- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Urinary Drainage Bags Market Size USD 7.2B | 5.8% CAGR

Global Urinary Drainage Bags Market Size, Share & Industry Analysis By Product Type (Leg Bags, Bedside Bags), By Material, By Usage (Short-Term, Long-Term), By End User (Hospitals, Homecare, Nursing Facilities), Regional Market Dynamics, Competitive Insights & Forecast 2025–2034

Report Overview

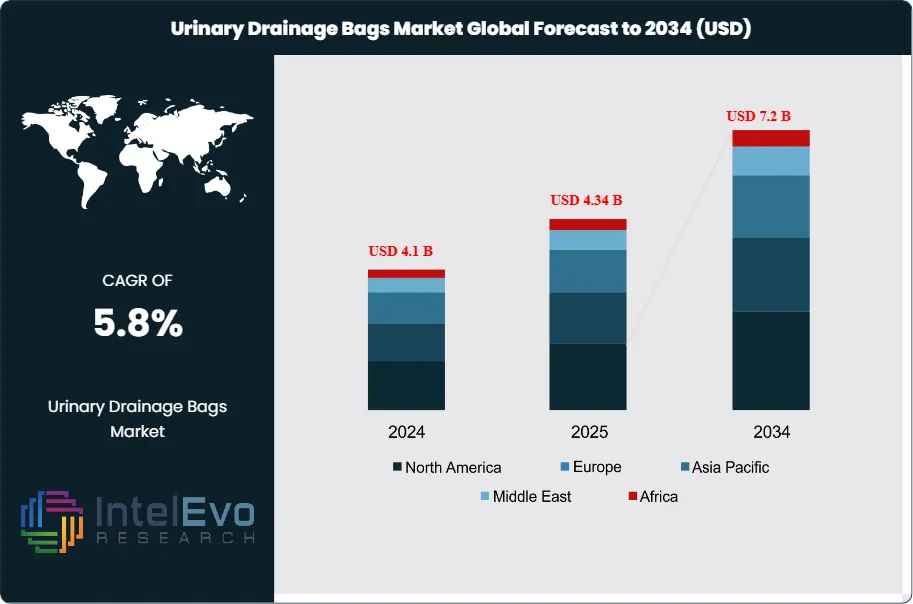

The Urinary Drainage Bags Market is estimated at USD 4.1 billion in 2024 and is projected to reach approximately USD 7.2 billion by 2034, registering a CAGR of about 5.8% during 2025–2034. Market growth is supported by the rising prevalence of urinary incontinence, chronic kidney disease, and post-surgical catheterization needs, particularly among the aging population. Increasing hospitalization rates, expansion of long-term care facilities, and growing demand for home healthcare solutions are further driving adoption. Additionally, product innovations focused on infection control, patient comfort, and discreet wearable designs are enhancing acceptance and positioning urinary drainage bags as an essential component of modern urological care.

Get More Information about this report -

Request Free Sample ReportThe market has witnessed steady growth over the past decade, driven by increasing demand for urinary drainage solutions due to rising cases of urinary incontinence, urinary retention, and related health conditions. The aging population, particularly women aged 40 to 70, is a significant contributor to this trend. Studies from the National Center for Biotechnology Information indicate that the prevalence of urinary incontinence rises with age, underscoring the growing need for effective solutions. Governments and organizations, both profit and non-profit, are actively promoting awareness around urinary incontinence care, further supporting market expansion.

On the supply side, advancements in medical technologies are reshaping the industry. The development of user-friendly and efficient catheter systems, along with improved drainage bag designs, has enhanced patient comfort and reduced risks of infection. Digital monitoring tools are increasingly being integrated into these systems to track urine output more accurately, making them indispensable in critical care settings. Automation in manufacturing processes has also contributed to higher product quality and availability.

Regionally, North America leads the market due to its advanced healthcare infrastructure and higher awareness of urinary health issues. Europe follows closely, supported by its aging population and government initiatives to improve elder care. Meanwhile, Asia-Pacific is emerging as a dynamic growth region. The region’s rapidly expanding healthcare sector, coupled with increasing awareness and affordability of medical devices, presents significant investment opportunities. Countries like India and China are expected to see a surge in demand due to their large aging populations and rising healthcare spending.

Despite these opportunities, challenges persist. Price sensitivity in developing regions, coupled with risks of infection associated with improper catheter use, remains a hurdle. However, the market is primed for continued growth as healthcare providers adopt advanced solutions and awareness initiatives gain traction globally. The industry’s evolution is being shaped by the convergence of technological advancements and increasing demand, making it an attractive space for stakeholders.

, By Material, By Usage (Short-Term, Long-Term), By End User (Hospitals, Homecare, Nursing Facilities), Regional Market Dynamics, Competitive Insights & Forecast 2025–2034")

Key Takeaways

- Market Growth: The Urinary Drainage Bags Market is projected to reach USD 7.2 billion by 2034, growing at a CAGR of 5.8% from its 2024 valuation of USD 4.1 billion. Key drivers include the aging population and increasing prevalence of urinary incontinence.

- Product Type: Leg bags, particularly those with 500-1000 ml capacity, account for 58% of the market share. Their ease of mobility and ability to prevent backflow make them the preferred choice for users.

- Chamber Type: Single-chamber drainage bags dominate due to their widespread use in post-surgical care. However, two-chamber bags are gaining traction, driven by demand for improved urine collection efficiency.

- Usage Type: Disposable drainage bags generate the highest revenue, as they mitigate the risks of urinary tract infections and are convenient for both patients and caregivers.

- End-Use Dominance: Hospitals hold a 44% market share, attributed to the high volume of surgeries and better access to advanced healthcare infrastructure. Ambulatory surgical centers and home care settings are emerging as significant growth areas, particularly for chronic disease management.

- Driver: Rising urinary incontinence rates, particularly among individuals aged 40 and above, are fueling market demand. This trend is further supported by government and non-profit initiatives aimed at promoting urinary health awareness.

- Restraint: Lack of awareness about urinary drainage solutions in developing economies limits market penetration, particularly in low-income regions.

- Opportunity: The growing geriatric population presents a significant market opportunity. Increased life expectancy and age-related health conditions are expected to drive demand for urinary drainage solutions, particularly in Asia-Pacific.

- Trend: Technological advancements, such as digital urine monitoring systems integrated with drainage bags, are gaining adoption in critical care settings. These solutions enhance patient management and reduce infection risks.

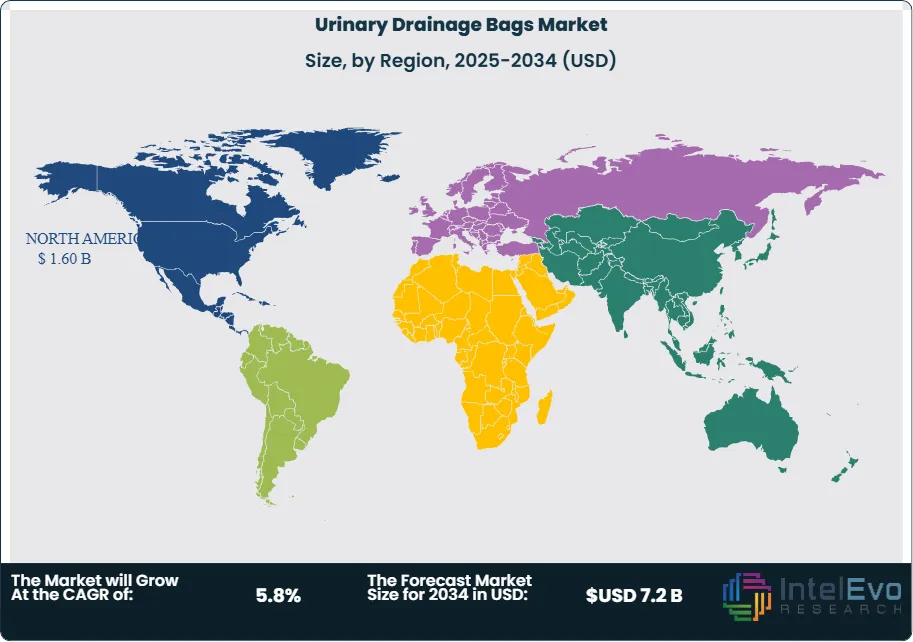

- Regional Analysis: North America leads with a 39% market share, driven by advanced healthcare facilities and higher awareness levels. Asia-Pacific is the fastest-growing region, supported by expanding healthcare infrastructure, increasing geriatric populations, and improved distribution networks.

Type Analysis

The urinary drainage bags market is segmented into large-capacity bags (1,000–2,000 ml) and leg bags (500–1,000 ml). Among these, the leg bags segment accounted for 58% of the market share in 2025 and is expected to grow steadily over the forecast period. This dominance is attributed to their convenience, as leg bags allow users greater mobility and privacy. Features such as anti-reflux valves, which minimize the risk of urine backflow, further drive adoption in both home care and clinical settings.

Large-capacity bags, with a urine-holding capacity of 1,000–2,000 ml, represent the second-largest segment and are projected to grow at a notable CAGR. These products are primarily used in hospitals and long-term care facilities where frequent monitoring of urine output is required. However, their relatively higher cost compared to leg bags may limit their adoption in low-income regions.

Number of Chambers Analysis

Based on the number of chambers, the market is categorized into single-chamber, two-chamber, and three-chamber bags. Single-chamber bags lead the market, driven by their widespread use during surgical and post-operative care. The availability of these products from leading manufacturers, combined with their cost-effectiveness, supports their dominance.

Two-chamber bags, however, are gaining momentum and are expected to grow at the fastest rate during the forecast period. Their design enhances comfort and wearability, making them a preferred choice among patients requiring extended use. While three-chamber bags remain a niche segment, they may find greater adoption in specialized medical settings.

Usage Analysis

In terms of usage, the market is divided into reusable and disposable urinary drainage bags. Disposable bags dominate the segment, generating the highest revenue share as of 2025. Their popularity stems from their ease of use and ability to minimize the risk of urinary tract infections (UTIs) associated with improper bag cleaning. Users benefit from the convenience of single-use disposal, eliminating the need for frequent emptying or maintenance.

Reusable bags, while cost-effective in the long term, are less popular due to the additional effort required for proper cleaning and maintenance. However, they remain an option in regions with limited access to disposable products.

End-Use Analysis

The end-use segment is divided into hospitals, clinics, ambulatory surgical centers (ASCs), home care, and others. Hospitals are the largest end-user, holding 44% of the market share in 2025. This dominance is attributed to the high volume of urological surgeries and the availability of advanced healthcare facilities. The hospital sector is expected to maintain its leadership throughout the forecast period.

Ambulatory surgical centers (ASCs) are expected to exhibit robust growth due to their cost-effective procedures and increasing preference for outpatient surgical services. Additionally, the home care segment is growing rapidly, fueled by the rising prevalence of chronic diseases among the aging population and the shift toward in-home treatment for long-term care.

Regional Analysis

North America leads the global urinary drainage bags market, accounting for 39% of revenue in 2025. The region's dominance is driven by the high prevalence of urological disorders, advanced healthcare infrastructure, and the strong presence of key market players. According to the Urology Care Foundation, millions of Americans suffer from overactive bladder and related conditions, further boosting demand for urinary drainage solutions.

Asia-Pacific is projected to register the fastest growth during the forecast period. Factors such as expanding healthcare expenditure, improving distribution networks, and a growing geriatric population are driving demand for urinary drainage bags in countries like China and India. Increased awareness of urinary health and improving access to medical devices also contribute to the region's growth potential.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Product

- Large Capacity Bags (1000- 2000 ml)

- Leg Bags (500-1000 ml)

By Number of Chambers

- Single Chamber

- Two Chamber

- Three Chamber

By Usage

- Reusable

- Disposable

By End-User

- Hospitals

- Clinics

- Ambulatory Surgical Centers

- Home Care

- Other End Users

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2024) | USD 4.1 B |

| Forecast Revenue (2034) | USD 7.2 B |

| CAGR (2024-2034) | 5.8% |

| Historical data | 2020-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product (Large Capacity Bags (1000- 2000 ml), Leg Bags (500-1000 ml)), By Number of Chambers (Single Chamber, Two Chamber, Three Chamber), By Usage (Reusable, Disposable), By End-User (Hospitals, Clinics, Ambulatory Surgical Centers, Home Care, Other End Users) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Medline Industries, Inc., BD, Moore Medical LLC, Manfred Sauer GmbH, McKesson Medical Surgical, Inc., ConvaTec Group PLC, Leboo Healthcare Products Limited, Braun Melsungen, Cardinal Health, Inc., Flexicare Medical Ltd., Becton, Dickinson and Company, Clinisupplies Ltd., Coloplast A/S, Teleflex Incorporated |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Material, By Usage (Short-Term, Long-Term), By End User (Hospitals, Homecare, Nursing Facilities), Regional Market Dynamics, Competitive Insights & Forecast 2025–2034")

, By Material, By Usage (Short-Term, Long-Term), By End User (Hospitals, Homecare, Nursing Facilities), Regional Market Dynamics, Competitive Insights & Forecast 2025–2034")

, By Material, By Usage (Short-Term, Long-Term), By End User (Hospitals, Homecare, Nursing Facilities), Regional Market Dynamics, Competitive Insights & Forecast 2025–2034")

Select Licence Type

Connect with our sales team

Urinary Drainage Bags Market

Published Date : 23 Dec 2025 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date