- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Vegan Pet Food Market Size, Growth & Forecast | CAGR 7.4%

Global Vegan Pet Food Market Size, Share & Industry Analysis By Form (Organic, Conventional), By Pet Type (Dog, Puppy, Adult, Senior, Cat, Kitten, Birds, Others), By Product Type (Dry Pet Food, Wet Pet Food, Treats & Snacks), By Distribution Channel (Supermarkets & Hypermarkets, Specialty Stores, Online Sales) Industry Region & Key Players – Segment Overview, Market Drivers, Restraints, Competitive Strategies, Emerging Trends & Forecast 2025–2034

Report Overview

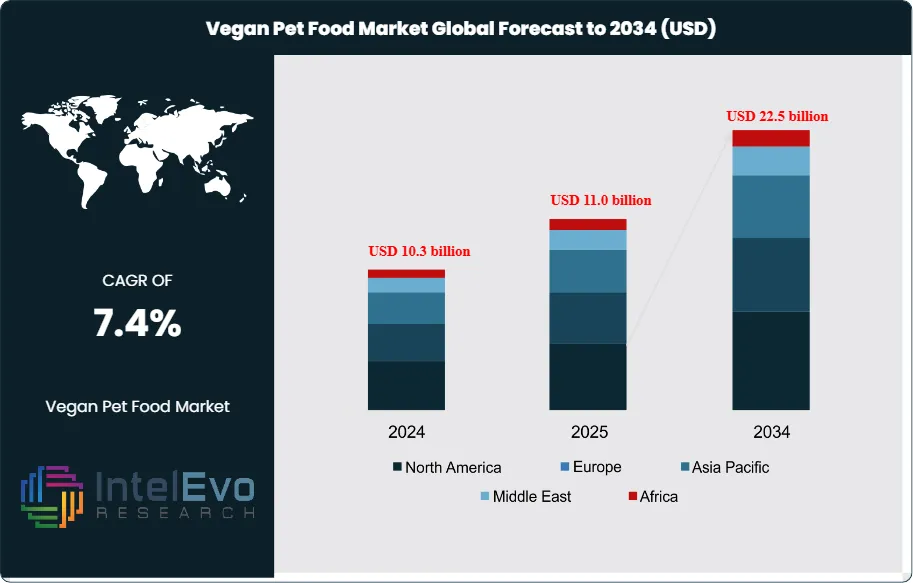

The Vegan Pet Food Market is valued at approximately USD 11.0 billion in 2025 and is projected to reach around USD 22.5 billion by 2034, expanding at a compound annual growth rate (CAGR) of about 7.4% during the forecast period from 2026 to 2034. Market growth is driven by rising pet humanization trends, increasing adoption of plant-based lifestyles among pet owners, and growing awareness of sustainability and ethical sourcing in pet nutrition. In addition, advancements in plant-based protein formulations, improved nutritional completeness, and expanding availability through online and specialty retail channels are accelerating adoption, positioning the market for strong and sustained global expansion. This expansion reflects a steady shift in pet nutrition toward plant-based formulations aligned with health, environmental, and ethical priorities among pet owners.

Get More Information about this report -

Request Free Sample ReportVegan pet food consists of plant-based recipes that replace meat, dairy, and other animal inputs with legumes, grains, vegetables, oils, and synthetic amino acids to achieve complete and balanced nutrition. Demand rises as more pets present allergies and intolerances linked to traditional animal-based proteins, pushing households toward hypoallergenic diets. Growth in human vegan and flexitarian eating patterns reinforces this trend, as owners extend personal values and wellness preferences to companion animals.

Capital flows into plant-based and alternative-protein pet food ventures underscore the market’s evolution. Startups such as OMNI in the United Kingdom, which raised €1.3 million in 2022, and Good Dog Food, which secured about £3.6 million (USD 4.5 million) in seed funding in 2023, illustrate growing investor interest. Munich-based Vegdog attracted €3.5 million in 2021 to scale nutritionally complete vegan dog food, while Scrumbles received around £6 million (USD 7.3 million) in 2023 to expand plant-based dog food offerings. Producers increasingly use AI-driven formulation tools, precision nutrition analytics, and automated manufacturing to optimize amino acid profiles, digestibility, and palatability while controlling costs.

On the supply side, producers face challenges around ingredient price volatility, protein quality assurance, and strict compliance with pet food safety and labeling rules. Regulatory agencies closely monitor claims around “complete” and “balanced” nutrition, which raises entry barriers but also builds trust in accredited brands. Digitalization reshapes go-to-market strategies, as direct-to-consumer channels, online subscription models, and data-driven recommendation engines allow brands to target niche segments such as allergy-prone dogs or environmentally conscious urban owners.

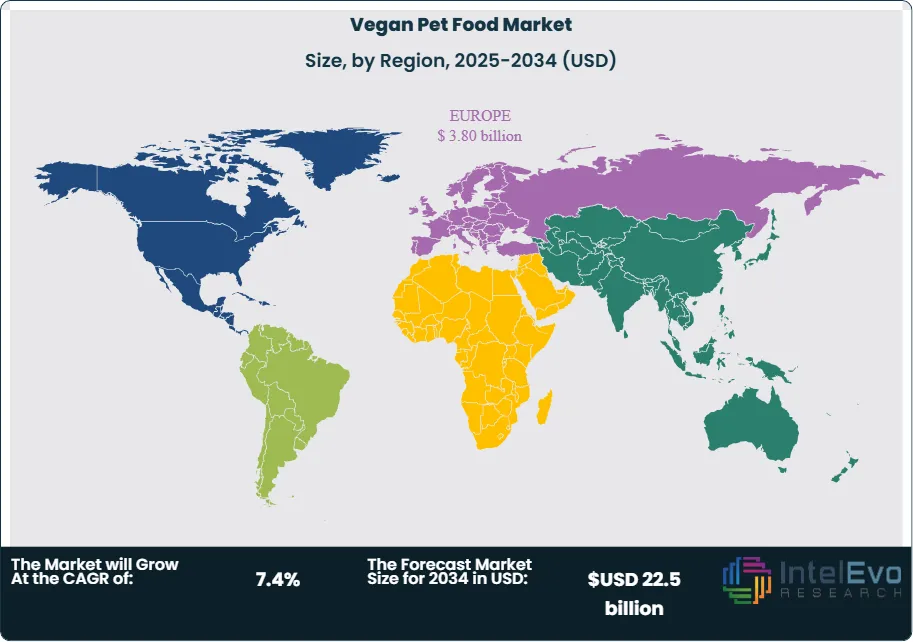

Regionally, Europe leads with an estimated USD 3.8 billion in revenue and about 36.9% share in 2024, supported by high pet humanization, strong retail penetration of vegan products, and stricter environmental policies. North America follows with a sizeable premium segment and active venture funding into alternative proteins. Asia Pacific is likely to post the fastest growth through 2034, driven by rising pet ownership, expanding middle-class incomes, and rapid adoption of e-commerce, making it an emerging hotspot for strategic investment and brand expansion.

, By Pet Type (Dog, Puppy, Adult, Senior, Cat, Kitten, Birds, Others), By Product Type (Dry Pet Food, Wet Pet Food, Treats & Snacks), By Distribution Channel (Supermarkets & Hypermarkets, Specialty Stores, Online Sales) Industry Region & Key Players – Segment Overview, Market Drivers, Restraints, Competitive Strategies, Emerging Trends & Forecast 2025–2034")

Key Takeaways

- Market Growth: The global vegan pet food market stands at 10.3 billion USD, 2024; USD 11.0 billion in 2025 and is projected to reach 22.5 billion USD, 2034, delivering a 7.4% CAGR, 2026-2034.

- Segment Dominance: Conventional vegan pet food commands a 63.2% share, 2024, confirming strong preference for familiar formulations. This segment generates estimated: 6.5 billion USD, 2024 in revenue tied to established product formats.

- Segment Dominance: Dogs represent 72.3% share, 2024 of vegan pet food demand, underscoring the focus on canine nutrition. This dominance corresponds to estimate: 7.4 billion USD, 2024 in dog-specific vegan offerings.

- Driver: Dry vegan pet food holds 56.2% share, 2024 of category sales as buyers prioritize convenience, shelf life, and storage efficiency. This format contributes estimated: 5.8 billion USD, 2024 to global revenues.

- Restraint: Supermarkets and hypermarkets account for 48.2% share, 2024 of vegan pet food distribution, reinforcing dependence on large retail chains. The remaining estimated: 51.8% share, 2024 disperses across online, specialty, and independent outlets, limiting visibility in some markets.

- Opportunity: Expanding digital and specialty retail channels could unlock estimated: 3.0 billion USD, 2030 in incremental vegan pet food sales. This expansion would build on the 10.3 billion USD, 2024 baseline and support diversification beyond conventional formats.

- Trend: Plant-based formulations continue to gain traction, with vegan products projected to reach estimated: 5.0% share of the global pet food market, 2030. This momentum aligns with a 6.7% CAGR, 2024-2034 in the vegan pet food segment.

- Regional Analysis: Europe leads with 3.8 billion USD, 2024 in vegan pet food revenue and a 36.9% share, 2024, reflecting strong adoption and retail penetration. High-growth regions such as Asia Pacific are expected to add estimated: 2.0 billion USD, 2034 in new demand over 2024-2034.

By Form

Conventional vegan pet food maintains the largest share of global demand. In 2025, conventional formats account for about 63.2 percent of total sales due to well-established production systems and broad consumer familiarity. Brands continue to scale these lines with plant-based proteins sourced from peas, lentils, soy, and other legumes. Conventional formulas remain widely available across retail channels, which supports consistent adoption in both mature and developing markets.

Growth in this segment is tied to rising concerns about food sensitivities and digestive complications in pets. Many owners are shifting to plant-based diets to address allergies, weight management, and long-term health conditions. Sustainability also plays a central role as households aim to reduce the footprint associated with traditional meat-based pet food. As a result, you see steady interest in products that meet nutritional standards while aligning with environmental values.

The outlook points to further improvement in nutrient composition, especially amino acid fortification and enhanced texture. Companies are working with veterinarians and pet nutrition experts to increase acceptance among pets and reassure owners about adequacy. Expansion in price-sensitive regions is expected as supply chains stabilize and distribution networks broaden.

By Pet Type

Dogs represent the highest share of vegan pet food consumption. In 2025, dogs account for roughly 72.3 percent of global demand. Their omnivorous nature supports easier adaptation to plant-based diets compared to cats, and this has encouraged manufacturers to advance protein blends and balanced formulations targeted at canine needs.

The category benefits from rising cases of food allergies, skin issues, and digestive concerns in dogs. Many owners view plant-based diets as a controlled solution to reduce exposure to certain animal proteins. You also see wider availability of fortified recipes that include taurine, carnitine, and omega fatty acids to support long-term health. These additions help reinforce consumer confidence and expand adoption across urban markets.

Future growth will depend on flavor improvement, palatability research, and premium offerings for puppies, adult dogs, and seniors. Companies that invest in clinical validation and vet-endorsed product ranges are positioned to strengthen share as the market matures.

By Product Type

Dry vegan pet food continues to lead global sales. In 2025, dry formats represent about 56.2 percent of the market. Owners prefer dry kibble for its ease of storage, long shelf life, and compatibility with automated feeders. Brands are also adding fortified nutrients and refined plant-based proteins to address health needs without compromising texture.

Demand rises as more households adopt sustainable and health-focused feeding routines. Dry formats remain widely stocked in supermarkets, specialty stores, and major e-commerce channels. This consistent retail presence strengthens buyer confidence and encourages repeat purchases.

The segment outlook highlights opportunities in premium blends, expanded protein sources, and flavor development. Some companies are testing emerging plant-based ingredients to improve digestibility and support new product tiers. Growth in emerging regions will rely on education campaigns and broader distribution through both online and physical retail chains.

By Distribution Channel

Supermarkets and hypermarkets remain the primary distribution points for vegan pet food. In 2025, these outlets hold about 48.2 percent of global sales. Their broad reach and competitive pricing attract buyers who prefer to compare products in person. Retail chains are increasing shelf space for plant-based pet food as interest in sustainable diets grows.

These stores offer clear labeling, ingredient comparisons, and promotional pricing that influence purchasing decisions. Many major retailers have introduced private-label vegan pet food lines, which appeal to cost-conscious households. The visibility of these products contributes to steady category expansion.

Growth opportunities include stronger in-store displays, retailer-brand partnerships, and tailored assortments for high-volume regions. Companies focused on exclusive supermarket placements and education-driven promotions can strengthen brand recognition and accelerate adoption.

By Region

Europe continues to lead the market in 2025, maintaining a share of about 36.9 percent and a value near 3.8 billion USD. High awareness of plant-based diets, stringent sustainability policies, and a strong retail ecosystem support adoption. Many pet owners in the region cite ethical and environmental considerations as primary factors in switching to vegan diets. The presence of established brands and specialty retailers reinforces market stability.

North America follows with strong demand driven by health-focused consumers and high spending on premium pet food. The United States remains a key market with a growing base of pet parents seeking plant-based formulas to address allergies and chronic conditions. Broad distribution across supermarkets and online channels contributes to consistent growth.

Asia Pacific shows the fastest long-term potential. Rising incomes, expanding pet ownership, and improving retail access support adoption in markets such as China, Japan, and Australia. Latin America and the Middle East and Africa remain in the early adoption stage. Urbanization and rising awareness of pet nutrition will support gradual expansion, especially as brands strengthen distribution networks and introduce affordable product lines.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Form

- Organic

- Conventional

By Pet Type

- Cat

- Kitten

- Senior

- Dog

- Puppy

- Adult

- Senior

- Birds

- Others

By Product Type

- Dry Pet Food

- Wet Pet Food

- Treats and Snacks

- Others

By Distribution Channel

- Supermarket/Hypermarket

- Specialty Stores

- Online Sales Channel

- Others

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 11.0 billion |

| Forecast Revenue (2034) | USD 22.5 billion |

| CAGR (2025-2034) | 7.4% |

| Historical data | 2020-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Form, (Organic, Conventional), By Pet Type, (Cat, Kitten, Senior, Dog, Puppy, Adult, Senior, Birds, Others), By Product Type, (Dry Pet Food, Wet Pet Food, Treats and Snacks, Others), By Distribution Channel, (Supermarket/Hypermarket, Specialty Stores, Online Sales Channel, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Soopa Pets, Vegeco Ltd., Antos B.V., YARRAH, Bond Pet Foods, Inc., FreshWoof – Urban Tails Pvt. Ltd., V-dog, Inc., My Aistra, Ami Planet Srl, Wild Earth Inc., Halo Pets, Anything Vegan Private Limited, THE PACK PET LIMITED, Isoropimene Zootrofe Georgios Tsappis Ltd., Benevo, Compassion Circle, Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Pet Type (Dog, Puppy, Adult, Senior, Cat, Kitten, Birds, Others), By Product Type (Dry Pet Food, Wet Pet Food, Treats & Snacks), By Distribution Channel (Supermarkets & Hypermarkets, Specialty Stores, Online Sales) Industry Region & Key Players – Segment Overview, Market Drivers, Restraints, Competitive Strategies, Emerging Trends & Forecast 2025–2034")

, By Pet Type (Dog, Puppy, Adult, Senior, Cat, Kitten, Birds, Others), By Product Type (Dry Pet Food, Wet Pet Food, Treats & Snacks), By Distribution Channel (Supermarkets & Hypermarkets, Specialty Stores, Online Sales) Industry Region & Key Players – Segment Overview, Market Drivers, Restraints, Competitive Strategies, Emerging Trends & Forecast 2025–2034")

, By Pet Type (Dog, Puppy, Adult, Senior, Cat, Kitten, Birds, Others), By Product Type (Dry Pet Food, Wet Pet Food, Treats & Snacks), By Distribution Channel (Supermarkets & Hypermarkets, Specialty Stores, Online Sales) Industry Region & Key Players – Segment Overview, Market Drivers, Restraints, Competitive Strategies, Emerging Trends & Forecast 2025–2034")

Frequently Asked Questions

How big is the Vegan Pet Food Market?

The global vegan pet food market was valued at USD 11.0 billion in 2025 and is projected to reach USD 22.5 billion by 2034, growing at a CAGR of 7.4% from 2026 to 2034, driven by pet humanization, plant-based nutrition trends, sustainable sourcing, and expanding online and specialty retail channels.

Who are the major players in the Vegan Pet Food Market?

Soopa Pets, Vegeco Ltd., Antos B.V., YARRAH, Bond Pet Foods, Inc., FreshWoof – Urban Tails Pvt. Ltd., V-dog, Inc., My Aistra, Ami Planet Srl, Wild Earth Inc., Halo Pets, Anything Vegan Private Limited, THE PACK PET LIMITED, Isoropimene Zootrofe Georgios Tsappis Ltd., Benevo, Compassion Circle, Inc.

Which segments covered the Vegan Pet Food Market?

By Form, (Organic, Conventional), By Pet Type, (Cat, Kitten, Senior, Dog, Puppy, Adult, Senior, Birds, Others), By Product Type, (Dry Pet Food, Wet Pet Food, Treats and Snacks, Others), By Distribution Channel, (Supermarket/Hypermarket, Specialty Stores, Online Sales Channel, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date