- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Warehouse Robotics as a Service Market Size, Share | CAGR 26.8%

Global Warehouse Robotics as a Service Market Size, Share, Analysis By Robot Type (Autonomous Mobile Robots (AMRs), Automated Guided Vehicles (AGVs), Robotic Picking Systems, Robotic Sorting Systems, Palletizing & Depalletizing Robots, Collaborative Robots, AS/RS Robots), By Pricing Model, By Application, By End-User, Industry Trends, Market Dynamics & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

|---|---|---|---|

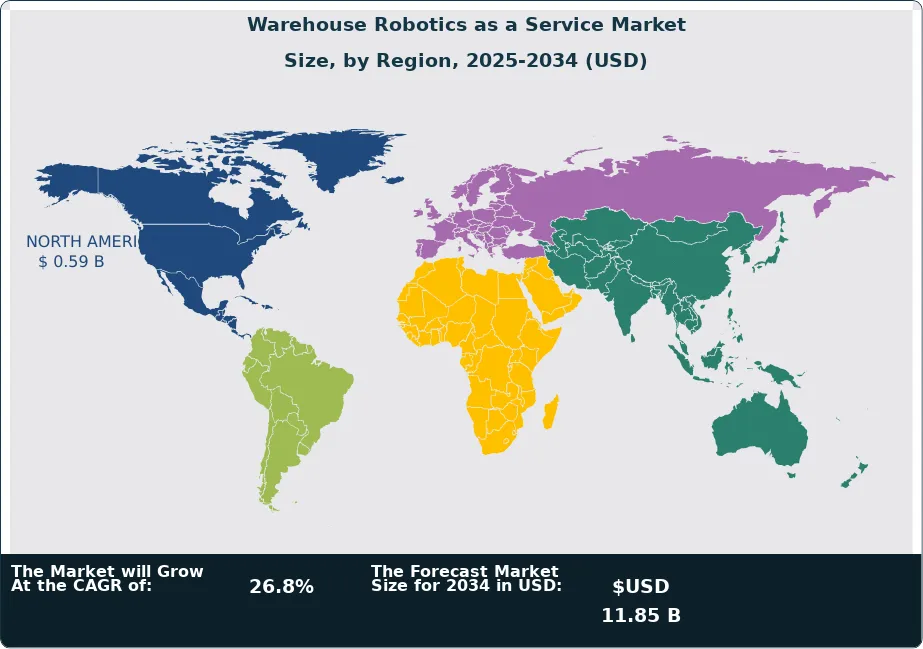

| USD 1.40 Billion | USD 11.85 Billion | 26.8% | North America, 42.3% |

The Warehouse Robotics as a Service Market was valued at approximately USD 1.10 Billion in 2024 and reached USD 1.40 Billion in 2025. The market is projected to grow to USD 11.85 Billion by 2034, expanding at a CAGR of 26.8% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 10.45 Billion over the analysis period. The expansion reflects sustained spending on subscription-based autonomous mobile robots (AMRs), goods-to-person systems, and automated storage and retrieval (AS/RS) deployments that convert capital expenditure into operational expenditure for warehouse operators.

Get More Information about this report -

Request Free Sample ReportDemand acceleration during 2025 traces directly to the International Federation of Robotics finding that the global RaaS fleet for transportation and logistics grew 42% in 2024, with 102,900 service robots sold for transportation and logistics applications worldwide. Of that volume, approximately 81,800 units were mobile robots dedicated to intralogistics, with Asia Pacific accounting for nearly 84% of intralogistics mobile robot supply, Europe 11%, and the Americas 5%. Persistent labor shortages compound the demand: industry projections place unfilled warehouse positions in the United States at approximately 2.1 million by 2030, while approximately 95% of warehouses globally remain unautomated.

Regulatory and standards activity reinforced the warehouse robotics as a service market through 2025. The Association for Advancing Automation (A3) published ANSI/A3 R15.06-2025 on October 29, 2025, replacing the 2012 industrial robot safety standard with a 403-page document harmonized to ISO 10218-1:2025 and ISO 10218-2:2025. ANSI/A3 R15.06-3-2025, approved October 7, 2025, addresses user requirements specific to warehouse and end-user environments, while ANSI/RIA R15.08 Parts 1 and 2 govern industrial mobile robot deployments. OSHA cites these standards under General Duty Clause Section 5(a)(1) inspections.

North America held the largest revenue share at 42.3% in 2025, valued at approximately USD 0.59 Billion, driven by Locus Robotics, Symbotic, and inVia Robotics deployments across DHL, GXO Logistics, Walmart, Target, and Albertsons distribution centers. Asia Pacific captured the second-largest share at 29.5% and is forecast as the fastest-growing region at a 30.4% CAGR through 2034 because Geek+, Hai Robotics, and Quicktron have built dense subscription deployments across Chinese 3PL and e-commerce operators. AMRs led robot-type segmentation at 38.4% revenue share in 2025 because LocusONE, GreyMatter, and CarouselAI orchestration platforms enable rapid OPEX-based scaling.

The forward outlook through 2034 is shaped by three structural shifts. Fleet orchestration software will migrate from differentiator to commodity as Locus, Geek+, and Symbotic open APIs to multi-vendor robot fleets. Outcome-based pricing models priced per pick or per pallet, currently around 5% of contracts, will reach an estimated 18% by 2030 because operators tie costs to throughput rather than fleet size. Humanoid bipedal robots from Agility Robotics and Figure AI will enter RaaS catalogs by 2027, opening brownfield warehouses that lack the floor flatness or rack regularity AMR fleets require.

Market Definition & Scope

The warehouse robotics as a service market is defined as subscription, per-pick, per-hour, or outcome-based contracts that bundle robotic hardware, fleet management software, deployment, ongoing maintenance, and software upgrades into a recurring operating expense. The market encompasses autonomous mobile robots (AMRs), automated guided vehicles (AGVs), goods-to-person and automated storage and retrieval (AS/RS) systems, robotic picking arms, sortation robots, and autonomous forklifts when delivered through subscription contracts rather than capital purchase.

This analysis covers warehouse and distribution-center deployments only, including 3PL fulfillment centers, e-commerce hubs, retail distribution facilities, and industrial intralogistics. Excluded from scope are last-mile delivery robots from Avride and Starship Technologies, drone logistics from Zipline, surgical and medical robots, agricultural robots, household robots, manufacturing robotic cells inside production lines, and capital-purchase warehouse robotics where the customer holds title to the asset. Warehouse RaaS represents approximately 14.7% of the broader USD 9.50 Billion global warehouse robotics parent market in 2025.

, Automated Guided Vehicles (AGVs), Robotic Picking Systems, Robotic Sorting Systems, Palletizing & Depalletizing Robots, Collaborative Robots, AS/RS Robots), By Pricing Model, By Application, By End-User, Industry Trends, Market Dynamics & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global warehouse robotics as a service market grows from USD 1.40 Billion in 2025 to USD 11.85 Billion by 2034, expanding at a 26.8% CAGR over the forecast period.

- Segment Dominance by Robot Type: Autonomous mobile robots held 38.4% revenue share in 2025, generating USD 0.54 Billion, anchored by Locus Robotics, Geek+, and 6 River Systems platforms.

- Segment Dominance by Application: Order picking and fulfillment captured 38.7% of revenue in 2025, the direct result of e-commerce volume requiring 2x to 3x productivity gains over manual picking.

- Driver: International Federation of Robotics data show RaaS fleet growth of 42% in 2024 for transportation and logistics, against an unautomated warehouse base estimated at 95% of global facilities.

- Restraint: Subscription unit economics remain unproven over multi-year horizons, with Locus Robotics emerging from Chapter 11 in 2023 and several AMR competitors compressing margins to win contracts.

- Opportunity: Outcome-based pricing tied to picks-per-hour represents an estimated USD 2.1 Billion incremental opportunity by 2030 as Symbotic, Locus, and AutoStore expand performance-linked contracts.

- Trend: Humanoid robot integration by Agility Robotics (Digit) and Figure AI is being piloted at GXO and Spanx warehouses with subscription contracts targeting 2026-2027 commercial availability.

- Regional: North America led with 42.3% share and USD 0.59 Billion revenue in 2025, anchored by Symbotic deployments at Walmart, Target, and Albertsons distribution centers.

Key Insights Summary

- The International Federation of Robotics World Robotics 2025 report (released September 2025) recorded 102,900 transportation and logistics service robots sold worldwide in 2024, a 14% increase, with the RaaS fleet specifically growing 42% during the same period.

- Locus Robotics surpassed 6 billion robot-assisted picks in October 2025, the fastest-ever pace, with deployments at more than 350 facilities across 20 countries and a customer base exceeding 150 enterprises including DHL, GXO Logistics, and Radial.

- ANSI/A3 R15.06-2025 was published October 29, 2025 as a 403-page replacement for the 2012 industrial robot safety standard, adding cybersecurity requirements, functional safety clarifications, and Part 3 user obligations approved October 7, 2025.

- Symbotic agreed in January 2026 to acquire Walmart's Advanced Systems and Robotics business for USD 200 million in cash plus up to USD 350 million contingent consideration, alongside USD 230 million in development funding from Walmart, expanding micro-fulfillment addressable market by USD 300 billion in the United States.

- Asia Pacific accounted for approximately 84% of global mobile robot supply for intralogistics in 2024 according to International Federation of Robotics data, primarily through Geek+, Hai Robotics, and Quicktron exports to global 3PL operators.

- Western European countries reached 267 industrial robots per 10,000 manufacturing employees in 2024 versus 204 in North America and 131 in Asia, signaling Europe's higher automation density even as RaaS adoption lags United States subscription penetration.

Competitive Landscape Overview

The warehouse robotics as a service market is moderately fragmented with the top four vendors (Locus Robotics, Symbotic, Geek+, and AutoStore) accounting for an estimated combined 38% of global revenue in 2025. Competition shifted through 2025 from hardware specifications toward fleet orchestration software, deployment speed (4 to 6 weeks for Locus versus 6 to 12 months for AutoStore), and proven unit economics for multi-year contracts. Symbotic's January 2026 acquisition of Walmart's Advanced Systems and Robotics for USD 200 million plus contingent consideration and its February 2026 acquisition of Fox Robotics signal aggressive consolidation by public-market players.

Pure-play RaaS specialists including Locus Robotics, inVia Robotics, Vecna Robotics, and Brightpick lead in subscription-first contracting, while broader automation vendors including Symbotic, Honeywell, and ABB compete on integrated platform deals. New entrants Mytra (USD 120 million Series C) and Dexory (EUR 143 million Series C) are differentiating on data-first warehouse intelligence, while humanoid pioneers Agility Robotics and Figure AI are positioning for 2027 commercial RaaS launches in brownfield facilities that AMR fleets cannot serve.

Competitive Landscape Matrix

| Company Name | Headquarters | Market Position | Key Product/Solution | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| Locus Robotics | United States | Leader | LocusONE platform with Origin, Vector, and Array AMRs | Global, NA-led | Surpassed 6 billion picks in October 2025; launched Locus Array at MODEX 2025 |

| Symbotic | United States | Leader | SymBots fleet for case handling and dense storage | North America | Acquired Fox Robotics in Q1 FY2026 and Walmart ASR for USD 200M in Q1 2026 |

| Geek+ Robotics | China | Leader | Shelf-to-Person, PopPick, MovePick AMRs orchestrated by CarouselAI | Asia, Europe | Launched next-generation RaaS platform for global logistics providers in Q1 2025 |

| AutoStore | Norway | Leader | Cube storage AS/RS with R5 Pro and Carousel robots | Global, Europe-led | Expanded distribution through 18 system integrators in 2025 |

| 6 River Systems (Ocado) | United States | Challenger | Chuck collaborative AMRs with cloud orchestration | North America, Europe | Operating under Ocado Intelligent Automation banner since 2023 sale |

| GreyOrange | United States/India | Challenger | GreyMatter AI orchestration with Ranger AMRs | Global | Expanded GreyMatter platform integrations across 3PL operators in 2025 |

| Exotec | France | Challenger | Skypod climbing AS/RS robots | Europe, North America | Launched Next-Gen Skypod in February 2026 |

| Berkshire Grey | United States | Challenger | Robotic Pick and Pack solutions | North America | Operates as SoftBank subsidiary post-2023 acquisition |

| inVia Robotics | United States | Niche Player | Picker autonomous mobile robots | North America | Won multi-year RaaS contract with major US retailer in Q1 2025 |

| Brightpick | Slovakia | Niche Player | Autopicker multi-purpose AI robot | Europe, North America | Launched Autopicker 2.0 in June 2025 |

By Robot Type

The warehouse robotics as a service market by robot type is led by autonomous mobile robots (AMRs), which captured 38.4% revenue share in 2025 valued at approximately USD 0.54 Billion. AMRs dominate because Locus Origin, Locus Vector, Geek+ Shelf-to-Person, and 6 River Systems Chuck robots can be deployed in 4 to 6 weeks without warehouse retrofit, supporting brownfield 3PL operators that cannot tolerate construction downtime. Automated guided vehicles followed at 23.7% share, primarily for high-payload pallet movement under subscription contracts from Seegrid, Vecna Robotics, and Toyota Material Handling.

Goods-to-person and AS/RS systems including AutoStore, Exotec Skypod, and Symbotic SymBot fleets accounted for 19.1% in 2025. While AS/RS deployments require 6 to 12 month construction cycles incompatible with rapid AMR scaling, they deliver up to 400% storage density gains and are increasingly procured via subscription through partner integrators. Robotic picking arms (Berkshire Grey, RightHand Robotics, Covariant) reached 12.6%, with Covariant Robotics Foundation Model RFM-1 (introduced November 2024) enabling unseen-item handling. Sortation and conveyor robots held the residual 6.2% share.

By Pricing Model

Per-robot-per-month subscription contracts captured 56.8% of revenue in 2025 because the format aligns with operator IT budgeting cycles and matches the predictable cost model 3PL contract-renewal teams require. Pay-per-pick or pay-per-hour pricing held 24.3%, with Relay Robotics at approximately USD 4 per hour and Locus Robotics offering per-pick variants for seasonal customers. Hybrid base-fee-plus-variable pricing reached 13.5% in 2025, particularly inside Symbotic and Honeywell platform deployments where fleet baseline plus throughput overage matches uneven volume profiles.

Outcome-based pricing tied to defined service levels (orders shipped on time, picks per hour, error rate) accounted for the residual 5.4% of revenue in 2025 and is forecast at a 38.5% CAGR through 2034, the fastest of any pricing model. Outcome-based contracts are particularly attractive in healthcare logistics (Locus reports 60% of US medical supplies including artificial knees ship next-day via Locus robots) and pharmaceuticals where service-level penalties carry contractual force. ROI calculations from buying committees increasingly justify warehouse RaaS by comparing 2x to 3x picker productivity gains against per-pick subscription fees of USD 0.04 to USD 0.12.

By Application

Order picking and fulfillment captured the largest application share at 38.7% in 2025 because e-commerce SKU diversity has expanded beyond manual picker capacity, and AMRs deliver measured productivity gains of 2x to 3x against baseline picker rates of 60 to 90 units per hour. Material transport followed at 24.6% revenue share, addressing pallet, tote, and case movement between zones via Vecna, Seegrid, and Locus Vector deployments. Storage and retrieval applications held 18.2%, dominated by AutoStore, Exotec, and Symbotic AS/RS subscription contracts.

Sorting and packaging captured 11.8% of revenue in 2025, with Berkshire Grey, Covariant, and Brightpick Autopicker 2.0 (launched June 2025) covering parcel sort and depalletization workflows. Inventory management and reverse logistics accounted for the residual 6.7%, including cycle counting drones from Dexory and returns processing automation. Application-specific RaaS procurement checklists from buyers increasingly require sub-30-second cycle times for picking, 99.5%+ order accuracy, and integration with SAP EWM, Oracle WMS, Manhattan, or Korber within an 8-week project window.

By End-User

E-commerce and retail captured 37.4% of revenue in 2025 because order volume growth and same-day delivery service-level agreements forced fulfillment center automation. Walmart's USD 14 billion automation commitment and Amazon Robotics' continuing internal scaling anchor this category, with Symbotic supplying Walmart, Target, and Albertsons under multi-year contracts. Third-party logistics (3PL) operators followed at 24.8% share, led by DHL Supply Chain, GXO Logistics, Ceva, ASDA, and Radial deployments where robots-as-a-service economics fit short customer contract terms better than capital purchases.

Manufacturing held 16.7% of revenue, particularly automotive parts and electronics intralogistics where AMRs replace manual material movement between assembly cells. Food and beverage captured 9.5%, an end-user segment that Symbotic specifically targets through cold-chain dense AS/RS. Pharmaceuticals and healthcare logistics held 6.8% with Locus reporting that 60% of US medical supplies including artificial knees ship next-day via Locus AMRs. Apparel, automotive aftermarket, and other distribution segments held the residual 4.8% combined.

Regional Analysis

North America

The global warehouse robotics as a service market spans five regions with distinct adoption profiles. North America held the largest 2025 share at 42.3%, valued at approximately USD 0.59 Billion. The United States anchored regional revenue through Symbotic deployments at Walmart, Target, and Albertsons distribution centers, Locus Robotics installations at DHL Supply Chain and GXO Logistics, and Honeywell Robotics Innovation Hub investments of USD 50 million. Canada contributed via Avidbots-DHL partnership deployments and Clearpath Robotics enterprise sales. Mexico saw rising automation adoption through Geek+ and Hai Robotics under USMCA-driven nearshoring. The November 2025 ANSI/A3 R15.06-2025 publication and Part 3 user-requirements release reinforced North American compliance demand.

Asia Pacific

Asia Pacific captured 29.5% revenue share in 2025 valued at approximately USD 0.41 Billion, and is forecast as the fastest-growing region at a 30.4% CAGR through 2034. China dominated regional supply with Geek+, Hai Robotics, Quicktron, and ForwardX exporting more than 84% of global intralogistics mobile robot units according to International Federation of Robotics data. Japan's working time legislation effective April 2024 (capping heavy truck driver hours at 960 annually) created acute logistics labor pressure that mobile robotics solutions are filling. India recorded 9,100 industrial robot installations in 2024 (up 7%), with warehousing applications driving SME-targeted RaaS contracts. South Korea installed 30,600 industrial robot units in 2024, ranking fourth globally.

Europe

Europe represented 21.7% revenue share in 2025 valued at approximately USD 0.30 Billion. Germany led with 26,982 industrial robot installations in 2024 (32% of European total), driven by Industrie 4.0 strategy continuation and BSI cybersecurity certification of mobile robot fleets. The United Kingdom recorded 2,500 installations in 2024, and Italy 8,783 units. Exotec (France) launched Next-Gen Skypod in February 2026, while AutoStore (Norway) extended distribution through 18 system integrators. The EU Machinery Regulation 2023/1230, applicable from January 2027, will tighten safety requirements for mobile robotic systems including AMRs and AGVs.

Latin America

Latin America held 3.8% share in 2025 valued at approximately USD 0.05 Billion, with Brazil leading regional adoption through Mercado Libre fulfillment automation and 3PL operators serving cross-border e-commerce. Mexican distribution centers serving USMCA supply chains accelerated AMR adoption during 2025, with Geek+ and Locus Robotics extending channel partnerships through regional integrators including Penske Logistics Mexico and DHL Supply Chain Brazil.

Middle East and Africa

Middle East and Africa captured 2.7% revenue share in 2025 valued at approximately USD 0.04 Billion. Saudi Arabia's Vision 2030 logistics-hub strategy and the United Arab Emirates' DP World automation rollout anchored regional adoption, with Geek+ and Hai Robotics deployments in Riyadh, Jeddah, and Dubai super-regional distribution centers. South Africa's e-commerce expansion under retailers Takealot and Pick n Pay drove smaller-scale Locus and inVia deployments through 2025.

Country Analysis

United States

The United States warehouse robotics as a service market reached approximately USD 0.51 Billion in 2025, growing at a country-specific CAGR of 26.4% through 2034. Federal demand traces to OSHA General Duty Clause enforcement coupled with the new ANSI/A3 R15.06-2025 standard published October 29, 2025 and ANSI/RIA R15.08 industrial mobile robot safety guidelines. The US Department of Labor projected 2.1 million unfilled warehouse positions by 2030, accelerating procurement among Fortune 500 retailers. Walmart's USD 14 billion automation budget and Amazon Robotics' deployment of more than 750,000 robots across fulfillment centers anchor industry demand. State-level momentum from California Assembly Bill 1228 warehouse worker rules and the Washington Warehouse Worker Protection Act has compounded enterprise spending.

China

China generated approximately USD 0.18 Billion in 2025 warehouse robotics as a service revenue, growing at a country CAGR of 31.7% through 2034. The Made in China 2025 initiative and Ministry of Industry and Information Technology robotics roadmap drive subscription robotics adoption among 3PL operators including Cainiao, JD Logistics, and SF Express. Geek+, Hai Robotics, Quicktron, and ForwardX collectively exported more than 84% of global intralogistics mobile robot units in 2024 according to International Federation of Robotics data, while domestic deployment scale rose with cross-border e-commerce volumes from Shein and Temu.

Japan

Japan recorded approximately USD 0.085 Billion in 2025 warehouse robotics as a service revenue with a country CAGR of 28.1% through 2034. The April 2024 working time legislation capping heavy truck driver hours at 960 annually created acute intralogistics labor pressure that mobile robotics is filling, and Japanese 3PL operators including Yamato Holdings, Sagawa Express, and Nippon Express scaled subscription robot fleets through 2025. Ministry of Economy, Trade and Industry (METI) Smart Factory subsidies under Robot Strategy 2.0 fund up to 50% of RaaS deployment costs for SME logistics. Japan installed 44,500 industrial robot units in 2024, retaining its second-largest market position globally with 450,500 units in operational use.

Germany

Germany generated approximately USD 0.105 Billion in 2025 warehouse robotics as a service revenue, with a country CAGR of 25.6% through 2034. The Federal Office for Information Security (BSI) certification framework, the German NIS2 implementation law (NIS2-Umsetzungsgesetz finalized late 2025), and the Plattform Industrie 4.0 reference architecture govern automated warehouse deployments. Volkswagen, BMW, Bosch, and Siemens drive enterprise adoption, while logistics operators DHL Supply Chain, Dachser, and Kuehne+Nagel expanded BITO Lagertechnik partnership deployments after the February 2025 Locus Robotics partnership announcement. Germany installed 26,982 industrial robot units in 2024, the largest European market and fifth largest globally.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Robot Type

- Autonomous Mobile Robots (AMRs)

- Automated Guided Vehicles (AGVs)

- Robotic Picking Systems

- Robotic Sorting Systems

- Palletizing and Depalletizing Robots

- Collaborative Robots (Cobots)

- Automated Storage and Retrieval System (AS/RS) Robots

- Inventory Scanning and Inspection Robots

- Goods-to-Person (GTP) Robots

- Forklift and Material Handling Robots

By Pricing Model

- Subscription-Based Model

- Pay-Per-Use Model

- Usage-Based Billing Model

- Lease-Based Model

- Outcome-Based Pricing Model

- Hybrid Pricing Model

By Application

- Order Picking and Fulfillment

- Sorting and Packaging

- Inventory Management and Cycle Counting

- Material Handling and Transportation

- Palletizing and Depalletizing

- Goods Receiving and Put-Away

- Returns Processing

- Quality Inspection and Monitoring

- Cross-Docking Operations

- Warehouse Security and Surveillance

By End-User

- E-Commerce and Retail

- Third-Party Logistics (3PL) Providers

- Manufacturing

- Food and Beverage

- Healthcare and Pharmaceuticals

- Automotive

- Consumer Electronics

- Aerospace and Defense

- Cold Chain and Refrigerated Warehousing

- Others (Chemicals, Textiles, and General Merchandise)

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 1.40 B |

| Forecast Revenue (2034) | USD 11.85 B |

| CAGR (2025-2034) | 26.8% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Robot Type, (Autonomous Mobile Robots (AMRs), Automated Guided Vehicles (AGVs), Robotic Picking Systems, Robotic Sorting Systems, Palletizing and Depalletizing Robots, Collaborative Robots (Cobots), Automated Storage and Retrieval System (AS/RS) Robots, Inventory Scanning and Inspection Robots, Goods-to-Person (GTP) Robots, Forklift and Material Handling Robots), By Pricing Model, (Subscription-Based Model, Pay-Per-Use Model, Usage-Based Billing Model, Lease-Based Model, Outcome-Based Pricing Model, Hybrid Pricing Model), By Application, (Order Picking and Fulfillment, Sorting and Packaging, Inventory Management and Cycle Counting, Material Handling and Transportation, Palletizing and Depalletizing, Goods Receiving and Put-Away, Returns Processing, Quality Inspection and Monitoring, Cross-Docking Operations, Warehouse Security and Surveillance), By End-User, (E-Commerce and Retail, Third-Party Logistics (3PL) Providers, Manufacturing, Food and Beverage, Healthcare and Pharmaceuticals, Automotive, Consumer Electronics, Aerospace and Defense, Cold Chain and Refrigerated Warehousing, Others (Chemicals, Textiles, and General Merchandise)) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | LOCUS ROBOTICS, SYMBOTIC, GEEK+ ROBOTICS, AUTOSTORE, 6 RIVER SYSTEMS (OCADO), GREYORANGE, EXOTEC, BERKSHIRE GREY (SOFTBANK), INVIA ROBOTICS, BRIGHTPICK, VECNA ROBOTICS, FETCH ROBOTICS (ZEBRA TECHNOLOGIES), HAI ROBOTICS, QUICKTRON, SEEGRID, AGILITY ROBOTICS, COVARIANT, MYTRA, DEXORY, FORMIC TECHNOLOGIES, OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, Automated Guided Vehicles (AGVs), Robotic Picking Systems, Robotic Sorting Systems, Palletizing & Depalletizing Robots, Collaborative Robots, AS/RS Robots), By Pricing Model, By Application, By End-User, Industry Trends, Market Dynamics & Forecast 2026-2034")

, Automated Guided Vehicles (AGVs), Robotic Picking Systems, Robotic Sorting Systems, Palletizing & Depalletizing Robots, Collaborative Robots, AS/RS Robots), By Pricing Model, By Application, By End-User, Industry Trends, Market Dynamics & Forecast 2026-2034")

, Automated Guided Vehicles (AGVs), Robotic Picking Systems, Robotic Sorting Systems, Palletizing & Depalletizing Robots, Collaborative Robots, AS/RS Robots), By Pricing Model, By Application, By End-User, Industry Trends, Market Dynamics & Forecast 2026-2034")

Frequently Asked Questions

How big is the Warehouse Robotics as a Service Market?

The Global Warehouse Robotics as a Service Market was valued at USD 1.10 Billion in 2024 and is projected to reach USD 11.85 Billion by 2034, growing at a CAGR of 26.8% from 2026 to 2034. Growth is driven by rising warehouse automation, expanding e-commerce fulfillment operations, increasing adoption of Robotics-as-a-Service (RaaS) models, and advancements in AI-powered autonomous mobile robots, cloud-based fleet management, and intelligent supply chain optimization solutions worldwide.

Who are the major players in the Warehouse Robotics as a Service Market?

LOCUS ROBOTICS, SYMBOTIC, GEEK+ ROBOTICS, AUTOSTORE, 6 RIVER SYSTEMS (OCADO), GREYORANGE, EXOTEC, BERKSHIRE GREY (SOFTBANK), INVIA ROBOTICS, BRIGHTPICK, VECNA ROBOTICS, FETCH ROBOTICS (ZEBRA TECHNOLOGIES), HAI ROBOTICS, QUICKTRON, SEEGRID, AGILITY ROBOTICS, COVARIANT, MYTRA, DEXORY, FORMIC TECHNOLOGIES, OTHERS

Which segments covered the Warehouse Robotics as a Service Market?

By Robot Type, (Autonomous Mobile Robots (AMRs), Automated Guided Vehicles (AGVs), Robotic Picking Systems, Robotic Sorting Systems, Palletizing and Depalletizing Robots, Collaborative Robots (Cobots), Automated Storage and Retrieval System (AS/RS) Robots, Inventory Scanning and Inspection Robots, Goods-to-Person (GTP) Robots, Forklift and Material Handling Robots), By Pricing Model, (Subscription-Based Model, Pay-Per-Use Model, Usage-Based Billing Model, Lease-Based Model, Outcome-Based Pricing Model, Hybrid Pricing Model), By Application, (Order Picking and Fulfillment, Sorting and Packaging, Inventory Management and Cycle Counting, Material Handling and Transportation, Palletizing and Depalletizing, Goods Receiving and Put-Away, Returns Processing, Quality Inspection and Monitoring, Cross-Docking Operations, Warehouse Security and Surveillance), By End-User, (E-Commerce and Retail, Third-Party Logistics (3PL) Providers, Manufacturing, Food and Beverage, Healthcare and Pharmaceuticals, Automotive, Consumer Electronics, Aerospace and Defense, Cold Chain and Refrigerated Warehousing, Others (Chemicals, Textiles, and General Merchandise))

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Warehouse Robotics as a Service Market

Published Date : 11 Jun 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date