- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Vehicle-to-Grid Technology Market Size, Share | CAGR 19.4%

Global Vehicle-to-Grid Technology Market Size, Share, Growth Analysis By Component (Hardware, Software, Services), By End-User (Commercial & Industrial, Residential, Utility), By Charging Standard (CCS, CHAdeMO, OEM Proprietary Protocols), Smart Grid Integration Trends, Bidirectional EV Charging Innovations & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

| USD 5.84 Billion | USD 28.97 Billion | 19.4% | North America, 38.2% |

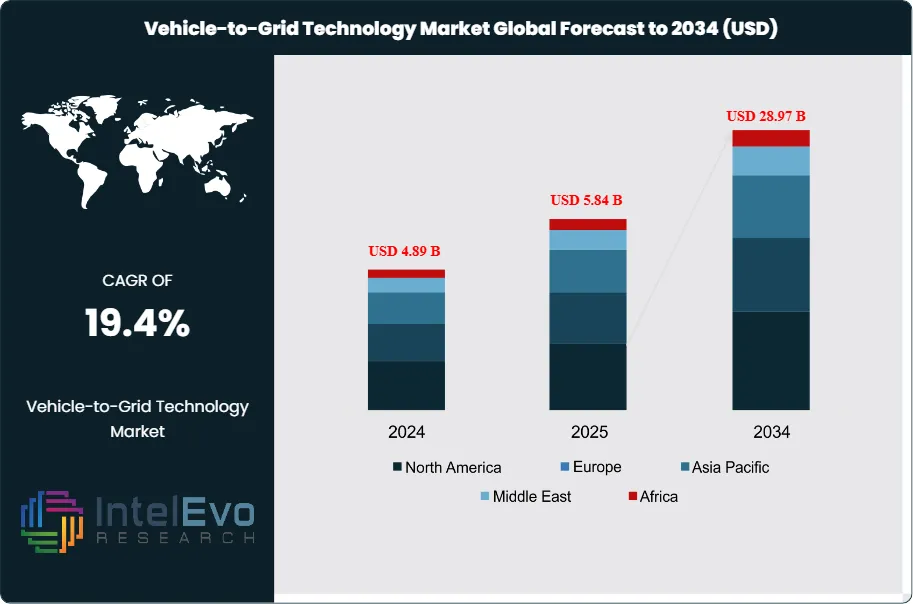

The Vehicle-to-Grid Technology Market was valued at approximately USD 4.89 Billion in 2024 and reached USD 5.84 Billion in 2025. The market is projected to grow to USD 28.97 Billion by 2034, expanding at a CAGR of 19.4% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 23.13 Billion over the analysis period, establishing Vehicle-to-Grid Technology as one of the fastest-expanding segments within the broader energy transition and smart grid infrastructure domain.

Get More Information about this report -

Request Free Sample ReportVehicle-to-Grid Technology enables bidirectional power flow between electric vehicles and the electrical grid, allowing EVs to discharge stored energy back to grid operators, utilities, or building systems during peak demand periods. The fundamental value proposition rests on three pillars: grid stabilization through distributed storage, revenue generation for EV owners through demand-response programs, and accelerated decarbonization of electricity systems. As battery capacity per vehicle continues to rise, the aggregate dispatchable storage represented by connected EV fleets has grown into a strategically material resource for grid operators worldwide.

Market growth is primarily driven by the convergence of rapid EV adoption and deteriorating grid reliability in key markets. The U.S. Energy Information Administration reported that grid disturbances and weather-related outages cost the U.S. economy an estimated USD 150 billion annually, creating acute utility demand for flexible distributed storage assets. The International Energy Agency projected that by 2025, the global EV fleet surpassed 40 million units, providing a theoretical storage capacity exceeding 2,000 GWh. Vehicle-to-Grid Technology systems capture a growing fraction of this latent capacity through aggregation platforms and managed charging protocols.

Regulatory catalysts are accelerating commercial deployment. The European Union's revised Energy Performance of Buildings Directive mandates smart charging readiness in new construction, while the U.S. Federal Energy Regulatory Commission's Order 2222 opened wholesale electricity markets to aggregated distributed energy resources including EV fleets. Japan's Ministry of Economy, Trade and Industry has designated Vehicle-to-Grid Technology as a priority technology under its Green Growth Strategy, committing JPY 500 billion in grid modernization funding through 2030. These policy frameworks have translated directly into utility procurement programs and OEM V2G integration roadmaps.

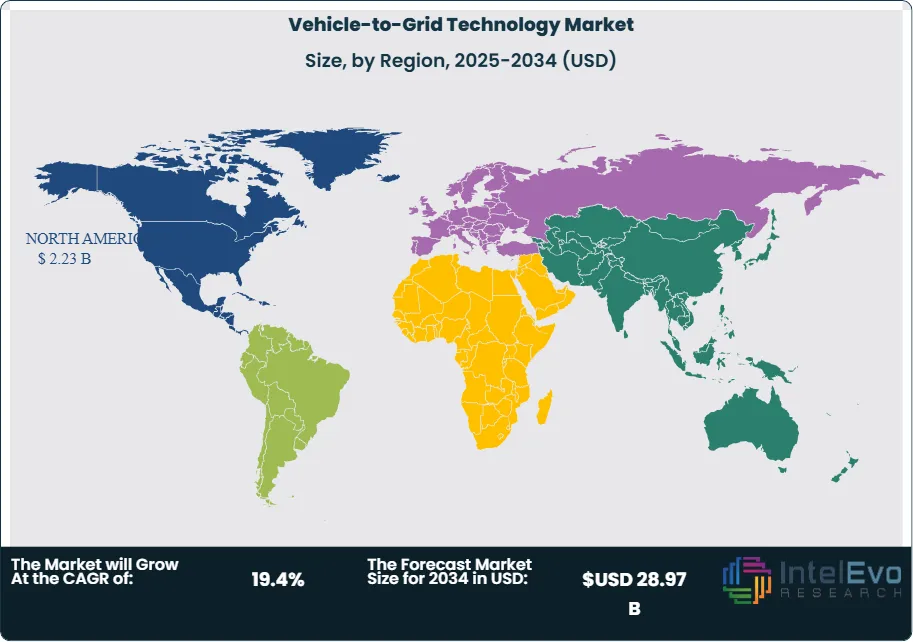

North America accounts for the largest regional share at 38.2% of global revenue in 2025, supported by aggressive state-level EV mandates, strong utility participation in demand-response markets, and the presence of technology pioneers. Asia Pacific follows at 31.5%, driven by Japan's leading V2G demonstration projects and China's state-directed smart grid investment. Competitive intensity is rising as automotive OEMs, energy management software firms, and grid infrastructure providers converge on the Vehicle-to-Grid Technology space, with partnership activity between EV manufacturers and utilities accelerating sharply since 2024.

, By End-User (Commercial & Industrial, Residential, Utility), By Charging Standard (CCS, CHAdeMO, OEM Proprietary Protocols), Smart Grid Integration Trends, Bidirectional EV Charging Innovations & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global Vehicle-to-Grid Technology market reached USD 5.84 Billion in 2025 and is forecast to reach USD 28.97 Billion by 2034, expanding at a CAGR of 19.4% over the 2026–2034 forecast period.

- Segment Dominance: The Hardware segment, comprising bidirectional chargers and inverter systems, held the largest share at 42.3% of global revenue in 2025, reflecting continued infrastructure buildout ahead of software-layer monetization.

- Segment Dominance: The Commercial and Industrial end-user segment led application demand with a 38.7% share in 2025, as fleet operators and C&I energy buyers generated superior economics from peak-demand arbitrage versus residential users.

- Driver: Surging EV adoption combined with grid reliability mandates is the primary growth driver; EV registrations exceeded 14 million units globally in 2024, expanding the addressable V2G-capable fleet by approximately 31% year-over-year.

- Restraint: Interoperability fragmentation across charging standards, including CCS, CHAdeMO, and proprietary OEM protocols, constrains aggregation platform scalability and raises integration costs by an estimated 18–22% versus fully standardized deployments.

- Opportunity: V2G-enabled behind-the-meter storage for commercial real estate and microgrids represents an addressable opportunity of approximately USD 8.4 Billion by 2034, driven by corporate sustainability mandates and rising commercial electricity tariffs.

- Trend: AI-driven fleet aggregation and predictive dispatch is the dominant 2025 trend, with machine learning models reducing dispatch latency below 200 milliseconds and improving energy yield per session by 12–15% versus static scheduling algorithms.

- Regional Analysis: North America leads the global Vehicle-to-Grid Technology market with a 38.2% share in 2025, representing approximately USD 2.23 Billion, supported by FERC Order 2222 market access and strong utility demand-response program participation.

Competitive Landscape Overview

The global Vehicle-to-Grid Technology market is moderately consolidated at the platform layer but fragmented at hardware manufacturing. The top four players, Nuvve Corporation, Volkswagen Group (through Elli and its V2G ecosystem), Nissan Motor (through the Leaf V2G program and Enel X partnership), and Honda Motor (V2G-enabled Clarity and Prologue platforms), collectively hold approximately 31.4% of global market revenue in 2025. Competition is primarily technology-driven at the software aggregation layer, where proprietary dispatch algorithms, grid operator integrations, and OEM API partnerships create durable differentiation. Hardware competition at the bidirectional charger level is intensifying, with Asian manufacturers compressing margins. M&A activity accelerated in 2024–2025 as utilities acquired aggregation software firms to internalize V2G dispatch capabilities.

Competitive Landscape Matrix

| Company | HQ Country | Market Position | Key Product / Platform | Geographic Strength | Recent Strategic Move (2024–2026) |

| Nuvve Corporation | USA | Leader | Nuvve V2G Platform | North America | Expanded utility partnership program to 14 U.S. states; signed multi-year fleet V2G agreement with San Diego MTS (Jan 2025). |

| Volkswagen Group (Elli) | Germany | Leader | Elli bidirectional charging system | Europe | Launched V2G-enabled ID.7 wagons with grid export capability across 5 EU markets (Mar 2025). |

| Nissan / Enel X | Japan / Italy | Leader | CHAdeMO V2G solution | Asia Pacific / Europe | Extended Nissan Leaf V2G scheme to UK National Grid, targeting 10,000 enrolled vehicles by Q3 2025. |

| Honda Motor | Japan | Leader | Honda Power Manager V2G | Asia Pacific / North America | Launched V2G integration with Tokyo Electric Power Co., reaching 3,200 enrolled Prologue units (Feb 2026). |

| Fermata Energy | USA | Challenger | FE-20 bidirectional EVSE | North America | Secured USD 30M Series B to expand commercial fleet V2G deployments across Sun Belt states (Sep 2025). |

| The Mobility House | Germany | Challenger | ChargePilot platform | Europe | Partnered with E.ON Drive Infrastructure to deploy 5,000 V2G-capable charging points in Germany (Dec 2024). |

| Kaluza (OVO Energy) | UK | Challenger | Kaluza EV Platform | Europe | Won UK Flexibility Innovation Programme contract to aggregate 50,000 EVs for National Grid ESO (Jun 2025). |

| SAFT (TotalEnergies) | France | Niche Player | SAFTDrive V2G module | Europe / MEA | Integrated V2G module into TotalEnergies fleet electrification contracts across France and UAE (Jan 2026). |

| Centrica | UK | Niche Player | Centrica V2G tariff scheme | Europe | Launched residential V2G tariff in partnership with Octopus Energy covering 4,000 UK households (Apr 2025). |

By Component:

The Vehicle-to-Grid Technology hardware segment, encompassing bidirectional chargers, inverters, and power conversion units, commanded the largest share of the market in 2025 at 42.3% of global revenue, equivalent to approximately USD 2.47 Billion. This dominance reflects the capital-intensive infrastructure phase of V2G deployment, where utilities and fleet operators are installing bidirectional EVSE (Electric Vehicle Supply Equipment) at scale ahead of full software-layer monetization. Bidirectional level-2 chargers priced between USD 2,000 and USD 8,000 per unit represent the highest-volume hardware sub-category. DC fast chargers with V2G capability, priced at USD 25,000–USD 80,000, serve commercial fleet depots and represent the highest per-unit revenue segment. Leading hardware manufacturers include ABB, BTC Power, Fermata Energy, and Wallbox, which collectively are expanding production capacity in anticipation of OEM mandates requiring V2G-capable onboard chargers by 2027–2028 in key markets.

The software segment held a 33.8% share in 2025, valued at approximately USD 1.97 Billion, and is forecast to grow at the fastest rate within the component breakdown, driven by the shift toward aggregation-as-a-service models. Energy management systems (EMS), fleet dispatch platforms, and vehicle-grid integration middleware are the principal software sub-categories. Aggregation platforms that bundle V2G dispatch with demand-response market participation command premium pricing, with annual software-as-a-service contracts ranging from USD 50,000 for mid-sized fleets to USD 2 million-plus for large utility programs. Services accounted for the remaining 23.9% share in 2025, covering grid integration consulting, regulatory compliance support, and ongoing monitoring and maintenance contracts.

By End-User:

The commercial and industrial end-user segment represented 38.7% of the global Vehicle-to-Grid Technology market in 2025, approximately USD 2.26 Billion, driven by the superior unit economics of V2G arbitrage at the C&I scale. Fleet operators deploying 50-plus electric vehicles at a single depot can generate USD 3,000–USD 8,000 per vehicle per year through peak-demand charge reduction, demand-response revenue, and grid services capacity payments. School bus electrification programs in the United States, notably in California and New York, have become high-profile V2G deployments, with the California Energy Commission funding 1,500 V2G-capable school buses through its Clean Transportation Program. Logistics and delivery operators, including Amazon's electric delivery van fleet, have evaluated V2G integration for depot-level grid services.

Residential end-users accounted for 29.4% of global market revenue in 2025. The residential segment is characterized by higher customer acquisition costs and lower per-unit dispatch revenue than the C&I segment, but benefits from government incentive programs and growing consumer interest in energy bill reduction. Virtual power plant (VPP) models aggregating thousands of residential EVs have demonstrated meaningful grid value; Pacific Gas and Electric's VPP program in California enrolled over 18,000 participants in 2024. The utility segment at 31.9% encompasses direct utility procurement of V2G aggregation services, grid stabilization contracts, and frequency regulation service agreements. Utilities in markets with high renewable penetration are the most active V2G buyers, as intermittency from solar and wind creates acute demand for fast-response dispatchable storage.

By Charging Standard:

The Combined Charging System (CCS) standard held a 47.2% share of V2G deployments in 2025, reflecting its dominance among European and North American OEMs. CCS Combo 2 with V2G capability is now incorporated into platforms from Volkswagen, BMW, Ford, and General Motors, giving the standard a strong growth trajectory through 2034 as these OEMs scale EV production. CHAdeMO, the standard historically championed by Nissan and Mitsubishi, accounted for 28.6% of V2G deployments in 2025. CHAdeMO has the longest commercial V2G track record, with Japan's Nissan Leaf program demonstrating grid export since 2013. However, CHAdeMO's share is declining as European and North American OEMs standardize on CCS and, increasingly, on NACS (North American Charging Standard). OEM proprietary protocols accounted for the remaining 24.2%, primarily reflecting Tesla's proprietary charging architecture and other vertically integrated systems.

Regional Analysis

North America

North America held the dominant regional share of the global Vehicle-to-Grid Technology market at 38.2% in 2025, representing approximately USD 2.23 Billion in revenue. The United States is the primary market driver, accounting for roughly 85% of regional V2G revenue, supported by FERC Order 2222's mandate to open wholesale electricity markets to distributed energy resource aggregators including EV fleets. California leads U.S. V2G deployment, with the California Public Utilities Commission having approved V2G export tariffs for all three investor-owned utilities. The California Energy Commission allocated USD 1.5 Billion in grid modernization funding in 2024 that includes V2G infrastructure components. New York's Con Edison has operated pilot V2G programs with school bus fleets since 2022, and the state's Climate Leadership and Community Protection Act creates additional regulatory tailwinds. Canada is emerging as a secondary North American market, with British Columbia and Ontario utilities initiating V2G pilot procurements in 2024–2025. Mexico's grid modernization program under CENACE includes demand-response provisions compatible with V2G aggregation, though regulatory clarity for export tariffs remains pending.

Europe

Europe represented 26.4% of the global Vehicle-to-Grid Technology market in 2025, approximately USD 1.54 Billion, positioning it as the second-largest regional market. Germany is Europe's largest V2G market by absolute value, reflecting its combination of high EV penetration, a liberalized electricity market, and Volkswagen Group's strategic commitment to V2G integration across its OEM brands. The UK is the second-largest European market, with Ofgem's flexibility policy framework and National Grid ESO's Enhanced Frequency Response program creating commercial pathways for V2G aggregators. Octopus Energy's Intelligent Octopus Go tariff has enrolled over 100,000 EV drivers in smart charging programs, providing a foundation for V2G expansion. The Netherlands has operated commercial V2G schemes since 2019, and the Dutch government targets 1 million V2G-capable vehicles by 2030. The EU's revised Renewable Energy Directive and Clean Energy Package explicitly recognize V2G as a key flexibility mechanism, ensuring continued regulatory support. Nordic markets, particularly Denmark and Norway with high EV penetration rates exceeding 25% of new car sales, represent high-growth subregions.

Asia Pacific

Asia Pacific accounted for 31.5% of global Vehicle-to-Grid Technology revenue in 2025, approximately USD 1.84 Billion, and is the fastest-growing regional market on an absolute dollar basis. Japan is the regional pioneer, having hosted the world's first commercial V2G projects using the Nissan Leaf and CHAdeMO protocol from 2013 onward. Japan's Agency for Natural Resources and Energy has backed V2G demonstration projects involving over 4,000 vehicles as of 2025. China represents the largest Asia Pacific market by vehicle count and is rapidly building regulatory infrastructure for V2G, with the National Energy Administration publishing V2G technical standards in 2024. China's State Grid Corporation has initiated V2G pilot programs in Shanghai, Guangdong, and Zhejiang provinces involving commercial EV fleets. South Korea's Korea Electric Power Corporation (KEPCO) operates the largest single-utility V2G pilot in the region, covering 2,100 enrolled EVs as of 2025. Australia's high renewable penetration and grid instability are creating commercial urgency for V2G, with several state governments funding V2G trials through the Australian Renewable Energy Agency.

Latin America

Latin America held a 2.4% share of the global Vehicle-to-Grid Technology market in 2025, valued at approximately USD 140 Million. The region's V2G development is nascent, constrained by lower EV penetration rates, grid infrastructure gaps, and limited regulatory frameworks for distributed energy resource monetization. Brazil is the region's largest V2G-adjacent market, with Aneel, the national electricity regulator, initiating consultations on demand-response programs that could accommodate V2G aggregators. Chile, with its high renewable energy penetration and proactive grid modernization program under the Ministry of Energy, is positioned as the most likely early-mover market for commercial V2G deployment. Colombia and Mexico are monitoring international V2G developments but have not yet established tariff structures permitting grid export. The region's longer-term growth trajectory through 2034 will depend on EV adoption acceleration, currently concentrated among premium urban consumers, and on grid operator appetite for flexibility procurement mechanisms.

Middle East & Africa

The Middle East and Africa region represented 1.5% of the global Vehicle-to-Grid Technology market in 2025, approximately USD 88 Million. The UAE is the regional leader, with Abu Dhabi's Department of Energy and Dubai Electricity and Water Authority both having initiated smart grid programs that include V2G readiness requirements for new charging infrastructure. The UAE's Net Zero 2050 Strategic Initiative allocates significant capital toward grid flexibility technologies, and the Abu Dhabi EV infrastructure rollout by TAQA and Masdar includes V2G-compatible hardware specifications. Saudi Arabia's Vision 2030 energy transition framework and NEOM smart city project incorporate V2G as a component of integrated energy management systems for planned car-free urban zones. South Africa's acute grid reliability crisis, including load-shedding events totaling thousands of hours annually, creates economic urgency for distributed backup and grid support technologies, though the formal V2G regulatory pathway remains undeveloped. The region's market will scale primarily from the Gulf Cooperation Council states, where energy subsidies are being restructured and grid modernization investment is substantial.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Component

- Hardware (Bidirectional Chargers, Inverters, Power Conversion Units)

- Software (Energy Management Systems, Aggregation Platforms, Fleet Dispatch Software)

- Services (Grid Integration Consulting, Monitoring & Maintenance, Regulatory Compliance)

By End-User

- Commercial and Industrial

- Residential

- Utility

By Charging Standard

- CCS (Combined Charging System)

- CHAdeMO

- OEM Proprietary Protocols (including NACS)

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 5.84 B |

| Forecast Revenue (2034) | USD 28.97 B |

| CAGR (2025-2034) | 19.4% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Component, (Hardware (Bidirectional Chargers, Inverters, Power Conversion Units), Software (Energy Management Systems, Aggregation Platforms, Fleet Dispatch Software), Services (Grid Integration Consulting, Monitoring & Maintenance, Regulatory Compliance)), By End-User, (Commercial and Industrial, Residential, Utility), By Charging Standard, (CCS (Combined Charging System), CHAdeMO, OEM Proprietary Protocols (including NACS)) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | NUVVE CORPORATION, VOLKSWAGEN GROUP (ELLI), NISSAN MOTOR / ENEL X, HONDA MOTOR, FERMATA ENERGY, THE MOBILITY HOUSE, KALUZA (OVO ENERGY), SAFT (TOTALENERGIES), CENTRICA, OCTOPUS ENERGY, FORD MOTOR COMPANY, GENERAL MOTORS (ULTIUM PLATFORM), WALLBOX CHARGERS, ABB E-MOBILITY, BTC POWER, REVEL TRANSIT, VIRTUAL PEAKER, AUTOGRID (SCHNEIDER ELECTRIC), Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By End-User (Commercial & Industrial, Residential, Utility), By Charging Standard (CCS, CHAdeMO, OEM Proprietary Protocols), Smart Grid Integration Trends, Bidirectional EV Charging Innovations & Forecast 2026-2034")

, By End-User (Commercial & Industrial, Residential, Utility), By Charging Standard (CCS, CHAdeMO, OEM Proprietary Protocols), Smart Grid Integration Trends, Bidirectional EV Charging Innovations & Forecast 2026-2034")

, By End-User (Commercial & Industrial, Residential, Utility), By Charging Standard (CCS, CHAdeMO, OEM Proprietary Protocols), Smart Grid Integration Trends, Bidirectional EV Charging Innovations & Forecast 2026-2034")

Frequently Asked Questions

How big is the Vehicle-to-Grid Technology Market?

The Global Vehicle-to-Grid Technology Market was valued at USD 4.89 Billion in 2024 and is projected to reach USD 28.97 Billion by 2034, growing at a CAGR of 19.4% from 2026 to 2034, driven by rising electric vehicle adoption, increasing investments in smart grid infrastructure, growing demand for bidirectional charging technologies, and expanding renewable energy integration across residential, commercial, and utility-scale applications worldwide.

Who are the major players in the Vehicle-to-Grid Technology Market?

NUVVE CORPORATION, VOLKSWAGEN GROUP (ELLI), NISSAN MOTOR / ENEL X, HONDA MOTOR, FERMATA ENERGY, THE MOBILITY HOUSE, KALUZA (OVO ENERGY), SAFT (TOTALENERGIES), CENTRICA, OCTOPUS ENERGY, FORD MOTOR COMPANY, GENERAL MOTORS (ULTIUM PLATFORM), WALLBOX CHARGERS, ABB E-MOBILITY, BTC POWER, REVEL TRANSIT, VIRTUAL PEAKER, AUTOGRID (SCHNEIDER ELECTRIC), Others

Which segments covered the Vehicle-to-Grid Technology Market?

By Component, (Hardware (Bidirectional Chargers, Inverters, Power Conversion Units), Software (Energy Management Systems, Aggregation Platforms, Fleet Dispatch Software), Services (Grid Integration Consulting, Monitoring & Maintenance, Regulatory Compliance)), By End-User, (Commercial and Industrial, Residential, Utility), By Charging Standard, (CCS (Combined Charging System), CHAdeMO, OEM Proprietary Protocols (including NACS))

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Vehicle-to-Grid Technology Market

Published Date : 22 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date