- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Vertical Farming Technology Market Size & Forecast | CAGR of 19.1%

Global Vertical Farming Technology Market Size, Share, Growth By Component (Hardware, Software, Services), By Growing System (Hydroponics, Aeroponics, Aquaponics), By Application (Fruits, Vegetables, Herbs, Microgreens), By Facility (Building-Based, Shipping Container, Indoor Greenhouses) Region, Key Players – Dynamics, Smart Agriculture & Sustainable Food Production Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

| USD 8.52 Billion | USD 41.00 Billion | 19.1% | North America, 37.5% |

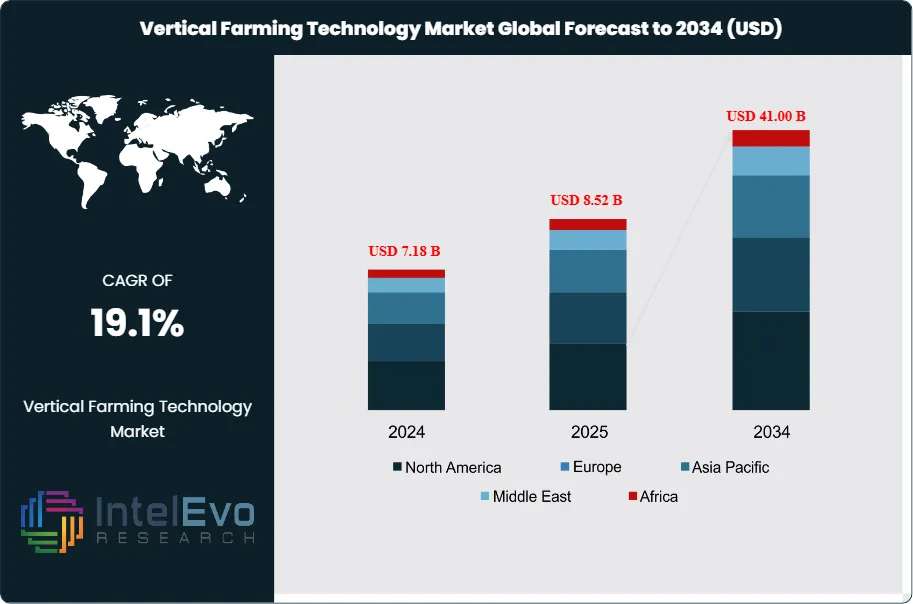

The Vertical Farming Technology Market was valued at USD 7.18 Billion in 2024 and is estimated to reach USD 8.52 Billion in 2025. The market is projected to reach USD 41.00 Billion by 2034, expanding at a CAGR of 19.1% during the forecast period (2026–2034). This represents an absolute dollar opportunity of USD 32.48 Billion over the analysis period.

Get More Information about this report -

Request Free Sample ReportThe vertical farming technology market covers LED grow lighting, hydroponic and aeroponic systems, climate-control equipment, nutrient dosing, robotics, crop analytics, farm-management software, and fully integrated indoor production platforms. Demand is moving away from venture-funded leafy-green scale projects toward facilities that combine premium crops, dense retail distribution, and energy-aware production because electricity and labor now decide unit economics.

Market sizing remains dispersed because publishers define the boundary differently, with 2025 estimates clustered around USD 8.0 Billion to USD 9.6 Billion and 2034 forecasts ranging from near USD 40 Billion to higher outlier cases. This report adopts USD 8.52 Billion for 2025 and USD 41.00 Billion for 2034, reflecting a mid-range technology-led view rather than a food-sales-only view.

The core driver is urban food resilience. USDA Agricultural Research Service described vertical farming in January 2025 as indoor crop production in stacked layers using hydroponics, aquaponics, and other artificial growing systems. Controlled environments reduce dependence on weather, shorten supply chains, and protect high-value crops such as basil, leafy greens, strawberries, microgreens, cannabis, and medicinal plants from field volatility.

Regulation is becoming a screening factor in the vertical farming technology market. USDA UAIP grants support urban production infrastructure, while EU Farm to Fork policy, Singapore Food Agency food-security programs, Gulf food-security targets, and India’s protected-cultivation subsidies support local production. Buyers also evaluate HACCP, GlobalG.A.P., organic certification, food-safety traceability, and energy-efficiency documentation before approving facilities.

Competitive momentum changed sharply in 2025. 80 Acres Farms and Soli Organic combined in August 2025 to build a national indoor farming network with projected first-year revenue approaching USD 200 Million and more than 17,000 U.S. retail locations. By contrast, Plenty’s March 2025 Chapter 11 filing, Bowery Farming’s 2024 shutdown, and Eden Green Technology’s December 2025 Cleburne closure pushed investors toward operators with proven utilization, retail pull-through, and lower capital intensity.

Through 2034, the vertical farming technology market will be shaped by three economics-led shifts. LED vendors such as Signify and Heliospectra will sell adjustable spectrum and power-management tools. Farm operators such as 80 Acres Farms, AeroFarms, Oishii, Gotham Greens, and Planet Farms will focus on crops with pricing power. Automation providers such as Intelligent Growth Solutions, Growcer, and Freight Farms asset acquirers will sell modular systems to institutions that want local supply without building mega-farms.

Market Definition & Scope

The vertical farming technology market is defined as the commercial market for hardware, software, systems integration, and production platforms that enable crops to be grown in vertically stacked, controlled indoor environments. The market includes LED horticulture lighting, HVAC and dehumidification equipment, fertigation, nutrient-film technique systems, aeroponic misting, robotics, sensors, computer vision, AI crop recipes, farm-management software, and modular grow towers.

This analysis includes technology sold to vertical farms, container farms, plant factories, indoor greenhouses, institutional farms, research farms, and commercial operators producing vegetables, herbs, fruits, microgreens, mushrooms, cannabis, and medicinal plants. It excludes open-field precision agriculture, conventional greenhouse structures without vertical stacking, commodity grain farming, broad hydroponic hobby kits, and standalone food retail revenue where the farming technology layer cannot be separated. The vertical farming technology market sits within controlled environment agriculture, which includes greenhouse, indoor, and plant-factory systems.

, By Growing System (Hydroponics, Aeroponics, Aquaponics), By Application (Fruits, Vegetables, Herbs, Microgreens), By Facility (Building-Based, Shipping Container, Indoor Greenhouses) Region, Key Players – Dynamics, Smart Agriculture & Sustainable Food Production Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The vertical farming technology market moves from USD 8.52 Billion in 2025 to USD 41.00 Billion by 2034 at a 19.1% CAGR, creating USD 32.48 Billion in absolute dollar opportunity.

- Segment Dominance: Hydroponic systems led by nutrient-film technique, deep-water culture, and substrate-based recirculation represented 58.0% of technology revenue in 2025, equal to USD 4.94 Billion.

- Segment Dominance: Leafy greens, herbs, and microgreens accounted for 46.5% of crop-application revenue in 2025 because short production cycles support higher facility turns.

- Driver: Retailers and foodservice buyers are funding local supply because indoor farms can run year-round, with 80 Acres Farms and Soli Organic serving more than 17,000 U.S. retail locations after their 2025 merger.

- Restraint: Energy intensity remains the largest barrier, with lighting and climate-control systems accounting for roughly 40.0% to 60.0% of electricity demand in fully enclosed farms.

- Opportunity: Premium fruit, medicinal plants, and seedling production represent a USD 10.6 Billion opportunity by 2034 because higher selling prices absorb LED and HVAC cost better than lettuce-only models.

- Trend: Adjustable spectrum control, AI crop recipes, robotic harvesting, and digital twins are shifting procurement from equipment-only purchases to measured yield-per-kWh performance contracts.

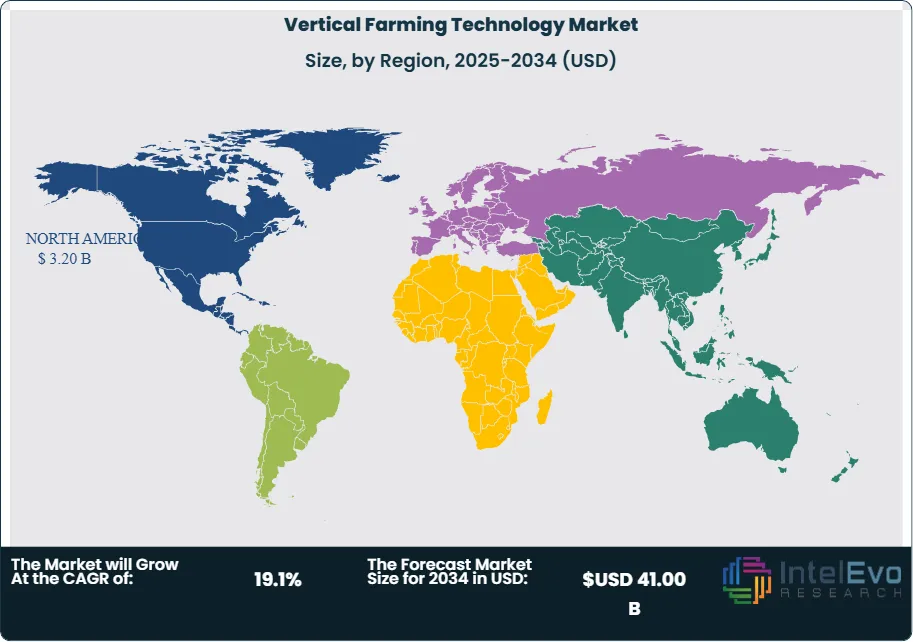

- Regional: North America led with 37.5% share in 2025, equal to USD 3.20 Billion, supported by U.S. retail partnerships, CEA research grants, and consolidation among indoor farming operators.

Key Insights Summary

- USDA Agricultural Research Service characterized vertical farming in January 2025 as indoor production in stacked layers using artificial systems such as hydroponics and aquaponics, validating the technology as a mainstream CEA format.

- 80 Acres Farms and Soli Organic created a combined indoor farming company in August 2025 with projected first-year revenue near USD 200 Million, seven vertical farms, and more than 17,000 retail outlets.

- Signify reported EUR 5.8 Billion in 2025 sales and about 27,000 employees across more than 70 markets, giving its Philips horticulture lighting unit global procurement reach.

- Heliospectra reported 2025 net sales of SEK 11.6 Million for Q4 2025 and moved its Poland contract-manufacturing setup forward, showing cost pressure across specialist lighting vendors.

- Eden Green Technology’s Texas WARN filing affected more than 100 jobs and made its Cleburne greenhouse closure permanent in December 2025, highlighting the financing risk of capital-heavy CEA projects.

- Vertical farms can reduce water demand by roughly 70.0% to 95.0% versus field production when recirculating hydroponic systems are correctly engineered, but electricity costs can offset that environmental benefit.

- The AVF Asia Forum 2026 in Bengaluru focused on medicinal and herbal plants as regulated CEA crops, signaling demand beyond salads and culinary herbs in Asia Pacific.

Competitive Landscape Overview

The vertical farming technology market is moderately fragmented, with the top four participants, Signify, 80 Acres Farms/Soli Organic, AeroFarms, and Intelligent Growth Solutions, representing an estimated 24.0% to 28.0% of addressable technology and integrated-farm activity in 2025. Market power is split between lighting vendors, farm operators, modular-system providers, automation suppliers, and seed-to-retail brands.

Competition has shifted from farm count to operating proof. Signify, Heliospectra, and ams OSRAM compete on photon efficacy, spectrum control, and fixture lifetime. 80 Acres Farms, AeroFarms, Oishii, Gotham Greens, and Planet Farms compete on crop economics, shelf presence, and plant science. Intelligent Growth Solutions, Growcer, Freight Farms asset buyers, and CubicFarms compete on modular deployment speed and lower upfront risk.

Competitive Landscape Matrix

| Company Name | Headquarters | Market Position | Key Product/Solution | Geographic Strength | Recent Strategic Move |

| Signify N.V. | Netherlands | Leader | Philips GreenPower LED and GrowWise controls | Global lighting channels | Entered the fifth year of UBC pepper-lighting trials in 2026 using GreenPower TLF 2.1 fixtures. |

| 80 Acres Farms / Soli Organic | United States | Leader | GroLoop platform and indoor farm network | United States retail network | Merged in August 2025, targeting near USD 200 Million first-year revenue and more than 17,000 retail locations. |

| AeroFarms | United States | Leader | Aeroponic vertical farms and crop analytics | United States, Middle East projects | Moved forward after post-bankruptcy restructuring and secured investor support for further farm planning in 2025. |

| Intelligent Growth Solutions | United Kingdom | Leader | Growth Tower modular vertical farming systems | Europe, Middle East, Asia | Advanced modular tower projects serving food-security programs, including Gulf-region farm infrastructure. |

| Oishii Farm Corporation | United States | Challenger | Premium strawberry and tomato vertical farms | United States metro retail | Scaled high-price fruit production from New Jersey farms and broadened beyond strawberries into tomatoes. |

| Gotham Greens Holdings | United States | Challenger | Hydroponic greenhouse and branded greens | United States grocery channels | Marked 15 years in 2026 with founder Viraj Puri moving to executive chairman. |

| Heliospectra AB | Sweden | Niche Player | MITRA and adjustable LED systems | Europe, North America | Published 2025 results in February 2026 and advanced contract manufacturing in Poland. |

| Growcer Inc. | Canada | Niche Player | Modular hydroponic farms | Canada, United States | Acquired Freight Farms assets in 2025, extending container-farm service coverage. |

| Planet Farms | Italy | Challenger | Large-scale vertical farm platform | Europe | Opened a new Milan-area headquarters in 2025 to support European farm operations. |

| Freight Farms assets / Growcer | Canada / United States | Niche Player | Containerized Leafy Green Machine assets | North America institutions | Asset transfer in 2025 preserved installed-base service options for container farms. |

By Component

The vertical farming technology market by component is led by lighting and climate systems, which together accounted for 43.0% of 2025 revenue, equal to USD 3.66 Billion. LEDs dominate capital budgets because light intensity, spectrum, photoperiod, and thermal load determine yield per kWh in enclosed farms. Signify, Heliospectra, ams OSRAM, Fluence, and Gavita compete on photon efficacy and control software, while HVAC, dehumidification, and CO2 dosing providers defend margins through energy modeling. Lighting leads irrigation at 24.0% and software at 13.0% because every rack needs fixtures before advanced analytics create value.

Hydroponic and aeroponic hardware captured 24.0% of the vertical farming technology market in 2025, or USD 2.04 Billion. Nutrient tanks, pumps, filters, substrates, root-zone sensors, and dosing systems benefit from recurring maintenance demand after facility commissioning. AeroFarms, 80 Acres Farms, Gotham Greens, and Oishii apply proprietary grow recipes on top of standard fluid-handling systems, which makes integration skill more valuable than component resale. Software, AI, sensors, and robotics represented 13.0%, while farm structures, racks, and integration services represented 20.0%. Procurement teams now compare vertical farming technology vendors by three-year cost per kg, not equipment price alone.

By Growing System

The vertical farming technology market by growing system is led by hydroponics, with 58.0% share and USD 4.94 Billion in 2025 revenue. Hydroponics dominates because nutrient-film technique, deep-water culture, drip substrates, and ebb-and-flow systems are easier to certify, train, and service than aeroponics. Gotham Greens and 80 Acres Farms use hydroponic or hybrid approaches that support predictable crop cycles. Hydroponics also suits herbs and microgreens, where roots remain short and harvest periods are measured in days or weeks.

Aeroponics held 21.5% share, equal to USD 1.83 Billion, because mist-based root delivery can reduce water and nutrient use while improving oxygen exposure. AeroFarms is the category reference operator, but aeroponic systems require tight nozzle maintenance and water-quality control. Aquaponics and hybrid biological systems represented 7.5% because fish integration adds food-safety and operational complexity. Substrate-based vertical farming, including coco coir, peat alternatives, and rockwool, held 13.0% because strawberries, tomatoes, and medicinal plants need stronger root support than lettuce.

By Application

The vertical farming technology market by application is led by leafy greens, herbs, and microgreens, which held 46.5% share in 2025, equivalent to USD 3.96 Billion. These crops fit vertical stacking because they have short cycles, low plant height, lower pollination needs, and established retail packaging. 80 Acres Farms, Soli Organic, Gotham Greens, AeroFarms, and Growcer all serve this segment. The weakness is margin compression, as lettuce competes against field growers and greenhouses during favorable seasons.

Fruits and vine crops represented 18.0% of 2025 revenue, or USD 1.53 Billion, and will outgrow leafy greens through 2034. Oishii’s strawberries and tomatoes, Plenty’s strawberry focus, and Signify’s pepper-lighting trials show why higher-value crops matter. Cannabis, medicinal plants, and pharmaceutical botanicals represented 15.5%, supported by regulated indoor production and repeatable cannabinoid or phytochemical profiles. Seedlings, plant research, and institutional food systems captured the remaining 20.0%, with universities, hospitals, military bases, and city farms using smaller footprints and modular farms.

By Facility Type

The vertical farming technology market by facility type is led by building-based farms, which represented 53.0% of 2025 revenue, equal to USD 4.52 Billion. Warehouses and purpose-built plant factories provide better vertical height, climate zoning, and automation access than container farms. 80 Acres Farms, AeroFarms, Oishii, and Planet Farms demonstrate the scale advantages of building-based assets. The tradeoff is higher permitting, HVAC design cost, and debt exposure when utilization slips below plan.

Container and modular farms accounted for 21.0% of 2025 revenue, or USD 1.79 Billion, because schools, remote communities, hotels, and defense users prefer fast installation. Growcer and Freight Farms asset operators compete in this category. Greenhouse-integrated vertical systems held 26.0%, as Gotham Greens, Signify, and greenhouse automation vendors mix sunlight with LED supplementation to lower power cost. Hybrid greenhouse-vertical systems will gain share because they reduce the all-electric burden while preserving controlled crop quality.

Regional Analysis

North America

North America led the vertical farming technology market with 37.5% share in 2025, equal to USD 3.20 Billion. The United States accounted for about USD 2.75 Billion, followed by Canada and Mexico. Demand is anchored by grocery distribution, food-service localization, USDA urban agriculture programs, and CEA research at Cornell University, Ohio State University, University of Arizona, and USDA ARS. 80 Acres Farms and Soli Organic created the strongest 2025 consolidation signal, while Eden Green Technology’s December 2025 Texas closure showed that scale alone does not remove debt and energy risk.

Europe

Europe held 27.0% of the vertical farming technology market in 2025, equal to USD 2.30 Billion. The Netherlands, Germany, the United Kingdom, France, Italy, and the Nordic countries form the core demand base because greenhouse expertise, LED manufacturing, and food-security policy are mature. Signify, Heliospectra, Planet Farms, GrowUp Farms, Infarm’s remaining assets, and IGS-linked deployments shape regional competition. EU energy-price volatility forced buyers to model variable tariffs, heat reuse, and renewable power-purchase agreements before approving new farms.

Asia Pacific

Asia Pacific accounted for 24.0% share and USD 2.04 Billion in 2025, with China, Japan, Singapore, India, South Korea, and Australia leading adoption. Singapore’s local food targets, Japan’s plant-factory expertise, India’s protected-cultivation incentives, and China’s food-safety concerns drive demand. The AVF Asia Forum 2026 in Bengaluru shifted attention toward medicinal and herbal crops, which can earn better margins than lettuce. Japan and Singapore prefer compact, automated, high-yield systems because land, labor, and import risk are structural constraints.

Latin America

Latin America represented 6.5% of the vertical farming technology market in 2025, or USD 0.55 Billion. Brazil, Mexico, Chile, Colombia, and Argentina lead adoption through urban retail, hotel foodservice, and seedling production rather than mega-farm concepts. Energy pricing, financing cost, and cold-chain gaps limit fast deployment. Container farms and greenhouse-integrated systems are more realistic than fully enclosed high-rise farms in this region because they reduce capital requirements and fit local distribution.

Middle East & Africa

Middle East and Africa held 5.0% share in 2025, equal to USD 0.43 Billion. The United Arab Emirates, Saudi Arabia, Qatar, Israel, and South Africa form the main demand cluster. Food-import dependence and water scarcity support CEA investment, while Gulf food-security programs make strawberries, herbs, and leafy greens viable for premium retail. Plenty’s 2024 UAE joint venture plan remains a reference for regional ambition, even though the company’s 2025 restructuring made financing discipline more visible across the sector.

Country Analysis

United States

The United States vertical farming technology market reached USD 2.75 Billion in 2025 and is forecast to grow at a 17.9% country CAGR through 2034. Demand is driven by grocery chains, restaurant distributors, universities, USDA UAIP grants, and food-security programs in cities. 80 Acres Farms, Soli Organic, AeroFarms, Oishii, Gotham Greens, Eden Green Technology, and Vertical Harvest represent different operating models. The 2025 80 Acres Farms-Soli Organic merger increased retail reach, while Eden Green’s Texas shutdown stressed the need for conservative power, labor, and debt assumptions.

Netherlands

The Netherlands vertical farming technology market reached USD 0.62 Billion in 2025 and is projected to expand at an 18.4% country CAGR. Dutch strength comes from horticulture engineering, greenhouse exports, Wageningen University research, and lighting leadership through Signify. Buyers in the Netherlands blend vertical racks with greenhouse assets because natural light lowers energy intensity. Signify’s 2025-2026 pepper trial with the University of British Columbia reflects Dutch-led lighting know-how moving into North American crop protocols.

Japan

Japan’s vertical farming technology market reached USD 0.54 Billion in 2025 and is projected to grow at a 19.8% country CAGR. Plant factories fit Japan’s land scarcity, aging farm labor, urban retail density, and strict food-quality standards. Spread Co., Mirai-linked plant-factory expertise, Panasonic-associated automation history, and Oishii’s Japanese agronomic influence support domestic and export knowledge flows. Japan favors small-footprint, high-control facilities for lettuce, herbs, strawberries, and specialty crops because shoppers pay for consistency and freshness.

India

India’s vertical farming technology market reached USD 0.33 Billion in 2025 and is projected to grow at a 21.0% country CAGR. Demand is led by urban centers such as Bengaluru, Mumbai, Delhi NCR, Pune, Hyderabad, and Chennai, where fresh herbs, microgreens, hydroponic lettuce, and medicinal plants can command premium prices. Protected-cultivation subsidies, start-up incubation, and the AVF Asia Forum 2026 in Bengaluru support knowledge transfer. India’s biggest constraint is power reliability, which makes hybrid solar, efficient LEDs, and low-cost climate control decisive.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Component

- Hardware

- Software

- Services

By Growing System

- Hydroponics

- Aeroponics

- Aquaponics

By Application

- Fruits & Vegetables

- Herbs & Microgreens

- Flowers & Ornamentals

- Others

By Facility Type

- Building-Based Vertical Farms

- Shipping Container Farms

- Indoor Greenhouses

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 8.52 B |

| Forecast Revenue (2034) | USD 41.00 B |

| CAGR (2025-2034) | 19.1% |

| Historical data | 2021-2025 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Component, (Hardware, Software, Services), By Growing System, (Hydroponics, Aeroponics, Aquaponics), By Application, (Fruits & Vegetables, Herbs & Microgreens, Flowers & Ornamentals, Others), By Facility Type, (Building-Based Vertical Farms, Shipping Container Farms, Indoor Greenhouses, Others), |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | 80 ACRES FARMS / SOLI ORGANIC, AEROFARMS, INTELLIGENT GROWTH SOLUTIONS, OISHII FARM CORPORATION, GOTHAM GREENS HOLDINGS, HELIOSPECTRA AB, PLANET FARMS, GROWCER INC., FREIGHT FARMS ASSETS / GROWCER, FLUENCE BIOENGINEERING, AMS OSRAM AG, CUBICFARM SYSTEMS CORP., VERTICAL HARVEST FARMS, SPREAD CO., LTD., BRIGHTFARMS, URBAN CROP SOLUTIONS, FARM.ONE, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Growing System (Hydroponics, Aeroponics, Aquaponics), By Application (Fruits, Vegetables, Herbs, Microgreens), By Facility (Building-Based, Shipping Container, Indoor Greenhouses) Region, Key Players – Dynamics, Smart Agriculture & Sustainable Food Production Trends & Forecast 2026-2034")

, By Growing System (Hydroponics, Aeroponics, Aquaponics), By Application (Fruits, Vegetables, Herbs, Microgreens), By Facility (Building-Based, Shipping Container, Indoor Greenhouses) Region, Key Players – Dynamics, Smart Agriculture & Sustainable Food Production Trends & Forecast 2026-2034")

, By Growing System (Hydroponics, Aeroponics, Aquaponics), By Application (Fruits, Vegetables, Herbs, Microgreens), By Facility (Building-Based, Shipping Container, Indoor Greenhouses) Region, Key Players – Dynamics, Smart Agriculture & Sustainable Food Production Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Vertical Farming Technology Market?

Global Vertical Farming Technology Market was valued at USD 7.18 billion in 2024 and is projected to reach USD 41.00 billion by 2034, at a CAGR of 19.1% (2026–2034).

Who are the major players in the Vertical Farming Technology Market?

80 ACRES FARMS / SOLI ORGANIC, AEROFARMS, INTELLIGENT GROWTH SOLUTIONS, OISHII FARM CORPORATION, GOTHAM GREENS HOLDINGS, HELIOSPECTRA AB, PLANET FARMS, GROWCER INC., FREIGHT FARMS ASSETS / GROWCER, FLUENCE BIOENGINEERING, AMS OSRAM AG, CUBICFARM SYSTEMS CORP., VERTICAL HARVEST FARMS, SPREAD CO., LTD., BRIGHTFARMS, URBAN CROP SOLUTIONS, FARM.ONE, Others

Which segments covered the Vertical Farming Technology Market?

By Component, (Hardware, Software, Services), By Growing System, (Hydroponics, Aeroponics, Aquaponics), By Application, (Fruits & Vegetables, Herbs & Microgreens, Flowers & Ornamentals, Others), By Facility Type, (Building-Based Vertical Farms, Shipping Container Farms, Indoor Greenhouses, Others),

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Vertical Farming Technology Market

Published Date : 16 Jul 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date