- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Vehicle Cybersecurity Market Size, Share & Forecast | CAGR 14.8%

Global Vehicle Cybersecurity Market Size, Share, Analysis By Security Domain (Vehicle & On-Board Systems, Backend & Cloud, Wireless & V2X Telecommunication, Operational Technology IIoT, Supply-Chain Security), By Solution Type (Embedded Security Software, Hardware Security Modules, VSOC Cloud Platforms, Cybersecurity Engineering Services), By Vehicle Type (Passenger, LCVs, HCVs, Electric & Hybrid Vehicles), By End-User (OEMs, Tier-1 Suppliers, Fleet Operators) Region & Key Players-Dynamics, Strategies & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

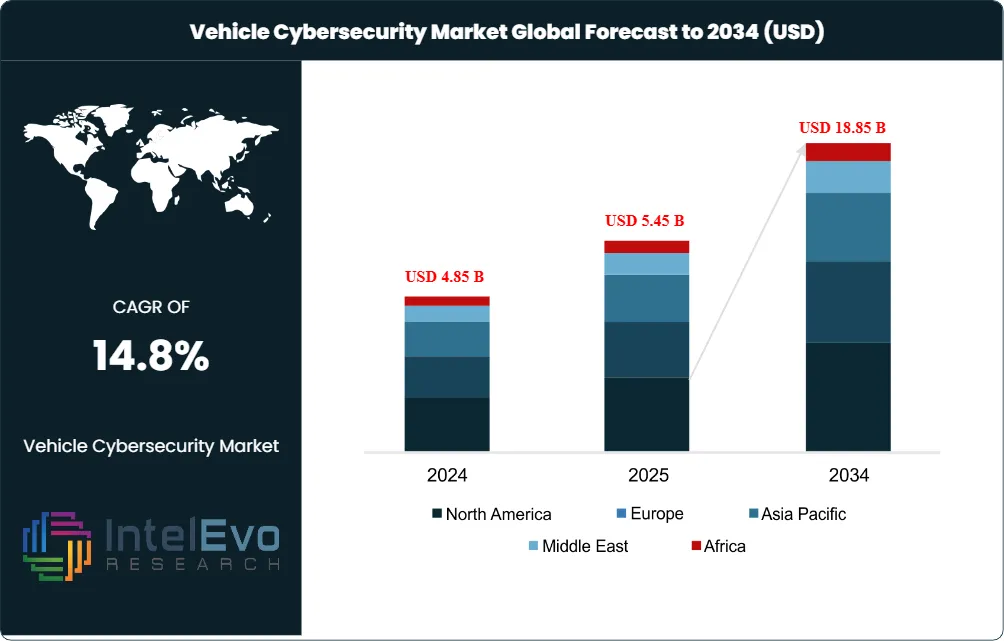

| USD 5.45 Billion | USD 18.85 Billion | 14.8% | Asia Pacific, 36.4% |

The Vehicle Cybersecurity Market was valued at USD 4.85 Billion in 2024 and USD 5.45 Billion in 2025. The market is projected to reach USD 18.85 Billion by 2034, expanding at a CAGR of 14.8% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 13.40 Billion over the analysis period.

Get More Information about this report -

Request Free Sample ReportThe vehicle cybersecurity market spans embedded security software for electronic control units (ECUs), hardware security modules (HSMs), trusted platform modules (TPMs), secure vehicle network gateways, intrusion detection and prevention systems (IDPS), cloud-based vehicle security operations center (VSOC) platforms, secure over-the-air (OTA) update management, vehicle-to-everything (V2X) communication security, secure boot and cryptographic identity management, API security for telematics backends, and managed detection and response services for connected and autonomous vehicles. Modern vehicles ship with more than 100 Million lines of code across upwards of 100 ECUs, with software faults already accounting for an increasing share of vehicle safety recall notices, reinforcing the necessity of embedded intrusion detection and encrypted firmware delivery.

Regulatory anchors are concentrated under UN Regulation No. 155 (UN R155) administered by UNECE WP.29, which became mandatory for all new vehicle types in the European Union from July 2024 and applies across 54 UNECE 1958 Agreement contracting parties. UN R156 mandates Software Update Management Systems (SUMS) for OTA security. ISO/SAE 21434 'Road vehicles - Cybersecurity engineering' provides the de facto technical framework, with most certification bodies using ISO/SAE 21434 compliance as a core criterion for R155 certification. China administers parallel GB standards, India implements AIS 189, Japan and South Korea adopt UN R155 (with South Korea using a self-certification model). U.S. NHTSA published cybersecurity best practices guidance for connected vehicles. The Upstream 2026 Global Automotive and Smart Mobility Cybersecurity Report, released February 2026, identified that ransom-related incidents accounted for 44% of all reported incidents, doubling versus 2024.

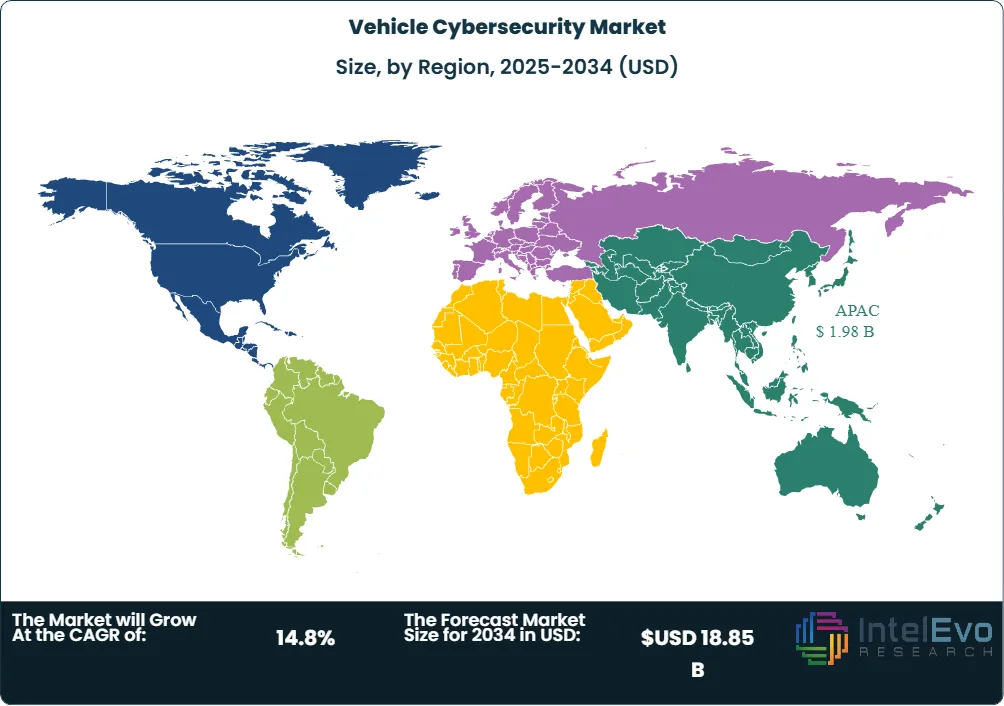

Industry consolidation accelerated through 2024-2026. Continental AG owns PlaxidityX (formerly Argus Cyber Security, acquired November 2017 for approximately USD 430 Million and rebranded August 2024) operating under the Elektrobit subsidiary. Cadence Design Systems announced intent to acquire Secure-IC in January 2025, bringing embedded security IP to automotive semiconductor customers. Upstream Security launched OceanAI in February 2025 to automate VSOC investigation and response workflows. Panasonic Automotive Systems and VicOne expanded their xCarbon partnership in August 2025 covering next-generation cockpit systems. AUTOCRYPT unveiled Automotive-CIS, a Global Integrated Cybersecurity Infrastructure Standard, at CES January 2026. VicOne recorded 405 automotive cybersecurity incidents in Q1 2026, with EV charging incidents tripling year-on-year. Regionally, Asia Pacific held 36.4% revenue share in 2025, equating to approximately USD 1.98 Billion.

Market Definition and Scope

The vehicle cybersecurity market is defined as the segment of cybersecurity, automotive electronics, and software covering technologies, processes, and services designed to protect vehicle electronic systems, communication networks, and data from unauthorized access, malicious attacks, and integrity breaches across the connected vehicle lifecycle. The market encompasses on-board security (in-vehicle ECU protection, HSMs, TPMs, secure boot, intrusion detection, runtime integrity), in-vehicle network security (CAN, LIN, FlexRay, Automotive Ethernet protection), backend and telecom security (cloud-based VSOC, API security, telematics backends), production cybersecurity (operational technology and IIoT in smart factories), and software update management.

This analysis covers vendor revenue from embedded security software licensing, hardware security module sales, professional services (consulting, integration, penetration testing, type approval support), managed detection and response subscriptions, and threat intelligence feeds. Major participants include Continental AG (Elektrobit, PlaxidityX), NXP Semiconductors, Upstream Security, Harman International (Samsung), Robert Bosch GmbH (ETAS, ESCRYPT), Cadence Design Systems (Secure-IC), VicOne (Trend Micro), Synopsys, AUTOCRYPT, Karamba Security, GuardKnox, Aurora Labs, C2A Security, RunSafe Security, BlackBerry QNX, Cisco Systems, Infineon Technologies, Vector Informatik (Microvast), Honeywell International, Broadcom, DENSO Corporation, and Panasonic Automotive Systems. Excluded from this scope are general-purpose enterprise IT cybersecurity platforms without automotive-specific features, dealer management system security, and consumer-facing identity protection products. The parent global cybersecurity software and services market reached approximately USD 220 Billion in 2025; vehicle cybersecurity represented approximately 2.5% of broader cybersecurity value.

, By Solution Type (Embedded Security Software, Hardware Security Modules, VSOC Cloud Platforms, Cybersecurity Engineering Services), By Vehicle Type (Passenger, LCVs, HCVs, Electric & Hybrid Vehicles), By End-User (OEMs, Tier-1 Suppliers, Fleet Operators) Region & Key Players-Dynamics, Strategies & Forecast 2026-2034")

Key Takeaways

- Market Growth: The vehicle cybersecurity market expanded from USD 5.45 Billion in 2025 toward a projected USD 18.85 Billion by 2034, registering a CAGR of 14.8% during the forecast period.

- Segment Dominance by Security Domain: Vehicle and on-board systems security captured approximately 46.0% revenue share in 2025, anchored by HSMs, intrusion detection, secure boot, and runtime integrity for ECUs; production OT and IIoT security is growing fastest at 25.0% CAGR through 2030.

- Segment Dominance by Solution Type: Embedded security software captured approximately 37.5% solution-type revenue share in 2025, while cloud-based security platforms are projected to grow at 25.4% CAGR through 2030, with hardware security modules anchoring the residual hardware-tier value.

- Driver: UN Regulation No. 155 mandatory enforcement for all new EU vehicle types since July 2024, ISO/SAE 21434 as the de facto engineering framework, China GB standards, India AIS 189, and Japan-Korea UN R155 adoption created compliance demand across 54 UNECE 1958 Agreement contracting parties; modern vehicles ship 100 Million+ lines of code across 100+ ECUs.

- Restraint: Auto industry faces an estimated USD 24 Billion loss exposure over five years from cyberattacks per Upstream Auto analysis, with system downtime costs from automotive cyberattacks reaching USD 1.99 Billion in H1 2023; in-vehicle integration complexity and certification timelines (typically 18-36 months for UN R155 type approval) constrain SMB Tier 2 supplier adoption.

- Opportunity: Vehicle and Smart Mobility Cybersecurity Report data showed ransom-related incidents accounted for 44% of all reported incidents in 2025 (doubling versus 2024), with EV charging incidents tripling year-on-year, expanding the addressable VSOC, API security, and managed detection market.

- Trend: AI-driven cybersecurity expanded across the OEM software-defined vehicle stack with Upstream OceanAI launched February 2025, Panasonic-VicOne xCarbon partnership expansion August 2025, and AUTOCRYPT Automotive-CIS Global Integrated Cybersecurity Infrastructure Standard unveiled at CES January 2026.

- Regional: Asia Pacific held the largest regional share at 36.4%, equating to approximately USD 1.98 Billion in 2025, anchored by China GB standards, Japan ISO/SAE 21434 adoption, South Korea UN R155 self-certification, India AIS 189, and high regional vehicle production volume.

Key Insights Summary

- Effective July 2024, UN Regulation No. 155 became compulsory for all new vehicle types submitted for EU type approval, requiring valid Cybersecurity Management System (CSMS) certification and vehicle-level cybersecurity assessment across 54 UNECE 1958 Agreement contracting parties; ISO/SAE 21434 serves as the recognized engineering framework underpinning R155 compliance.

- Upstream's 2026 Global Automotive and Smart Mobility Cybersecurity Report, published in February 2026, attributed 44% of all reported automotive cybersecurity incidents in 2025 to ransom-related activity, with the count doubling versus 2024 as organized threat actors increasingly target AI-powered backend platforms and APIs at ecosystem scale.

- VicOne tracked 405 automotive cybersecurity incidents during Q1 2026; ransomware remained the leading attack vector, EV charging incidents tripled year-over-year, and AI surfaced as an additional attack vector spanning vehicle, cloud, and API tiers.

- In January 2025 Cadence Design Systems disclosed an agreement to acquire Secure-IC, bringing embedded security IP to automotive semiconductor customers and reinforcing Cadence's position in chip-level security relevant to ISO/SAE 21434 compliance.

- Continental AG rebranded the Argus Cyber Security business as PlaxidityX in August 2024; the unit, originally purchased in November 2017 for roughly USD 430 Million, sits under Elektrobit and supports the largest global OEMs and Tier 1 suppliers from a Tel Aviv headquarters with sites in Detroit, Silicon Valley, Stuttgart, and Tokyo.

- A modern vehicle now contains more than 100 Million lines of code distributed across upwards of 100 ECUs alongside roughly 1,500 semiconductors per electric vehicle; per Upstream Auto analysis, the industry's projected five-year cyber loss exposure approaches USD 24 Billion, with H1 2023 ransomware costs reaching USD 209.6 Million, nearly twice the USD 74.7 Million logged in 2021.

Competitive Landscape Overview

The vehicle cybersecurity market is moderately consolidated at the Tier 1 supplier and semiconductor tier and competitive at the pure-play VSOC and embedded security tier. Tier 1 platform leaders include Continental AG (with Elektrobit and PlaxidityX subsidiaries), Robert Bosch GmbH (ETAS and ESCRYPT divisions), Harman International (Samsung subsidiary, SHIELD platform), DENSO Corporation, Aptiv, and Lear. Semiconductor security leaders include NXP Semiconductors (S32 platform), Infineon Technologies, STMicroelectronics, Renesas Electronics, and Cadence Design Systems (post-Secure-IC). Pure-play VSOC and SaaS leaders include Upstream Security (Herzliya, Israel; cloud-based XDR with OceanAI), VicOne (Trend Micro Tokyo subsidiary; xCarbon platform), and PlaxidityX. Embedded security and ISO/SAE 21434 toolchain vendors include Karamba Security (Israel), GuardKnox (Israel), C2A Security (Israel), RunSafe Security, BlackBerry QNX (BlackBerry Limited), Synopsys (Black Duck SBOM and fuzz testing), Vector Informatik, AUTOCRYPT (Seoul, V2X security and Cybersecurity Testing Platform), Aurora Labs, and ETAS. Industry analysis identifies 52 active automotive cybersecurity startups globally with 30 funded entities (19 with Series A+ funding); the United States hosts 19 startups, Israel 13, and Germany 5, with concentrated alumni networks from Tel Aviv University, Technion, and Israel Defense Forces Unit 8200.

Competitive Landscape Matrix

| Company Name | Headquarters | Market Position | Key Product / Solution | Geographic Strength | Recent Strategic Move |

| Continental AG (Elektrobit, PlaxidityX) | Hanover, Germany | Leader | PlaxidityX automotive cyber suite, secure OTA, EB tresos | Europe, North America, Asia Pacific | Argus rebranded as PlaxidityX in August 2024 under Elektrobit |

| NXP Semiconductors N.V. | Eindhoven, Netherlands | Leader | S32 automotive secure processor, hardware security modules | Global | Continued S32 platform expansion for software-defined vehicles in 2025 |

| Upstream Security | Herzliya, Israel | Leader | Cloud-based XDR, AutoThreat intelligence, OceanAI VSOC platform | North America, Europe, APAC | Launched OceanAI VSOC automation platform in February 2025 |

| Harman International (Samsung) | Stamford, Connecticut, USA | Leader | SHIELD vehicle cybersecurity suite, OTA management, telematics security | Global | Expanded SHIELD platform across Samsung connected device portfolio in 2025 |

| Robert Bosch GmbH (ETAS) | Stuttgart, Germany | Challenger | ETAS ESCRYPT automotive cybersecurity suite, secure HSM stack | Europe, North America, Asia Pacific | ESCRYPT integration with software-defined vehicle platforms expanded 2025 |

| Cadence Design Systems | San Jose, USA | Challenger | Embedded security IP for automotive semiconductors via Secure-IC | Global | Announced intent to acquire Secure-IC in January 2025 |

| VicOne (Trend Micro) | Tokyo, Japan | Challenger | xCarbon vehicle cyber detection, VSOC, AutoThreat Forecast | Asia Pacific, Global | Expanded Panasonic Automotive Systems xCarbon partnership in August 2025 |

| Synopsys Inc. | Sunnyvale, USA | Challenger | Black Duck SBOM, fuzz testing, automotive security testing | Global | Continued automotive ISO/SAE 21434 compliance toolchain expansion |

| AUTOCRYPT | Seoul, South Korea | Niche Player | Cybersecurity Testing Platform (CSTP), V2X security | Asia Pacific, Europe | Unveiled Automotive-CIS global cybersecurity infrastructure standard at CES January 2026 |

| Karamba Security | Hod HaSharon, Israel | Niche Player | XGuard runtime integrity, ISO/SAE 21434 toolchain | North America, Europe, Israel | Continued runtime ECU integrity deployment with Tier 1 suppliers in 2025 |

By Security Domain

The vehicle cybersecurity market by security domain is led by vehicle and on-board systems security, which captured approximately 46.0% revenue share in 2025 driven by ECU protection, HSMs, secure boot, runtime integrity, and intrusion detection across CAN, LIN, FlexRay, and Automotive Ethernet networks. Backend and telecom security captured 24.6% share, anchored by Upstream Security cloud XDR, VicOne xCarbon, and Harman SHIELD telematics protection. API security and operational technology security held 14.8% share, growing at the fastest 25.0% CAGR through 2030 driven by 5G connectivity expansion and software-defined vehicle architectures.

Production cybersecurity covering OT and IIoT in smart manufacturing environments captured 8.4% share, with OEMs including Ford and Stellantis experimenting with Zero Trust architectures within smart factories. EV charging infrastructure security represented 6.2% share, growing rapidly as VicOne reported EV charging incidents tripling year-on-year in Q1 2026. Comparison: cloud-based VSOC platforms grew at 26.8% CAGR versus 11.4% CAGR for on-premise solutions, reflecting the structural shift toward agentless cloud-based security and software-defined vehicle architectures. Procurement leads at OEMs and Tier 1 suppliers should evaluate vehicle cybersecurity vendors against three criteria: ISO/SAE 21434 certified processes mapping directly to UN R155 CSMS, UN R156 Software Update Management System (SUMS) compliance support, and concurrent China GB standards compatibility for global vehicle programs.

By Solution Type

The vehicle cybersecurity market by solution type is led by embedded security software at approximately 37.5% revenue share in 2025, anchored by intrusion detection systems integrated within vehicle ECUs, runtime integrity monitoring (Karamba XGuard), secure boot and cryptographic identity (NXP S32, Infineon AURIX), and OS-level security (BlackBerry QNX, ETAS RTA). Hardware security modules and TPMs captured 21.6% share, anchored by NXP Semiconductors, Infineon Technologies, and STMicroelectronics. Cloud-based security platforms held 18.4% share, growing at the fastest 25.44% CAGR through 2030 with Upstream Security, VicOne, and Harman SHIELD anchoring.

Professional services including consulting, integration, penetration testing, fuzz testing, and type approval support captured 14.8% share, anchored by Synopsys Black Duck, Cadence post-Secure-IC, Karamba toolchain, NCC Group, and accredited technical service auditors. Threat intelligence feeds and managed detection and response captured the residual 7.7% share, with Upstream AutoThreat, VicOne AutoThreat Forecast, and Auto-ISAC threat sharing anchoring. Procurement procurement timelines for full UN R155 type approval typically span 18 to 36 months from initial CSMS gap assessment through certification, with average enterprise cost of USD 850,000 to USD 4.2 Million for a complete program.

By Vehicle Type

The vehicle cybersecurity market by vehicle type is led by passenger vehicles at approximately 61.4% revenue share in 2025, anchored by passenger BEVs, PHEVs, and ICE connected vehicles across mass-market, premium, and luxury segments. Passenger sedan and SUV configurations dominate within the segment, with hatchbacks and crossovers representing the residual passenger split. Light commercial vehicles (LCVs) captured 17.8% share, anchored by delivery fleets, fleet operators (UPS, FedEx, DHL), and last-mile mobility providers. Heavy commercial vehicles (HCVs) including trucks, buses, and special-purpose vehicles captured 14.6% share, growing at 16.4% CAGR through 2034 driven by fleet telematics, autonomous trucking pilots, and CSMS retrofit programs.

Two-wheeler and three-wheeler connected vehicles contributed 4.2% share, anchored by India and Southeast Asia electric scooter and motorcycle deployment. Off-highway and agricultural vehicles captured the residual 2.0% share, with John Deere, AGCO, and CNH Industrial anchoring connected farm equipment cybersecurity. By electric vehicle type, battery electric vehicles (BEVs) captured the largest electric sub-segment at 58% of EV cybersecurity spend, with hybrid electric vehicles (HEVs) and plug-in hybrid electric vehicles (PHEVs) contributing the remainder.

By End-User

The vehicle cybersecurity market by end-user is led by automotive OEMs at approximately 49.6% share in 2025, anchored by direct vendor procurement at Toyota, Volkswagen Group, Stellantis, Ford, General Motors, BMW Group, Mercedes-Benz, Hyundai-Kia, Renault Group, Honda, Nissan, Tesla, BYD, NIO, Li Auto, and XPeng. OEM cybersecurity teams typically include 20 to 200 dedicated cyber engineers under a Chief Information Security Officer reporting directly to product engineering or chief technology officer functions.

Tier 1 and Tier 2 suppliers captured 28.4% share, growing at 15.1% CAGR through 2034. Tier 1 leaders including Continental AG, Bosch, Denso, ZF Friedrichshafen, Magna International, Aptiv, and Lear procure cybersecurity tooling for software components shipped to OEM platforms. Smart factory operators captured 12.4% share, growing fastest at 24.1% CAGR through 2030 driven by Industry 4.0 and Zero Trust manufacturing architectures. Aftermarket service providers and authorized dealers contributed 6.2% share, anchored by independent aftermarket telematics and diagnostic security. Government and regulatory bodies, including type approval authorities and accredited technical services, captured the residual 3.4% share.

Regional Analysis

The vehicle cybersecurity market by region is led by Asia Pacific at 36.4% revenue share in 2025, equating to approximately USD 1.98 Billion. China dominates regional value through GB standards parallel to UN R155, the world's largest connected and electric vehicle production volume, and concentrated activity at BYD, NIO, Li Auto, XPeng, Geely, SAIC, Great Wall Motors, and CATL battery integration. Japan anchors regional supply through Toyota, Honda, Nissan, Mazda, Subaru, plus Tier 1 suppliers Denso, Aisin, and Panasonic Automotive Systems integrating VicOne xCarbon. South Korea hosts Hyundai-Kia and Samsung-owned Harman International, with the country adopting UN R155 under a self-certification model. India implements AIS 189 covering CSMS requirements aligned with UN R155, with Tata Motors, Mahindra, and Ola Electric anchoring domestic activity.

Europe held 33.4% share in 2025, equivalent to approximately USD 1.82 Billion. UN R155 became mandatory for all new vehicle types in the EU from July 2024 administered by national type approval authorities (KBA in Germany, OTC in France, RDW in Netherlands, VCA in UK pre-Brexit harmonized framework). Germany hosts Continental AG (Hanover), Robert Bosch GmbH (Stuttgart), Volkswagen Group (Wolfsburg), Mercedes-Benz Group (Stuttgart), BMW Group (Munich), Porsche, Audi, ETAS (Stuttgart), and Vector Informatik (Stuttgart). France hosts Stellantis, Renault Group, and Valeo cybersecurity engineering. The Netherlands hosts NXP Semiconductors (Eindhoven). Italy hosts Stellantis Italian operations and Magneti Marelli supplier base.

North America captured 22.8% share in 2025, valued at approximately USD 1.24 Billion, with the U.S. automotive cybersecurity market alone reaching USD 1.62 Billion in 2025 by some industry analyses (representing the broader market including services). The U.S. is projected at 14.6% U.S. CAGR through 2034. NHTSA published cybersecurity best practices guidance for connected vehicles. Major OEMs include Ford, General Motors, Stellantis North America, and Tesla. Cybersecurity vendors concentrate in Detroit corridor, Silicon Valley, and Boston, with Cadence Design Systems (San Jose), Synopsys (Sunnyvale), and Harman International (Stamford) anchoring. Auto-ISAC information sharing among 30+ OEM members supports threat intelligence collaboration.

Middle East and Africa held 4.2% share in 2025, approximately USD 229 Million. The United Arab Emirates and Saudi Arabia anchor regional activity with Mubadala-backed automotive technology investments and NEOM autonomous mobility initiatives. Latin America contributed 3.2% share, valued at approximately USD 174 Million in 2025. Brazil leads through Stellantis Brazil, Volkswagen do Brasil, and General Motors Brazil operations under MERCOSUR vehicle regulation harmonization.

Country Analysis

United States

The vehicle cybersecurity market in the United States was valued at approximately USD 985 Million in 2025 and is projected to grow at a CAGR of 16.4% during 2025-2034. NHTSA cybersecurity best practices guidance for connected vehicles applies across federal motor vehicle safety standards. Federal Trade Commission and state attorney general enforcement covers connected vehicle data privacy under California Consumer Privacy Act (CCPA) and Colorado Privacy Act. Major U.S. OEMs include Ford, General Motors, Stellantis, and Tesla; cybersecurity vendor concentration includes Cadence Design Systems (San Jose, post-Secure-IC), Synopsys (Sunnyvale), Harman International (Stamford), Karamba Security (U.S. operations), GuardKnox (U.S. operations), and RunSafe Security. Auto-ISAC operates from the Automotive Information Sharing and Analysis Center supporting 30+ OEM and supplier members. The Department of Transportation Volpe Center coordinates federal connected vehicle research.

Germany

Germany's vehicle cybersecurity market reached approximately USD 685 Million in 2025 with a country CAGR of 13.6% during 2025-2034, representing the largest European national market by value. The Kraftfahrt-Bundesamt (KBA) administers UN R155 type approval following mandatory enforcement from July 2024. Continental AG (Hanover) anchors domestic activity through its Elektrobit subsidiary and PlaxidityX (rebranded August 2024 from Argus Cyber Security). Robert Bosch GmbH (Stuttgart) operates ETAS and ESCRYPT cybersecurity divisions. Volkswagen Group (Wolfsburg), Mercedes-Benz Group (Stuttgart), BMW Group (Munich), Porsche, and Audi anchor OEM demand. Vector Informatik (Stuttgart) supplies AUTOSAR-aligned cybersecurity tooling. The German Federal Office for Information Security (BSI) coordinates national cybersecurity guidance complementing UN R155 obligations.

China

China's vehicle cybersecurity market reached approximately USD 920 Million in 2025 with a country CAGR of 17.4% during 2025-2034, anchored by the world's largest connected and electric vehicle production volume. The Ministry of Industry and Information Technology (MIIT) administers GB standards including GB/T 40861-2021 (Cybersecurity General Technical Requirements for Vehicles), GB 44495-2024 (Technical Requirements for Vehicle Cybersecurity), and GB 44496-2024 (Technical Requirements for Software Updates). Domestic OEMs include BYD, NIO, Li Auto, XPeng, Geely, Great Wall Motors, SAIC, BAIC, and Chery. CATL anchors battery management system cybersecurity. The Cyberspace Administration of China (CAC) coordinates cross-border data transfer rules affecting connected vehicle telemetry. Tencent and Huawei provide automotive operating system security alongside emerging domestic vendors.

Japan

Japan's vehicle cybersecurity market reached approximately USD 425 Million in 2025 with a country CAGR of 14.2% during 2025-2034. Japan adopted UN R155 with Ministry of Land, Infrastructure, Transport and Tourism (MLIT) administering type approval. Toyota, Honda, Nissan, Mazda, Subaru, Mitsubishi Motors, and Suzuki anchor OEM demand. Tier 1 suppliers Denso, Aisin, and Panasonic Automotive Systems anchor supply with VicOne (Trend Micro Tokyo subsidiary) providing xCarbon vehicle cyber detection following expanded August 2025 partnership. Japanese automakers integrate cybersecurity into the vehicle lifecycle following UN R155 and ISO/SAE 21434 standards with focus on risk management, supply chain security, and incident response. The Information-technology Promotion Agency (IPA) coordinates national cybersecurity guidance.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Security Domain

- In-Vehicle Network Security

- Application Security

- Endpoint Security

- Cloud Security

- Wireless Communication Security

- Over-the-Air (OTA) Update Security

- Identity and Access Management (IAM)

- Data Encryption and Privacy Protection

- Others

By Solution Type

- Hardware Security Solutions

- Software Security Solutions

- Cybersecurity Services

- Intrusion Detection and Prevention Systems (IDPS)

- Security Information and Event Management (SIEM)

- Threat Intelligence and Monitoring Solutions

- Security Testing and Validation

- Risk Assessment and Compliance Solutions

- Others

By Vehicle Type

- Passenger Vehicles

- Light Commercial Vehicles (LCVs)

- Heavy Commercial Vehicles (HCVs)

- Electric Vehicles (EVs)

- Hybrid Vehicles

- Autonomous Vehicles

- Connected Vehicles

- Off-Highway Vehicles

- Others

By End-User

- Automotive Original Equipment Manufacturers (OEMs)

- Automotive Suppliers and Tier-1 Vendors

- Fleet Operators

- Mobility Service Providers

- Government and Defense Organizations

- Automotive Cybersecurity Solution Providers

- Aftermarket Service Providers

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 5.45 B |

| Forecast Revenue (2034) | USD 18.85 B |

| CAGR (2025-2034) | 14.8% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Security Domain, (In-Vehicle Network Security, Application Security, Endpoint Security, Cloud Security, Wireless Communication Security, Over-the-Air (OTA) Update Security, Identity and Access Management (IAM), Data Encryption and Privacy Protection, Others), By Solution Type, (Hardware Security Solutions, Software Security Solutions, Cybersecurity Services, Intrusion Detection and Prevention Systems (IDPS), Security Information and Event Management (SIEM), Threat Intelligence and Monitoring Solutions, Security Testing and Validation, Risk Assessment and Compliance Solutions, Others), By Vehicle Type, (Passenger Vehicles, Light Commercial Vehicles (LCVs), Heavy Commercial Vehicles (HCVs), Electric Vehicles (EVs), Hybrid Vehicles, Autonomous Vehicles, Connected Vehicles, Off-Highway Vehicles, Others), By End-User, (Automotive Original Equipment Manufacturers (OEMs), Automotive Suppliers and Tier-1 Vendors, Fleet Operators, Mobility Service Providers, Government and Defense Organizations, Automotive Cybersecurity Solution Providers, Aftermarket Service Providers, Others), |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | CONTINENTAL AG (ELEKTROBIT, PLAXIDITYX), NXP SEMICONDUCTORS N.V., UPSTREAM SECURITY, HARMAN INTERNATIONAL (SAMSUNG), ROBERT BOSCH GMBH (ETAS, ESCRYPT), CADENCE DESIGN SYSTEMS, VICONE (TREND MICRO), SYNOPSYS INC., AUTOCRYPT, KARAMBA SECURITY, GUARDKNOX CYBER-TECHNOLOGIES, C2A SECURITY, RUNSAFE SECURITY, BLACKBERRY QNX, CISCO SYSTEMS, INC., INFINEON TECHNOLOGIES AG, STMICROELECTRONICS, RENESAS ELECTRONICS, VECTOR INFORMATIK GMBH, HONEYWELL INTERNATIONAL INC., BROADCOM INC., DENSO CORPORATION, PANASONIC AUTOMOTIVE SYSTEMS, AURORA LABS, APPLIED INTUITION, ARM LIMITED, ARILOU TECHNOLOGIES, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Solution Type (Embedded Security Software, Hardware Security Modules, VSOC Cloud Platforms, Cybersecurity Engineering Services), By Vehicle Type (Passenger, LCVs, HCVs, Electric & Hybrid Vehicles), By End-User (OEMs, Tier-1 Suppliers, Fleet Operators) Region & Key Players-Dynamics, Strategies & Forecast 2026-2034")

, By Solution Type (Embedded Security Software, Hardware Security Modules, VSOC Cloud Platforms, Cybersecurity Engineering Services), By Vehicle Type (Passenger, LCVs, HCVs, Electric & Hybrid Vehicles), By End-User (OEMs, Tier-1 Suppliers, Fleet Operators) Region & Key Players-Dynamics, Strategies & Forecast 2026-2034")

, By Solution Type (Embedded Security Software, Hardware Security Modules, VSOC Cloud Platforms, Cybersecurity Engineering Services), By Vehicle Type (Passenger, LCVs, HCVs, Electric & Hybrid Vehicles), By End-User (OEMs, Tier-1 Suppliers, Fleet Operators) Region & Key Players-Dynamics, Strategies & Forecast 2026-2034")

Frequently Asked Questions

How big is the Vehicle Cybersecurity Market?

The Global Vehicle Cybersecurity Market was valued at USD 4.85 Billion in 2024 and USD 5.45 Billion in 2025, and is projected to reach USD 18.85 Billion by 2034, growing at a CAGR of 14.8% from 2026 to 2034. Market growth is driven by connected vehicles, automotive cybersecurity, AI-powered threat detection, and secure OTA updates.

Who are the major players in the Vehicle Cybersecurity Market?

CONTINENTAL AG (ELEKTROBIT, PLAXIDITYX), NXP SEMICONDUCTORS N.V., UPSTREAM SECURITY, HARMAN INTERNATIONAL (SAMSUNG), ROBERT BOSCH GMBH (ETAS, ESCRYPT), CADENCE DESIGN SYSTEMS, VICONE (TREND MICRO), SYNOPSYS INC., AUTOCRYPT, KARAMBA SECURITY, GUARDKNOX CYBER-TECHNOLOGIES, C2A SECURITY, RUNSAFE SECURITY, BLACKBERRY QNX, CISCO SYSTEMS, INC., INFINEON TECHNOLOGIES AG, STMICROELECTRONICS, RENESAS ELECTRONICS, VECTOR INFORMATIK GMBH, HONEYWELL INTERNATIONAL INC., BROADCOM INC., DENSO CORPORATION, PANASONIC AUTOMOTIVE SYSTEMS, AURORA LABS, APPLIED INTUITION, ARM LIMITED, ARILOU TECHNOLOGIES, Others

Which segments covered the Vehicle Cybersecurity Market?

By Security Domain, (In-Vehicle Network Security, Application Security, Endpoint Security, Cloud Security, Wireless Communication Security, Over-the-Air (OTA) Update Security, Identity and Access Management (IAM), Data Encryption and Privacy Protection, Others), By Solution Type, (Hardware Security Solutions, Software Security Solutions, Cybersecurity Services, Intrusion Detection and Prevention Systems (IDPS), Security Information and Event Management (SIEM), Threat Intelligence and Monitoring Solutions, Security Testing and Validation, Risk Assessment and Compliance Solutions, Others), By Vehicle Type, (Passenger Vehicles, Light Commercial Vehicles (LCVs), Heavy Commercial Vehicles (HCVs), Electric Vehicles (EVs), Hybrid Vehicles, Autonomous Vehicles, Connected Vehicles, Off-Highway Vehicles, Others), By End-User, (Automotive Original Equipment Manufacturers (OEMs), Automotive Suppliers and Tier-1 Vendors, Fleet Operators, Mobility Service Providers, Government and Defense Organizations, Automotive Cybersecurity Solution Providers, Aftermarket Service Providers, Others),

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Vehicle Cybersecurity Market

Published Date : 01 Jul 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date