agendas. These rules raise treatment intensity per unit of gas processed, especially in Europe, North America, and export-linked projects in the Middle East.

Regional investment patterns remain uneven. North America leads the unconventional gas treatment market on installed base and retrofit demand. Asia Pacific is the fastest-expanding pocket, supported by China’s deeper shale work and India’s rising gas-infrastructure buildout. The Middle East is emerging as the highest-value new-build zone because Saudi Arabia’s Jafurah program alone is adding large raw-gas treatment and NGL infrastructure, with Aramco outlining phase-one Jafurah gas plant progress and a long-term midstream deal tied to treating raw gas from the field. Latin America is gaining weight through Vaca Muerta-linked processing and export preparation. Europe remains smaller in upstream volumes but larger in treatment intensity due to methane, sulfur, and carbon constraints.

, By Source Application (Shale Gas, Tight Gas, Coalbed Methane, Other Unconventional Sources), By Technology (Amine Systems, Membrane Separation, Adsorption, Cryogenic Processes), By Facility Type, Industry Trends, Competitive Landscape & Forecast 2026–2034")

Key Takeaways

- Market Growth: The unconventional gas treatment market stood at USD 9.2 Billion in 2025 and is projected to reach USD 15.6 Billion by 2034. That implies a 6.0% CAGR across 2025–2034, supported by shale-linked processing demand, methane rules, and LNG pretreatment buildout.

- Segment Dominance: By treatment process, gas sweetening led with a 31.0% share in 2025, equal to about USD 2.9 Billion. Sour-gas handling, acid-gas removal, and sulfur-spec compliance kept amine-based systems in the lead.

- Segment Dominance: By source application, shale gas accounted for 46.0% of the unconventional gas treatment market in 2025, or about USD 4.2 Billion. U.S. shale scale and Argentina’s Vaca Muerta growth kept shale gas well ahead of tight gas and coalbed methane.

- Driver: Methane regulation and gas-quality compliance remain the main growth driver. The fossil fuel sector contributes nearly one-third of methane emissions from human activity, while energy-sector methane stayed above 120 Mt annually, pushing operators toward tighter treatment and monitoring systems.

- Restraint: Capital intensity remains the main restraint. Large gas-processing and pretreatment projects require multi-year spending, and buying patterns can pause when commodity prices weaken, as seen in Enerflex’s 2025 commentary on deferred customer decisions despite a USD 1.2 Billion engineered-systems backlog.

- Opportunity: Modular and skid-mounted systems represent the clearest opening, with a 43.0% 2025 share or roughly USD 4.0 Billion. Remote shale basins, flare-reduction programs, and phased LNG pretreatment favor faster-deployment plant formats.

- Trend: Digital treatment and emissions monitoring are becoming standard. SLB’s methane LiDAR approval in 2025 and its electric completions launch point to a broader shift toward digitally managed production and processing assets through 2034.

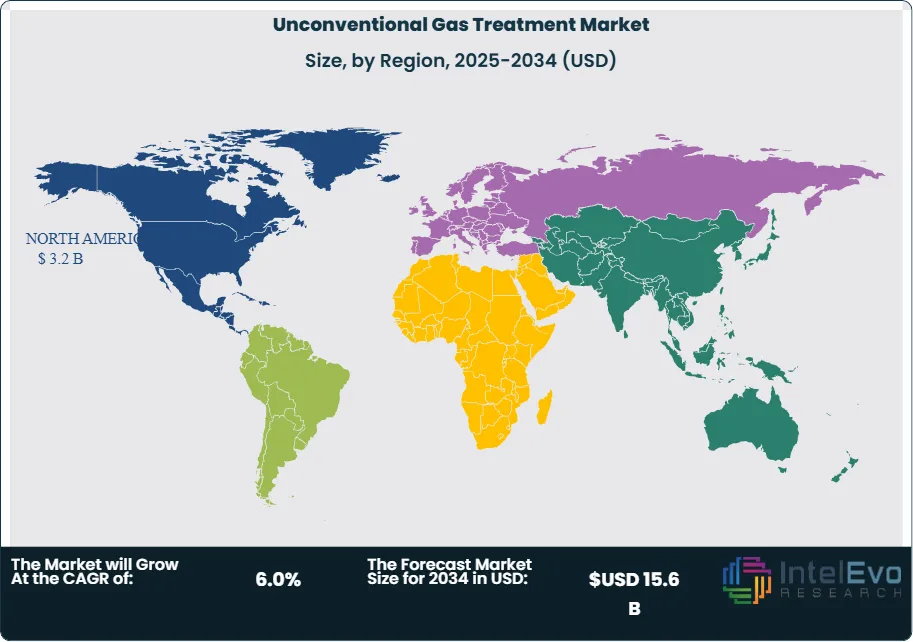

- Regional Analysis: North America led the unconventional gas treatment market with a 35.0% share in 2025, equal to USD 3.2 Billion. The region benefits from the largest shale gas processing base and sustained LNG-linked pretreatment demand.

Competitive Landscape

The unconventional gas treatment market is moderately consolidated. The top four players held an estimated 39.0% share in 2025. Competition is technology-driven in sweetening, sulfur recovery, cryogenic separation, and digital emissions control, but price and delivery speed matter in modular projects. Competitive intensity rose in 2025–2026 as Baker Hughes moved to acquire Chart Industries for USD 13.6 Billion, SLB deepened its unconventional gas exposure in Saudi Arabia, and Technip Energies added major LNG and gas-processing awards.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| Honeywell UOP | US | Leader | Amine Guard FS gas treating and LNG pretreatment suite | North America, Middle East | Partnered with Argent LNG in April 2025 to assess pretreatment solutions including MRU, AGRU and SeparSIV for a Louisiana LNG project. |

| Technip Energies | France | Leader | CRYOMAX NGL recovery and sulfur recovery/tail-gas treatment | Middle East, Europe | Won a major QatarEnergy North Field West LNG contract in February 2026. |

| SLB | US | Leader | Symmetry process software and methane detection tools | North America, Middle East | Secured a five-year Saudi Aramco unconventional gas contract in December 2025. |

| Baker Hughes | US | Leader | Modular LNG and gas technology packages | North America, Asia Pacific, Middle East | Announced a USD 13.6 Billion acquisition of Chart Industries in July 2025. |

| Enerflex | Canada | Challenger | Modular gas processing and treated-water infrastructure | North America, Latin America, Middle East | Reported USD 1.5 Billion EI backlog in May 2025 and agreed to divest a non-core business in February 2026. |

| Chart Industries | US | Challenger | IPSMR liquefaction and modular gas systems | North America | Won LNG Alliance process technology scope for a 7.8 MTPA Mexico facility in July 2025. |

| John Wood Group | UK | Niche Player | Gas facility operations and maintenance services | Middle East, North America | Won a 10-year Rio Grande LNG maintenance contract in December 2025. |

| Air Liquide Engineering & Construction | France | Niche Player | Cryocap and gas purification systems | Europe, Asia Pacific | Closed the DIG Airgas acquisition in South Korea in early 2026 after signing the deal in August 2025. |

By Treatment Process

By treatment process, gas sweetening held the largest share at 31.0% in 2025, equivalent to USD 2.9 Billion. Operators continue to prioritize CO2 and H2S removal because shale and tight reservoirs increasingly feed LNG, NGL, and cross-border gas systems that demand tighter quality control. Dehydration followed with 24.0%, or USD 2.2 Billion, supported by pipeline-spec moisture limits and corrosion risk reduction. Sulfur recovery and tail-gas treatment represented 19.0%, or USD 1.7 Billion, reflecting higher sour-gas intensity in the Middle East and selected North American and Chinese plays. NGL recovery accounted for 16.0%, or USD 1.5 Billion, while produced-water and associated fluid treatment made up 10.0%, or USD 0.9 Billion. The share pattern reflects where treatment sits in the value chain: sweetening and dehydration appear across almost every plant, while sulfur and liquids recovery concentrate in higher-value streams. Honeywell UOP and Technip Energies remain strong in gas treating, LNG pretreatment, sulfur recovery, and NGL recovery. Enerflex and Chart gain share where operators prefer packaged or modular formats over large site-built plants.

By Source Application

By source application, shale gas dominated the unconventional gas treatment market with 46.0% of 2025 revenue, or USD 4.2 Billion. The segment leads because U.S. shale and Argentina’s Vaca Muerta set the pace for gathering, compression, sweetening, dehydration, NGL extraction, and export-linked pretreatment. Tight gas followed with 32.0%, equal to USD 2.9 Billion. Tight-gas projects often need strong dehydration and acid-gas handling because reservoir quality and composition vary more sharply across basins. Coalbed methane accounted for 14.0%, or USD 1.3 Billion, with Australia, China, and selected North American areas sustaining niche demand for water-heavy treatment trains and gas cleanup. Other unconventional streams, including associated low-permeability gas and hybrid shale-tight developments, represented 8.0%, or USD 0.7 Billion. Shale gas keeps the lead because it combines scale, infrastructure, and downstream pull from LNG and petrochemical feedstock markets. China’s move into deeper shale formations and Saudi Arabia’s unconventional gas expansion should narrow the gap somewhat by 2034, but shale remains the anchor segment for global unconventional gas treatment growth.

By Technology

By technology, amine-based systems held 38.0% of the market in 2025, or USD 3.5 Billion. They remain the default choice for bulk acid-gas removal in gas sweetening and LNG pretreatment. Membrane systems represented 22.0%, or USD 2.0 Billion, gaining ground in modular, offshore-adjacent, and smaller-footprint projects where lower maintenance and faster deployment matter. Adsorption systems, including molecular sieves and related dehydration technologies, accounted for 18.0%, or USD 1.7 Billion. Cryogenic processes contributed 14.0%, or USD 1.3 Billion, mainly through NGL recovery and liquids-rich gas projects. Other technologies, including hybrid chemical-physical processes and specialty sulfur cleanup, made up 8.0%, or USD 0.7 Billion. Competitive positioning follows complexity. Honeywell UOP and Technip Energies stay strongest in amine, sulfur, and pretreatment process design. Chart and modular packagers gain more traction in cryogenic and compact process trains. The long-term shift favors hybrid systems that combine chemical treating, digital controls, methane detection, and modular fabrication, especially where operators need phased buildouts rather than one large plant.

By Facility Configuration

By facility configuration, centralized processing plants held 57.0% of 2025 revenue, or USD 5.2 Billion, because large basins still favor hub-and-spoke gathering systems tied to regional gas plants, NGL fractionation, or LNG feedgas conditioning. Modular and skid-mounted plants captured 43.0%, or USD 4.0 Billion, and this is the faster-moving slice of the market. Remote shale basins, early-production systems, flare-reduction projects, and phased development models all support modular adoption. Honeywell’s modular pretreatment positioning, Chart’s modular liquefaction systems, and Enerflex’s backlog profile point to continued movement in this direction. The key competitive issue is not only equipment cost. It is delivery speed, standardization, site labor availability, and ease of redeployment. Centralized plants will still dominate value through 2034 because the largest unconventional developments need full-scale sweetening, sulfur, and NGL trains. Even so, modular systems should gain share in Latin America, the Middle East, and secondary North American basins where operators want quicker cash generation and lower upfront execution risk.

Regional Analysis

Market in North America

North America held 35.0% of the unconventional gas treatment market in 2025, equal to USD 3.2 Billion. The United States drives the region by a wide margin because shale and tight formations continue to dominate the country’s gas supply base, and U.S. dry natural gas production reached nearly 38 trillion cubic feet in 2024. The country also benefits from a deep installed base of gas plants, NGL extraction, LNG pretreatment, sulfur cleanup, and emissions-control retrofits. Canada remains the second-largest regional market, supported by Montney and Duvernay activity, midstream tie-ins, and LNG Canada-related conditioning demand. Mexico is smaller but relevant through cross-border gas use, industrial demand, and LNG-linked project development on the Gulf and Pacific coasts. Policy is now as important as geology. U.S. methane rules under OOOOb/c and EPA compliance guidance are increasing the share of treatment budgets linked to vapor recovery, leak control, and monitored process equipment. Baker Hughes, Honeywell UOP, SLB, Chart, and Enerflex all have strong regional positions because North America combines scale with retrofit intensity. This remains the largest unconventional gas treatment market through 2034, even though growth rates will be lower than in Asia Pacific and the Middle East.

Market in Europe

Europe accounted for 22.0% of the unconventional gas treatment market in 2025, equivalent to USD 2.0 Billion. The region has a smaller unconventional production base than North America, but treatment intensity is higher because methane, sulfur, and carbon rules are stricter. Germany, the UK, the Netherlands, and Norway shape most regional demand through engineering, equipment supply, gas quality control, and LNG-related treatment services rather than large domestic shale volumes. Regulation (EU) 2024/1787 changed the tone of the market by requiring stronger methane measurement, reporting, verification, and importer compliance, which pushes more treatment and monitoring requirements into projects supplying Europe. That matters for both domestic facilities and import-linked assets abroad. The UK also remains relevant through gas-fired generation and infrastructure projects where treatment and carbon-linked conditioning technologies matter. Technip Energies, Air Liquide, Honeywell UOP, and Wood have strong positions in this market because Europe buys process design, sulfur systems, cryogenic purification, and long-term maintenance capabilities rather than only field services. Europe’s unconventional gas treatment market grows on compliance value, LNG integration, and decarbonized processing rather than raw volume expansion.

Market in Asia Pacific

Asia Pacific represented 26.0% of the unconventional gas treatment market in 2025, or USD 2.4 Billion. China is the core market. Its deeper shale breakthrough in the Sichuan Basin and state support for shale gas and coalbed methane continue to pull in gas sweetening, dehydration, water handling, and sulfur recovery systems. India is a rising buyer of imported technology and modular treatment equipment as gas infrastructure, CGD expansion, and industrial gas use rise. Australia remains a niche but high-value market due to coal seam gas processing and LNG feedgas conditioning. Indonesia is the fourth strategically important country because it combines sour-gas processing, LNG infrastructure, and rising offshore-to-onshore treatment needs. The region’s investment case rests on a simple pattern. Domestic demand is rising, but gas quality and methane control requirements are also getting tighter. That raises the treatment spend per unit of gas developed. Honeywell and Baker Hughes are active across LNG-linked pretreatment in the region, while modular system providers gain ground where basin infrastructure remains uneven. Asia Pacific should record the fastest growth in the unconventional gas treatment market through 2034, supported by China’s shale depth gains and India’s expanding downstream gas system.

Market in Latin America

Latin America held 9.0% of the unconventional gas treatment market in 2025, equal to USD 0.8 Billion. Argentina dominates the region because Vaca Muerta now accounts for more than 70% of national gas output and reached 74% of natural gas production in September 2024. That production profile is pushing demand for gathering, dehydration, liquids recovery, water handling, and export-oriented pretreatment. Brazil is the second key country because it stands to absorb more regional gas trade and industrial gas demand. Mexico remains relevant in Latin America from a market-coverage standpoint through LNG and industrial linkages, although its treatment demand is often counted with North America in operator planning. Colombia is the fourth strategically important country due to unconventional resource interest and gradual gas infrastructure development. Latin America still faces midstream bottlenecks, financing constraints, and project timing risk. Even so, the region benefits from shorter-cycle unconventional wells and lower-cost modular processing options. Enerflex is well placed in this geography because of its Latin American infrastructure footprint, while U.S.-based process licensors benefit from export and LNG positioning. Latin America’s growth rate should outpace Europe through 2034, even from a smaller base.

Market in Middle East & Africa

Middle East & Africa accounted for 8.0% of the unconventional gas treatment market in 2025, or USD 0.7 Billion. Saudi Arabia is the pivotal country because Jafurah is one of the largest unconventional gas developments globally and requires significant raw-gas processing, treatment, and NGL infrastructure. Aramco’s 2025 disclosures point to phase-one Jafurah gas plant progress, a 2.0 bscfd sustainable sales-gas target by 2030, and major midstream arrangements tied to treating raw gas from the field. The UAE is the second major market due to unconventional development partnerships and strong project execution ecosystems. South Africa is smaller but relevant through coalbed methane and gas monetization potential. The rest of MEA, including Oman and Bahrain, remains important for modular processing, contract operations, and sulfur-rich gas work. This region carries the highest average project value per installation because assets are often large, integrated, and linked to industrial feedstock or export chains. SLB, Technip Energies, Baker Hughes, Enerflex, and Wood all have strong regional exposure. Middle East & Africa should post one of the strongest value-growth profiles through 2034 because new-build treatment plants here tend to be large and specification-heavy.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Treatment Process

- Gas Sweetening

- Dehydration

- Sulfur Recovery and Tail Gas Treatment

- NGL Recovery

- Produced Water and Associated Fluid Treatment

By Source Application

- Shale Gas

- Tight Gas

- Coalbed Methane

- Other Unconventional Gas

By Technology

- Amine-Based Systems

- Membrane Separation

- Adsorption Systems

- Cryogenic Processes

- Other Technologies

By Facility Configuration

- Centralized Processing Plants

- Modular and Skid-Mounted Plants

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 9.2 B |

| Forecast Revenue (2034) | USD 15.6 B |

| CAGR (2025-2034) | 6.0% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Treatment Process (Gas Sweetening, Dehydration, Sulfur Recovery and Tail Gas Treatment, NGL Recovery, Produced Water and Associated Fluid Treatment), By Source Application (Shale Gas, Tight Gas, Coalbed Methane, Other Unconventional Gas), By Technology (Amine-Based Systems, Membrane Separation, Adsorption Systems, Cryogenic Processes, Other Technologies), By Facility Configuration (Centralized Processing Plants, Modular and Skid-Mounted Plants) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | HONEYWELL UOP, TECHNIP ENERGIES, SLB, BAKER HUGHES, ENERFLEX, CHART INDUSTRIES, JOHN WOOD GROUP, AIR LIQUIDE ENGINEERING & CONSTRUCTION, HALLIBURTON, SULZER, ALFA LAVAL, JEREH GROUP, EXPRO, WÄRTSILÄ GAS SOLUTIONS, JOHNSON MATTHEY, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Source Application (Shale Gas, Tight Gas, Coalbed Methane, Other Unconventional Sources), By Technology (Amine Systems, Membrane Separation, Adsorption, Cryogenic Processes), By Facility Type, Industry Trends, Competitive Landscape & Forecast 2026–2034")

, By Source Application (Shale Gas, Tight Gas, Coalbed Methane, Other Unconventional Sources), By Technology (Amine Systems, Membrane Separation, Adsorption, Cryogenic Processes), By Facility Type, Industry Trends, Competitive Landscape & Forecast 2026–2034")

, By Source Application (Shale Gas, Tight Gas, Coalbed Methane, Other Unconventional Sources), By Technology (Amine Systems, Membrane Separation, Adsorption, Cryogenic Processes), By Facility Type, Industry Trends, Competitive Landscape & Forecast 2026–2034")

Frequently Asked Questions

How big is the Unconventional Gas Treatment Market?

The Global Unconventional Gas Treatment Market was valued at USD 9.2 Billion in 2025, projected to reach USD 15.6 Billion by 2034, growing at a CAGR of 6.0% from 2026–2034, driven by rising shale gas production, LNG expansion, and demand for advanced gas purification technologies.

Who are the major players in the Unconventional Gas Treatment Market?

HONEYWELL UOP, TECHNIP ENERGIES, SLB, BAKER HUGHES, ENERFLEX, CHART INDUSTRIES, JOHN WOOD GROUP, AIR LIQUIDE ENGINEERING & CONSTRUCTION, HALLIBURTON, SULZER, ALFA LAVAL, JEREH GROUP, EXPRO, WÄRTSILÄ GAS SOLUTIONS, JOHNSON MATTHEY, Others

Which segments covered the Unconventional Gas Treatment Market?

By Treatment Process (Gas Sweetening, Dehydration, Sulfur Recovery and Tail Gas Treatment, NGL Recovery, Produced Water and Associated Fluid Treatment), By Source Application (Shale Gas, Tight Gas, Coalbed Methane, Other Unconventional Gas), By Technology (Amine-Based Systems, Membrane Separation, Adsorption Systems, Cryogenic Processes, Other Technologies), By Facility Configuration (Centralized Processing Plants, Modular and Skid-Mounted Plants)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Unconventional Gas Treatment Market

Published Date : 19 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date