- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Wearable Air Purifier Market Size, Share & Forecast | CAGR 13.0%

Global Wearable Air Purifier Market Size, Share, Analysis By Product Type (Neck-Worn Wearable Air Purifiers, Clip-On Wearable Air Purifiers, Mask-Integrated Air Purifiers, Pendant & Lanyard Air Purifiers, Wrist-Worn and Other Wearable Air Purifiers), By Technology (Negative Ion Generation, HEPA Filtration, Electrostatic Filtration, Activated Carbon Filtration, UV-C Sterilization, Hybrid Air Purification Systems), By Distribution Channel (Online Retail & E-Commerce, Brand-Owned Stores, Consumer Electronics Retailers, Pharmacies & Healthcare Stores, Specialty Retail Stores), By End-User Application and Battery Type Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

|---|---|---|---|

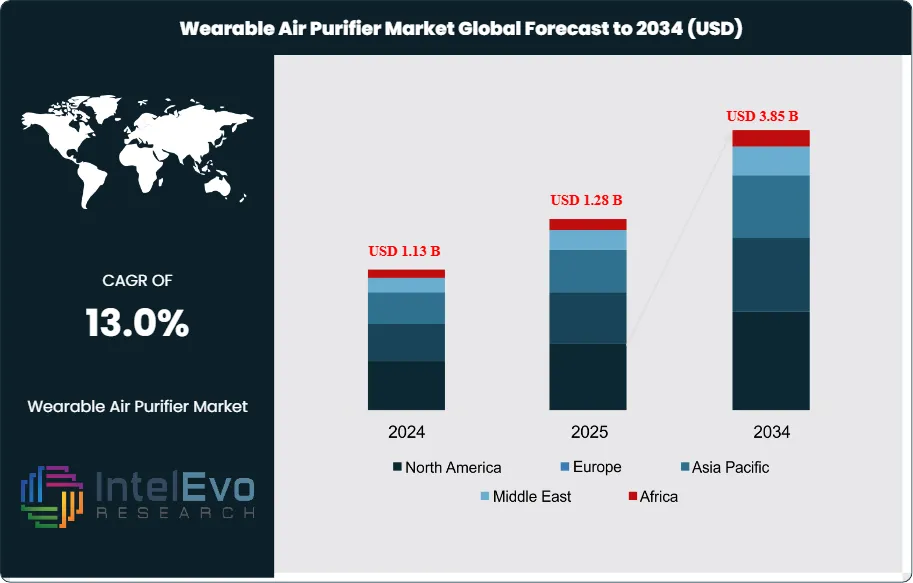

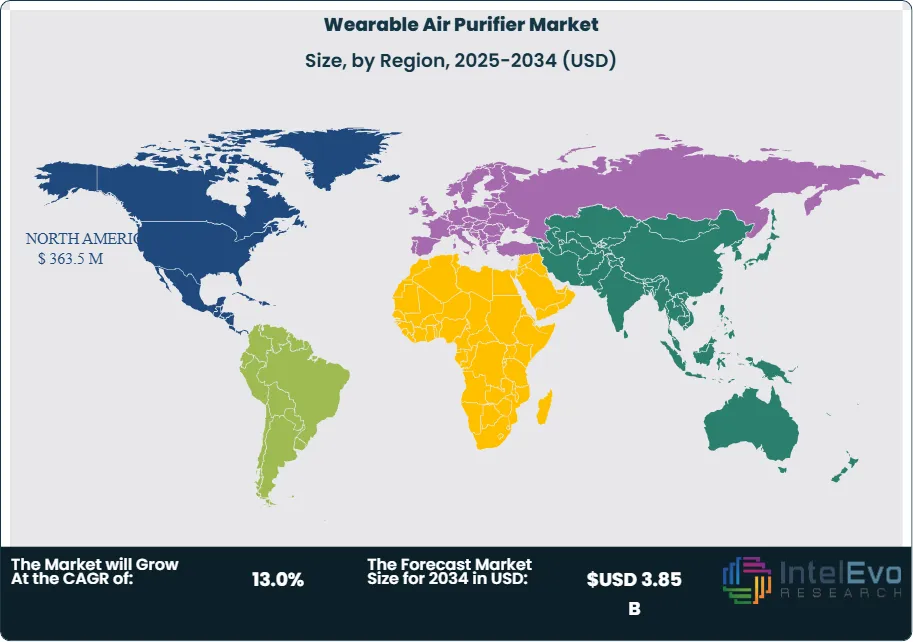

| USD 1.28 Billion | USD 3.85 Billion | 13.0% | Asia Pacific, 39.5% |

The Wearable Air Purifier Market was valued at approximately USD 1.13 Billion in 2024 and reached USD 1.28 Billion in 2025. The market is projected to grow to USD 3.85 Billion by 2034, expanding at a CAGR of 13.0% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 2.57 Billion over the analysis period. The market growth is driven by rising concerns regarding air pollution, airborne pathogens, allergens, and respiratory health across urban environments. Increasing consumer awareness about personal air quality protection, coupled with growing adoption of portable and wearable health technologies, is fueling demand for wearable air purification devices worldwide.

Get More Information about this report -

Request Free Sample ReportGrowth in the wearable air purifier market is anchored in three structural drivers. First, chronic outdoor air-pollution exposure across Asia Pacific and parts of Europe remains elevated, with India's 2025 average PM2.5 concentration reaching 48.9 micrograms per cubic metre, approximately 9.78 times the World Health Organization annual guideline of 5 micrograms per cubic metre, according to the IQAir 2025 World Air Quality Report. Second, wildfire smoke events across North America and the Mediterranean are driving episodic demand for personal protection against PM2.5 particles, which penetrate deep into the lungs and can enter the bloodstream, the Environmental Protection Agency and Centers for Disease Control and Prevention confirm. Third, allergen-driven indoor use is expanding, with the Respiray Wear A+ demonstrating 48% to 60% reductions in total symptom scores for birch pollen, house dust mite, and cat allergen exposure in a standardized allergen exposure chamber study published in 2024.

The regulatory environment for wearable air purifiers is consolidating around three frameworks. The US Food and Drug Administration regulates medical-grade respirators under 21 CFR 878.4040 and the Centers for Disease Control and Prevention's National Institute for Occupational Safety and Health certifies N95 and N99 respirators under 42 CFR Part 84. The European Union classifies FFP2 and FFP3 respirators under Regulation (EU) 2016/425 on personal protective equipment. China applies the GB2626-2019 KN95 standard, and the Korean Food and Drug Administration regulates KF94 certification.

Demand is structurally broadening across powered mask, neck-hung necklace, and hybrid audio-visor form factors. LG Electronics' PuriCare Wearable Air Purifier with dual H13 HEPA filters, the Airvida M1 ionic wearable generating 2 million negative ions per cubic centimetre, and AirTamer A310 electrostatic necklace with 50-hour runtime define the volume-tier competitive set. Higher-end entrants including Respiray Wear A+ at approximately 250 grams and the discontinued Dyson Zone define the engineered-premium tier. China, India, and South Korea account for the largest user concentrations because of chronic urban air-pollution exposure, while North America and Europe anchor the premium-priced segment.

Asia Pacific held the largest wearable air purifier market share at 39.5% in 2025, anchored by LG Electronics in Seoul, Airvida in Taiwan, Xiaomi Corporation, and a large installed user base across China and India. North America represented the second-largest region at 28.4%, with AirTamer, Wein Products, Flo Mask, and a heavy wildfire-driven replenishment cycle. The technology roadmap through 2034 tilts toward lighter H13 HEPA modules, longer-duration electrostatic cells, app-connected dose tracking through platforms such as IQAir's AirVisual app, and clinical-grade allergen validation extending from Respiray's laboratory trials.

Market Definition & Scope

The wearable air purifier market is defined as the global commercial activity in body-worn personal air purification devices that actively filter, ionize, or electrostatically treat the air a user breathes. The market encompasses powered mask-style purifiers such as LG PuriCare, neck-hung ionic necklaces such as Airvida M1 and AirTamer A310, HEPA collar purifiers such as Respiray Wear A+, and hybrid audio-visor devices such as the now-discontinued Dyson Zone. Filtration technologies covered include H13 HEPA, activated carbon, electrostatic ionization, and UV-C sanitization.

Included in the scope are hardware revenues, replacement HEPA and activated carbon filter revenues, UV sanitization accessories, and associated app-based dose tracking services tied to wearable air purifiers. Explicitly excluded are room air purifiers such as the Dyson HushJet Purifier Compact and LG PuriCare 360, passive cloth or disposable N95 masks without active filtration, HVAC-grade filters, and industrial respirators for occupational use only. The wearable air purifier market is a subset of the USD 17.96 Billion global air purifier market and sits adjacent to the USD 479 Million wearable air purifier mask sub-category for 2025.

, By Technology (Negative Ion Generation, HEPA Filtration, Electrostatic Filtration, Activated Carbon Filtration, UV-C Sterilization, Hybrid Air Purification Systems), By Distribution Channel (Online Retail & E-Commerce, Brand-Owned Stores, Consumer Electronics Retailers, Pharmacies & Healthcare Stores, Specialty Retail Stores), By End-User Application and Battery Type Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The wearable air purifier market expands from USD 1.28 Billion in 2025 to USD 3.85 Billion by 2034, a CAGR of 13.0% over the forecast period.

- Segment Dominance by Product Type: Powered air purifier masks led in 2025 with 38.6% share, driven by LG PuriCare Wearable and follow-on FFP2-equivalent active filtration devices.

- Segment Dominance by Technology: H13 HEPA filtration accounted for 52.8% of 2025 revenue, reflecting its 99.97% particle-capture specification at 0.3 microns across LG, Respiray, and Flo Mask products.

- Driver: India's average PM2.5 concentration reached 48.9 micrograms per cubic metre in 2025, approximately 9.78 times the WHO annual guideline, per the IQAir 2025 World Air Quality Report.

- Restraint: Dyson's mid-2025 discontinuation of the Dyson Zone signalled a design-led challenge for mask-visor hybrids and constrained the premium-tier shelf in North America and Europe.

- Opportunity: Allergen-specific wearable HEPA demand represents a USD 410 Million 2034 opportunity, underpinned by Respiray Wear A+ clinical data showing 48%-60% symptom reductions.

- Trend: App-connected air-quality dose tracking expanded through 2025, with IQAir's AirVisual app covering 10,000+ global monitoring points and Bluetooth-enabled wearable purifier pairing.

- Regional: Asia Pacific led the wearable air purifier market with 39.5% share and USD 505.6 Million in revenue in 2025, followed by North America at 28.4%.

Key Insights Summary

- Dyson launched the HushJet Purifier Compact on September 30, 2025, at USD 349.99 SRP on Dyson.com, Dyson Demo Stores, and select third-party retailers, following Dyson's mid-2025 discontinuation of the Dyson Zone wearable air-purifying headphones confirmed by Wired reporting and Stuff magazine coverage.

- India's average PM2.5 concentration reached 48.9 micrograms per cubic metre in 2025, approximately 9.78 times the WHO annual guideline of 5 micrograms per cubic metre, placing India sixth globally in the IQAir 2025 World Air Quality Report and underwriting sustained wearable air purifier demand.

- The LG PuriCare Wearable Air Purifier uses dual H13 HEPA filters with 99.97% particle capture efficiency at 0.3 microns, weighs 126 grams, and runs 4 to 8 hours on its 820 milliamp-hour to 1,000 milliamp-hour battery, with the Gen 2 AP551AWFA adding Bluetooth, the companion app, and VoiceON amplification technology.

- The Respiray Wear A+ clinical allergen-exposure-chamber study, published in 2024 in the Respiratory Research literature, demonstrated statistically significant total symptom score reductions of approximately 49% for birch pollen, 48% for house dust mite, and 60% for cat allergen exposure across 101 allergic patients in a standardized allergen chamber.

- Airvida M1 and L1 ionic wearable air purifiers generate 20 million negative ions per cubic centimetre, approximately 100 times the ion concentration measured in natural forests, and the Airvida range holds CES 2020 and CES 2023 Innovation Awards plus the 2022 German Innovation Award for Medical and Health.

- AirTamer A310 electrostatic necklace air purifiers deliver 50-hour runtimes on a single charge through a USB cable and create a claimed three-foot sphere of cleaner air around the wearer's head, with ion emitters rated at 9x the cleaning power of comparable 2024 predecessors in manufacturer-published tests.

- Respiray launched the Wear A+ Activated Carbon model in 2025, described as the world's first wearable activated-carbon air purifier, combining H12 HEPA with activated carbon for 97.6% allergen capture plus volatile organic compound and fragrance protection, a category-first against pre-2025 HEPA-only wearables.

Competitive Landscape Overview

The wearable air purifier market is moderately fragmented, with consumer electronics majors, specialized wearable-air brands, and pollution-mask incumbents competing across distinct product form factors. The top four companies, LG Electronics, Dyson, ible Technology (Airvida), and FilterStream (AirTamer), accounted for an estimated 38.6% of combined 2025 revenue, based on public disclosures and retail sell-through estimates. Competition is product-type and technology led, because a KN95-FFP2 active mask, an ionic necklace, and a HEPA collar address different buyer intents on any wearable air purifier procurement checklist.

Competitive dynamics shifted in 2025 as Dyson discontinued the Dyson Zone mid-year and pivoted to the HushJet Purifier Compact for room-scale purification launched September 30, 2025. Respiray extended the HEPA-plus-activated-carbon category with Wear A+ Activated Carbon during 2025, and IQAir strengthened pollution-mask distribution through India-market medical-grade mask bundles paired with air-purifier orders. Consolidation and retreat in mask-visor hybrids redirects shelf space toward neck-hung ionic devices, which the AirTamer A310, AirTamer A320, Airvida M1, and Airvida L1 dominate by volume across online retail channels including Amazon and specialty stores.

Competitive Landscape Matrix:

| Company | Headquarters | Position | Key Product | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| LG Electronics Inc. | South Korea | Leader | PuriCare Wearable Air Purifier AP300AWFA; Gen 2 AP551AWFA with VoiceON | Asia Pacific, Middle East | Scaled Gen 2 PuriCare Wearable distribution with UV-C sanitizing case through 2025 |

| Dyson Ltd. | United Kingdom | Leader | Dyson Zone (legacy); HushJet Purifier Compact | North America, Europe | Discontinued Dyson Zone in mid-2025; launched HushJet Purifier Compact on September 30, 2025 |

| ible Technology Inc. (Airvida) | Taiwan | Leader | Airvida L1; Airvida M1; Airvida C1 | Asia Pacific, North America | Expanded M1 titanium-necklace and C1 kids ranges; holds CES 2020 and 2023 Innovation Awards |

| FilterStream, LLC (AirTamer) | United States | Leader | AirTamer A310; A315; A320 electrostatic purifiers | North America, Europe | Maintained A310 and A320 flagships with silent electrostatic ion emission through 2025 |

| Respiray OU | Estonia | Challenger | Respiray Wear A+; Wear A+ Activated Carbon | Europe, North America | Launched world's first wearable activated carbon air purifier for VOC protection in 2025 |

| Xiaomi Corporation | China | Challenger | Xiaomi AirPop Active; AirMotion wearable accessories | Asia Pacific | Expanded mask accessory ecosystem via AirPop partnership through 2024-2025 |

| Koninklijke Philips N.V. | Netherlands | Challenger | Philips Fresh Air Mask; commercial respirators | Asia Pacific, Europe | Sustained Asia Pacific presence for pollution mask ranges through 2025 |

| IQAir (IQAir North America, Inc.) | Switzerland | Niche Player | IQAir FFP2 Mask; AirVisual app | North America, Europe, Asia | Released 2025 World Air Quality Report confirming India ranked 6th most polluted country |

| Wein Products, Inc. | United States | Niche Player | Wein AS Personal Ionic Air Purifier | North America | Maintained personal ionic air purifier product line through 2025 |

| Flo Mask (Flo Mask, Inc.) | United States | Niche Player | Flo Mask Pro; Flo Mask Kids | North America | Sustained premium reusable PM2.5 and wildfire mask sales through 2025 fire seasons |

Segmentation Analysis

The wearable air purifier market segments by product type, technology, distribution channel, end-user application, and battery type. Each segmentation type maps to distinct buying criteria on a wearable air purifier procurement checklist, including filtration efficiency at 0.3 microns, battery runtime, certification under KN95, FFP2, or N95 standards, and app connectivity.

By Product Type

Powered air purifier masks led the wearable air purifier market at 38.6% share in 2025, approximately USD 494 Million, with LG PuriCare Wearable Air Purifier AP300AWFA and Gen 2 AP551AWFA anchoring the category. The sub-segment benefits from concrete medical-equivalent positioning, because dual H13 HEPA filters match specifications used in LG's room PuriCare family, while VoiceON technology amplifies user speech through an integrated speaker to overcome the social friction that limited earlier pollution masks. Flo Mask, IQAir FFP2 Mask, and Cambridge Masks occupy the premium end of the powered and reusable mask sub-segment.

Neck-hung necklace-style wearable air purifiers held 34.4% of 2025 revenue, approximately USD 440 Million, led by Airvida L1, Airvida M1, AirTamer A310, and AirTamer A320. These devices use fanless ionic or electrostatic designs operating at near-zero decibels and up to 50 to 120 hours of runtime per charge, positioning them against active-fan masks for long-wear use in offices, cars, and public transport. Headphone and visor hybrids, including the now-discontinued Dyson Zone and older AirPop ranges, held 11.8% in 2025, approximately USD 151 Million. Clip-on and compact portable models held 15.2%, covering travel-oriented devices marketed on Amazon and specialty sites.

By Technology

H13 HEPA filtration led the wearable air purifier market at 52.8% share in 2025, approximately USD 676 Million, because its 99.97% particle-capture efficiency at 0.3 microns matches the NIOSH N95 and EU FFP2 performance floor. Leading H13 HEPA wearable air purifier products include LG PuriCare with dual H13 filters, Respiray Wear A+ with H12 HEPA, and the IQAir FFP2 Mask meeting KN95 GB2626-2019 and FFP2 Regulation (EU) 2016/425 standards.

Air ionization and electrostatic technologies held 31.2% in 2025, approximately USD 399 Million, including Airvida ionic wearables and AirTamer electrostatic purifiers. Activated carbon solutions held 9.6%, including Respiray Wear A+ Activated Carbon launched in 2025 as the category's first activated-carbon wearable. UV and photocatalytic technologies held 6.4%, including UV-C sanitizing cases such as LG's optional charging case that kills 99.9% of bacteria and germs per LG's published lab data. Comparative evaluation shows H13 HEPA wearables are preferred for wildfire smoke and pollution-heavy urban environments, while ionic and electrostatic devices serve office and indoor-allergen applications with near-silent operation.

By Distribution Channel

Online retail led the wearable air purifier market at 58.3% in 2025, approximately USD 746 Million, with Amazon, Best Buy, Dyson.com, LG.com, AirTamer.com, Airvida.co, and Respiray.com as the principal sales channels. Specialty stores held 21.5%, approximately USD 275 Million, including allergy-focused retailers and regional electronics chains. Supermarkets and hypermarkets held 12.8%, concentrated in Asia Pacific markets where wearable air purifiers appear next to consumer electronics and health accessories. Other channels held 7.4%, including pharmacy distribution for medical-grade devices and corporate procurement for enterprise wellness programs.

By End-User Application

Personal consumer use held the largest wearable air purifier end-user share at 62.4% in 2025, approximately USD 799 Million, spanning commuting, urban walking, sports, and general pollution protection. Healthcare and allergy-specific use held 18.6%, approximately USD 238 Million, validated by Respiray's clinical allergen-exposure-chamber studies covering 101 birch pollen, house dust mite, and cat-allergic participants in 2024. Travel and commuter use held 10.5%, with airport duty-free and e-commerce channels as primary acquisition routes.

Occupational and construction use held 5.6% in 2025, focused on dust and particle protection on job sites. Sports and outdoor use held 2.9%, including cycling, running, and urban running in high-pollution zones across Delhi, Beijing, Jakarta, and Los Angeles during wildfire events. The wearable air purifier ROI calculation for allergy sufferers, based on Respiray's trial data, compares annual device and replacement-filter costs to pharmaceutical costs for antihistamines and intranasal steroids, typically producing payback inside 14 to 18 months for regular allergy patients.

By Battery Type

Rechargeable battery-powered wearable air purifiers held 87.2% of the 2025 market, approximately USD 1.116 Billion, because lithium-ion cells deliver the 4 to 50 hours of runtime buyers expect across LG PuriCare, Airvida, AirTamer, and Respiray products. Charging-type and continuously-wired devices held 12.8%, approximately USD 164 Million, concentrated in industrial and occupational categories. The fastest-growing sub-segment is Bluetooth and app-connected rechargeable wearable air purifiers, which the LG PuriCare Gen 2 AP551AWFA pioneered for consumer use, enabling airflow adjustment, filter-duration tracking, and real-time battery data.

Regional Analysis

The wearable air purifier market is geographically led by Asia Pacific, North America, and Europe, together accounting for 90.2% of 2025 revenue. Regional dynamics differ sharply, with Asia Pacific leading on installed user base, North America leading on premium-tier sales, and Europe leading on clinical validation and regulatory rigour.

North America

North America held 28.4% of the wearable air purifier market in 2025, approximately USD 363.5 Million. The United States dominates through AirTamer based in Pennsylvania, Flo Mask, Wein Products, and US distribution of LG PuriCare, Airvida, and Respiray. Canadian demand is driven by wildfire smoke events from 2023 through 2025, when the US Environmental Protection Agency AirNow system reported widespread elevated PM2.5 episodes across Ontario, Quebec, and adjacent US states. Mexico is an emerging buyer, concentrated around Mexico City and Monterrey air-quality episodes. FDA 21 CFR 878.4040 and NIOSH 42 CFR Part 84 respirator certifications define North American wearable air purifier compliance requirements.

Europe

Europe accounted for 22.3% of the wearable air purifier market in 2025, approximately USD 285.4 Million. The United Kingdom leads through Dyson's R&D presence in Malmesbury and Cambridge Masks in Cambridge, Estonia leads on Respiray's innovation from Tallinn with clinical trials conducted in Germany, Germany and France anchor premium consumer demand, and the Netherlands hosts Philips' global HQ. The EU's personal protective equipment Regulation (EU) 2016/425 governs FFP2 and FFP3 respirator certification, and the EU Medical Device Regulation 2017/745 applies when devices make clinical claims. European Union air-quality targets under the 2024 Ambient Air Quality Directive revision set tighter PM2.5 limits through 2030, supporting structural demand.

Asia Pacific

Asia Pacific held 39.5% of the wearable air purifier market in 2025, approximately USD 505.6 Million, the leading region by both volume and value. South Korea anchors the premium supplier base through LG Electronics. China hosts Xiaomi Corporation, a large OEM manufacturing footprint, and the domestic GB2626-2019 KN95 regulatory standard. India hosts IQAir India, Nirvana Being, and strong Airvida and AirTamer demand, with the country's 2025 average PM2.5 concentration of 48.9 micrograms per cubic metre per IQAir. Taiwan hosts ible Technology (Airvida), which developed its ionic wearable air purifier platform from 2015 and has since won CES 2020 and CES 2023 Innovation Awards. Japan contributes through Panasonic's nanoe-X technology adjacent research and premium consumer demand.

Latin America

Latin America held 5.8% of the wearable air purifier market in 2025, approximately USD 74.2 Million. Brazil leads on volume through Sao Paulo and Rio de Janeiro consumer adoption, followed by Mexico and Argentina. Regional price benchmarks for wearable air purifiers sit roughly 25% to 35% below North American pricing because of currency dynamics and import duties. Brazil's Agência Nacional de Vigilância Sanitária (ANVISA) regulates respirator-class certifications, and Mexico's COFEPRIS oversees medical-device claims attached to wearable air purifiers.

Middle East & Africa

Middle East & Africa accounted for 4.0% of the wearable air purifier market in 2025, approximately USD 51.2 Million. The United Arab Emirates and Saudi Arabia lead regional adoption, driven by recurring dust-storm events and urban construction-related particulate exposure. Egypt contributes through Cairo air-quality demand, and South Africa leads sub-Saharan adoption through wildfire-related demand and mining-industry occupational applications. Emirates Authority for Standardization and Metrology (ESMA) and the Saudi Food and Drug Authority align wearable air purifier standards with EU FFP2 and US NIOSH N95 certifications.

Country Analysis

Four national wearable air purifier markets, the United States, China, India, and South Korea, collectively accounted for approximately 56.8% of 2025 revenue. These countries concentrate vendor headquarters, regulatory frameworks, and the air-quality episode patterns that drive the wearable air purifier replacement cycle.

United States

The United States represented approximately USD 329 Million in 2025 wearable air purifier revenue, with a country CAGR estimated at 12.6% through 2034. Federal activity concentrated around the Environmental Protection Agency's AirNow wildfire smoke advisories issued regularly through 2024 and 2025 fire seasons, and the CDC-NIOSH respirator approval program under 42 CFR Part 84. The FDA's premarket clearance pathways govern wearable air purifiers making medical claims, distinct from OSHA-regulated occupational respirators. US wildfire-driven demand spiked during the 2023 Canadian smoke event that blanketed New York, Chicago, and Washington DC. California Proposition 65 warnings require ozone-emission disclosure on ionic wearable air purifiers, and state wildfire-preparedness programs fund personal protective-equipment purchases across Oregon, Washington, and California.

China

China represented approximately USD 212 Million in 2025 wearable air purifier revenue, with a country CAGR estimated at 13.8% through 2034. Xiaomi Corporation and local OEMs dominate the domestic volume-tier, while LG PuriCare, Airvida, and Philips compete in the premium tier through Tmall and JD.com channels. China's GB2626-2019 KN95 standard is the national benchmark for particulate respirators, and the Ministry of Ecology and Environment operates the country's air-quality monitoring network. Beijing, Shijiazhuang, and Chengdu remain among the most PM2.5-exposed cities globally per IQAir 2025 data, sustaining structural urban demand for wearable air purifiers.

India

India represented approximately USD 146 Million in 2025 wearable air purifier revenue, with a country CAGR estimated at 14.2% through 2034, the fastest among the four profiled countries. Delhi and Kolkata ranked among the most-polluted cities globally per IQAir readings in April 2026, and India's 2025 average PM2.5 concentration of 48.9 micrograms per cubic metre was 9.78 times the WHO annual guideline. Domestic brand Nirvana Being, IQAir India, and Smart Air operate the local pollution-mask channel. The Bureau of Indian Standards and the Central Pollution Control Board govern respirator-performance standards, and the Ministry of Health and Family Welfare's 2019 National Clean Air Programme funds air-quality improvement targets. Household emissions contribute approximately 30% to 50% of ambient PM2.5 levels in India year-round per IQAir's 2025 analysis.

South Korea

South Korea represented approximately USD 40 Million in 2025 wearable air purifier revenue, with a country CAGR estimated at 11.8% through 2034. LG Electronics' Seoul headquarters anchors national supplier leadership, with PuriCare Wearable manufacturing concentrated in domestic facilities. Samsung Electronics holds an adjacent research position through its consumer electronics and health-device programs. The Korean Food and Drug Administration regulates KF94 and KF80 respirator certifications, and the Ministry of Environment's air-quality alerts under the 2019 Special Act on Reduction and Management of Fine Dust set wearable-purifier usage recommendations on high-pollution days. Seoul's recurrent yellow-dust episodes originating from the Gobi desert sustain structural demand.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Product Type

- Neck-Worn Wearable Air Purifiers

- Clip-On Wearable Air Purifiers

- Mask-Integrated Air Purifiers

- Pendant and Lanyard Air Purifiers

- Wrist-Worn and Other Wearable Air Purifiers

By Technology

- Negative Ion Generation Technology

- HEPA Filtration Technology

- Electrostatic Filtration Technology

- Activated Carbon Filtration Technology

- UV-C Sterilization Technology

- Hybrid Air Purification Systems

By Distribution Channel

- Online Retail & E-Commerce Platforms

- Brand-Owned Stores

- Consumer Electronics Retailers

- Pharmacies & Healthcare Stores

- Specialty Retail Stores

By End-User Application

- Personal Daily Use

- Healthcare & Medical Use

- Industrial & Occupational Safety

- Travel & Transportation

- Sports & Outdoor Activities

By Battery Type

- Rechargeable Lithium-Ion Batteries

- Rechargeable Lithium-Polymer Batteries

- Replaceable Batteries

- Hybrid Power Systems

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 1.28 B |

| Forecast Revenue (2034) | USD 3.85 B |

| CAGR (2025-2034) | 13.0% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product Type, (Neck-Worn Wearable Air Purifiers, Clip-On Wearable Air Purifiers, Mask-Integrated Air Purifiers, Pendant and Lanyard Air Purifiers, Wrist-Worn and Other Wearable Air Purifiers), By Technology, (Negative Ion Generation Technology, HEPA Filtration Technology, Electrostatic Filtration Technology, Activated Carbon Filtration Technology, UV-C Sterilization Technology, Hybrid Air Purification Systems), By Distribution Channel, (Online Retail & E-Commerce Platforms, Brand-Owned Stores, Consumer Electronics Retailers, Pharmacies & Healthcare Stores, Specialty Retail Stores), By End-User Application, (Personal Daily Use, Healthcare & Medical Use, Industrial & Occupational Safety, Travel & Transportation, Sports & Outdoor Activities), By Battery Type, (Rechargeable Lithium-Ion Batteries, Rechargeable Lithium-Polymer Batteries, Replaceable Batteries, Hybrid Power Systems) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | LG ELECTRONICS INC., DYSON LTD., IBLE TECHNOLOGY INC. (AIRVIDA), FILTERSTREAM, LLC (AIRTAMER), RESPIRAY OU, XIAOMI CORPORATION, KONINKLIJKE PHILIPS N.V., IQAIR (IQAIR NORTH AMERICA, INC.), WEIN PRODUCTS, INC., FLO MASK, INC., AIRPOP (FRESH AIR INVESTMENT HOLDING CORP.), CAMBRIDGE MASKS CO., WINIX INC., 3M COMPANY, HONEYWELL INTERNATIONAL INC., O2 CANADA, NIRVANA BEING (BREATHE EASY LABS PRIVATE LIMITED), PURE ENRICHMENT (VISION INNOVATIONS, INC.), AIRTOMO, AIRDINBOR, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Technology (Negative Ion Generation, HEPA Filtration, Electrostatic Filtration, Activated Carbon Filtration, UV-C Sterilization, Hybrid Air Purification Systems), By Distribution Channel (Online Retail & E-Commerce, Brand-Owned Stores, Consumer Electronics Retailers, Pharmacies & Healthcare Stores, Specialty Retail Stores), By End-User Application and Battery Type Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

, By Technology (Negative Ion Generation, HEPA Filtration, Electrostatic Filtration, Activated Carbon Filtration, UV-C Sterilization, Hybrid Air Purification Systems), By Distribution Channel (Online Retail & E-Commerce, Brand-Owned Stores, Consumer Electronics Retailers, Pharmacies & Healthcare Stores, Specialty Retail Stores), By End-User Application and Battery Type Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

, By Technology (Negative Ion Generation, HEPA Filtration, Electrostatic Filtration, Activated Carbon Filtration, UV-C Sterilization, Hybrid Air Purification Systems), By Distribution Channel (Online Retail & E-Commerce, Brand-Owned Stores, Consumer Electronics Retailers, Pharmacies & Healthcare Stores, Specialty Retail Stores), By End-User Application and Battery Type Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Wearable Air Purifier Market?

The Global Wearable Air Purifier Market was valued at USD 1.13 Billion in 2024 and is projected to reach USD 3.85 Billion by 2034, growing at a CAGR of 13.0% from 2026 to 2034. Growth is driven by rising air pollution levels, increasing respiratory health concerns, demand for personal air quality protection, wearable health technologies, advanced filtration systems, ionization technologies, smart air purification devices, and growing urbanization worldwide.

Who are the major players in the Wearable Air Purifier Market?

LG ELECTRONICS INC., DYSON LTD., IBLE TECHNOLOGY INC. (AIRVIDA), FILTERSTREAM, LLC (AIRTAMER), RESPIRAY OU, XIAOMI CORPORATION, KONINKLIJKE PHILIPS N.V., IQAIR (IQAIR NORTH AMERICA, INC.), WEIN PRODUCTS, INC., FLO MASK, INC., AIRPOP (FRESH AIR INVESTMENT HOLDING CORP.), CAMBRIDGE MASKS CO., WINIX INC., 3M COMPANY, HONEYWELL INTERNATIONAL INC., O2 CANADA, NIRVANA BEING (BREATHE EASY LABS PRIVATE LIMITED), PURE ENRICHMENT (VISION INNOVATIONS, INC.), AIRTOMO, AIRDINBOR, Others

Which segments covered the Wearable Air Purifier Market?

By Product Type, (Neck-Worn Wearable Air Purifiers, Clip-On Wearable Air Purifiers, Mask-Integrated Air Purifiers, Pendant and Lanyard Air Purifiers, Wrist-Worn and Other Wearable Air Purifiers), By Technology, (Negative Ion Generation Technology, HEPA Filtration Technology, Electrostatic Filtration Technology, Activated Carbon Filtration Technology, UV-C Sterilization Technology, Hybrid Air Purification Systems), By Distribution Channel, (Online Retail & E-Commerce Platforms, Brand-Owned Stores, Consumer Electronics Retailers, Pharmacies & Healthcare Stores, Specialty Retail Stores), By End-User Application, (Personal Daily Use, Healthcare & Medical Use, Industrial & Occupational Safety, Travel & Transportation, Sports & Outdoor Activities), By Battery Type, (Rechargeable Lithium-Ion Batteries, Rechargeable Lithium-Polymer Batteries, Replaceable Batteries, Hybrid Power Systems)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Wearable Air Purifier Market

Published Date : 02 Jun 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date