- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Water Recycling and Reuse Market Size, Share | CAGR 10.1%

Global Water Recycling and Reuse Market Size, Share & Industry Analysis By Equipment (Systems(Filtration, Activated Carbon Filtration, Disinfection, Biological Treatment, Pumps and Monitoring), Membrane Bioreactors, Sludge Treatment Equipment), By Capacity (Less than 25,000 m³/day, 25,000–50,000 m³/day, 50,001–100,000 m³/day, 100,001–250,000 m³/day and Above 250,000 m³/day), By End Use (Municipal, Industrial, Commercial, Agricultural Irrigation and Residential), By Water Source (Municipal Wastewater, Industrial Wastewater, Greywater, Blackwater and Stormwater Runoff) Industry Region & Key Players – Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

|---|---|---|---|

| USD 19.20 Billion | USD 45.50 Billion | 10.1% | Asia Pacific, 42.0% |

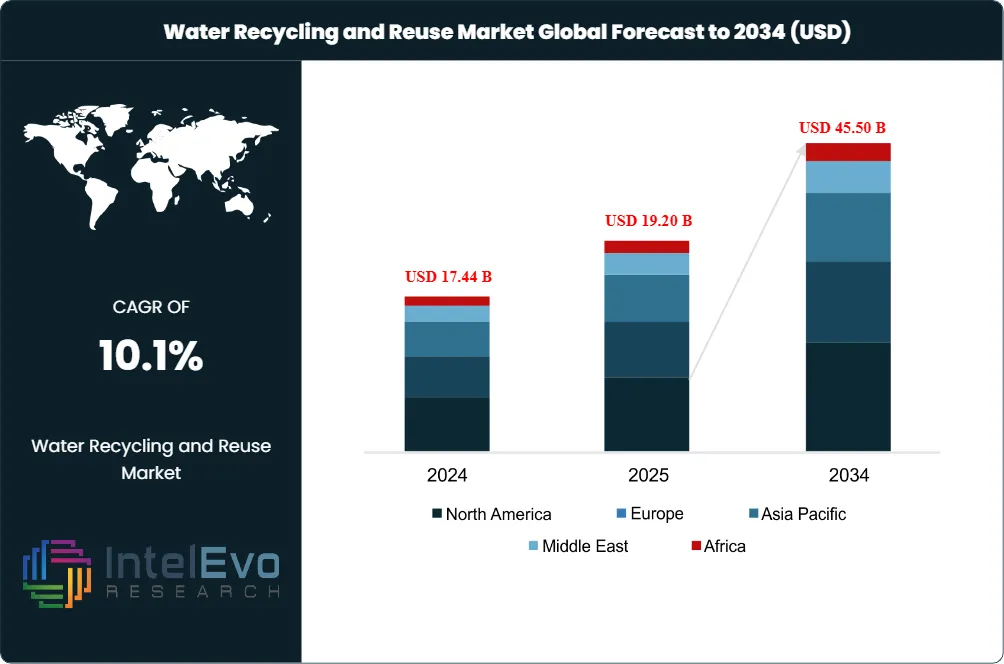

The Water Recycling and Reuse Market was valued at USD 17.44 Billion in 2024 and USD 19.20 Billion in 2025. The market is projected to reach USD 45.50 Billion by 2034, expanding at a CAGR of 10.1% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 26.30 Billion over the analysis period, driven by mandatory disclosure regimes, climate-induced freshwater scarcity affecting more than 2 billion people per UN-Water 2024 reporting, and accelerated industrial zero-liquid-discharge deployments across semiconductor, energy and data center value chains.

Get More Information about this report -

Request Free Sample ReportRegulatory action is the dominant catalyst across the water recycling and reuse market. The U.S. Environmental Protection Agency released the Water Reuse Action Plan 2.0 on April 16, 2026 under Administrator Lee Zeldin, expanding national framework actions for industrial reuse, AI data center cooling and energy sector adoption. The European Union Regulation (EU) 2020/741 on minimum requirements for water reuse, applicable since June 26, 2023, defines four reclaimed water quality classes for agricultural irrigation across all 27 member states, while California State Water Resources Control Board direct potable reuse regulations under Title 22, approved by the Office of Administrative Law in August 2024, became operational on October 1, 2024.

Industrial demand compounds the regulatory tailwind. Veolia Environnement secured a USD 550 million contract in May 2025 for the design, construction and 16-year operation of an ultrapure water and wastewater treatment facility serving a major U.S. Midwest semiconductor plant. Veolia Water Technologies generated revenues of EUR 4.973 billion and EBITDA of EUR 612 million in 2024, with stable Q1 2025 revenues of EUR 1.156 billion and over USD 750 million in new contracts secured during the quarter across energy and semiconductors. The GreenUp strategic roadmap targets a 50% Veolia Water Technologies revenue increase by 2030, including approximately EUR 1 billion in PFAS treatment work.

Technology and innovation dynamics are reshaping the water recycling and reuse market through membrane bioreactor maturation, AI-driven process optimization and decentralized deployment models. The Tuas Water Reclamation Plant under design in Singapore by Jacobs Engineering is targeted as the world's largest membrane bioreactor facility at 800,000 cubic meters per day. DuPont Water Solutions received the 2025 BIG Innovation Award on January 30, 2025 for the Sustainability Navigator digital tool that helps customers select efficient water purification technologies.

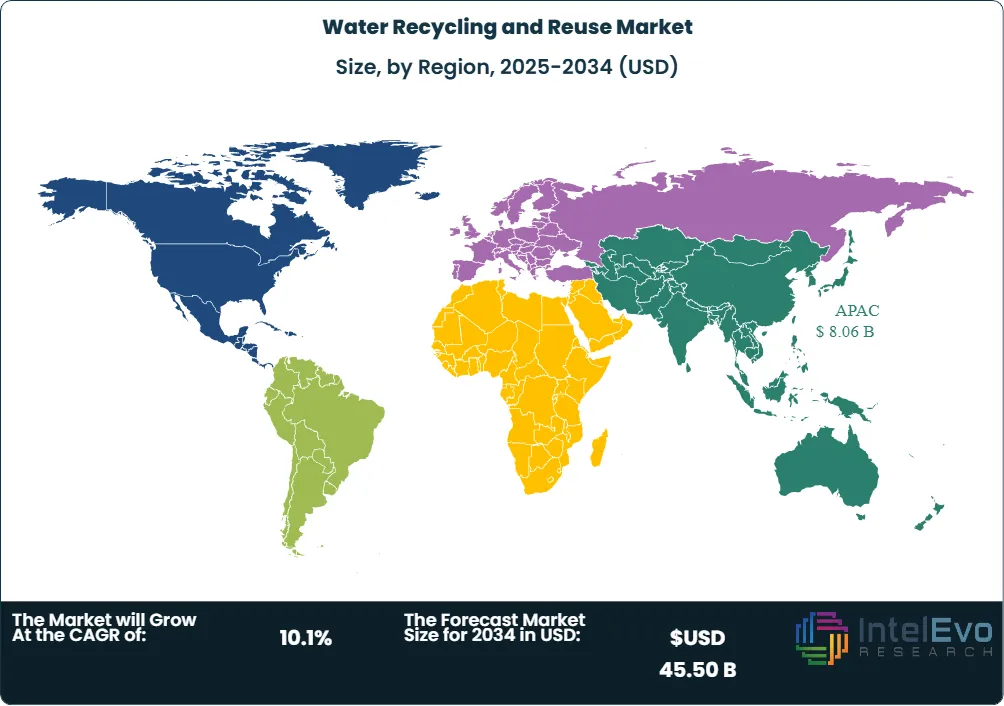

Asia Pacific held an estimated 42.0% revenue share of the water recycling and reuse market in 2025, anchored by Singapore NEWater meeting up to 40% of national water demand and forecast to reach 55% by 2060, India urban infrastructure programs, and China industrial reuse mandates across more than 300 listed entities. North America registered the second-largest revenue share, driven by California Title 22 direct potable reuse permits issued from October 1, 2024, Texas Senate Bill 14 effective January 1, 2026 creating impact fee credits for water reuse projects, and Illinois House Bill 3046 repealing the state water reuse prohibition.

Outlook through 2034 anticipates continued double-digit growth in the water recycling and reuse market as direct potable reuse, industrial closed-loop systems and agricultural reclaimed water capture incremental share. Convergence of EU Water Reuse Regulation, EPA WRAP 2.0, India SEBI BRSR Core water disclosure mandates and Middle East Vision 2030 water strategies will favour vendors with multi-technology portfolios, advanced membrane capabilities and AI-driven smart monitoring through the forecast period.

Market Definition & Scope

The water recycling and reuse market is defined as the integrated equipment, technology and service ecosystem that captures wastewater, treats it through primary, secondary and tertiary processes, and delivers reclaimed water for non-potable, indirect potable and direct potable end-uses. The market encompasses membrane filtration systems, membrane bioreactors, reverse osmosis, ultrafiltration, advanced oxidation processes, ultraviolet disinfection, zero-liquid-discharge plants, smart monitoring software and engineering, procurement and construction services.

This analysis includes municipal wastewater reuse, industrial closed-loop systems, agricultural irrigation reclaimed water, and commercial and residential greywater systems sold to utilities, manufacturers and end-users globally. It excludes pure desalination of seawater (covered separately), bottled water purification, point-of-use residential filters, and stormwater capture without treatment for reuse. The water recycling and reuse market sits within the parent global water and wastewater treatment market estimated at over USD 305 billion in 2024, with reuse capturing approximately 6% of total spend in 2025 and rising through the forecast period.

, Membrane Bioreactors, Sludge Treatment Equipment), By Capacity (Less than 25,000 m³/day, 25,000–50,000 m³/day, 50,001–100,000 m³/day, 100,001–250,000 m³/day and Above 250,000 m³/day), By End Use (Municipal, Industrial, Commercial, Agricultural Irrigation and Residential), By Water Source (Municipal Wastewater, Industrial Wastewater, Greywater, Blackwater and Stormwater Runoff) Industry Region & Key Players – Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The water recycling and reuse market expanded from USD 19.20 Billion in 2025 to a projected USD 45.50 Billion by 2034, advancing at a 10.1% CAGR over the 2025-2034 forecast period.

- Segment Dominance: Tertiary equipment, including reverse osmosis, ultrafiltration and ultraviolet disinfection systems, held the largest revenue share of the water recycling and reuse market in 2025, exceeding 38% of total equipment spend.

- Segment Dominance: The Industrial end-use segment commanded approximately 42% of water recycling and reuse market revenue in 2025, with industrial reuse forecast to register the swiftest 12.9% CAGR through 2034.

- Driver: U.S. EPA Water Reuse Action Plan 2.0 launched April 16, 2026 created federal momentum for AI data center, energy and industrial reuse, while Texas Senate Bill 14 effective January 1, 2026 added impact-fee credits for water reuse projects across the state.

- Restraint: High capital expenditure of USD 5-15 million for mid-scale municipal reclamation plants and 3-5 year permitting cycles continue to slow adoption despite cloud-based smart-monitoring price reductions.

- Opportunity: Direct potable reuse is forecast to register a 13.0% CAGR through 2034, the fastest sub-segment, driven by California Title 22 permits issued from October 1, 2024 and Florida Environmental Regulation Commission potable reuse rules approved December 13, 2024.

- Trend: AI-powered process optimization and predictive maintenance, exemplified by DuPont Sustainability Navigator and Xylem Vue, dominated 2025-2026 vendor roadmaps alongside membrane bioreactor scale-up at Singapore Tuas Water Reclamation Plant.

- Regional: Asia Pacific led the water recycling and reuse market with 42.0% share and approximately USD 8.06 Billion in revenue in 2025, with Singapore NEWater, India Smart Cities Mission and China industrial reuse anchoring regional demand.

Key Insights Summary

- U.S. EPA Administrator Lee Zeldin launched Water Reuse Action Plan 2.0 on April 16, 2026, expanding national reuse actions to industry, AI data centers and energy sectors, building on the original 2020 framework that grew to over 96 actions and 215 partner leaders.

- EU Regulation 2020/741 on minimum requirements for water reuse became applicable across all 27 EU member states on June 26, 2023, defining four reclaimed water quality classes (A, B, C, D) for agricultural irrigation, with approximately 40 billion cubic meters of wastewater treated annually in the EU and only about 1 billion cubic meters reused per European Commission data.

- Veolia Environnement closed a USD 1.75 Billion full acquisition of CDPQ's 30% stake in Water Technologies and Solutions in May 2025, positioning Veolia Water Technologies for a 50% revenue increase by 2030 and approximately EUR 1 billion in PFAS-related treatment under the GreenUp roadmap.

- California Office of Administrative Law approved Direct Potable Reuse regulations under Cal. Code Regs. tit. 22 § 64669 in August 2024, enabling public water systems to begin applying for and receiving DPR permits after October 1, 2024 with 16/10/11 log reduction requirements for enteric viruses, Giardia and Cryptosporidium.

- Singapore Public Utilities Board NEWater currently meets up to 40% of national water demand from four operational plants with combined capacity of approximately 760,000 cubic meters per day, with the Tuas Water Reclamation Plant designed by Jacobs Engineering targeted at 800,000 cubic meters per day as the world's largest membrane bioreactor facility on completion.

- Texas Senate Bill 14 of the 89th Legislature became effective January 1, 2026, requiring water reuse projects to be issued credits against water and wastewater impact fees, supporting state water plan targets for reuse to account for 15% of Texas water supply over the coming decades.

- Illinois House Bill 3046 of the 103rd General Assembly repealed the state ban on water reuse and approved revisions to facilitate industrial water reuse opportunities, joining 28 U.S. states with active water reuse regulatory frameworks tracked by the EPA REUSExplorer database.

Competitive Landscape Overview

The water recycling and reuse market is moderately consolidated, with the top four vendors, including Veolia, Xylem, Ecolab and SUEZ, controlling an estimated 28% combined revenue share in 2025. Competition operates across four axes: technology breadth, geographic footprint, sector specialization and digital capability. Veolia commands a 9.5% share of the broader industrial water treatment market, while Ecolab competes through Nalco Water industrial programs and Xylem leverages the 2023 USD 7.5 billion Evoqua acquisition for U.S. mid-market depth.

Competitive evolution accelerated through 2025 as Veolia closed full ownership of Water Technologies and Solutions in May 2025 and secured over USD 750 million in new contracts during Q1 2025 across energy and semiconductors. Pure-play sustainability players Gradiant Corporation, Aquatech International and Fluence Corporation Limited compete on advanced membrane technologies and decentralized deployment, while DuPont Water Solutions, Pentair plc and Kurita Water Industries Ltd. anchor industrial chemistry and membrane element supply. New mid-market entrants targeting AI data center cooling, including Nalco Water and IDE Technologies, expanded U.S. industrial portfolios through 2025 and early 2026.

Competitive Landscape Matrix

| Company | Headquarters | Position | Key Solution | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| Veolia Environnement | Aubervilliers, France | Leader | Veolia Water Technologies & Solutions | Global (44 countries) | USD 1.75 Billion full acquisition of CDPQ stake in WTS (May 2025) |

| Xylem Inc. | Washington, D.C., US | Leader | Xylem Vue, Evoqua treatment platform | North America, EMEA | USD 7.5 Billion Evoqua acquisition integration; new MBR rollouts (2025) |

| Ecolab Inc. | Saint Paul, Minnesota, US | Leader | Nalco Water industrial water programs | Global | USD 50 Million acquisition of Barclay Water Management (November 2024) |

| SUEZ SA | Paris, France | Leader | SUEZ AquaAdvanced, Aquadvanced Water Networks | Europe, Asia, Middle East | Post-Veolia spinout; smart resource management contracts (2025) |

| DuPont de Nemours | Wilmington, Delaware, US | Challenger | DuPont Water Solutions (FilmTec, IntegraTec) | Global | Sustainability Navigator launched January 2025; BIG Innovation Award |

| Pentair plc | London, UK | Challenger | Pentair Water Treatment, Pelican Water | North America, Europe | Industrial water reuse technology expansion across data centers (2025) |

| Kurita Water Industries | Tokyo, Japan | Challenger | Kurita Dropwise, water and process chemicals | Asia Pacific, North America | Patent leadership in wastewater treatment innovation (2025) |

| Fluence Corporation | White Plains, New York, US | Niche Player | Fluence Aspiral MABR, NIROBOX desalination | Latin America, Europe, MEA | Decentralized membrane bioreactor deployments across emerging markets |

| Gradiant Corporation | Boston, US | Niche Player | Gradiant Counter Flow RO, ClearLogix | North America, Asia, MEA | USD 228 Million in cumulative VC funding; unicorn valuation in 2024 |

| IDE Technologies | Kadima, Israel | Niche Player | IDE Progreen, MaxH2O Desalter | Middle East, North America | Carlsbad expansion and SoftQA rollout for industrial reuse (2025) |

Segmentation Analysis

Water recycling and reuse market segmentation operates across four primary dimensions: equipment type, capacity, end-use and water source. Each axis carries distinct procurement implications for utility planners, industrial water managers and EPC contractors evaluating water recycling and reuse vendors against EPA WRAP 2.0, EU 2020/741 or California Title 22 compliance checklists.

By Equipment

The water recycling and reuse market is led by Tertiary Equipment, which captured approximately 38.0% of total revenue in 2025, equivalent to USD 7.30 Billion. Tertiary equipment includes membrane filtration, reverse osmosis trains, ultraviolet disinfection systems, advanced oxidation processes, activated carbon filters and ion exchange systems used to meet stringent reclaimed water quality classes including California Title 22 and EU 2020/741 Class A. The Changi NEWater Project Phase 2 in Singapore demonstrates tertiary economics at scale, with operational costs between USD 0.08 and USD 0.15 per cubic meter for two-stage microfiltration plus reverse osmosis treatment producing 73.5% recovery.

Secondary Equipment, including activated sludge processes, sequencing batch reactors and membrane bioreactors, represented 35.0% of water recycling and reuse market revenue in 2025, equivalent to USD 6.72 Billion. Primary Equipment, covering screening, grit removal, sedimentation tanks and primary clarifiers, accounted for the remaining 27.0%. Tertiary Equipment is forecast to register the highest CAGR through 2034 as direct potable reuse and industrial ultrapure water demand intensify across California, Florida and Singapore project pipelines.

By Capacity

Capacity above 100,000 liters per day held the largest share of the water recycling and reuse market in 2025 at approximately 41.0%, equivalent to USD 7.87 Billion, supported by municipal wastewater treatment plants and industrial sites such as the U.S. Midwest semiconductor plant served by Veolia at 30 million gallons per day. Large-scale California State Water Resources Control Board grant funding of USD 161.9 million for FY 2025-26 under the Water Recycling Funding Program continues to anchor capacity additions of at least 10,000 acre-feet per year per project phase, with up to USD 15 million per project phase available.

The 50,001-100,000 liters per day capacity bracket captured 28.0% of water recycling and reuse market revenue in 2025 and is forecast to register the highest CAGR through 2034 as decentralized industrial parks, food and beverage processing plants and mid-scale municipal reuse projects scale up. Below 25,000 liters held 16.0% share in 2025, while 25,001-50,000 liters captured 15.0%. Decentralized membrane bioreactor systems from KUBOTA Corporation and Fluence Corporation Aspiral are extending the addressable market across emerging-market urban developments.

By End Use

The Industrial end-use segment commanded approximately 42.0% of water recycling and reuse market revenue in 2025, equivalent to USD 8.06 Billion, anchored by power generation, semiconductors, oil and gas, chemicals, pharmaceuticals, food processing and pulp-and-paper. PepsiCo announced a Net Water Positive 2030 commitment to replenish more water than it consumes, while Coca-Cola, BMW, Pfizer and Adnoc are documented Gradiant Corporation customers. Industrial closed-loop systems are forecast to grow at a 12.9% CAGR through 2034 as PFAS treatment, AI data center cooling and zero-liquid-discharge mandates expand.

Commercial end-use captured 31.0% of water recycling and reuse market revenue in 2025, supported by office buildings, hotels, data centers and large institutional campuses. Residential end-use held 27.0%, including greywater and rainwater modules deployed during construction in water-stressed metros. The Massachusetts Foxborough decentralized reuse system enabling stadium operations and El Paso Water purified reuse are reference points cited in the EPA WRAP 2.0 booklet released April 16, 2026.

By Water Source

Municipal Wastewater represented approximately 58.0% of water recycling and reuse market revenue in 2025, equivalent to USD 11.14 Billion, with utilities and public-private partnerships dominating volume. Singapore NEWater, Orange County Water District in California and the Hampton Roads Sanitation District SWIFT Program in Virginia anchor benchmark deployments. The U.S. EPA Water Infrastructure Finance and Innovation Act program issued a USD 268 million WIFIA loan to Hampton Roads Sanitation District as the third tranche of a USD 1.3 billion agreement supporting drinking water supply for 1.9 million Virginians.

Industrial Wastewater accounted for the remaining 42.0% of water recycling and reuse market revenue in 2025 and is forecast to register the highest growth through 2034. Semiconductor fabs, data centers, refineries, microelectronics manufacturing and hydrogen plants invest in closed-loop recycling to secure supply, meet ESG metrics, and comply with state-level discharge mandates. EPA WRAP 2.0 actions for industrial cooling water and recycled water permits for data centers underscore the regulatory tailwind extending the water recycling and reuse market addressable opportunity.

Regional Analysis

The water recycling and reuse market shows distinct regional dynamics anchored by water stress, regulatory regime maturity and EPC contractor density. Buyers comparing regional opportunities should factor in permitting timelines, public acceptance studies and local membrane element supply.

Asia Pacific

Asia Pacific captured 42.0% of the water recycling and reuse market in 2025, approximately USD 8.06 Billion, with India, China, Japan, Australia and Singapore anchoring regional demand. Singapore NEWater meets up to 40% of national water demand and is forecast to reach 55% by 2060 per Singapore Public Utilities Board projections, while the Tuas Water Reclamation Plant designed by Jacobs Engineering is targeted at 800,000 cubic meters per day. India is forecast to register the fastest national growth in the region at over 10.6% CAGR through 2030, supported by World Bank investments of USD 500 million in reuse infrastructure. China industrial reuse mandates extend across Jiangsu Province at projected minimum unconventional water usage allocations of 14.6 hundred million cubic meters in 2025.

North America

North America held 28.0% of the water recycling and reuse market in 2025, equivalent to approximately USD 5.38 Billion, with the United States contributing the largest country share. EPA WRAP 2.0 launched April 16, 2026 created national policy momentum, while California State Water Resources Control Board direct potable reuse regulations under Title 22 became operational October 1, 2024. Texas Senate Bill 14 effective January 1, 2026 created impact-fee credits for water reuse projects, and Illinois House Bill 3046 repealed the state water reuse prohibition. Veolia, Xylem, Ecolab and Aquatech International anchor regional supply with combined trailing-12-month North American revenue exceeding USD 4.5 Billion.

Europe

Europe held approximately 18.5% of the water recycling and reuse market in 2025, equivalent to USD 3.55 Billion, anchored by Spain, Italy, France, Germany and Cyprus. EU Regulation 2020/741 on minimum requirements for water reuse, applicable since June 26, 2023, governs agricultural irrigation reclaimed water across four quality classes (A, B, C, D), with European Commission Guidelines 2022/C 298/01 supporting member-state implementation. Cyprus reuses more than 90% of its wastewater, Malta exceeds 60%, while Italy, Spain and Greece reuse 5-12% of effluents. Veolia, Suez and Acciona Water lead the Spanish reuse contract pipeline.

Middle East & Africa

Middle East and Africa contributed 7.0% of the water recycling and reuse market in 2025, approximately USD 1.34 Billion, with Saudi Arabia, the United Arab Emirates and Israel leading regional adoption. Saudi Arabia Vision 2030 deployed SR230 billion in completed water projects including over 1,000 dams alongside reclaimed water capacity, while January 2026 tenders covered upgrades to water stations, transmission pipelines and water quality systems nationwide. IDE Technologies, ACCIONA Water and Veolia Middle East dominate regional EPC supply, with Israel reuse rates exceeding 90% of wastewater effluent.

Latin America

Latin America accounted for 4.5% of the water recycling and reuse market in 2025, equivalent to USD 864 Million, led by Brazil, Mexico, Chile and Argentina. Veolia secured three strategic contracts totaling nearly USD 170 million with key energy sector partners in Brazil and the UAE in 2025, implementing membrane technology to remove sulfates from injection water used in offshore oil production. Mexico National Water Commission CONAGUA and Chile Sanitation Agency SISS anchor municipal reuse permits, while Aquatech International and Fluence Corporation supply decentralized industrial systems to mining and food and beverage clients.

Country Analysis

Country-level water recycling and reuse market dynamics diverge sharply based on water stress, regulatory regime and EPC ecosystem. The United States, India, Singapore and Saudi Arabia represent the four most consequential national markets through 2034.

United States

The United States water recycling and reuse market was valued at approximately USD 4.30 Billion in 2025 and is forecast to grow at a 9.6% CAGR through 2034, reaching roughly USD 9.85 Billion. EPA Water Reuse Action Plan 2.0 launched April 16, 2026 anchored federal momentum across AI data center cooling, industrial process water and energy sector reuse, while California Title 22 direct potable reuse permits became available October 1, 2024. Texas Senate Bill 14 effective January 1, 2026, Illinois House Bill 3046 water reuse prohibition repeal, and Florida Environmental Regulation Commission potable reuse rules approved December 13, 2024 expanded state-level addressable demand. The H.R. 2940 Advancing Water Reuse Act proposes a federal industrial water reuse tax credit. Veolia, Xylem, Ecolab, Aquatech and Gradiant anchor U.S. supply.

India

India water recycling and reuse market revenue reached approximately USD 1.95 Billion in 2025, projected to expand at a 10.6% CAGR through 2034 driven by Smart Cities Mission projects and SEBI BRSR Core water disclosure mandates. World Bank investment of USD 500 million in India's reuse infrastructure supports municipal reclamation expansion across Maharashtra, Karnataka, Tamil Nadu and Gujarat. The June 2025 Carbon Credit Trading Scheme operationalization by India's Ministry of Power adds compliance-driven demand. Va Tech Wabag Ltd. is the dominant domestic engineering procurement and construction contractor, while Veolia India, Triveni Engineering, Thermax Limited and Hitachi anchor multi-technology supply.

Singapore

Singapore water recycling and reuse market revenue reached approximately USD 480 Million in 2025, projected to expand at a 9.5% CAGR through 2034 driven by Tuas Water Reclamation Plant scale-up and PUB Deep Tunnel Sewerage System Phase 2 construction. NEWater currently meets up to 40% of national water demand from four operational plants delivering approximately 760,000 cubic meters per day, and is forecast to reach 55% by 2060. The Bedok NEWater Factory and Visitor Centre closed July 31, 2024, with capacity consolidated at Kranji, Ulu Pandan and Changi. Keppel Seghers and Sembcorp Industries operate the Ulu Pandan and Changi plants under design-build-own-operate concessions. Mandatory water recycling requirements apply to new projects in water-intensive non-domestic sectors per the World Bank March 2025 update.

Saudi Arabia

Saudi Arabia water recycling and reuse market revenue reached approximately USD 510 Million in 2025, projected to expand at a 11.2% CAGR through 2034 driven by Vision 2030 water targets. The Saudi government deployed SR230 billion in completed water projects including more than 1,000 dams under public-private partnership models, while January 2026 tenders covered nationwide upgrades to water stations, transmission pipelines and water quality systems. Saudi Water Authority and Saline Water Conversion Corporation anchor public procurement, with ACCIONA Water, Veolia, IDE Technologies and Saudi Industrial Investment Group serving the EPC pipeline. Saudi Arabia targets a 50% reuse rate of treated wastewater under the National Water Strategy 2030.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Equipment

- Filtration Systems

- Microfiltration (MF) Systems

- Ultrafiltration (UF) Systems

- Nanofiltration (NF) Systems

- Reverse Osmosis (RO) Systems

- Membrane Bioreactors (MBR)

- Activated Carbon Filtration Systems

- Disinfection Systems

- Ultraviolet (UV) Disinfection Systems

- Ozonation Systems

- Chlorination Systems

- Biological Treatment Systems

- Sludge Treatment Equipment

- Pumps and Conveyance Systems

- Monitoring and Control Systems

- Evaporation and Crystallization Systems

- Others

By Capacity

- Less than 25,000 m³/day

- 25,000–50,000 m³/day

- 50,001–100,000 m³/day

- 100,001–250,000 m³/day

- More than 250,000 m³/day

By End Use

- Municipal

- Industrial

- Food and Beverage

- Oil and Gas

- Power Generation

- Chemicals and Petrochemicals

- Pharmaceuticals

- Pulp and Paper

- Textile

- Mining and Metals

- Semiconductor and Electronics

- Others

- Commercial

- Agricultural Irrigation

- Residential

- Environmental and Recreational Applications

By Water Source

- Municipal Wastewater

- Industrial Wastewater

- Stormwater Runoff

- Greywater

- Blackwater

- Desalination Plant Effluent

- Agricultural Wastewater

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 19.20 B |

| Forecast Revenue (2034) | USD 45.50 B |

| CAGR (2025-2034) | 10.1% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Equipment, (Filtration Systems, Membrane Bioreactors (MBR), Activated Carbon Filtration Systems, Disinfection Systems, Biological Treatment Systems, Sludge Treatment Equipment, Pumps and Conveyance Systems, Monitoring and Control Systems, Evaporation and Crystallization Systems, Others), By Capacity, (Less than 25,000 m³/day, 25,000–50,000 m³/day, 50,001–100,000 m³/day, 100,001–250,000 m³/day, More than 250,000 m³/day), By End Use, (Municipal, Industrial, Commercial, Agricultural Irrigation, Residential, Environmental and Recreational Applications), By Water Source, (Municipal Wastewater, Industrial Wastewater, Stormwater Runoff, Greywater, Blackwater, Desalination Plant Effluent, Agricultural Wastewater, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | VEOLIA ENVIRONNEMENT, XYLEM INC., ECOLAB INC., SUEZ SA, DUPONT DE NEMOURS, INC., PENTAIR PLC, KURITA WATER INDUSTRIES LTD., FLUENCE CORPORATION LIMITED, GRADIANT CORPORATION, IDE TECHNOLOGIES, AQUATECH INTERNATIONAL LLC, ALFA LAVAL AB, HITACHI, LTD., KUBOTA CORPORATION, SIEMENS AG, BLACK & VEATCH, ACCIONA AGUA, THERMAX LIMITED, VA TECH WABAG LTD., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, Membrane Bioreactors, Sludge Treatment Equipment), By Capacity (Less than 25,000 m³/day, 25,000–50,000 m³/day, 50,001–100,000 m³/day, 100,001–250,000 m³/day and Above 250,000 m³/day), By End Use (Municipal, Industrial, Commercial, Agricultural Irrigation and Residential), By Water Source (Municipal Wastewater, Industrial Wastewater, Greywater, Blackwater and Stormwater Runoff) Industry Region & Key Players – Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

, Membrane Bioreactors, Sludge Treatment Equipment), By Capacity (Less than 25,000 m³/day, 25,000–50,000 m³/day, 50,001–100,000 m³/day, 100,001–250,000 m³/day and Above 250,000 m³/day), By End Use (Municipal, Industrial, Commercial, Agricultural Irrigation and Residential), By Water Source (Municipal Wastewater, Industrial Wastewater, Greywater, Blackwater and Stormwater Runoff) Industry Region & Key Players – Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

, Membrane Bioreactors, Sludge Treatment Equipment), By Capacity (Less than 25,000 m³/day, 25,000–50,000 m³/day, 50,001–100,000 m³/day, 100,001–250,000 m³/day and Above 250,000 m³/day), By End Use (Municipal, Industrial, Commercial, Agricultural Irrigation and Residential), By Water Source (Municipal Wastewater, Industrial Wastewater, Greywater, Blackwater and Stormwater Runoff) Industry Region & Key Players – Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Water Recycling and Reuse Market?

The Global Water Recycling and Reuse Market was valued at USD 17.44 Billion in 2024 and USD 19.20 Billion in 2025, and is projected to reach USD 45.50 Billion by 2034, growing at a CAGR of 10.1% from 2026 to 2034. Market growth is driven by increasing water scarcity, stringent wastewater regulations, and rising investments in sustainable water management solutions.

Who are the major players in the Water Recycling and Reuse Market?

VEOLIA ENVIRONNEMENT, XYLEM INC., ECOLAB INC., SUEZ SA, DUPONT DE NEMOURS, INC., PENTAIR PLC, KURITA WATER INDUSTRIES LTD., FLUENCE CORPORATION LIMITED, GRADIANT CORPORATION, IDE TECHNOLOGIES, AQUATECH INTERNATIONAL LLC, ALFA LAVAL AB, HITACHI, LTD., KUBOTA CORPORATION, SIEMENS AG, BLACK & VEATCH, ACCIONA AGUA, THERMAX LIMITED, VA TECH WABAG LTD., Others

Which segments covered the Water Recycling and Reuse Market?

By Equipment, (Filtration Systems, Membrane Bioreactors (MBR), Activated Carbon Filtration Systems, Disinfection Systems, Biological Treatment Systems, Sludge Treatment Equipment, Pumps and Conveyance Systems, Monitoring and Control Systems, Evaporation and Crystallization Systems, Others), By Capacity, (Less than 25,000 m³/day, 25,000–50,000 m³/day, 50,001–100,000 m³/day, 100,001–250,000 m³/day, More than 250,000 m³/day), By End Use, (Municipal, Industrial, Commercial, Agricultural Irrigation, Residential, Environmental and Recreational Applications), By Water Source, (Municipal Wastewater, Industrial Wastewater, Stormwater Runoff, Greywater, Blackwater, Desalination Plant Effluent, Agricultural Wastewater, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Water Recycling and Reuse Market

Published Date : 12 Jun 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date