- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

US Coiled Tubing Services Market Size, Share & Growth Analysis | 4% CAGR

US Coiled Tubing Services Market Size, Share & Industry Analysis By Service (Well Intervention & Production, Drilling, Completion, Other Services & P&A Support), By Operation (Circulation & Cleanout, Pumping, Logging, Perforation), By Application (Onshore, Offshore), By Well Type (Conventional Wells, Unconventional Wells, Decommissioning & P&A Wells) Industry Region & Key Players – Market Segment Overview, Competitive Landscape, Oilfield Service Trends, Market Dynamics & Forecast 2025–2034

Report Overview

| Market Size (2025) | Forecast (2034) | CAGR | Lead Region (2025) |

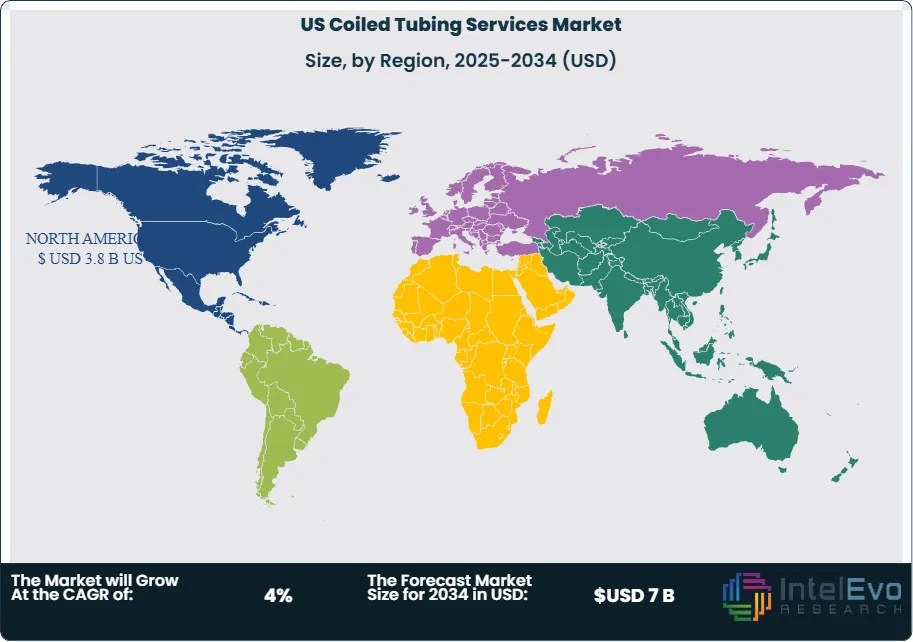

| USD 3.8 Billion | USD 7 Billion | 4% | US |

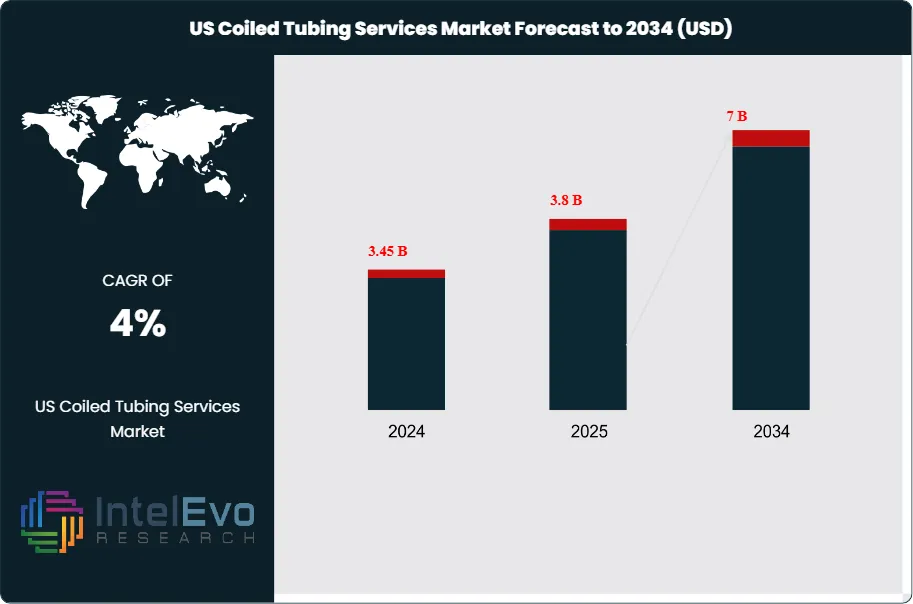

The US Coiled Tubing Services Market was valued at USD 3.8 Billion in 2025 and is expected to reach USD 7 Billion by 2034, growing at a CAGR of 4% during the forecast period 2025-2034. The Coiled Tubing Services Market sits inside the broader well intervention and production-optimization chain, where operators use continuous pipe on a reel to run cleanouts, stimulation, logging, perforation, milling, nitrogen kickoffs, and drilling with less rig time than conventional methods. Public market tracking shows North America as the clear revenue leader in 2025, while service mix remains led by well intervention and production work. That pattern reflects a large installed base of mature wells, continuing unconventional activity, and operator preference for lower-cost intervention methods that extend output instead of funding only new developments.

Get More Information about this report -

Request Free Sample ReportDemand in the Coiled Tubing Services Market is driven by three linked forces. First, mature-field decline keeps intervention demand firm. The IEA said mature fields show observed decline rates close to 6% globally, which means around 5 million barrels per day of supply must be replaced each year just to keep production flat. Second, global liquids consumption and supply still support ongoing oilfield activity, even with more volatile prices. Third, operators remain cautious on capital spending. The IEA expects a 6% fall in upstream oil investment in 2025, which favors service lines that raise output from existing wells with lower well-possession time and lower cost than full rig-based workovers. These conditions support cleanout, circulation, production logging, and through-tubing stimulation demand across both onshore and offshore assets.

Supply in the Coiled Tubing Services Market remains concentrated around a small set of global leaders with strong intervention portfolios, large installed fleets, and digital job planning tools, but the field is not fully consolidated. SLB, Halliburton, Baker Hughes, and Weatherford anchor the high-spec global market, while NOV supplies a large share of core equipment and regional players such as Trican, STEP, Calfrac, Archer, and KLX deepen basin-level competition. Automation, real-time telemetry, and AI-linked planning tools are now shaping job design, fleet deployment, and downhole diagnostics. SLB is pushing autonomous intervention and digital workflows. Halliburton is expanding real-time hybrid coiled tubing capability. Baker Hughes is scaling underbalanced coiled tubing drilling in Saudi Arabia. Weatherford is commercializing digitally connected thru-tubing systems.

Regionally, North America held 53.3% of the Coiled Tubing Services Market in 2025 and remains the anchor for shale and mature-well intervention. Latin America is gaining from offshore Brazil contract flow. The Middle East is rising on unconventional gas and brownfield work, especially in Saudi Arabia and the UAE. Europe stays relevant through North Sea intervention, plug and abandonment, and Norway's high 2025 petroleum investment cycle. Asia Pacific is led by China, Australia, India, and Southeast Asia, where mature fields and gas projects lift demand. Risks remain real. Lower oil prices can delay nonessential work. Steel and tariff pressures can lift tubing and equipment costs. Offshore work remains exposed to vessel costs, permitting cycles, and customer budget resets.

, By Operation (Circulation & Cleanout, Pumping, Logging, Perforation), By Application (Onshore, Offshore), By Well Type (Conventional Wells, Unconventional Wells, Decommissioning & P&A Wells) Industry Region & Key Players – Market Segment Overview, Competitive Landscape, Oilfield Service Trends, Market Dynamics & Forecast 2025–2034")

Key Takeaways

- Market Growth: The Coiled Tubing Services Market stood at USD 7.88 Billion in 2025 and is projected to reach USD 12.39 Billion by 2034 at a 5.1% CAGR over 2025-2034.

- Segment Dominance: Well intervention and production remained the top service segment with an estimated 67.0% share in 2025, equal to about USD 5.28 Billion.

- Segment Dominance: Onshore applications led with an estimated 78.0% share in 2025, or USD 6.15 Billion, supported by shale, mature land wells, and faster mobilization economics.

- Driver: The main growth driver is mature-well intervention demand. Mature fields decline at roughly 6.0% a year and require around 5 million barrels/day of replacement supply annually.

- Restraint: The main restraint is upstream spending pressure. Upstream oil investment is expected to fall 6.0% in 2025, which slows discretionary work, especially in smaller offshore campaigns and price-sensitive basins.

- Opportunity: The largest opportunity sits in unconventional gas and brownfield gas. Baker Hughes' Saudi expansion lifts its active underbalanced coiled tubing drilling fleet from 4 to 10 units beginning in 2026.

- Trend: The defining trend is digital and real-time intervention. SLB cites CT setup time reductions from 3 hours to under 30 minutes on rapid-deployment equipment.

- Regional Analysis: North America led the Coiled Tubing Services Market with a 53.3% share in 2025, equal to about USD 4.20 Billion.

Coiled Tubing Services Market Competitive Landscape

Competitive Summary

The Coiled Tubing Services Market is moderately consolidated. The top four players, SLB, Halliburton, Baker Hughes, and Weatherford, account for an estimated 47.0% of 2025 market revenue. Competition is mainly technology-driven and geography-driven. Global leaders win where real-time telemetry, offshore execution, and integrated intervention packages matter most, while regional firms stay strong in basin-led onshore work. Competitive intensity increased in 2025-2026 through Petrobras and Aramco awards, Trican's Iron Horse acquisition, and STEP's push into ultra-deep reel capacity.

Competitive Landscape Matrix

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| SLB | US | Leader | ACTive / CT intervention portfolio | North America, Middle East, Latin America | Awarded Petrobras an USD 800 million offshore integrated services contract in Brazil in Dec 2024 |

| Halliburton | US | Leader | SPECTRUM real-time hybrid coiled tubing | North America, Latin America, Middle East | Won Petrobras offshore intervention and P&A contract, starting in Q2 2025 |

| Baker Hughes | US | Leader | Integrated UBCTD and TeleCoil intelligent CT | Middle East, North America | Secured Aramco expansion to raise active UBCTD fleet from 4 to 10 units, announced Oct 2025 |

| Weatherford | US | Leader | SMART-LINK and thru-tubing intervention systems | Middle East, Europe, Asia Pacific | Reported a 3-year thru-tubing well services contract in offshore Malaysia in Jul 2025 |

| NOV | US | Challenger | Hydra Rig coiled tubing injectors and reels | North America, Middle East | Reported delivery of integrated packages including coiled tubing units and injector heads in Q2 2025 |

| Trican Well Service | Canada | Challenger | Integrated coiled tubing and frac services | Canada | Closed Iron Horse acquisition in Aug 2025 for C$77.35 million cash plus 33.76 million shares |

| STEP Energy Services | Canada | Challenger | COIL+ and UDx ultra-deep reel trailer | Canada, US Permian | Introduced UDx in Feb 2026 with capacity up to 35,000 ft of 2-5/8 in. coiled tubing |

| Calfrac Well Services | Canada | Niche Player | Basin-based coiled tubing and cementing | Canada, Argentina | Reported year-over-year coiled tubing activity growth and fleet adjustment in Q2 2025 |

| Archer | Bermuda | Niche Player | North Sea coiled tubing and P&A services | Europe | Expanded service scope under an existing 5-year P&A contract covering around 130 wells in Nov 2025 |

| KLX Energy Services | US | Niche Player | Rapid-deployment CT support and downhole tools | US land basins | Reported Rocky Mountains revenue growth in Q2 2025 driven by coiled tubing, pressure pumping, and tech services |

Segmentation Analysis

Coiled Tubing Services Market by Service

Well intervention and production led the Coiled Tubing Services Market with an estimated 67.0% share in 2025, or USD 5.28 Billion. This segment includes cleanouts, stimulation, nitrogen kickoffs, logging conveyance, reperforation support, and production-restoration work. Public coiled tubing market data shows well intervention and production as the largest service segment, and operator behavior supports that structure because mature wells need repeat interventions, while CT reduces trip time and avoids larger rig spreads. SLB, Halliburton, Baker Hughes, and Weatherford all position CT as a central intervention tool across the well life cycle. Competitive advantage in this segment comes from digital modeling, downhole telemetry, offshore deployment packages, and integrated pumping and diagnostics. Pricing stays firmer here than in pure commodity land work because job design and execution risk matter more.

Drilling services accounted for an estimated 15.0% share in 2025, or USD 1.18 Billion. This segment is smaller than intervention but strategically important in re-entry, slimhole, underbalanced, and unconventional gas programs. Baker Hughes' coiled tubing drilling focus and the 2025 Aramco expansion show where this market is moving. The commercial case is strongest where operators need lower formation damage, lower footprint, and improved access in complex wells. Growth is faster in the Middle East than in mature North American basins because national operators are scaling gas supply and unconventional development. The segment remains technically demanding and capital intensive, so market access is limited to firms with surface package depth, engineering support, and field reliability.

Completion services represented an estimated 10.0% share in 2025, or USD 0.79 Billion. CT-supported completion activity includes selective stimulation, sand control support, velocity-string installation, and completion-removal tasks. This segment grows where operators prioritize lower well-possession time and selective remediation over full recompletions. Baker Hughes and Weatherford both promote CT-enabled completion and well-preparation systems, while Halliburton's subsea and downline packages support offshore completion-related intervention. This segment is less recurring than production cleanout work but benefits from higher service intensity per campaign and stronger margins offshore.

Other services, including P&A support, held an estimated 8.0% share in 2025, or USD 0.63 Billion. The bucket includes milling, fishing support, barrier placement, selective abandonment, and pre-abandonment preparation. Europe and parts of the Gulf of Mexico give this segment structural support because aging fields need lower-cost decommissioning workflows. Archer's North Sea scope expansion and Halliburton's Brazil intervention and P&A award show how CT is increasingly tied to well-life-end economics, not only production uplift. This segment will grow faster than the total market through 2034, but from a smaller base.

Coiled Tubing Services Market by Operation

Circulation and cleanout accounted for an estimated 34.0% share in 2025, equal to USD 2.68 Billion. This remains the most common CT operation because solids removal, wellbore cleanup, and restart work repeat across mature well inventories. Halliburton's SandKleen and similar packages show how service firms keep refining this basic but high-volume activity. The segment wins where downtime costs are visible and operator teams want rigless restoration. It is also less exposed to commodity price spikes than discretionary drilling support because it protects existing output.

Pumping operations held an estimated 29.0% share in 2025, or USD 2.29 Billion. This category includes acidizing, nitrogen kickoffs, chemical placement, and selective stimulation. It benefits from brownfield output management and from gas wells that need efficient lift or cleanup. Weatherford, SLB, and Baker Hughes all pair CT with pumping-related service lines, and the value per job is higher than basic circulation because chemical design and placement precision directly affect production response. Middle East gas and offshore Brazil are strong growth zones for this segment.

Logging represented an estimated 20.0% share in 2025, or USD 1.58 Billion. Logging conveyed by CT grows when wells are highly deviated, when conventional wireline faces reach limits, or when operators want more data in a single intervention campaign. Weatherford's Norway work and SLB's powered measurements cases show why this segment is gaining technical relevance. While smaller than circulation or pumping, logging is one of the more technology-rich CT niches and supports premium pricing.

Perforation accounted for an estimated 17.0% share in 2025, or USD 1.34 Billion. The segment remains important in remedial campaigns, offshore interventions, and selective re-entry work. It often appears bundled with logging and stimulation in integrated packages rather than sold as a stand-alone line item. Because perforation relies on job sequencing, pressure control, and completion compatibility, larger global providers hold an edge.

Coiled Tubing Services Market by Application

Onshore dominated the Coiled Tubing Services Market with an estimated 78.0% share in 2025, equal to USD 6.15 Billion. Onshore strength comes from shale basins in the US and Canada, mature conventional fields in the Middle East, and land-based brownfield activity in China, India, and Latin America. Public coiled tubing market research has long shown strong structural onshore dominance, and company fleet strategies still reflect that pattern. STEP, Trican, Calfrac, KLX, and the land divisions of the global leaders all compete heavily here. The segment is more price-sensitive than offshore, but utilization is deeper and redeployment cycles are shorter.

Offshore held an estimated 22.0% share in 2025, or USD 1.73 Billion. Offshore jobs are fewer in count but richer in revenue per intervention because vessel costs, pressure control, and campaign complexity are much higher. Brazil, the Gulf of Mexico, Norway, the UK North Sea, Malaysia, and parts of the Middle East anchor this segment. Recent Petrobras awards to SLB and Halliburton and Weatherford's offshore Malaysia contract confirm that offshore CT remains a strategic growth pocket. Digital modeling, catenary systems, subsea downline services, and integrated completions support are key differentiators.

Coiled Tubing Services Market by Well Type

Conventional wells represented an estimated 54.0% share in 2025, or USD 4.26 Billion. The segment remains large because national oil companies and offshore operators still manage vast conventional field inventories that require production maintenance, cleanouts, and selective remedial work. Demand is strongest in the Middle East, Latin America, offshore Africa, and legacy North Sea and Gulf of Mexico assets. Providers with offshore and brownfield engineering depth win most of this work.

Unconventional wells accounted for an estimated 31.0% share in 2025, or USD 2.44 Billion. North America still dominates the segment, but Saudi unconventional gas is becoming a major second growth pole. The segment depends on fast fleet turns, pumping integration, and longer-reach capability. It is more cyclical than conventional brownfield work, but it supports repeat intervention volume when completions activity is healthy. Baker Hughes' Aramco expansion is the clearest current proof point.

Decommissioning and P&A wells held an estimated 15.0% share in 2025, or USD 1.18 Billion. The share is smaller today, but the growth outlook is strong in Europe and selected offshore basins. CT is increasingly used to cut rig requirements and compress campaign time during selective abandonment and restoration work. Archer's and Halliburton's recent scope expansion in P&A-related activity supports this direction.

Regional Analysis

North America Coiled Tubing Services Market

North America held 53.3% of the Coiled Tubing Services Market in 2025, equal to about USD 4.20 Billion. The US drives most of that total through shale, mature land wells, and deep service infrastructure. Canada adds a strong second pillar through basin-focused intervention and completion support, while Mexico contributes offshore demand. Public market data identifies North America as the global leader in 2025, and the region remains structurally advantaged by fleet density, faster mobilization, and operator familiarity with CT-based workflows. STEP, Trican, Calfrac, KLX, Halliburton, Baker Hughes, and SLB all maintain strong positions. The US remains service-intensive even as commodity prices move because operators keep prioritizing low-cost production maintenance and output protection.

Country-wise, the US remains the dominant market because the Permian, Eagle Ford, Bakken, and other mature unconventional basins generate repeat cleanout, circulation, and stimulation-linked CT demand. Canada remains important for deep-capacity land fleets and integrated fracturing plus CT programs. Mexico gains relevance through Trion and Gulf activity. Regulatory pressure in North America is more about safety, emissions, and cost control than outright intervention limits, so service providers are responding with faster deployment, digital modeling, and lower-footprint equipment.

Europe Coiled Tubing Services Market

Europe accounted for an estimated 14.8% of the Coiled Tubing Services Market in 2025, or USD 1.17 Billion. The region is smaller than North America but more specialized. Norway, the UK, Germany, and the Netherlands matter most, with Norway and the UK clearly dominating oilfield service demand. Europe's CT demand leans toward offshore well intervention, late-life asset support, and P&A-related activity rather than large-scale land drilling. Norway is especially important because national production remains strategically valuable to Europe, and official data showed petroleum investment peaking in 2025 before easing in 2026. That still supports a high level of intervention and maintenance work.

Norway anchors the regional market through North Sea intervention and plug-and-abandonment scope, and Archer remains highly relevant there. The UK stays important in mature offshore basins and well integrity programs. Germany contributes marginally through smaller onshore and service engineering demand, while the Netherlands adds gas-field support and offshore engineering relevance. Europe's regulatory environment is tougher on emissions, safety, and decommissioning compliance than most regions, which increases demand for lower-footprint, rigless intervention methods. That supports CT adoption where operators need faster interventions with smaller surface spreads.

Asia Pacific Coiled Tubing Services Market

Asia Pacific represented an estimated 13.9% of the Coiled Tubing Services Market in 2025, or USD 1.10 Billion. The region is diverse. China, Australia, India, and Malaysia are the key strategic countries. China and India support steady onshore brownfield and gas activity. Australia contributes gas and mature well work. Malaysia stands out for offshore intervention and integrated well services. Growth in Asia Pacific is tied to gas security, brownfield optimization, and selective offshore investment rather than a single basin story.

China remains the largest country market in the region because of its broad upstream base and continuing pressure to sustain domestic supply. Australia supports intervention work through gas-oriented assets and long-life field management. India stays relevant through national operators and continued well servicing demand, including tenders for CT-linked service packages. Malaysia is rising as offshore intervention work deepens, with Weatherford highlighting a three-year thru-tubing services contract there in 2025. The region's policy framework centers on energy security and domestic output support, which tends to favor brownfield interventions over purely speculative drilling campaigns.

Latin America Coiled Tubing Services Market

Latin America held an estimated 10.7% of the Coiled Tubing Services Market in 2025, or USD 0.84 Billion. Brazil, Mexico, Argentina, and Colombia are the most relevant countries. Brazil dominates by a wide margin due to Petrobras-led offshore programs, deepwater well construction, and intervention demand across the Campos and Santos basins. Petrobras awarded SLB an USD 800 million three-year offshore services contract in December 2024, and Halliburton also secured intervention and drilling awards tied to Brazil. Those contract flows make Latin America one of the clearest offshore CT growth zones.

Brazil is the regional anchor. Mexico adds strategic offshore value through Trion and Gulf activity. Argentina remains more cyclical because shale and pressure-pumping swings affect CT utilization and margins. Colombia remains a smaller but steady mature-field market. Political and budget volatility still create risk across the region, but brownfield economics and national production targets keep intervention demand intact.

Middle East & Africa Coiled Tubing Services Market

Middle East & Africa accounted for an estimated 7.3% of the Coiled Tubing Services Market in 2025, equal to roughly USD 0.58 Billion. The region remains smaller in global revenue than North America because large national fields often have longer-cycle development programs, but the strategic upside is high. Saudi Arabia, the UAE, South Africa, and Oman are the most relevant markets in this framework. Saudi Arabia is the key growth engine because unconventional gas and brownfield work are lifting demand for high-spec intervention and underbalanced CT drilling. Public disclosures from Baker Hughes and SLB show that Aramco continues to allocate major contracts that directly support CT-linked service growth.

Saudi Arabia leads through unconventional gas and integrated well services. The UAE remains strong in brownfield optimization and offshore maintenance. Oman contributes through mature field intervention and land-based service demand. South Africa is smaller today but retains long-term offshore optionality and regional service relevance. Policy in the region remains supportive of upstream capacity growth, gas monetization, and field-life extension. That benefits CT service lines because they fit lower-footprint, production-focused intervention strategies.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Service

- Well Intervention and Production

- Drilling

- Completion

- Other Services and P&A Support

By Operation

- Circulation and Cleanout

- Pumping

- Logging

- Perforation

By Application

- Onshore

- Offshore

By Well Type

- Conventional Wells

- Unconventional Wells

- Decommissioning and P&A Wells

Regional Analysis and Coverage

- US

| Report Attribute | Details |

| Market size (2026) | USD 3.8 B |

| Forecast Revenue (2034) | USD 7 B |

| CAGR (2026-2034) | 4% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Service (Well Intervention and Production, Drilling, Completion, Other Services and P&A Support), By Operation (Circulation and Cleanout, Pumping, Logging, Perforation), By Application (Onshore, Offshore), By Well Type (Conventional Wells, Unconventional Wells, Decommissioning and P&A Wells) |

| Research Methodology |

|

| Regional scope | US |

| Competitive Landscape | SLB, HALLIBURTON, BAKER HUGHES, WEATHERFORD, NOV, TRICAN WELL SERVICE, STEP ENERGY SERVICES, CALFRAC WELL SERVICES, ARCHER, KLX ENERGY SERVICES, EXPRO, SUPERIOR ENERGY SERVICES, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Operation (Circulation & Cleanout, Pumping, Logging, Perforation), By Application (Onshore, Offshore), By Well Type (Conventional Wells, Unconventional Wells, Decommissioning & P&A Wells) Industry Region & Key Players – Market Segment Overview, Competitive Landscape, Oilfield Service Trends, Market Dynamics & Forecast 2025–2034")

, By Operation (Circulation & Cleanout, Pumping, Logging, Perforation), By Application (Onshore, Offshore), By Well Type (Conventional Wells, Unconventional Wells, Decommissioning & P&A Wells) Industry Region & Key Players – Market Segment Overview, Competitive Landscape, Oilfield Service Trends, Market Dynamics & Forecast 2025–2034")

, By Operation (Circulation & Cleanout, Pumping, Logging, Perforation), By Application (Onshore, Offshore), By Well Type (Conventional Wells, Unconventional Wells, Decommissioning & P&A Wells) Industry Region & Key Players – Market Segment Overview, Competitive Landscape, Oilfield Service Trends, Market Dynamics & Forecast 2025–2034")

Frequently Asked Questions

How big is the US Coiled Tubing Services Market?

The US Coiled Tubing Services Market was valued at USD 3.8 Billion in 2025 and is projected to reach USD 7 Billion by 2034, growing at a CAGR of 4%. Explore market trends, well intervention technologies, North America’s dominance, key drivers, competitive landscape, and future opportunities in oilfield services.

Who are the major players in the US Coiled Tubing Services Market?

SLB, HALLIBURTON, BAKER HUGHES, WEATHERFORD, NOV, TRICAN WELL SERVICE, STEP ENERGY SERVICES, CALFRAC WELL SERVICES, ARCHER, KLX ENERGY SERVICES, EXPRO, SUPERIOR ENERGY SERVICES, Others

Which segments covered the US Coiled Tubing Services Market?

By Service (Well Intervention and Production, Drilling, Completion, Other Services and P&A Support), By Operation (Circulation and Cleanout, Pumping, Logging, Perforation), By Application (Onshore, Offshore), By Well Type (Conventional Wells, Unconventional Wells, Decommissioning and P&A Wells)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

US Coiled Tubing Services Market

Published Date : 06 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date