- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Well Intervention Services Market Size, Share & Forecast | CAGR 5.9%

Global Well Intervention Services Market Size, Share, Growth Analysis By Intervention Type (Light Intervention, Medium Intervention, Heavy Intervention), By Service Type (Logging & Bottom Hole Survey, Stimulation, Tubing & Packer Repair, Sand Control & Zonal Isolation, Artificial Lift & Fishing Services), By Application (Onshore, Offshore), By Method (Wireline, Coiled Tubing, Hydraulic Workover, Slickline), Industry Trends, Competitive Landscape, Regional Insights & Forecast 2026–2034

Report Overview

| Market Size | Forecast Value | CAGR | Leading Region |

|---|---|---|---|

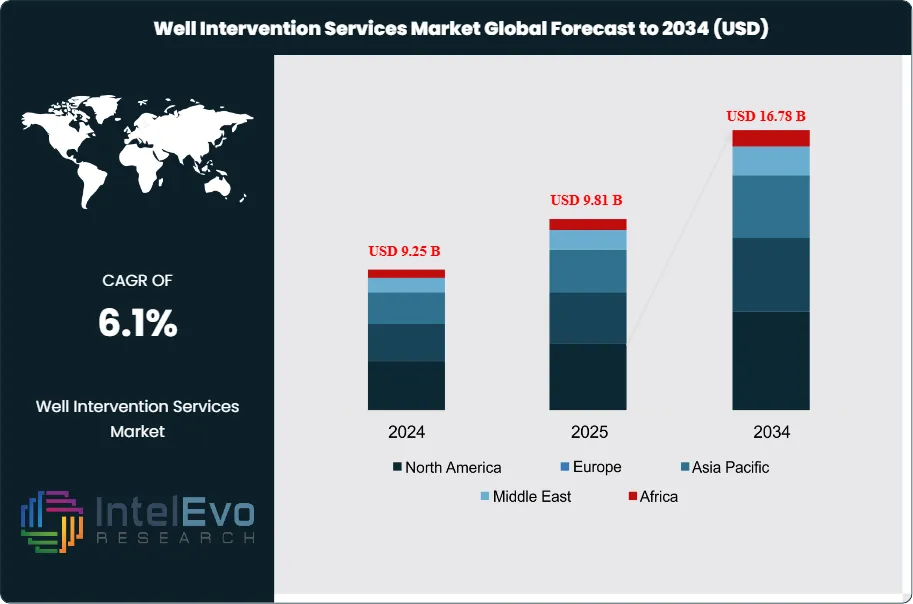

| USD 9.81 Billion, 2025 | USD 16.78 Billion, 2034 | 6.1%, 2026–2034 | North America, 37.2%, 2025 |

The Well Intervention Services Market was valued at approximately USD 9.25 Billion in 2024 and increased to USD 9.81 Billion in 2025. The market is projected to reach nearly USD 16.78 Billion by 2034, expanding at a compound annual growth rate (CAGR) of around 6.1% during the forecast period from 2026 to 2034. The 6.1% rate is mathematically consistent with the 2025 and 2034 values over a nine-year period. The Well Intervention Services Market remains a core part of upstream asset management because operators use intervention work to restore flow, manage water cut, repair tubing and packers, improve reservoir access, and extend well life without moving directly to full workovers or new drilling. North America led the market in 2025 with a 37.19% share, while onshore work remained the largest application and light intervention remained the largest intervention class.

Get More Information about this report -

Request Free Sample ReportThe Well Intervention Services Market is moving on two tracks. The first is volume recovery from mature wells. The IEA says nearly 90% of annual upstream oil and gas investment since 2019 has gone to offset production declines rather than to meet demand growth. The second is selective investment in higher-value offshore and gas assets where intervention lifts recovery faster than fresh drilling can. Lower oil prices are still constraining discretionary activity. The IEA expects a 6% fall in upstream oil investment in 2025, the first annual decline since the Covid slump. That pressure keeps customers focused on jobs with visible payback, especially logging, cleanout, stimulation, and light intervention campaigns.

Technology is changing how the Well Intervention Services Market competes. SLB is pushing autonomous intervention and digital control. Halliburton is expanding real-time hybrid coiled tubing. Baker Hughes is pairing telemetry and intelligent coiled tubing with mature-asset and subsea work. Weatherford is using SMART-LINK and digital monitoring to improve decision quality during intervention and production support. These tools matter because operators want fewer trips, better downhole visibility, tighter job design, and lower nonproductive time. Digital capability is now a practical differentiator in both offshore and complex onshore wells.

Regional activity patterns remain clear. North America is the volume center because of mature unconventional wells, strong service density, and ongoing production maintenance. Europe remains a premium market for offshore well stimulation, late-life intervention, and plug and abandonment support, with Norway’s oil and gas investment reaching a record in 2025 before easing in 2026. Latin America is gaining from Petrobras-led offshore work in Brazil. Asia Pacific is supported by gas security and brownfield activity in China, India, Australia, and Southeast Asia. The Middle East is rising through unconventional gas and large brownfield fields, especially in Saudi Arabia where the Jafurah program began output in late 2025. Risks remain. Tariffs and steel costs can raise service costs, and Baker Hughes warned of a USD 100 Million to USD 200 Million hit to 2025 core profit from tariffs.

, By Service Type (Logging & Bottom Hole Survey, Stimulation, Tubing & Packer Repair, Sand Control & Zonal Isolation, Artificial Lift & Fishing Services), By Application (Onshore, Offshore), By Method (Wireline, Coiled Tubing, Hydraulic Workover, Slickline), Industry Trends, Competitive Landscape, Regional Insights & Forecast 2026–2034")

Key Takeaways

- Market Growth: The Well Intervention Services Market was worth USD 9.81 Billion in 2025 and is projected to reach USD 16.78 Billion by 2034, at a 6.1% CAGR over 2026–2034. This growth profile aligns with current industry tracking and nine-year CAGR math.

- Segment Dominance: Light intervention led the market with an estimated 57.0% share in 2025, equal to about USD 5.59 Billion, 2025. It remains the largest intervention class because it supports repeat, lower-cost field maintenance.

- Segment Dominance: Onshore application led with an estimated 68.0% share in 2025, equal to about USD 6.67 Billion, 2025. Large mature land-well inventories and faster mobilization keep onshore demand ahead of offshore volume.

- Driver: The main driver is the rising need to offset decline from mature wells. Nearly 90.0% of annual upstream oil and gas investment since 2019 has gone to offset declines rather than meet demand growth.

- Restraint: The main restraint is capital discipline across upstream spending. Upstream oil investment is expected to fall 6.0% in 2025, while Baker Hughes flagged a possible USD 100 Million to USD 200 Million tariff impact on 2025 profit.

- Opportunity: The largest opportunity sits in offshore brownfield and unconventional gas assets. Saudi Arabia’s Jafurah program began output in December 2025 with first-phase capacity of 450 million cubic feet per day, creating a larger addressable base for intervention and production-enhancement services.

- Trend: The dominant trend is digital intervention. SLB’s autonomous multiline system reports a 30.0% increase in consistency and a 25.0% boost in efficiency, showing why automation is gaining traction.

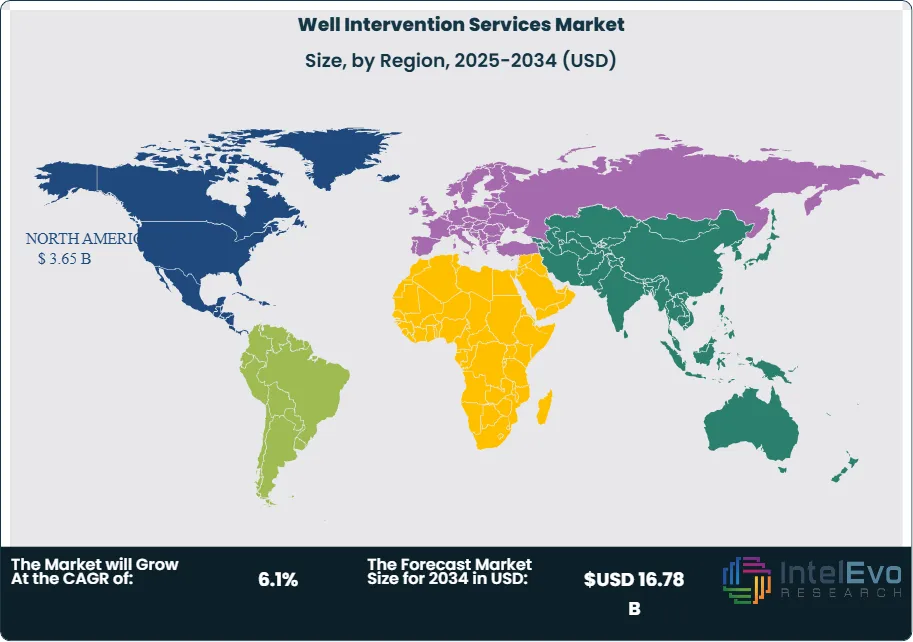

- Regional Analysis: North America led the Well Intervention Services Market with a 37.19% share in 2025, equal to about USD 3.65 Billion, 2025. The region leads because of mature land wells, shale intensity, and dense service infrastructure.

Competitive Summary

The Well Intervention Services Market is moderately consolidated. The top four companies, SLB, Halliburton, Baker Hughes, and Weatherford, held an estimated 46.0% of 2025 market revenue. Competition is mainly technology-driven and geographic. Global leaders win where offshore execution, real-time diagnostics, and integrated intervention packages matter most. Competitive intensity rose in 2025 and early 2026 through SLB’s acquisition of Stimline Digital, Halliburton’s North Sea stimulation award, Baker Hughes’ Petrobras offshore vessel extension, and Archer’s Equinor P&A award worth up to USD 140 Million.

Competitive Landscape Matrix

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| SLB | US | Leader | Autonomous Well Intervention platform | North America, Latin America, Middle East | Acquired Stimline Digital, a cloud-based well intervention software specialist, in Aug 2025 |

| Halliburton | US | Leader | SPECTRUM real-time hybrid coiled tubing service | North America, Europe, Middle East | Won a five-year North Sea well stimulation services contract from ConocoPhillips in Aug 2025 |

| Baker Hughes | US | Leader | SureVIEW TeleCoil intelligent monitoring telemetry service | Latin America, Middle East, North America | Secured a multi-year Petrobras contract extension for offshore stimulation vessels in Sep 2025 |

| Weatherford | US | Leader | SMART-LINK system | Middle East, Europe, Asia Pacific | Won an eight-year real-time digital wellsite monitoring contract from Romgaz in Sep 2025 across thousands of wells |

| Helix Energy Solutions | US | Challenger | Siem Helix riser-based well intervention vessels | Latin America, North America, North Sea | Won a multi-year U.S. Gulf production enhancement and well abandonment contract starting in 2026, announced Aug 2025 |

| Archer | Bermuda | Challenger | Platform Drilling and P&A well services | Europe, Latin America | Won an Equinor execution contract covering P&A of 30 subsea wells, worth up to USD 140 Million, in Jan 2026 |

| Expro | UK | Challenger | Subsea Well Access and RLWI systems | Europe, Australia, Middle East | Continued subsea intervention rollout and ELITE Completion service deployment through 2025–2026 |

| NOV | US | Niche Player | Hydra Rig intervention equipment | North America, Middle East | Continued 2025 delivery of intervention packages including coiled tubing units and injector heads |

| Oil States International | US | Niche Player | Intervention and workover equipment portfolio | North America | Expanded offshore and completion-tool exposure through 2025 integrated product deliveries |

| KLX Energy Services | US | Niche Player | Basin-based intervention and downhole tool support | North America | Reported stronger Rockies service demand in 2025 across coiled tubing, tech services, and production support |

By Intervention Type

Light intervention held an estimated 57.0% share of the Well Intervention Services Market in 2025, equal to roughly USD 5.59 Billion, 2025. This segment covers wireline, slickline, coiled tubing, and other lower-footprint activities used to restore production, gather downhole data, set plugs, remove debris, and handle smaller mechanical issues without moving to a full workover. Current market research identifies light intervention as the largest class in 2025, which fits operator behavior. Customers are protecting cash flow and favoring shorter, lower-cost jobs that can be repeated across mature well inventories. Light intervention also aligns with digital adoption because providers can combine telemetry, imaging, and real-time pressure and temperature data inside a lower-cost execution model. SLB, Halliburton, Baker Hughes, and Weatherford all have strong positions here through wireline, coiled tubing, and digitally enabled field systems. The segment should keep its lead through 2034 because it delivers the fastest payback and the broadest field applicability.

Medium intervention accounted for an estimated 25.0% share in 2025, or about USD 2.45 Billion, 2025. This segment includes more complex remedial work than light intervention but usually stops short of full heavy workover scope. It is widely used in subsea wells, higher-pressure wells, and jobs that require stronger mechanical access, higher lifting capacity, or more involved equipment replacement. The segment is gaining from rising subsea activity, which is a strong indicator for offshore brownfield basins in Brazil, Norway, West Africa, and the Gulf of Mexico. It benefits from deeper offshore portfolios where the economics of recovering a few extra days of uptime can justify higher service intensity. Helix, Expro, SLB, and Halliburton are well placed because they can combine vessel access, subsea tooling, diagnostics, and integrated field management. Medium intervention should outgrow light intervention in selected offshore basins, but it will remain smaller on a global basis because the installed base of mature onshore wells is far larger.

Heavy intervention represented an estimated 18.0% share in 2025, equal to about USD 1.77 Billion, 2025. Heavy intervention includes jobs that need major tubing replacement, full-scale equipment changeout, snubbing or hydraulic workover, or deeper mechanical repair that cannot be executed through light methods. This is the fastest-growing class because more mature wells are moving from diagnostic and minor repair work toward larger life-extension campaigns. Growth is strongest offshore and in older conventional assets where operators need to delay abandonment and recover more barrels from high-value infrastructure. Heavy intervention also benefits from a rising P&A and late-life well management workload in Europe and parts of Latin America. The competitive field is narrower than in light intervention because execution risk, equipment intensity, and HSE demands are higher. Halliburton, SLB, Helix, and Archer have stronger relative positions in this segment because they can manage larger offshore and complex well scopes.

By Service Type

Logging and bottom hole survey was the largest service segment in the Well Intervention Services Market with an estimated 28.0% share in 2025, equal to about USD 2.75 Billion, 2025. This positioning makes sense because data-led intervention sits at the center of production restoration, reservoir surveillance, and mature-field decision making. Operators increasingly want downhole information before committing to heavier remedial spend. This service line is strengthened by digital tools, deeper deviated wells, and offshore wells where data quality can change the full economics of an intervention campaign. SLB, Halliburton, and Baker Hughes are strong here because they connect wireline, telemetry, and intervention planning inside one package. Weatherford is also gaining ground where real-time monitoring links intervention with field production decisions.

Stimulation services accounted for an estimated 18.0% share in 2025, or about USD 1.77 Billion, 2025. This segment includes acidizing and other production-enhancement work performed to improve flow, reopen damaged intervals, and support mature reservoir recovery. It is especially important in offshore brownfield basins, high-value gas wells, and assets where a short production uplift can justify premium service pricing. Halliburton’s five-year North Sea well stimulation contract and Baker Hughes’ multi-year Petrobras offshore stimulation vessel extension both highlight the commercial importance of this segment in 2025. The segment benefits from tighter capital allocation because stimulation can restore output faster than greenfield drilling in many mature assets. Competitive strength sits with companies that combine chemistry, pumping, diagnostics, and offshore logistics.

Tubing and packer failure repair represented an estimated 16.0% share in 2025, equal to about USD 1.57 Billion, 2025. This segment remains essential because mechanical failure is one of the most common intervention triggers in aging wells. The work includes tubing leak repair, packer retrieval, isolation, and selective downhole equipment replacement. It is more labor and equipment intensive than logging, but less capital intensive than full heavy workover. Demand is strongest in mature onshore wells and older conventional offshore fields where incremental output still justifies remedial spend. Market competition is broad because global leaders and regional firms can both operate here, but scale matters in offshore settings where intervention timing and equipment readiness drive customer choice.

Sand control and zonal isolation together held an estimated 21.0% share in 2025, equal to about USD 2.06 Billion, 2025. This grouping matters in wells facing sand ingress, unwanted fluids, zonal communication, and completion degradation. Offshore operators rely heavily on these services because intervention cost is high and the penalty for poor zonal control is even higher. The segment is also linked to heavy and medium intervention work because mechanical access and completion compatibility often matter. Growth is strongest in offshore Latin America, Europe, and parts of the Middle East where operators are working large brownfield assets with long remaining platform or subsea infrastructure life. Global providers have an edge because these jobs require broader engineering support and tighter coordination with completions systems.

Artificial lift, fishing, and other services made up the remaining estimated 17.0% share in 2025, or about USD 1.67 Billion, 2025. These services include stuck-tool recovery, equipment retrieval, lift-system remediation, and smaller specialized tasks that keep wells online. While individually smaller, this bucket creates repeat demand in land basins and mature offshore fields. Bundled intervention support is becoming more common across drilling, completions, and field maintenance. This area remains less consolidated than premium offshore stimulation or logging, but global firms still win the higher-value packages because they can combine tools, people, and long-term contracts.

By Application

Onshore accounted for an estimated 68.0% share of the Well Intervention Services Market in 2025, equal to roughly USD 6.67 Billion, 2025. The large installed base of mature wells across North America, the Middle East, China, India, and parts of Latin America keeps onshore intervention ahead. Onshore intervention is driven by scale and repetition. Operators can mobilize faster, use a broader mix of local and international service firms, and apply intervention campaigns across many wells in sequence. The segment also benefits from tighter budgets because light intervention and production-restoration work on land often delivers the fastest payout. This segment is more price competitive than offshore, but utilization is broader and job frequency is higher.

Offshore held an estimated 32.0% share in 2025, or about USD 3.14 Billion, 2025. Offshore intervention volumes are lower than onshore, but revenue per job is materially higher because vessel cost, subsea access, HSE controls, and technical complexity all rise. Brazil, the North Sea, the U.S. Gulf, West Africa, and Australia are the main offshore demand centers. Petrobras awards to SLB and Baker Hughes, Halliburton’s North Sea stimulation contract, and Helix and Archer awards all show that offshore work remains the premium segment of the market. Offshore should outgrow onshore in rate terms through 2034, but its smaller base means onshore will remain the larger revenue pool.

By Intervention Method

Wireline was the largest intervention method with an estimated 31.0% share in 2025, equal to about USD 3.04 Billion, 2025. Wireline remains central because it supports logging, perforation, setting tools, and many lower-cost intervention tasks with relatively quick mobilization. The segment benefits from better sensors, deeper deviation capability, and digital controls. It is used across both land and offshore wells and is often the first step before more involved intervention.

Coiled tubing accounted for an estimated 27.0% share in 2025, or about USD 2.65 Billion, 2025. Coiled tubing is widely used for cleanout, stimulation support, nitrogen kickoffs, circulation, and remedial operations in both onshore and offshore wells. It is especially important in light and medium intervention because it gives mechanical access without moving directly to a heavy workover. Ongoing investment in telemetry and real-time systems is raising its value in complex wells. The method should gain share in data-rich and high-pressure applications where operators need more control during execution.

Hydraulic workover and snubbing represented an estimated 18.0% share in 2025, or about USD 1.77 Billion, 2025. This method serves live-well and higher-force interventions where tubing movement, well control, and deeper mechanical tasks make wireline or coiled tubing insufficient. It is more equipment intensive and more exposed to offshore and higher-value conventional fields. The segment will benefit from the aging of offshore wells and the rise in late-life asset management.

Slickline and other methods held the remaining estimated 24.0% share in 2025, or about USD 2.35 Billion, 2025. Slickline remains useful in lower-cost mechanical tasks, while other methods include niche retrieval, downhole tool deployment, and hybrid packages. The category stays relevant because not all wells need real-time power or larger tubing-conveyed solutions. Regional providers participate more heavily here, but digital field integration is steadily shifting more value toward firms with broader service portfolios.

Regional Analysis

North America Well Intervention Services Market

North America held 37.2% of the Well Intervention Services Market in 2025, equal to about USD 3.65 Billion, 2025. The region leads because it combines high well count, mature unconventional inventory, large service fleets, and rapid mobilization. The United States is the clear anchor. It benefits from shale maintenance, refrac-linked well servicing, production logging, tubing repair, and rising Gulf of Mexico activity. Canada remains the second key country because deep land basins and seasonal maintenance activity support repeat intervention work. Mexico is smaller but strategically important because offshore development such as Trion and broader Gulf activity create demand for intervention, completion support, and subsea services. Regulation in the region centers on safety, emissions control, and service reliability rather than direct restrictions on intervention activity. North America should remain the largest regional market through 2034, though its share will gradually ease as offshore Latin America and Middle East gas assets grow faster.

Europe Well Intervention Services Market

Europe accounted for an estimated 22.1% share in 2025, equal to about USD 2.17 Billion, 2025. The region remains a premium intervention market because of offshore complexity, mature basin economics, and heavy late-life asset management. Norway is the dominant country, with 2025 oil and gas investments reaching a record level before slowing in 2026. That supports demand for stimulation, logging, subsea intervention, and P&A support. The UK remains the second key market due to North Sea brownfield work, late-life interventions, and well abandonment scope. Germany is smaller and more service-engineering oriented, while the Netherlands remains relevant through gas-field support and offshore engineering exposure. Regulation is stricter here than in most other regions. Operators face more demanding HSE, decommissioning, and emissions requirements, which increases demand for lower-footprint intervention methods such as RLWI, wireline, and selected medium-intervention packages. Europe should keep its role as the highest-value intervention region on a per-well basis even if total revenue stays below North America.

Asia Pacific Well Intervention Services Market

Asia Pacific represented an estimated 18.6% share in 2025, or about USD 1.82 Billion, 2025. China is the largest country market because of its large mature onshore base and strong domestic production goals. India follows through national oil company intervention activity and rising need for production enhancement in older assets. Australia is strategically important because offshore gas and subsea developments create premium intervention demand. Malaysia is also important because offshore brownfield and gas-linked work remains steady. Demand in Asia Pacific is shaped by energy security. Governments across the region continue to favor domestic output and field-life extension. Competition is mixed between international service providers and national or regional firms. Asia Pacific should post solid growth through 2034 because gas demand, mature offshore infrastructure, and brownfield recovery work continue to support service demand.

Latin America Well Intervention Services Market

Latin America held an estimated 12.4% share in 2025, equal to about USD 1.22 Billion, 2025. Brazil dominates by a wide margin. Petrobras awarded SLB an USD 800 Million three-year offshore services contract in December 2024, and Baker Hughes later secured a multi-year extension for offshore stimulation vessels in September 2025. Those deals show that offshore Brazil remains one of the strongest intervention and production-enhancement markets in the world. Mexico is the second strategic country because offshore developments and field-life extension work in the Gulf support intervention demand. Argentina is the third key country through shale and mature-field work, though activity is more cyclical and pricing can move sharply with operator budgets. The regional market benefits from offshore brownfield recovery, pre-salt expansion, and deepwater development, but it also faces political and budget volatility. Latin America should grow faster than North America in percentage terms through 2034 because Brazil’s offshore development and brownfield scope remain large.

Middle East & Africa Well Intervention Services Market

Middle East & Africa accounted for an estimated 9.7% share in 2025, equal to about USD 0.95 Billion, 2025. Saudi Arabia is the main driver. Jafurah’s first phase began output in late 2025 at 450 million cubic feet per day, and the broader unconventional gas program is expected to displace 500,000 barrels per day of oil at peak. That creates a large future base for stimulation, coiled tubing, logging, and production-support intervention. The UAE remains important for large brownfield fields and offshore maintenance. South Africa is smaller today but retains long-term offshore relevance. Oman is the fourth strategic market because mature onshore fields keep intervention demand active. The region’s investment backdrop remains favorable for production extension and gas expansion, though geopolitical risk and procurement cycles can slow field execution. Middle East & Africa should gain share through 2034 as gas-led projects and mature giant fields demand more intervention intensity.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Intervention Type

- Light Intervention

- Medium Intervention

- Heavy Intervention

By Service Type

- Logging and Bottom Hole Survey

- Stimulation

- Tubing and Packer Failure Repair

- Sand Control and Zonal Isolation

- Artificial Lift, Fishing, and Other Services

By Application

- Onshore

- Offshore

By Intervention Method

- Wireline

- Coiled Tubing

- Hydraulic Workover and Snubbing

- Slickline and Other Methods

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 9.81 B |

| Forecast Revenue (2034) | USD 16.78 B |

| CAGR (2025-2034) | 6.1% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Intervention Type (Light Intervention, Medium Intervention, Heavy Intervention), By Service Type (Logging and Bottom Hole Survey, Stimulation, Tubing and Packer Failure Repair, Sand Control and Zonal Isolation, Artificial Lift, Fishing, and Other Services), By Application (Onshore, Offshore), By Intervention Method (Wireline, Coiled Tubing, Hydraulic Workover and Snubbing, Slickline and Other Methods) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | SLB, HALLIBURTON, BAKER HUGHES, WEATHERFORD, HELIX ENERGY SOLUTIONS, ARCHER, EXPRO, NOV, OIL STATES INTERNATIONAL, SUPERIOR ENERGY SERVICES, KLX ENERGY SERVICES, TECHNIPFMC, NEXXT ENERGY SERVICES, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Service Type (Logging & Bottom Hole Survey, Stimulation, Tubing & Packer Repair, Sand Control & Zonal Isolation, Artificial Lift & Fishing Services), By Application (Onshore, Offshore), By Method (Wireline, Coiled Tubing, Hydraulic Workover, Slickline), Industry Trends, Competitive Landscape, Regional Insights & Forecast 2026–2034")

, By Service Type (Logging & Bottom Hole Survey, Stimulation, Tubing & Packer Repair, Sand Control & Zonal Isolation, Artificial Lift & Fishing Services), By Application (Onshore, Offshore), By Method (Wireline, Coiled Tubing, Hydraulic Workover, Slickline), Industry Trends, Competitive Landscape, Regional Insights & Forecast 2026–2034")

, By Service Type (Logging & Bottom Hole Survey, Stimulation, Tubing & Packer Repair, Sand Control & Zonal Isolation, Artificial Lift & Fishing Services), By Application (Onshore, Offshore), By Method (Wireline, Coiled Tubing, Hydraulic Workover, Slickline), Industry Trends, Competitive Landscape, Regional Insights & Forecast 2026–2034")

Frequently Asked Questions

How big is the Well Intervention Services Market?

The Global Well Intervention Services Market was valued at USD 9.25 Billion in 2024 and USD 9.81 Billion in 2025, projected to reach USD 16.78 Billion by 2034, growing at a CAGR of 5.9% from 2026–2034, driven by rising demand for enhanced recovery, aging well maintenance, and offshore intervention services.

Who are the major players in the Well Intervention Services Market?

SLB, HALLIBURTON, BAKER HUGHES, WEATHERFORD, HELIX ENERGY SOLUTIONS, ARCHER, EXPRO, NOV, OIL STATES INTERNATIONAL, SUPERIOR ENERGY SERVICES, KLX ENERGY SERVICES, TECHNIPFMC, NEXXT ENERGY SERVICES, Others

Which segments covered the Well Intervention Services Market?

By Intervention Type (Light Intervention, Medium Intervention, Heavy Intervention), By Service Type (Logging and Bottom Hole Survey, Stimulation, Tubing and Packer Failure Repair, Sand Control and Zonal Isolation, Artificial Lift, Fishing, and Other Services), By Application (Onshore, Offshore), By Intervention Method (Wireline, Coiled Tubing, Hydraulic Workover and Snubbing, Slickline and Other Methods)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Well Intervention Services Market

Published Date : 18 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date