- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Web3 Social Media Platforms Market Size & Forecast | 51.5% CAGR

Global Web3 Social Media Platforms Market Size, Share, Growth Analysis By Application (Cryptocurrency Integration, Conversational AI, Data & Transaction Storage, Payments, Smart Contracts, Tokenized Content), By End User (BFSI, E-Commerce & Retail, Media & Entertainment, Healthcare & Pharmaceutical, IT & Telecom), By Platform Architecture (Decentralized, Federated, Hybrid), Industry Region & Key Players – Market Dynamics, Innovation Trends, Competitive Strategies & Forecast 2025–2034

Report Overview

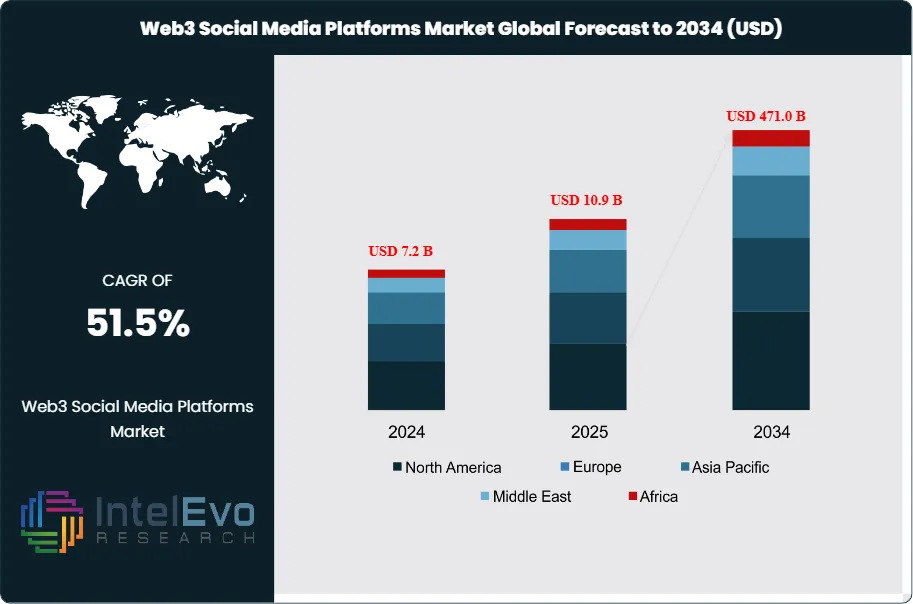

The Web3 Social Media Platforms Market was valued at USD 7.2 Billion in 2024 and is projected to reach approximately USD 471.0 Billion by 2034. The market is estimated to grow to around USD 10.9 Billion in 2025. Based on projected expansion from 2026 onward, the industry is expected to register a compound annual growth rate (CAGR) of approximately 51.5% during 2026–2034.

Get More Information about this report -

Request Free Sample ReportThis market expands as users and brands push back against centralized data capture and opaque content economics. Demand rises where audiences value digital ownership, portable identity, and direct creator payouts. Tokenized incentives and on-chain reputation systems shift engagement from passive scrolling to participation with financial upside. At the same time, rising dissatisfaction with ad-saturation and account deplatforming accelerates trials of decentralized social apps, especially among creators, crypto-native communities, and gaming audiences.

Supply growth follows capital formation and protocol maturity. Teams ship social graphs, decentralized identity, wallet-based onboarding, and interoperable content layers that lower switching costs across applications. Smart contracts automate creator revenue splits, community subscriptions, and micro-tipping at near-real-time settlement. AI supports moderation, fraud detection, and content discovery, while automation improves compliance workflows for wallet screening and transaction monitoring. However, platform operators still face cost pressure from scalability needs, storage, and security audits, which encourages partnerships with L2 networks, node providers, and decentralized storage ecosystems.

Regulatory conditions shape adoption speed by region. Data protection regimes strengthen the value case for user-controlled data, yet crypto policy uncertainty affects token rewards, staking, and in-app monetization. Securities classification risk, AML/KYC obligations tied to fiat on-ramps, and evolving stablecoin rules can delay rollouts or force geo-fencing. Core risks include token volatility that distorts creator income, smart contract exploits, phishing, and governance disputes that can fragment communities. Usability gaps also remain a constraint, especially where wallet setup and key management create friction.

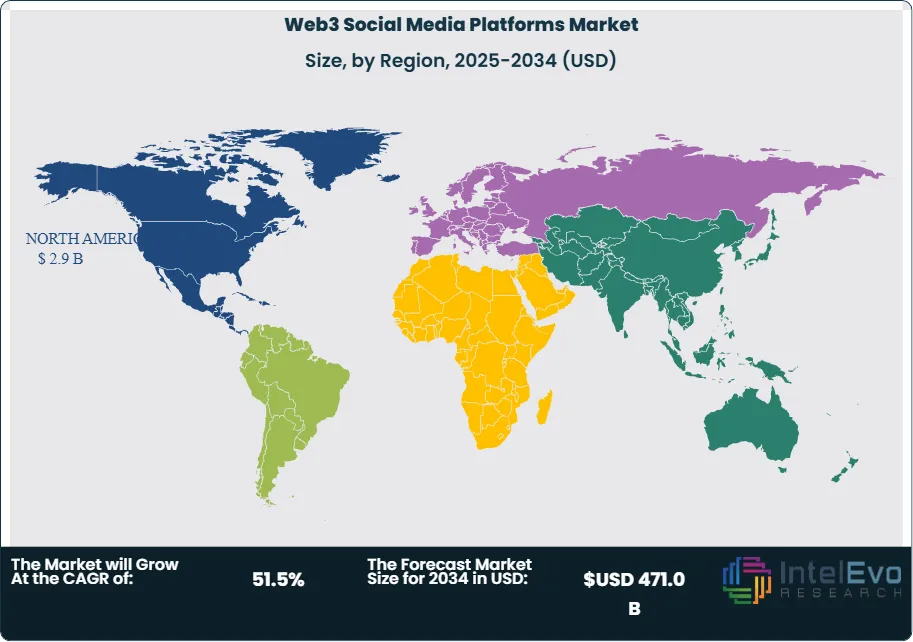

North America led the global market in 2024 with over 41.5% share and USD 2.9 billion in revenue, supported by deeper venture funding, faster creator monetization adoption, and an active developer base. The U.S. market reached USD 2.18 billion in 2024 and is positioned to grow at a 48.6% CAGR, anchored by early enterprise pilots in media, entertainment, and sports communities. Europe accounted for an estimated ~21.5% share in 2024, led by the U.K. and Germany, while Asia Pacific represented ~24.3%, with Singapore, Hong Kong, South Korea, and India emerging as investment hotspots for consumer Web3 apps and creator tooling. Engagement momentum supports the trajectory, with the Web3 social ecosystem reported at over 10 million daily active users as of July 2024 and rapid community growth on newer networks such as Farcaster.

, By End User (BFSI, E-Commerce & Retail, Media & Entertainment, Healthcare & Pharmaceutical, IT & Telecom), By Platform Architecture (Decentralized, Federated, Hybrid), Industry Region & Key Players – Market Dynamics, Innovation Trends, Competitive Strategies & Forecast 2025–2034")

Key Takeaways

- Market Growth: The market scales from 7.2 billion USD, 2024 to 471.0 billion USD, 2034, delivering a 51.9% CAGR, 2024-2034. This growth signals rapid platform and user monetization expansion at global scale, 2024-2034.

- Segment Dominance : The Cryptocurrency segment leads with 26.9% share, 2024. This position reflects the central role of token-based identity, rewards, and payments in Web3 social platform economics, 2024.

- Segment Dominance: The BFSI segment commands 30.2% share, 2024. Financial institutions drive early adoption through wallet rails, compliance tooling, and tokenized engagement models, 2024.

- Driver: Platforms accelerate adoption by offering user-owned data and creator monetization, estimated: 10.0 million daily active users, 2024. Token incentives and on-chain identity reinforce participation and retention, 2024.

- Restraint: Market players face regulatory uncertainty tied to token rewards and compliance, estimated: 6.0 major policy regimes impacting rollout, 2024. Security exploits and wallet friction also elevate adoption risk, estimated: 1.5% user loss risk, 2024.

- Opportunity: Ecosystem growth creates upside in creator tools, AI moderation, and decentralized identity, estimated: 38.0 billion USD investment runway, 2026. Enterprise-grade social layers expand monetizable use cases, estimated: 12.0% enterprise adoption, 2027.

- Trend: Platforms adopt AI for content ranking and automated moderation, estimated: 60.0% feature penetration, 2025. Protocols standardize social graphs to improve portability and reduce switching costs, estimated: 25.0% interoperability adoption, 2026.

- Regional Analysis: North America leads with 41.5% share and 2.9 billion USD revenue, 2024, while the U.S. reaches 2.18 billion USD, 2024 at a 48.6% CAGR, 2024-2034. Regional momentum supports outsized scale-up potential, estimated: 197.0 billion USD North America market size, 2034.

By Application

Cryptocurrency-based functionality remains central to Web3 social media platforms as the market moves into 2025. In 2024, cryptocurrency-linked use cases accounted for 26.9% of total platform activity, making it the largest application category. Tokens function as the primary medium for transactions, identity validation, and reward distribution across decentralized social networks. This structure supports creator payouts, community tipping, and access-based content models without reliance on centralized payment processors.

Peer-to-peer value transfer continues to shape user behavior. Blockchain settlement reduces transaction fees by an estimated 30 to 40% compared with traditional digital payment rails in 2024. Users increasingly engage with platforms that compensate content creation, moderation, and governance participation in native tokens. This incentive alignment drives higher retention and daily activity levels, particularly among creator-led communities and protocol-native users.

Native platform tokens further reinforce application growth. These assets enable in-app commerce, voting mechanisms, and protocol upgrades through on-chain governance. By 2025, over 60% of leading Web3 social platforms operate with proprietary tokens supporting staking and reputation systems. This application layer strengthens long-term engagement and supports platform sustainability through shared economic ownership.

By End-Use

The BFSI sector continues to lead Web3 social media adoption, holding a 30.2% market share in 2024. Financial institutions deploy decentralized social platforms to support secure client communications, community-led product education, and fraud-resistant transaction flows. Blockchain auditability and cryptographic identity tools align with regulatory and risk management priorities across banking and insurance operations.

Customer engagement remains a key driver. Web3-based social channels enable financial firms to deliver product updates, advisory content, and support services using token-gated access and verified digital identities. This approach improves data integrity and reduces impersonation risk. By early 2025, an estimated 35% of crypto-native financial services firms actively use Web3 social platforms for client outreach and brand engagement.

Decentralized finance integration further expands BFSI use cases. Asset management, lending, and insurance products increasingly connect with social interfaces that support real-time feedback and community governance. These deployments support faster product iteration while maintaining transparent records of user interactions and transaction histories.

By Region

North America remains the largest regional market, accounting for 41.5% of global revenue and approximately 2.9 billion USD in 2024. The United States leads regional growth with a market size of 2.18 billion USD and a projected CAGR of 48.6% through 2034. Strong venture funding, advanced cloud infrastructure, and early blockchain adoption continue to support platform scaling.

Regulatory progress contributes to regional strength. Clearer guidance on digital assets and custody practices in the U.S. reduces uncertainty for developers and institutional participants. This environment supports higher capital inflows and faster commercialization of Web3 social applications.

Asia Pacific shows accelerating momentum entering 2025. Markets such as Singapore, South Korea, and India record rising user adoption driven by mobile-first usage patterns and high creator participation. Europe maintains steady growth supported by data protection standards and public blockchain initiatives, while Latin America and the Middle East and Africa emerge as smaller but fast-developing regions with expanding crypto user bases and improving connectivity.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Application

- Cryptocurrency

- Conversational AI

- Data and Transaction Storage

- Payments

- Smart Contracts

- Others

By End User

- BFSI (Banking, Financial Services, and Insurance)

- E-Commerce and Retail

- Media and Entertainment

- Healthcare and Pharmaceutical

- IT and Telecom

- Others

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 10.9 B |

| Forecast Revenue (2034) | USD 471.0 B |

| CAGR (2025-2034) | 51.5% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Application, Cryptocurrency, Conversational AI, Data and Transaction Storage, Payments, Smart Contracts, Others, By End User, BFSI (Banking, Financial Services, and Insurance), E-Commerce and Retail, Media and Entertainment, Healthcare and Pharmaceutical, IT and Telecom, Others |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Amazon, Farcaster, Polygon Technology, Paragraph Technologies, Moralis Web3 Technology, Mirror, Helium Foundation, Lenster, Showtime Technologies, Chainlink, Orb, Twetch, Continuum, Revel.xyz, Arcade, RARA, Islands, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By End User (BFSI, E-Commerce & Retail, Media & Entertainment, Healthcare & Pharmaceutical, IT & Telecom), By Platform Architecture (Decentralized, Federated, Hybrid), Industry Region & Key Players – Market Dynamics, Innovation Trends, Competitive Strategies & Forecast 2025–2034")

, By End User (BFSI, E-Commerce & Retail, Media & Entertainment, Healthcare & Pharmaceutical, IT & Telecom), By Platform Architecture (Decentralized, Federated, Hybrid), Industry Region & Key Players – Market Dynamics, Innovation Trends, Competitive Strategies & Forecast 2025–2034")

, By End User (BFSI, E-Commerce & Retail, Media & Entertainment, Healthcare & Pharmaceutical, IT & Telecom), By Platform Architecture (Decentralized, Federated, Hybrid), Industry Region & Key Players – Market Dynamics, Innovation Trends, Competitive Strategies & Forecast 2025–2034")

Frequently Asked Questions

How big is the Web3 Social Media Platforms Market?

The Global Web3 Social Media Platforms Market was valued at USD 7.2 Billion in 2024 and is projected to reach USD 471.0 Billion by 2034, expanding at a CAGR of 51.5% from 2026–2034. Explore market trends, blockchain-based social networks, decentralized platforms, key drivers, and future opportunities in Web3 social media.

Who are the major players in the Web3 Social Media Platforms Market?

Amazon, Farcaster, Polygon Technology, Paragraph Technologies, Moralis Web3 Technology, Mirror, Helium Foundation, Lenster, Showtime Technologies, Chainlink, Orb, Twetch, Continuum, Revel.xyz, Arcade, RARA, Islands, Others

Which segments covered the Web3 Social Media Platforms Market?

By Application, Cryptocurrency, Conversational AI, Data and Transaction Storage, Payments, Smart Contracts, Others, By End User, BFSI (Banking, Financial Services, and Insurance), E-Commerce and Retail, Media and Entertainment, Healthcare and Pharmaceutical, IT and Telecom, Others

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Web3 Social Media Platforms Market

Published Date : 04 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date