- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Vertical AI solutions Market Size & Forecast 2034 | CAGR 20.4%

Global Vertical AI Solutions Market Size, Share, Growth & Industry Analysis By Offering (Platform/Software, Services), By Vertical (Healthcare & Life Sciences, Financial Services, Legal Technology, Logistics & Supply Chain, Insurance & Claims Processing, Agriculture & Food, Others), By Deployment (Cloud, On-Premise, Hybrid), By Enterprise Size (Large Enterprises, SMEs) Industry Trends, Competitive Landscape, Market Dynamics, Regional Insights & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2025–2034) | Largest Region (2025) |

| USD 5.4 Billion | USD 28.9 Billion | 20.4% | North America, 42.6% |

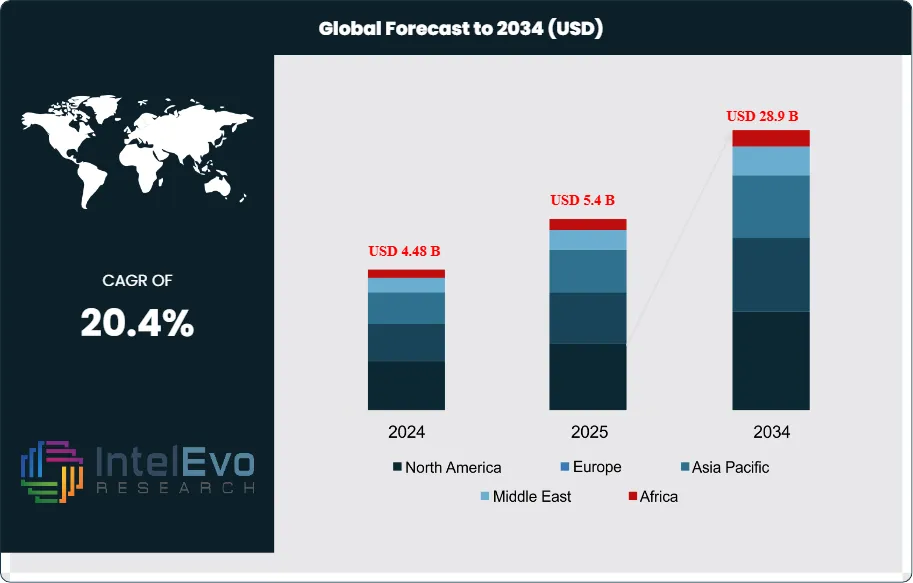

The Vertical AI Solutions Market was valued at about USD 4.48 billion in 2024 and grew to USD 5.4 billion in 2025. The market is expected to reach USD 28.9 billion by 2034, with a growth rate of 20.4% from 2026 to 2034. This represents an absolute dollar opportunity of USD 23.5 Billion over the analysis period. Vertical AI refers to artificial intelligence platforms purpose-built for a single industry, trained on domain-specific data, and designed to execute workflows native to that sector. Unlike horizontal AI tools that serve general functions such as text generation or image recognition, vertical AI solutions embed regulatory logic, industry taxonomy, and proprietary datasets into the model architecture itself; making them compliant, accurate, and immediately deployable within sectors such as healthcare, financial services, legal, logistics, insurance, and agriculture.

Get More Information about this report -

Request Free Sample ReportThe vertical AI solutions market is accelerating because enterprise buyers increasingly reject one-size-fits-all AI products that require months of customization to meet industry-specific compliance, data formatting, and workflow requirements. In healthcare alone, vertical AI platforms processed clinical decision support for 32% of U.S. hospital systems in 2025, up from 14% in 2022. Financial services firms allocated an average of USD 18 Million each to vertical AI procurement in 2025, targeting fraud detection, credit underwriting, and regulatory reporting. The EU AI Act, which classifies healthcare and financial AI as high-risk, has created a compliance moat around vertical AI vendors that pre-embed audit trails, explainability modules, and bias monitoring into their platforms. The NIST AI Risk Management Framework in the United States similarly rewards vertical AI providers that demonstrate domain-calibrated risk controls.

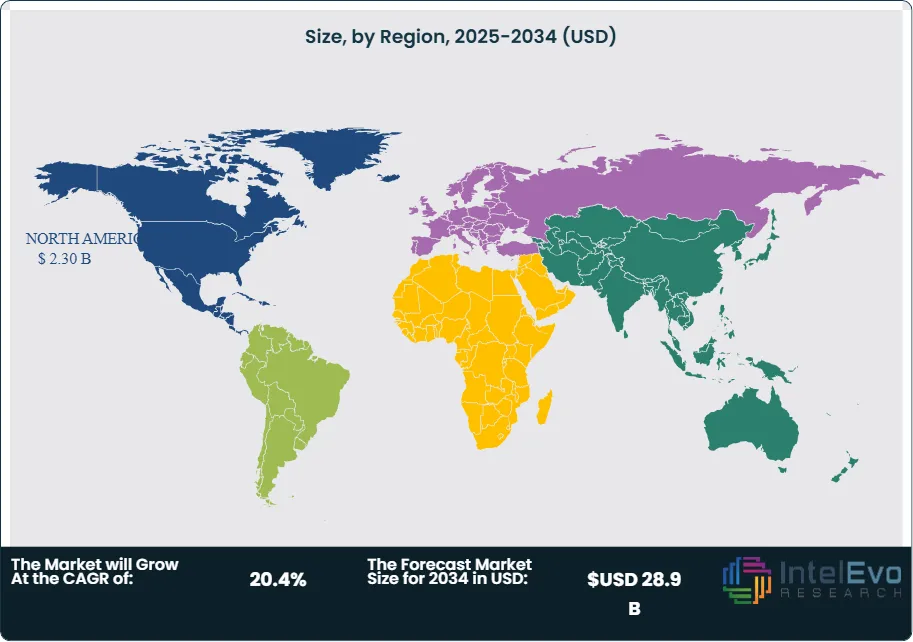

North America led the vertical AI solutions market with a 42.6% share in 2025, driven by venture capital deployment exceeding USD 4.2 Billion into vertical AI startups between 2023 and 2025. Europe held 26.8%, where GDPR and the EU AI Act accelerate demand for sector-compliant AI tools. Asia Pacific captured 20.1%, with China, India, and Japan investing heavily in agricultural AI, manufacturing AI, and fintech AI. The supply side remains fragmented; over 1,400 vertical AI startups operated globally in 2025, though the top 15 vendors accounted for 38% of total revenue. The shift from proof-of-concept to production deployment drove average contract values up 42% year over year in 2025, signaling a maturing market with growing enterprise commitment.

, By Vertical (Healthcare & Life Sciences, Financial Services, Legal Technology, Logistics & Supply Chain, Insurance & Claims Processing, Agriculture & Food, Others), By Deployment (Cloud, On-Premise, Hybrid), By Enterprise Size (Large Enterprises, SMEs) Industry Trends, Competitive Landscape, Market Dynamics, Regional Insights & Forecast 2026–2034")

Key Takeaways

- Market Growth: The vertical AI solutions market was valued at USD 5.4 Billion in 2025 and is projected to reach USD 28.9 Billion by 2034, expanding at a CAGR of 20.4% over the 2025–2034 forecast period.

- Segment Dominance (By Offering): The platform/software segment led with a 64.8% share in 2025, generating USD 3.50 Billion as enterprises prioritized self-service AI tools over consulting-heavy implementations.

- Segment Dominance (By Vertical): Healthcare and life sciences captured the largest vertical share at 27.4% in 2025, valued at USD 1.48 Billion, driven by clinical decision support, genomic AI, and drug discovery platforms.

- Driver: Regulatory mandates including the EU AI Act and NIST AI Framework created a compliance advantage for vertical AI vendors, increasing enterprise procurement of domain-specific platforms by 47% year over year in 2025.

- Restraint: Data fragmentation and interoperability gaps across legacy systems raise integration costs by 25–40%, limiting adoption among mid-market enterprises with annual IT budgets below USD 5 Million.

- Opportunity: Agricultural AI and food supply chain intelligence represent a USD 3.8 Billion addressable opportunity by 2034, with fewer than 8% of global farms using AI-driven precision tools in 2025.

- Trend: Foundation model fine-tuning for vertical use cases reached 56% adoption among vertical AI vendors in 2025, up from 21% in 2023, as vendors build domain-specific large language models on top of base architectures from OpenAI, Anthropic, and Google.

- Regional Analysis: North America dominated with a 42.6% share and USD 2.30 Billion in revenue in 2025, anchored by healthcare AI, legal AI, and fintech AI adoption across Fortune 500 enterprises.

Competitive Landscape Overview

The vertical AI solutions market is highly fragmented, with the top four players; Veeva Systems, Palantir Technologies, Tempus AI, and Toast; commanding a combined 26.3% market share in 2025. Competition is platform-driven, centered on depth of domain data, regulatory compliance features, and integration speed with industry-standard workflows. M&A activity surged through 2025; 23 acquisitions exceeding USD 50 Million each occurred as horizontal AI companies and private equity firms acquired vertical specialists. New entrants from the generative AI wave; particularly startups fine-tuning foundation models for legal, insurance, and construction verticals; have intensified competition in segments previously dominated by incumbents.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| Veeva Systems | US | Leader | Veeva Vault Platform (Life Sciences AI) | North America | Launched Veeva CRM Bot with GenAI copilot for pharma sales (Jan 2026) |

| Palantir Technologies | US | Leader | Palantir AIP for Defense & Healthcare | North America | Secured USD 1.2B U.S. Army AI contract extension (Mar 2025) |

| Tempus AI | US | Leader | Tempus ONE Genomic AI Platform | North America | Completed IPO at USD 6.1B valuation; expanded oncology AI to 40% of U.S. academic medical centers (Jun 2025) |

| Toast Inc. | US | Leader | Toast Restaurant AI Suite | North America | Launched AI-driven demand forecasting and labor scheduling module (Sep 2025) |

| nCino | US | Challenger | nCino Banking AI Platform | North America | Acquired DocFox for automated KYC onboarding (Dec 2024) |

| Flatiron Health | US | Challenger | Flatiron Oncology Real-World Data Platform | North America | Expanded real-world evidence AI to 8 new tumor types (Apr 2025) |

| Eigen Technologies | UK | Challenger | Eigen Financial Document AI | Europe | Raised USD 110M Series C for insurance and capital markets expansion (Feb 2025) |

| Tractable | UK | Niche Player | Tractable AI Visual Intelligence (Insurance) | Europe | Deployed auto-claims AI with Tokio Marine across Asia Pacific (Aug 2025) |

| Uniphore | US | Niche Player | Uniphore X-Platform (Contact Center AI) | Asia Pacific | Acquired Red Box for enterprise conversation intelligence (May 2025) |

| Samsara | US | Challenger | Samsara Connected Operations Cloud (Logistics AI) | North America | Surpassed 50,000 enterprise customers; launched AI-based route optimization (Nov 2025) |

By Offering:

The platform/software segment captured 64.8% of the vertical AI solutions market in 2025, generating USD 3.50 Billion. This category encompasses SaaS-delivered AI platforms pre-configured for specific industries, including clinical trial matching engines, insurance claims adjudication systems, legal contract analysis suites, and restaurant operations management tools. Veeva Systems, Tempus AI, and Toast lead this segment with platforms that combine proprietary domain datasets, pre-trained models, and workflow automation modules. Cloud-native delivery now accounts for 78% of platform revenue, enabling rapid deployment cycles averaging 6–8 weeks compared with 6–12 months for custom-built solutions. Enterprise annual recurring revenue (ARR) for vertical AI platforms grew 51% year over year in 2025, reflecting strong retention and expansion dynamics. The platform segment benefits from high switching costs; once an enterprise integrates a vertical AI platform into its core workflow, the average customer lifetime exceeds 5.8 years.

The services segment held 35.2% share, valued at USD 1.90 Billion in 2025. Services include implementation, model customization, data pipeline integration, training, and managed AI operations. Accenture, Deloitte, and McKinsey QuantumBlack have built vertical AI practices targeting financial services, healthcare, and energy clients. Implementation services grew 38% year over year, driven by complex data environment integration requirements in regulated industries. Managed AI-as-a-service models, where vendors operate and continuously retrain vertical AI models on behalf of clients, reached 22% of total services revenue in 2025.

By Vertical:

Healthcare and life sciences led the vertical AI solutions market with a 27.4% share in 2025, valued at USD 1.48 Billion. Clinical decision support systems, genomic analysis platforms, radiology AI, drug discovery engines, and patient matching tools drive this segment. Tempus AI, Flatiron Health, and PathAI lead in oncology AI. The FDA cleared 171 AI/ML-enabled medical devices by the end of 2024, and the pace accelerated in 2025 with vertical AI platforms increasingly targeting real-world evidence generation and clinical trial optimization. Healthcare AI adoption reached 32% of U.S. hospital systems in 2025.

Financial services captured 23.1% share, generating USD 1.25 Billion in 2025. Vertical AI platforms in this sector address fraud detection, credit scoring, anti-money laundering, regulatory reporting, and wealth management advisory. nCino dominates banking workflow AI, while Eigen Technologies leads in document intelligence for capital markets. The sector benefits from stringent compliance requirements under Basel III/IV, PSD2, and Dodd-Frank that favor pre-certified AI solutions over generic tools. Average AI spend per financial institution reached USD 18 Million in 2025.

Legal technology held 13.8% share, valued at USD 0.75 Billion. Contract analysis, litigation prediction, and due diligence automation platforms serve law firms and corporate legal departments. Harvey AI, Luminance, and Ironclad lead this sub-vertical. Logistics and supply chain captured 12.5%, where Samsara and FourKites deploy fleet optimization, demand forecasting, and warehouse AI. Insurance and claims processing held 11.7%, led by Tractable and Shift Technology for visual damage assessment and fraud detection. Agriculture and food accounted for 6.2%, with precision farming AI from companies like Indigo Ag and Taranis. The remaining 5.3% spans construction, real estate, and education verticals.

By Deployment:

Cloud deployment dominated with 71.3% of the vertical AI solutions market in 2025, reflecting the SaaS-first delivery model favored by vertical AI vendors and their enterprise customers. AWS, Microsoft Azure, and Google Cloud each launched industry-specific AI marketplaces between 2024 and 2025, providing pre-configured infrastructure for vertical AI workloads. Cloud delivery reduces time-to-value by 60–70% compared with on-premise installations and supports continuous model retraining with live data feeds. On-premise deployment held 17.2%, concentrated in defense, government, and highly regulated financial institutions where data sovereignty requirements prohibit cloud processing. Hybrid deployment captured 11.5%, serving healthcare organizations that process protected health information locally while sending de-identified data to cloud environments for model training and analytics.

By Enterprise Size:

Large enterprises accounted for 68.4% of the vertical AI solutions market in 2025, spending USD 3.69 Billion. Fortune 500 companies across healthcare, banking, insurance, and logistics drove the majority of vertical AI procurement, with average contract values reaching USD 1.2 Million per year. Large enterprises benefit from dedicated data science teams that can evaluate, deploy, and govern vertical AI platforms internally. Small and medium enterprises held 31.6% share, valued at USD 1.71 Billion. SME adoption accelerated 62% year over year in 2025 as vertical AI vendors introduced usage-based pricing, pre-built integrations with common SME software stacks, and self-service onboarding. Toast’s restaurant AI platform and Samsara’s logistics cloud are among the most successful at penetrating the SME segment.

Regional Analysis

North America Vertical AI Solutions Market:

North America commanded a 42.6% share of the Global Vertical AI Solutions Market in 2025, generating USD 2.30 Billion in revenue. The United States contributed 89% of regional revenue, driven by deep venture capital funding, a mature enterprise software buying culture, and early regulatory clarity from the NIST AI Framework and sector-specific FDA AI guidance. Healthcare AI adoption across U.S. hospital systems reached 32% in 2025. Financial services firms in New York and Charlotte deployed vertical AI for real-time fraud detection and credit decisioning at a rate 2.4 times higher than the global average. Silicon Valley and Boston remain the primary hubs for vertical AI startups, hosting 58% of funded vertical AI companies globally. Canada contributed through healthcare AI initiatives at the Vector Institute and agricultural AI pilots in the Prairie provinces. Mexico’s fintech sector, supported by the 2018 Fintech Law, began adopting vertical AI for lending and remittance workflows.

Europe Vertical AI Solutions Market:

Europe held 26.8% of the vertical AI solutions market in 2025, valued at USD 1.45 Billion. The EU AI Act, fully effective from 2025, classified healthcare AI, financial AI, and legal AI as high-risk applications, creating demand for vertical AI platforms with built-in compliance modules for audit trails, explainability, and bias monitoring. The United Kingdom led the region with 34% of European vertical AI spend, anchored by London’s strength in legal tech AI (Luminance, Eigen Technologies) and insurance AI (Tractable). Germany contributed through manufacturing and industrial AI adoption, with Siemens, Bosch, and SAP integrating vertical AI into factory operations. France’s healthcare AI sector grew 44% in 2025, supported by the Health Data Hub initiative. The Netherlands emerged as a vertical AI hub for agricultural technology, with Wageningen-linked startups deploying precision farming AI across European markets.

Asia Pacific Vertical AI Solutions Market:

Asia Pacific captured 20.1% of market share in 2025, generating USD 1.09 Billion. China led with 41% of regional revenue, driven by agricultural AI deployment across 2.4 million farms and fintech AI powering Alipay, WeChat Pay, and digital lending platforms. Japan’s vertical AI market focused on manufacturing quality inspection, elder care robotics, and supply chain AI, with Preferred Networks and NEC leading domestic deployments. India’s vertical AI adoption centered on fintech (credit scoring for 500+ million unbanked individuals), healthcare diagnostics AI, and agricultural advisory platforms; Niramai and CropIn represent notable Indian vertical AI companies. South Korea invested in semiconductor manufacturing AI and logistics optimization through government-backed programs under the Digital New Deal 2.0. Australia’s mining and agricultural sectors adopted vertical AI platforms for predictive equipment maintenance and crop yield optimization.

Latin America Vertical AI Solutions Market:

Latin America accounted for 5.8% of the Global Vertical AI Solutions Market in 2025, valued at USD 0.31 Billion. Brazil dominated with 52% of regional revenue, propelled by fintech AI adoption at Nubank, Stone, and PagBank, and agritech AI deployment across the Cerrado and Amazon agricultural frontier. The Central Bank of Brazil’s Pix instant payment system generated demand for fraud detection AI tailored to real-time payment flows. Mexico contributed 28% of regional revenue through fintech AI and insurance claims automation. Argentina’s agricultural sector adopted precision farming AI for soybean and corn production, with vertical AI platforms from Kilimo and Auravant gaining traction. Colombia’s healthcare system initiated telemedicine AI pilots in rural areas.

Middle East and Africa Vertical AI Solutions Market:

The Middle East and Africa held 4.7% of market share in 2025, generating USD 0.25 Billion, and represented one of the fastest-growing regions with a projected CAGR of 24.1% through 2034. The UAE’s National AI Strategy 2031 allocates USD 3 Billion to AI adoption across government services, healthcare, and financial sectors, positioning Abu Dhabi and Dubai as vertical AI adoption hubs. Saudi Arabia’s Vision 2030 directed investment toward healthcare AI for hospital operations and oil and gas operational AI. Israel’s vertical AI startups in cybersecurity, agricultural AI, and healthcare AI attracted USD 1.8 Billion in funding between 2023 and 2025. South Africa’s financial services sector deployed vertical AI for mobile banking fraud detection and micro-lending credit assessment. Nigeria’s fintech vertical AI adoption grew 72% in 2025, driven by mobile-first banking platforms serving 45 million digital wallet users.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Offering

- Platform/Software

- Services

By Vertical

- Healthcare and Life Sciences

- Financial Services

- Legal Technology

- Logistics and Supply Chain

- Insurance and Claims Processing

- Agriculture and Food

- Others (Construction, Real Estate, Education)

By Deployment

- Cloud

- On-Premise

- Hybrid

By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 5.4 B |

| Forecast Revenue (2034) | USD 28.9 B |

| CAGR (2025-2034) | 20.4% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Offering , (Platform/Software, Services), By Vertical , (Healthcare and Life Sciences, Financial Services, Legal Technology, Logistics and Supply Chain, Insurance and Claims Processing, Agriculture and Food, Others (Construction, Real Estate, Education)), By Deployment , (Cloud, On-Premise, Hybrid), By Enterprise Size , (Large Enterprises, Small and Medium Enterprises (SMEs)) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | VEEVA SYSTEMS, PALANTIR TECHNOLOGIES, TEMPUS AI, TOAST INC., NCINO, FLATIRON HEALTH (ROCHE), EIGEN TECHNOLOGIES, TRACTABLE, SAMSARA, UNIPHORE, HARVEY AI, LUMINANCE, SHIFT TECHNOLOGY, INDIGO AG, CROPIN, FOURKITES, IRONCLAD, PREFERRED NETWORKS, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Vertical (Healthcare & Life Sciences, Financial Services, Legal Technology, Logistics & Supply Chain, Insurance & Claims Processing, Agriculture & Food, Others), By Deployment (Cloud, On-Premise, Hybrid), By Enterprise Size (Large Enterprises, SMEs) Industry Trends, Competitive Landscape, Market Dynamics, Regional Insights & Forecast 2026–2034")

, By Vertical (Healthcare & Life Sciences, Financial Services, Legal Technology, Logistics & Supply Chain, Insurance & Claims Processing, Agriculture & Food, Others), By Deployment (Cloud, On-Premise, Hybrid), By Enterprise Size (Large Enterprises, SMEs) Industry Trends, Competitive Landscape, Market Dynamics, Regional Insights & Forecast 2026–2034")

, By Vertical (Healthcare & Life Sciences, Financial Services, Legal Technology, Logistics & Supply Chain, Insurance & Claims Processing, Agriculture & Food, Others), By Deployment (Cloud, On-Premise, Hybrid), By Enterprise Size (Large Enterprises, SMEs) Industry Trends, Competitive Landscape, Market Dynamics, Regional Insights & Forecast 2026–2034")

Frequently Asked Questions

How big is the ?

Global Vertical AI solutions market valued at USD 4.48B in 2024, reaching USD 28.9B by 2034, growing at a CAGR of 20.4% from 2026–2034.

Who are the major players in the ?

VEEVA SYSTEMS, PALANTIR TECHNOLOGIES, TEMPUS AI, TOAST INC., NCINO, FLATIRON HEALTH (ROCHE), EIGEN TECHNOLOGIES, TRACTABLE, SAMSARA, UNIPHORE, HARVEY AI, LUMINANCE, SHIFT TECHNOLOGY, INDIGO AG, CROPIN, FOURKITES, IRONCLAD, PREFERRED NETWORKS, Others

Which segments covered the ?

By Offering , (Platform/Software, Services), By Vertical , (Healthcare and Life Sciences, Financial Services, Legal Technology, Logistics and Supply Chain, Insurance and Claims Processing, Agriculture and Food, Others (Construction, Real Estate, Education)), By Deployment , (Cloud, On-Premise, Hybrid), By Enterprise Size , (Large Enterprises, Small and Medium Enterprises (SMEs))

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Vertical AI Solutions Market

Published Date : 31 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date