- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Vapor Recovery Unit Market Size & Forecast 2034 | CAGR 5.9%

Global Vapor Recovery Unit Market Size, Share, Growth & Industry Analysis By Technology (Adsorption, Absorption, Condensation, Membrane Separation, Hybrid Systems), By Application (Storage Tank Vapor Recovery, Loading Rack & Terminal Recovery, Process Vents, Transportation & Mobile Recovery), By End-Use Industry (Oil & Gas, Chemicals & Petrochemicals, Fuel Retail & Terminals, Wastewater & Industrial), By Operation (Upstream, Midstream, Downstream) Industry Trends, Competitive Landscape & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

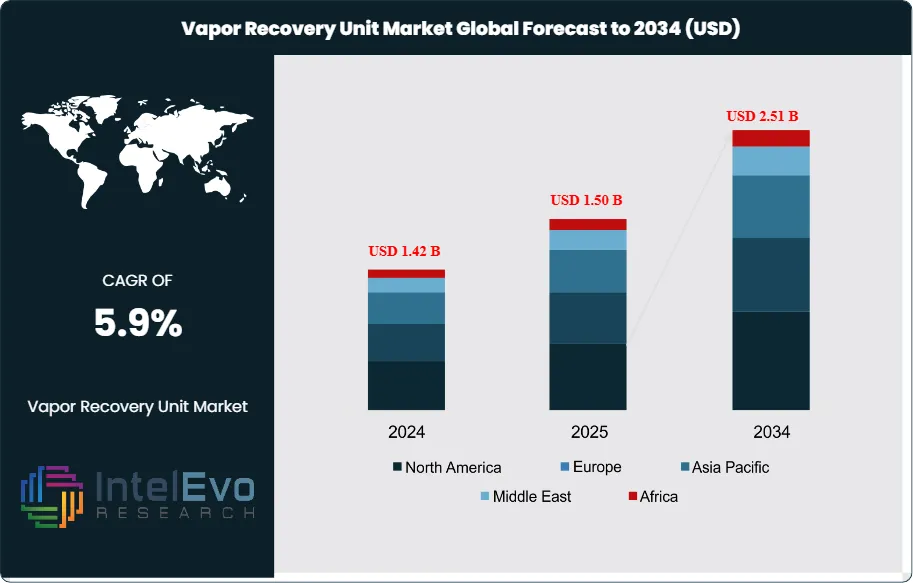

| USD 1.50 Billion | USD 2.51 Billion | 5.9% | North America, 31.0% |

The Vapor Recovery Unit Market was valued at approximately USD 1.42 Billion in 2024 and reached USD 1.50 Billion in 2025. The market is projected to grow to USD 2.51 Billion by 2034, expanding at a CAGR of 5.9% during the forecast period from 2026 to 2034.This represents an absolute dollar opportunity of USD 1.01 Billion over the analysis period. The Vapor Recovery Unit Market is expanding because operators now treat hydrocarbon vapor capture as both an emissions-control requirement and a product-recovery opportunity. U.S. EPA guidance states that vapor recovery units are used to capture methane emissions from storage tanks and other low-pressure vented sources across oil and gas operations, while long-standing EPA technical material notes that these systems can capture up to 95% of hydrocarbon vapors vented from tanks. That dual effect is shaping procurement across upstream tank batteries, midstream terminals, bulk gasoline loading, refining, and petrochemical handling systems.

Get More Information about this report -

Request Free Sample ReportThe Vapor Recovery Unit Market is also being pushed by tighter methane and VOC compliance. In the United States, EPA rules finalized in July 2024 require bulk gasoline terminals with vapor recovery units to install and operate continuous emissions monitoring systems under stricter performance standards. EPA compliance material for NSPS OOOOb also reinforces tighter requirements for closed vent systems and control routing at affected oil and gas facilities. In Europe, Regulation (EU) 2024/1787 established a formal framework for methane measurement, monitoring, reporting, verification, leak detection, and tighter limits on venting and flaring across the energy sector. These policy moves are shifting capital toward mechanical VRUs, activated-carbon systems, hybrid vapor recovery trains, and digital monitoring packages that can document performance in real time.

Demand patterns differ by end market. Oil and gas remains the largest revenue source because storage tanks, separators, dehydrators, compressor sites, and pipeline pigging operations generate recoverable vapors at scale. Terminals and fuel distribution remain the second major demand center because gasoline loading and unloading systems must control benzene-rich VOC streams. California’s vapor recovery program still covers service stations, tanker trucks, bulk plants, and terminals. India has also widened the addressable market through vapour recovery mandates in million-plus cities and high-volume fuel stations under national air-quality measures. These regulations create steady retrofit demand, not only greenfield demand.

Technology selection is becoming more segmented. Activated-carbon adsorption remains the workhorse for terminals because it handles variable flows and high recovery efficiency. Mechanical compression-based vapor recovery remains strong in oilfield tank vapor applications where recovered gas can be routed to sales, fuel, or processing. Hybrid packages that combine vapor recovery with combustion backup are gaining share where uptime, permit certainty, and gas composition vary widely. Suppliers are also adding CEM, CIM, PLC upgrades, and remote diagnostics because downtime now carries a regulatory cost as well as a lost-product cost. North America leads current spending, while Asia Pacific is the fastest-expanding build base for new terminals and petrochemical infrastructure. Europe remains regulation-led, and the Middle East is growing from downstream expansion and stricter venting control at hydrocarbon facilities.

, By Application (Storage Tank Vapor Recovery, Loading Rack & Terminal Recovery, Process Vents, Transportation & Mobile Recovery), By End-Use Industry (Oil & Gas, Chemicals & Petrochemicals, Fuel Retail & Terminals, Wastewater & Industrial), By Operation (Upstream, Midstream, Downstream) Industry Trends, Competitive Landscape & Forecast 2026–2034")

Key Takeaways

- Market Growth:Vapor Recovery Unit Market revenue stands at USD 1.50 Billion in 2025 and is projected to reach USD 2.51 Billion by 2034, reflecting a 5.9% CAGR across 2025-2034. The expansion is tied to methane-control rules, gasoline vapor standards, and wider use of vapor capture at storage and loading assets.

- Segment Dominance :The Vapor Recovery Unit Market by technology is led by adsorption systems with a 34.0% share in 2025, equal to about USD 0.51 Billion. Activated-carbon systems remain the preferred choice for terminal loading and multi-product vapor streams because they deliver high capture efficiency and wide turndown capability.

- Segment Dominance:The Vapor Recovery Unit Market by application is led by storage tank vapor recovery with a 39.0% share in 2025, or about USD 0.59 Billion. EPA guidance specifically identifies crude oil and condensate tanks as major low-pressure vent sources suited for VRU deployment.

- Driver:The main growth driver is the tightening of methane and VOC controls. EPA technical material shows VRUs can capture up to 95.0% of hydrocarbon vapors, while new terminal rules finalized in July 2024 added continuous monitoring requirements for VRU-equipped bulk gasoline terminals.

- Restraint:The main restraint is project economics at low-throughput sites. EPA case material shows strong returns only when vapor volumes are sufficient, which limits deployment in fragmented small-field assets and low-utilization loading systems.

- Opportunity:The biggest opportunity sits in monitored, compliance-ready retrofits. India alone reported installation of vapour recovery systems at 3,256 petrol pumps in Delhi-NCR under air-quality actions, while Delhi reached 392 equipped fuel stations in 2025.

- Trend:The dominant trend is the pairing of vapor recovery with digital measurement and service contracts. Zeeco and Cimarron both market continuous monitoring packages for carbon VRUs, and downtime reduction through PLC and retrofit work is becoming a buying criterion.

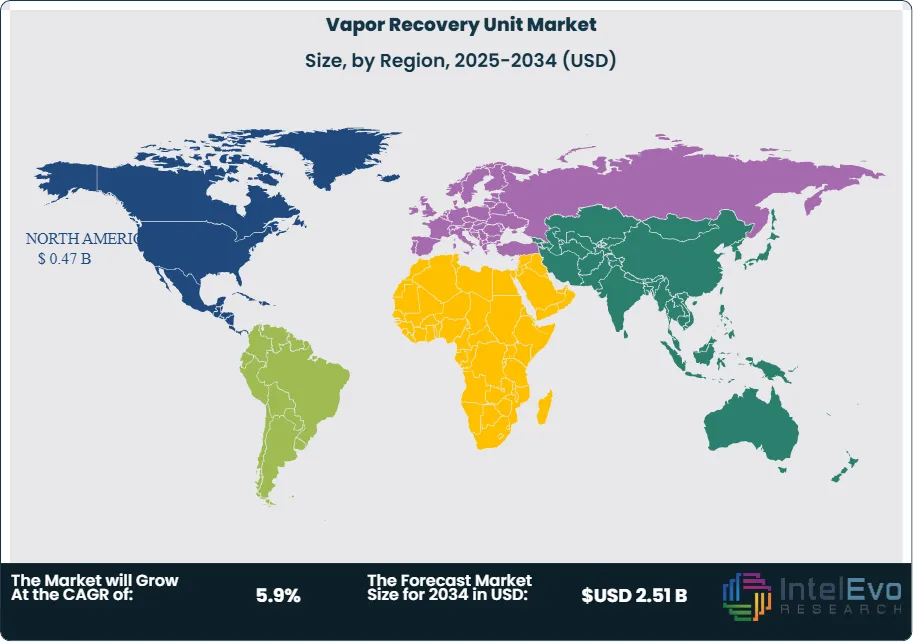

- Regional Analysis:North America leads the Vapor Recovery Unit Market with a 31.0% share and about USD 0.47 Billion in 2025. The region benefits from EPA methane rules, gasoline terminal regulation, dense oilfield storage infrastructure, and California vapor-control enforcement.

Competitive Landscape Overview

The Vapor Recovery Unit Market is moderately consolidated. The top four players account for an estimated 31.0% of 2025 revenue, with competition shaped by technology depth, field-service reach, terminal loading expertise, and emissions compliance support. John Zink, Zeeco, Cimarron AEREON, and OPW hold the strongest installed base positions across oil and gas, terminals, and downstream transfer systems. Competitive intensity rose through 2024-2026 as suppliers added monitoring packages, service upgrades, regional expansion, and bolt-on deals linked to emissions equipment and vapor handling.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

|---|---|---|---|---|---|

| John Zink | United States | Leader | Crude Oil Vapor Recovery System | North America | Expanded 2025 vapor-control promotion and service reach through ILTA 2025 and regional support across Asia Pacific and the Middle East. |

| Zeeco | United States | Leader | VRU Continuous Emissions Monitoring Systems | North America | Announced its Advanced Research Complex in February 2025 and completed the Devco Process Heaters acquisition in February 2026. |

| Cimarron AEREON | United States / Italy | Leader | Mechanical and Carbon-Based Vapor Recovery | North America, Middle East | Announced a strategic partnership with Bell Supply in December 2025 to expand VRU rental access across major U.S. basins. |

| OPW Engineered Systems | United States | Leader | Terminal Loading Arms and Vapor Recovery Adaptors | North America | Launched Loading Arm Central in January 2025 to support faster installation and maintenance for terminal systems. |

| Petrogas Systems | United States | Challenger | Hydrocarbon Vapor Recovery Systems | North America | Continued targeted deployment in hydrocarbon and loading applications during 2025 through engineered packaged solutions. |

| Carbtrol | United States | Challenger | Carbon Adsorption Vapor Recovery Systems | North America | Expanded focus on hydrocarbon and solvent vapor applications through modular carbon recovery offerings in 2025. |

| Cool Sorption | United States | Challenger | Refrigerated Vapor Recovery Systems | North America | Maintained niche position in condensation-led solvent and hydrocarbon recovery projects through 2025. |

| S&S Technical | United States | Niche Player | Vapor Recovery and Loading Control Packages | North America | Continued supply of packaged terminal and loading-vapor systems in 2025 across fuel handling markets. |

| Tecam | Spain | Niche Player | Vapour Recovery for Tank Storage | Europe | Showcased vapour recovery and emissions-abatement solutions at StocExpo 2025 in Rotterdam. |

| Flowco | United States | Niche Player | Oilfield Vapor Recovery Unit Systems | North America | Completed the acquisition of HPGL and VRU systems from Archrock in August 2025. |

By Technology

The Vapor Recovery Unit Market by technology is led by adsorption systems, which account for 34.0% of 2025 revenue, or USD 0.51 Billion. These systems are strongest in gasoline terminals, chemical loading, and multi-component hydrocarbon service because activated carbon handles variable flow and concentration ranges well. Zeeco states that activated-carbon vapor recovery remains a widely accepted approach with turndown from 0% to 100% of flow and inlet hydrocarbon concentration. Absorption systems hold 27.0%, or USD 0.41 Billion, and remain relevant where liquid absorbents fit the process scheme and recovered hydrocarbons can be integrated downstream. Condensation systems account for 22.0%, or USD 0.33 Billion, and perform best in solvent-rich or temperature-controlled streams. Membrane systems hold 10.0%, or USD 0.15 Billion, while hybrid systems represent 7.0%, or USD 0.11 Billion, largely in projects that combine vapor recovery, combustion backup, and digital monitoring. The strongest share gain through 2034 should come from hybrid and monitored adsorption packages because new rules increasingly require both capture and proof of compliant performance.

By Application

The Vapor Recovery Unit Market by application is led by storage tank vapor recovery at 39.0% of 2025 revenue, or USD 0.59 Billion. EPA guidance identifies crude oil and condensate tanks as major sources of low-pressure methane and VOC emissions, making tank batteries the clearest payback case when gas handling infrastructure is available. Loading racks and bulk terminals represent 26.0%, or USD 0.39 Billion. This segment is growing because terminal operators must control gasoline and hydrocarbon vapors during truck, rail, and marine transfer, and terminal permits are becoming more measurement-intensive. Process vents from compressors, dehydrators, separators, and pigging operations account for 21.0%, or USD 0.32 Billion. Transportation and mobile recovery applications, including tanker and retail-fuel vapor handling interfaces, hold 14.0%, or USD 0.21 Billion. Storage applications will remain dominant because they combine continuous emission streams, simple gas monetization routes, and direct regulatory exposure. Loading applications should record the fastest gains in Europe and India as vapor control at terminals and fuel distribution sites tightens.

By End-Use Industry

The Vapor Recovery Unit Market by end-use industry is led by oil and gas with a 46.0% share in 2025, equal to USD 0.69 Billion. This reflects emissions control needs at upstream production sites, gathering assets, compressor stations, and hydrocarbon storage infrastructure. Chemicals and petrochemicals hold 29.0%, or USD 0.44 Billion, because solvent and hydrocarbon vapor capture supports both compliance and raw-material recovery. Terminals and fuel retail account for 17.0%, or USD 0.26 Billion, supported by gasoline marketing rules, tank-truck interfaces, and Stage I and Stage II vapor-control programs. Wastewater, landfill, RNG, and other industrial uses represent 8.0%, or USD 0.12 Billion. The oil and gas segment will keep the largest revenue share through 2034, but chemicals and terminals will post strong incremental demand because these users are more likely to specify continuous monitoring, carbon polishing, and documented destruction or recovery performance in procurement packages.

By Operation

The Vapor Recovery Unit Market by operation shows midstream and terminal assets leading with 37.0% of 2025 revenue, or USD 0.56 Billion. These assets include bulk storage, gasoline terminals, transfer racks, and pipeline-linked facilities where vapor composition is predictable and compliance risk is high. Downstream refining and petrochemical operations follow at 32.0%, or USD 0.48 Billion, driven by storage, blending, and hydrocarbon transfer controls. Upstream production holds 31.0%, or USD 0.47 Billion, because tank battery emissions remain widespread but project selection is more volume-sensitive. Midstream and terminal operations are pulling ahead because 2024-2025 rulemaking increased attention on continuous emissions monitoring and documented control at gasoline and hydrocarbon transfer points. Upstream still offers the deepest installed-base opportunity, but growth is more uneven and tied to gas prices, produced-volume consistency, and field electrification or gathering access.

Regional Analysis

North America

The Vapor Recovery Unit Market in North America accounts for 31.0% of 2025 revenue, or USD 0.47 Billion. The United States drives nearly all regional demand because EPA methane rules, bulk-terminal VOC standards, and dense tank infrastructure create steady retrofit and service activity. California adds a separate compliance pull through its vapor recovery program for gasoline dispensing facilities, tanker trucks, bulk plants, and terminals. Canada supports demand through oil sands, liquids handling, and petrochemical storage, while Mexico remains relevant through fuel distribution and cross-border terminal assets. North America also has the deepest supplier base, led by John Zink, Zeeco, OPW, Cimarron, and a wide field-service network in Texas and the Permian. The region should retain leadership through 2034 because it combines regulatory pressure, monetizable recovered gas, and a strong installed base that needs upgrades, parts, and monitoring systems.

Asia Pacific

The Vapor Recovery Unit Market in Asia Pacific accounts for 28.0% of 2025 revenue, or USD 0.42 Billion. China leads because of refinery, terminal, and petrochemical expansion. India is the strongest regulation-led growth market in the region, supported by national clean-air actions that require vapour recovery systems in new and existing high-volume fuel stations and by wider rollout in major cities. Japan remains important for chemicals, refining, and terminal-grade emissions control, while South Korea supports demand through petrochemical and export-terminal infrastructure. Asia Pacific is also becoming a stronger manufacturing and service base for emissions equipment. John Zink highlights local offices across China, Japan, South Korea, India, Singapore, and Australia, supported by China-based manufacturing for lower lead times. That regional supply chain strengthens Asia Pacific’s growth case through 2034.

Europe

The Vapor Recovery Unit Market in Europe accounts for 24.0% of 2025 revenue, or USD 0.36 Billion. Europe’s demand is driven less by new oilfield development and more by strict methane, VOC, and industrial-emissions compliance. Regulation (EU) 2024/1787 is the central demand trigger because it establishes measurement, monitoring, reporting, leak detection, and tighter venting and flaring obligations across the energy sector. Germany, France, the United Kingdom, and Italy are the most relevant country markets because they combine refining, chemicals, tank storage, and transport-fuel infrastructure. Europe also shows stronger demand for documented performance, service availability, and retrofit engineering than for simple low-cost packages. That favors suppliers with deep compliance engineering and local field support. Europe should remain the second-largest retrofit-led revenue pool through 2034, especially in terminals, refining, chemicals, and methane-sensitive gas assets.

Middle East & Africa

The Vapor Recovery Unit Market in Middle East & Africa accounts for 10.0% of 2025 revenue, or USD 0.15 Billion. Saudi Arabia and the UAE lead regional spending through refinery, gas-processing, storage, and export infrastructure. South Africa provides a smaller but relevant fuel-distribution and industrial-vapor control market. The region’s growth case rests on stricter air-quality control at hydrocarbon facilities and on the business value of capturing recoverable vapors instead of routing them to destruction. John Zink and AEREON both emphasize regional support in the Middle East, which matters because local service response is a major buying factor for operators that cannot absorb downtime at export-linked assets. Growth remains below North America and Asia Pacific because standards differ widely by country, but the installed base opportunity is increasing in refining, terminals, and hydrocarbon storage.

Latin America

The Vapor Recovery Unit Market in Latin America accounts for 7.0% of 2025 revenue, or USD 0.11 Billion. Brazil leads because of refining, fuel terminals, and petrochemical handling. Mexico ranks second because of terminal infrastructure and fuel logistics, while Argentina remains relevant through liquids storage and hydrocarbon transfer projects. The regional market remains smaller because compliance enforcement is uneven and many projects still favor lower-capex combustion controls before full recovery systems. Even so, retrofit demand is building in fuel distribution and storage, especially where operators can show direct product recovery and payback. Latin America should post steady, not rapid, growth through 2034, with the best opportunities in high-throughput terminals, chemical plants, and selected oilfield storage clusters.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Technology

- Adsorption

- Absorption

- Condensation

- Membrane Separation

- Hybrid Systems

By Application

- Storage Tank Vapor Recovery

- Loading Rack and Terminal Vapor Recovery

- Process Vents

- Transportation and Mobile Recovery

By End-Use Industry

- Oil and Gas

- Chemicals and Petrochemicals

- Terminals and Fuel Retail

- Wastewater, Landfill, RNG, and Other Industrial

By Operation

- Midstream and Terminals

- Downstream Refining and Petrochemicals

- Upstream Production

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 1.50 B |

| Forecast Revenue (2034) | USD 2.51 B |

| CAGR (2025-2034) | 5.9% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Technology, (Adsorption, Absorption, Condensation, Membrane Separation, Hybrid Systems), By Application, (Storage Tank Vapor Recovery, Loading Rack and Terminal Vapor Recovery, Process Vents, Transportation and Mobile Recovery), By End-Use Industry, (Oil and Gas, Chemicals and Petrochemicals, Terminals and Fuel Retail, Wastewater, Landfill, RNG, and Other Industrial), By Operation, (Midstream and Terminals, Downstream Refining and Petrochemicals, Upstream Production) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | JOHN ZINK, ZEECO, CIMARRON AEREON, OPW ENGINEERED SYSTEMS, PETROGAS SYSTEMS, CARBTROL, COOL SORPTION, S&S TECHNICAL, TECAM, FLOWCO, ECO VAPOR RECOVERY SYSTEMS, JESSCO SOLUTIONS, OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Storage Tank Vapor Recovery, Loading Rack & Terminal Recovery, Process Vents, Transportation & Mobile Recovery), By End-Use Industry (Oil & Gas, Chemicals & Petrochemicals, Fuel Retail & Terminals, Wastewater & Industrial), By Operation (Upstream, Midstream, Downstream) Industry Trends, Competitive Landscape & Forecast 2026–2034")

, By Application (Storage Tank Vapor Recovery, Loading Rack & Terminal Recovery, Process Vents, Transportation & Mobile Recovery), By End-Use Industry (Oil & Gas, Chemicals & Petrochemicals, Fuel Retail & Terminals, Wastewater & Industrial), By Operation (Upstream, Midstream, Downstream) Industry Trends, Competitive Landscape & Forecast 2026–2034")

, By Application (Storage Tank Vapor Recovery, Loading Rack & Terminal Recovery, Process Vents, Transportation & Mobile Recovery), By End-Use Industry (Oil & Gas, Chemicals & Petrochemicals, Fuel Retail & Terminals, Wastewater & Industrial), By Operation (Upstream, Midstream, Downstream) Industry Trends, Competitive Landscape & Forecast 2026–2034")

Frequently Asked Questions

How big is the Vapor Recovery Unit Market?

Global vapor recovery unit market valued at USD 1.42B in 2024, reaching USD 2.51B by 2034, growing at a CAGR of 5.9% from 2026–2034.

Who are the major players in the Vapor Recovery Unit Market?

JOHN ZINK, ZEECO, CIMARRON AEREON, OPW ENGINEERED SYSTEMS, PETROGAS SYSTEMS, CARBTROL, COOL SORPTION, S&S TECHNICAL, TECAM, FLOWCO, ECO VAPOR RECOVERY SYSTEMS, JESSCO SOLUTIONS, OTHERS

Which segments covered the Vapor Recovery Unit Market?

By Technology, (Adsorption, Absorption, Condensation, Membrane Separation, Hybrid Systems), By Application, (Storage Tank Vapor Recovery, Loading Rack and Terminal Vapor Recovery, Process Vents, Transportation and Mobile Recovery), By End-Use Industry, (Oil and Gas, Chemicals and Petrochemicals, Terminals and Fuel Retail, Wastewater, Landfill, RNG, and Other Industrial), By Operation, (Midstream and Terminals, Downstream Refining and Petrochemicals, Upstream Production)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date