- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Underbalanced Drilling Market Size, Share & Forecast | CAGR 7.0%

Global Underbalanced Drilling Market Size, Share, Growth Analysis By Technique (Air Drilling, Mist Drilling, Foam Drilling, Aerated Mud Drilling), By Application (Onshore, Offshore), By Well Type (Horizontal & Directional Wells, Vertical Wells, Multilateral & High-Angle Wells), By End-Use (Mature Fields, Unconventional Reservoirs, HPHT & Deepwater Wells), Industry Trends, Competitive Landscape, Regional Insights & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

| USD 4.3 Billion | USD 7.9 Billion | 7.0% | North America, 31.0% |

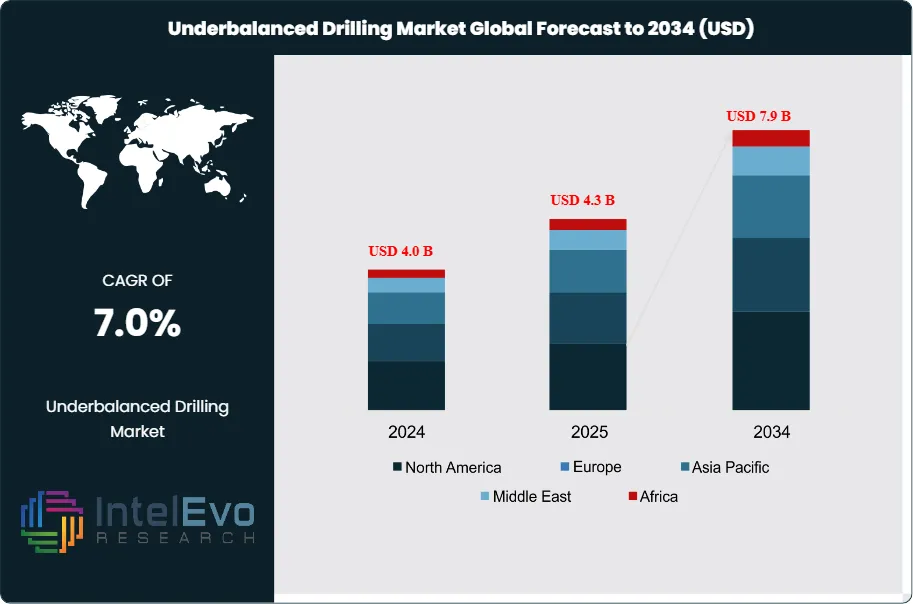

The Global Underbalanced Drilling Market was valued at approximately USD 4.0 Billion in 2024 and increased to USD 4.3 Billion in 2025. The market is projected to reach nearly USD 7.9 Billion by 2034, expanding at a compound annual growth rate (CAGR) of 7.0% during the forecast period from 2026 to 2034. The underbalanced drilling market is gaining share inside well construction budgets because operators want higher reservoir contact, lower formation damage, and faster production response from mature and pressure-sensitive assets. Underbalanced drilling keeps bottomhole pressure below formation pressure, which allows controlled inflow while drilling and reduces mud invasion into the reservoir. That technical advantage matters most in depleted fields, fractured carbonate formations, heavy-oil zones, and selected horizontal wells where conventional overbalanced drilling can impair deliverability.

Get More Information about this report -

Request Free Sample ReportDemand in the underbalanced drilling market is tied closely to upstream spending in existing fields rather than frontier exploration alone. Operators continue to direct capital toward decline mitigation, brownfield redevelopment, infill wells, and workover-linked drilling campaigns. This spending pattern favors underbalanced drilling in assets where production gains justify higher technical service intensity. North America remains the largest revenue pool because of broad horizontal drilling adoption and mature reservoir redevelopment. The Middle East follows closely, backed by low-cost reserves, rising NOC spending, and greater use of pressure-management services in carbonate and gas developments.

Supply remains concentrated among a small group of integrated drilling and pressure-control specialists. SLB, Halliburton, Weatherford, and Nabors shape the top tier, while Ensign, Parker Wellbore, NOV, Baker Hughes, and regional contractors fill equipment, rig, and niche service roles. Competition centers on pressure-control hardware, rotating control devices, remote choke systems, real-time modeling, automated drilling workflows, and crew competence. AI, automation, and digital drilling tools are now moving from pilot status to operating practice. Vendors are pairing underbalanced drilling with managed pressure drilling, closed-loop automation, and remote operations to tighten well control and reduce nonproductive time.

The main risk factors remain cost, operational complexity, gas-handling requirements, HSE exposure, and limited suitability in wells with unstable formations or narrow operating margins. Underbalanced drilling usually carries higher upfront service intensity than conventional drilling, and not every reservoir produces enough incremental recovery to justify the premium. Regulatory pressure is also rising around emissions, flare control, well integrity, and personnel certification. That is pushing vendors toward closed-loop systems, better separator packages, automated choke control, and accredited training. By 2025, North America accounts for 31.0% of the underbalanced drilling market, followed by Middle East and Africa at 27.0% and Asia Pacific at 21.0%. Investment hotspots through 2034 include the US Permian and mature Rockies assets, Saudi Arabia, the UAE, Oman, Mexico deepwater, Brazil offshore, and selected Southeast Asian gas projects.

, By Application (Onshore, Offshore), By Well Type (Horizontal & Directional Wells, Vertical Wells, Multilateral & High-Angle Wells), By End-Use (Mature Fields, Unconventional Reservoirs, HPHT & Deepwater Wells), Industry Trends, Competitive Landscape, Regional Insights & Forecast 2026–2034")

Key Takeaways

- Market Growth: The underbalanced drilling market stood at USD 4.3 Billion in 2025 and is projected to reach USD 7.9 Billion by 2034, reflecting a 7.0% CAGR across 2025-2034. Growth is supported by mature-field redevelopment, pressure-managed drilling uptake, and stronger digital drilling execution.

- Segment Dominance: By technique, air drilling led the market with a 38.0% share in 2025, equal to about USD 1.6 Billion. Operators favor it in hard formations and depleted zones where low fluid density supports rate of penetration and lower invasion risk.

- Segment Dominance: By application, onshore drilling held a 68.0% share in 2025, or roughly USD 2.9 Billion. The segment benefits from large mature well inventories in North America, the Middle East, and selected Asia Pacific basins.

- Driver: The main growth driver is the need to protect reservoir productivity in depleted and pressure-sensitive formations. Underbalanced approaches can lift flow performance materially, with field cases showing strong early production gains.

- Restraint: The main restraint is higher execution cost and safety complexity. Adoption remains strongest in premium wells because complex programs can add 15.0%-25.0% to direct service intensity.

- Opportunity: The largest opportunity sits in mature-field and redevelopment wells, which accounted for 46.0% of 2025 demand, or about USD 2.0 Billion. The addressable pool expands as operators keep directing capital toward decline mitigation.

- Trend: The leading trend is the fusion of underbalanced drilling with automation, managed pressure drilling controls, and AI-assisted workflows. Recent field programs have shown faster penetration, lower flat time, and measurable days saved.

- Regional Analysis: North America led the market in 2025 with a 31.0% share, equal to about USD 1.3 Billion. The region leads because it combines horizontal drilling density, service availability, and a large stock of mature and pressure-depleted wells.

Competitive Landscape

The underbalanced drilling market is moderately consolidated. The top four players held an estimated 47.0% of global revenue in 2025. Competition is primarily technology-driven, then execution-driven, with price pressure strongest in commoditized onshore work. Competitive intensity increased in 2025 as vendors pushed automation partnerships, managed pressure drilling contracts, and regional rig expansion.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| SLB | US | Leader | DrillOps / Drillbench workflows | North America, Middle East | Digital collaboration with Cactus Drilling to scale automated drilling (Jun 2025) |

| HALLIBURTON | US | Leader | Underbalanced Drilling Services | North America, Middle East | Advanced automation benchmarks with Nabors in Oman (Apr 2025) |

| WEATHERFORD | US | Leader | Victus Intelligent MPD / UBD | Middle East, Latin America | Added contracts in Kuwait, Mexico, and UAE during 2025-2026 |

| NABORS INDUSTRIES | Bermuda | Leader | MPD / SmartROS-enabled drilling | Middle East, North America | Reported MPD as a major growth driver in 4Q 2025 results |

| ENSIGN ENERGY SERVICES | Canada | Challenger | UBD and MPD services | Canada, US, Middle East | Upgraded Oman rigs tied to a five-year contract beginning 2026 |

| PARKER WELLBORE | US | Challenger | Managed Pressure Services | Middle East, US | Became part of Nabors strategic expansion after acquisition agreement |

| NOV | US | Niche Player | MPowerD MPD systems | Global offshore | Reported major offshore MPD equipment awards in early 2025 |

| BAKER HUGHES | US | Challenger | CoilTrak / AutoTrak drilling systems | Latin America, offshore global | Expanded drilling technology awards and offshore activity in 2026 |

| ADNOC DRILLING | UAE | Challenger | Integrated rig fleet and drilling services | UAE, GCC | Agreed to acquire 80% of MB Petroleum Services in Nov 2025 |

By Technique.

Air drilling remained the largest technique segment in 2025 with a 38.0% share, or USD 1.6 Billion. It leads because it offers the lowest equivalent circulating density, strong penetration rates, and a simpler cost profile in suitable dry, hard, or depleted formations. Adoption is highest in North American land wells, parts of the Middle East, and selected coalbed methane and tight-gas developments. Mist drilling accounted for 24.0%, or USD 1.0 Billion, and serves wells that need better cuttings transport and modest liquid support. Foam drilling reached 21.0%, or USD 0.9 Billion, where unstable formations or water-sensitive intervals require higher carrying capacity. Aerated mud held 17.0%, or USD 0.7 Billion, and remains important where operators want underbalanced benefits but need better bottomhole stability, deeper well reach, or easier transition from conventional programs.

By Application.

Onshore drilling dominated the market in 2025 with a 68.0% share, equal to USD 2.9 Billion. The segment leads because land operators can mobilize compressors, separators, and choke packages faster and at lower cost than offshore operators. The business case also improves in brownfield infill work, horizontal redevelopment, and workover-linked drilling in mature basins. Offshore drilling accounted for 32.0%, or USD 1.4 Billion, and has a higher revenue intensity per well because equipment complexity, HSE procedures, and logistics raise service pricing. Offshore adoption is strongest in Mexico, Brazil, the Gulf of Mexico, and selective Middle East and Southeast Asian projects where narrow pressure windows and reservoir protection justify the added complexity.

By Well Type.

Horizontal and directional wells formed the largest well-type segment in 2025 with a 44.0% share, or USD 1.9 Billion. These wells benefit most from underbalanced drilling because long reservoir exposure amplifies the impact of formation damage. Conventional vertical wells still represented a 31.0% share, or USD 1.3 Billion, especially in mature field redevelopment, smaller NOC projects, and well re-entry campaigns where the target interval is known and operational risk can be tightly managed. Multilateral and high-angle wells accounted for 25.0%, or USD 1.1 Billion. This segment is smaller in volume but high in revenue per well because execution requires stronger pressure control, better hydraulic modeling, and more experienced field crews.

By End Use.

Mature field redevelopment was the leading end-use segment in 2025 with a 46.0% share, or USD 2.0 Billion. This is the deepest demand pool because operators increasingly target decline mitigation rather than greenfield supply growth. Unconventional and tight reservoirs held 34.0%, or USD 1.5 Billion. The segment is strongest in North America and selective Asia Pacific gas plays, where horizontal drilling, lower-pressure targets, and production sensitivity to formation damage improve the economic case. HPHT and deepwater wells accounted for the remaining 20.0%, or USD 0.9 Billion. This segment grows from a smaller base but carries the fastest forecast because offshore operators are adopting more advanced pressure-control and automation tools in wells with narrow operating margins.

Regional Analysis

North America

North America held a 31.0% share of the market in 2025, equal to about USD 1.3 Billion. The US accounted for the bulk of regional revenue, followed by Canada and Mexico. The region leads because it combines mature-field redevelopment, widespread horizontal drilling, strong service capacity, and faster adoption of automation. Mexico is smaller by volume but higher in service intensity because offshore well complexity raises demand for pressure-managed techniques, including underbalanced and near-underbalanced modes.

Europe

Europe represented a 12.0% share in 2025, or roughly USD 0.5 Billion. Norway, the UK, the Netherlands, and Romania are the most relevant national markets. Norway anchors the region because offshore operators continue to pursue infill wells, tiebacks, and late-life field extensions in the North Sea. Europe grows more slowly than North America or the Middle East because regulatory scrutiny is higher and exploration growth is modest, but the region still values reservoir protection and well-control precision in mature offshore assets.

Asia Pacific

Asia Pacific accounted for a 21.0% share in 2025, equal to about USD 0.9 Billion. China, Australia, India, and Malaysia are the region’s most strategic country markets. China leads because of its large base of mature onshore fields, tight gas development, and continued need to improve well productivity in pressure-sensitive zones. The region offers a strong growth runway because operators are upgrading field development methods rather than relying on conventional drilling alone.

Latin America

Latin America held a 9.0% share in 2025, equal to around USD 0.4 Billion. Brazil, Mexico, and Argentina drive demand. Brazil is the region’s largest long-term opportunity because offshore pre-salt and frontier projects are pushing demand for higher-end drilling and pressure-control systems. Mexico remains highly relevant because deepwater and Gulf of Mexico programs raise the value of pressure-managed drilling.

Middle East and Africa

Middle East and Africa held a 27.0% share in 2025, equal to roughly USD 1.2 Billion. Saudi Arabia, the UAE, Oman, and South Africa are the key country references, though Saudi Arabia and the UAE dominate actual revenue. The region’s strength comes from large mature fields, extensive carbonate reservoirs, rising gas development, and strong NOC spending. This region is likely to post the fastest revenue expansion through 2034 because spending is stable, well complexity is rising, and operators are funding both output growth and late-life recovery work.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Technique

- Air Drilling

- Mist Drilling

- Foam Drilling

- Aerated Mud Drilling

By Application

- Onshore

- Offshore

By Well Type

- Horizontal and Directional Wells

- Conventional Vertical Wells

- Multilateral and High-Angle Wells

By End Use

- Mature Field Redevelopment

- Unconventional and Tight Reservoirs

- HPHT and Deepwater Wells

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 4.3 B |

| Forecast Revenue (2034) | USD 7.9 B |

| CAGR (2025-2034) | 7.0% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Technique (Air Drilling, Mist Drilling, Foam Drilling, Aerated Mud Drilling), By Application (Onshore, Offshore), By Well Type (Horizontal and Directional Wells, Conventional Vertical Wells, Multilateral and High-Angle Wells), By End Use (Mature Field Redevelopment, Unconventional and Tight Reservoirs, HPHT and Deepwater Wells) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | SLB, HALLIBURTON, WEATHERFORD, NABORS INDUSTRIES, ENSIGN ENERGY SERVICES, PARKER WELLBORE, NOV, BAKER HUGHES, ADNOC DRILLING, CACTUS DRILLING, AIR DRILLING ASSOCIATES, BLADE ENERGY PARTNERS, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Onshore, Offshore), By Well Type (Horizontal & Directional Wells, Vertical Wells, Multilateral & High-Angle Wells), By End-Use (Mature Fields, Unconventional Reservoirs, HPHT & Deepwater Wells), Industry Trends, Competitive Landscape, Regional Insights & Forecast 2026–2034")

, By Application (Onshore, Offshore), By Well Type (Horizontal & Directional Wells, Vertical Wells, Multilateral & High-Angle Wells), By End-Use (Mature Fields, Unconventional Reservoirs, HPHT & Deepwater Wells), Industry Trends, Competitive Landscape, Regional Insights & Forecast 2026–2034")

, By Application (Onshore, Offshore), By Well Type (Horizontal & Directional Wells, Vertical Wells, Multilateral & High-Angle Wells), By End-Use (Mature Fields, Unconventional Reservoirs, HPHT & Deepwater Wells), Industry Trends, Competitive Landscape, Regional Insights & Forecast 2026–2034")

Frequently Asked Questions

How big is the Underbalanced Drilling Market?

The Global Underbalanced Drilling Market was valued at USD 4.3 Billion in 2025, projected to reach USD 7.9 Billion by 2034, growing at a CAGR of 7.0% from 2026–2034, driven by demand for improved drilling efficiency, reduced formation damage, and increased adoption in complex and unconventional reservoirs.

Who are the major players in the Underbalanced Drilling Market?

SLB, HALLIBURTON, WEATHERFORD, NABORS INDUSTRIES, ENSIGN ENERGY SERVICES, PARKER WELLBORE, NOV, BAKER HUGHES, ADNOC DRILLING, CACTUS DRILLING, AIR DRILLING ASSOCIATES, BLADE ENERGY PARTNERS, Others

Which segments covered the Underbalanced Drilling Market?

By Technique (Air Drilling, Mist Drilling, Foam Drilling, Aerated Mud Drilling), By Application (Onshore, Offshore), By Well Type (Horizontal and Directional Wells, Conventional Vertical Wells, Multilateral and High-Angle Wells), By End Use (Mature Field Redevelopment, Unconventional and Tight Reservoirs, HPHT and Deepwater Wells)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Underbalanced Drilling Market

Published Date : 23 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date