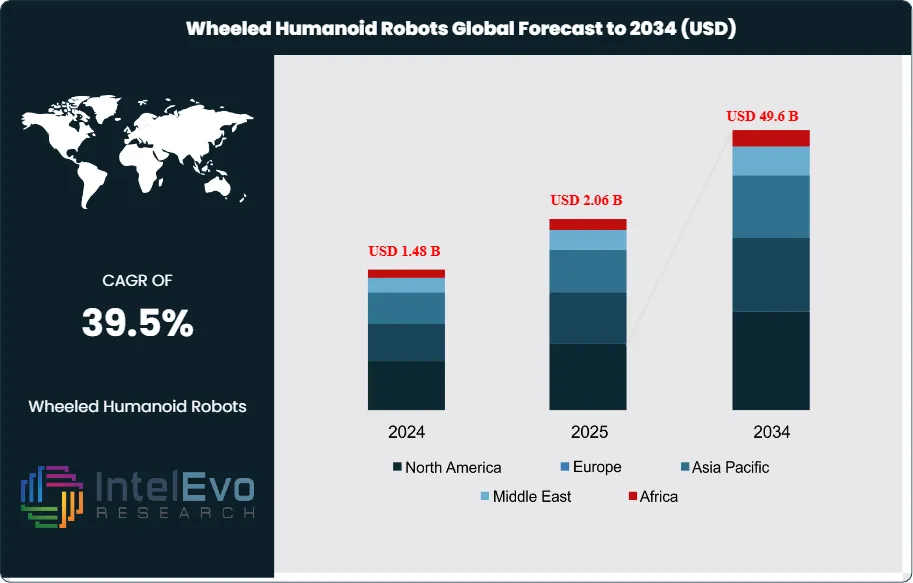

The Wheeled Humanoid Robots Market size is projected to reach approximately USD 49.6 Billion by 2034, up from USD 1.48 Billion in 2024, growing at a robust CAGR of 39.5% during the forecast period from 2025 to 2034. The surge in demand for autonomous and intelligent service robots across logistics, healthcare, defense, and retail sectors is fueling this unprecedented growth. As AI, sensor technology, and robotics integration continue to advance, wheeled humanoid robots are becoming more adaptive, efficient, and economically viable. This transformative shift is positioning humanoid robots as the next big leap in automation and human-robot collaboration.

The wheeled‑humanoid robots market comprises robots that combine a human‑like torso/head/arms with wheeled mobility. Variants include fully wheeled platforms, hybrid wheeled+leg systems, mobile‑manipulation units and telepresence humanoids. These platforms are designed primarily for indoor, structured environments where wheels provide speed, efficiency and stability on flat surfaces while humanoid form and manipulators enable human‑oriented tasks. Adoption is driven by persistent labor shortages in logistics/retail/healthcare; the need for 24/7 contactless service; and rapid progress in AI, sensing, batteries and compliant actuation that have improved reliability and lowered operating costs. These forces make wheeled‑humanoids attractive where mobility plus manipulation/interaction are required. High upfront costs, integration complexity and lengthy payback cycles restrict adoption among small and medium buyers. Regulatory uncertainty, safety standards and liability/privacy concerns for human‑facing robots create additional procurement friction and can delay large institutional rollouts. Large addressable opportunities exist in healthcare and eldercare, structured logistics and facility services, and commercial telepresence. Successful pilots that demonstrate safety and ROI can convert one‑off deployments into fleet rollouts and service contracts. The vendor landscape mixes research labs, deep‑tech startups and legacy robot manufacturers. Business models range from direct hardware sales to robotics‑as‑a‑service (RaaS), recurring software subscriptions and managed fleets. Consolidation risk exists as larger incumbents may bundle robotics into broader automation stacks.

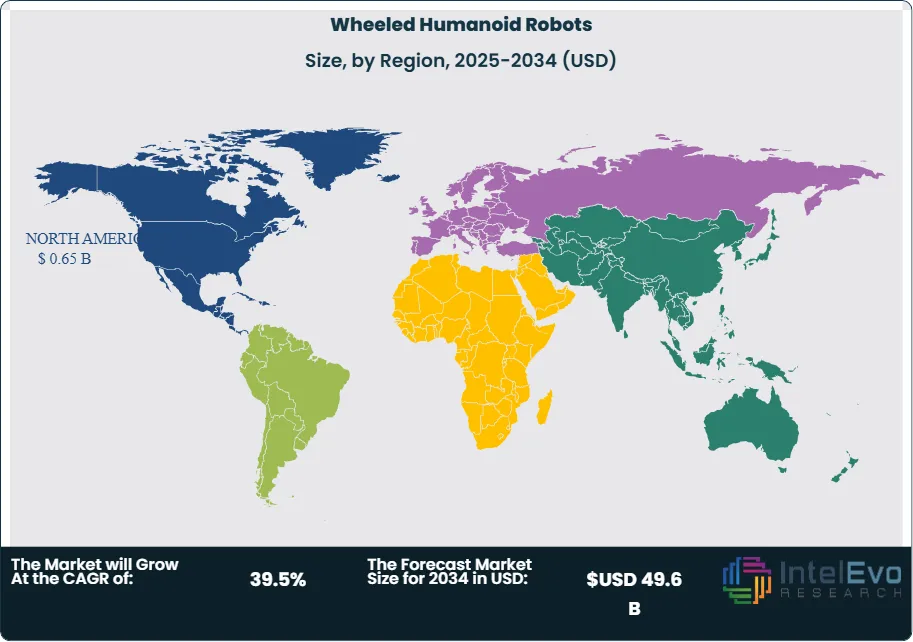

North America currently leads the market estimates ~43.2% share in 2024 due to concentrated venture/corporate funding, a dense ecosystem of early adopters and rapid commercialization pathways. APAC is a close follower with strong manufacturing capacity and fast adoption in service sectors; Europe emphasizes research, safety and regulated pilots that build long‑term trust.

The COVID‑19 pandemic acted as both an accelerant and a stress test for wheeled‑humanoid adoption. Early in the pandemic, healthcare providers, long‑term care facilities and retail/logistics operators prioritized contactless delivery, remote monitoring and labor‑saving automation — creating urgent pilot opportunities for robots that could operate without close human contact. That demand pull shortened some commercialization timelines for service and telepresence robots and increased willingness by buyers to trial robotic solutions. Geopolitics is an increasingly important determinant of how the wheeled‑humanoid market unfolds. Key vectors include trade tensions, export controls, national industrial policies that favor domestic champions, and defense/dual‑use scrutiny of advanced robotic systems. These forces push vendors and customers to reconfigure supply chains, seek diversified manufacturing footprints, and factor compliance and export licensing into product roadmaps. At the same time, state funding programs and strategic technology initiatives in the U.S., Europe, Japan and parts of APAC are accelerating R&D and early institutional procurement.

Key Takeaways

Market Growth: The wheeled‑humanoid segment is projected to expand rapidly from roughly USD 1.48 billion in 2024 to about USD 49.6 billion by 2034 driven by commercialization in logistics, healthcare and service verticals.

Product‑type analysis: Mobile‑manipulation wheeled humanoids (wheels + multi‑DOF arms) represent the largest product revenue pool because they combine fast, stable mobility with object handling and human‑facing interaction, unlocking the broadest set of end‑to‑end automation use cases.

Component analysis: Hardware captures the largest share of near‑term market value — the physical chassis, actuators, sensors, batteries and embedded electronics dominate BOM and upfront spend — while software (perception, motion control, fleet orchestration) is the fastest‑growing recurring revenue stream.

Application analysis: Personal assistance & caregiving, logistics/warehouse automation, hospitality/retail services and telepresence lead demand, with personal assistance/caregiving and structured indoor logistics showing the strongest willingness to pay for safety‑certified, interactive platforms.

Drivers: Persistent labor shortages in warehousing and eldercare, major private funding and corporate R&D, plus rapid improvements in AI/perception, battery technology and sensors are accelerating pilot-to-production transitions and expanding use cases.

Restraints: High upfront CAPEX, complex systems integration (IT/workflow/facility changes), unclear regulatory standards for human‑facing robots and liability/privacy concerns slow procurement cycles and limit SME uptake.

Opportunities: Large, addressable deployments in healthcare/eldercare (in‑facility and in‑home support), fleet conversions in logistics and managed‑service (RaaS) models offering lower entry cost and recurring revenue for vendors. Pilots that demonstrate safety and ROI can accelerate fleet rollouts.

Trends: Rise of Robotics‑as‑a‑Service and fleet orchestration platforms, hybrid wheeled/leg designs for better environment coverage, edge/embodied AI for safer autonomy, modular manipulation attachments, and tighter integrations between robot hardware and enterprise software stacks.

Regional leader: North America currently holds the 43.2 % largest share in the wheeled‑humanoid market to concentrated venture/corporate funding, dense early‑adopter verticals (warehousing, healthcare, retail), and rapid commercialization pathways; APAC (China, Japan, Korea) is a close, fast‑growing second with strong manufacturing scale and domestic vendors.

Product Analysis

Among the product categories you listed, mobile‑manipulation wheeled humanoids (wheels + multi‑DOF arms) currently capture the largest share of the wheeled‑humanoid market. These platforms combine dependable flat‑surface mobility with manipulation and interaction capabilities that unlock the widest set of commercial use cases (warehouse pick & place, room‑to‑room deliveries in hospitals, kiosk service in retail/hospitality and light facility maintenance). Because they can both move fast and handle objects or interact with people, buyers favor them for end‑to‑end automation workflows, which leads to larger order sizes, recurring service agreements (maintenance, fleet software) and higher revenue per unit versus simple telepresence or purely wheeled platforms. Vendors such as Aeolus, Figure and others have emphasized manipulation-capable wheeled designs for commercial pilots, reinforcing this product‑level demand concentration.

Component Analysis

The hardware component accounts for the maximum share of revenue in the wheeled‑humanoid market. Hardware includes the mechanical chassis/wheelbase, actuators, sensors (lidar/cameras/IMUs), power systems (batteries), and on‑board compute/embedded electronics—items that dominate bill‑of‑materials cost and require significant engineering and certification. Because initial procurement is capital‑intensive (robot bodies, safety systems, payload subsystems) and hardware replacement/upgrade cycles drive a large portion of spend, hardware captures the bulk of near‑term market value. Software (control stacks, perception models, fleet orchestration, SaaS analytics) is the fastest‑growing segment in percentage terms—enabling recurring revenue and operational improvements—but its relative share remains smaller versus the high CAPEX of physical platforms.

Regional Analysis

North America Leads with More Than 44% Market Share in Global Mobile Esports Market. North America currently holds the largest share of the wheeled‑humanoid robots market estimates 44% share in 2024, with the U.S. market ~USD 0.44B), and is the clear market leader today. Several factors explain North America’s lead: a dense concentration of robotics startups and tier‑one tech companies investing heavily in humanoid R&D; strong venture and corporate capital flows that accelerate prototype → pilot → commercialization cycles (e.g., high‑profile funding and partnerships); large, well‑funded early adopter verticals (warehousing, healthcare systems, retail chains and logistics operators) that can absorb upfront integration costs; and mature regulatory & standards ecosystems. APAC (notably China, Japan and South Korea) is a fast‑growing market with strong local manufacturers, large consumer and service sectors, and aggressive public/private investment in robotics — several broader humanoid market reports place APAC as a major contributor to near‑term volume. Europe is strong in research, demo‑grade deployments and human‑centric robotics (Germany, UK, Spain), with use cases in healthcare and industrial applications; regulatory caution in some European markets can slow rollouts but raises long‑term trust.

By Product (Fully wheeled humanoids (wheelbase only), Hybrid wheeled + leg (limited stepping for thresholds), Mobile manipulation humanoids (wheels + multi DOF arms), Telepresence wheeled humanoids (screen/head + mobility)), By Component (Hardware, Software, Services), By Deployment Model (Capital purchase, Robot-as-a-Service (RaaS) / subscription / per task pricing, Managed fleet + software subscription), By Mobility Type (Two-Wheeled Humanoid Robots, Four-Wheeled Humanoid Robots, Omni-Directional Wheeled Robots), By End User (Industrial, Commercial, Institutional, Residential), By Application (Logistics and Warehousing, Healthcare and Elder Care, Retail and Customer Service, Education and Research, Defense and Security, Others)

Research Methodology

Primary Research- 100 Interviews of Stakeholders

Secondary Research

Desk Research

Regional scope

North America (United States, Canada, Mexico)

Latin America (Brazil, Argentina, Columbia)

East Asia And Pacific (China, Japan, South Korea, Australia, Cambodia, Fiji, Indonesia)

Sea And South Asia (India, Singapore, Thailand, Taiwan, Malaysia)

Eastern Europe (Poland, Russia, Czech Republic, Romania)

Western Europe (Germany, U.K., France, Spain, Itlay)

Middle East & Africa (GCC Countries, Egypt, Nigeria, South Africa, Israel)

Competitive Landscape

SoftBank Robotics, Ubtech Robotics, Toyota Motor Corporation, Kawasaki Heavy Industries, PAL Robotics, CloudMinds,Hanson Robotics, AgileX Robotics, Fourier Intelligence, Promobot, Keenon Robotics, Unitree Robotics, Future Robot Co.Ltd., Robotis, Siasun Robot & Automation

Customization Scope

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements.

Pricing and Purchase Options

Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF).

TABLE OF CONTENTS

1. EXECUTIVE SUMMARY

1.1. MARKET SNAPSHOT

1.2. KEY FINDINGS & INSIGHTS

1.3. ANALYST RECOMMENDATIONS

1.4. FUTURE OUTLOOK

2. RESEARCH METHODOLOGY

2.1. MARKET DEFINITION & SCOPE

2.2. RESEARCH OBJECTIVES: PRIMARY & SECONDARY DATA SOURCES

2.3. DATA COLLECTION SOURCES

2.3.1. COVERAGE OF 100+ PRIMARY RESEARCH/CONSULTATION CALLS WITH INDUSTRY STAKEHOLDERS

FIGURE 17 NORTH AMERICA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 18 NORTH AMERICA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 19 MARKET SHARE BY COUNTRY

FIGURE 20 LATIN AMERICA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 21 LATIN AMERICA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 22 MARKET SHARE BY COUNTRY

FIGURE 23 EASTERN EUROPE WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 24 EASTERN EUROPE WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 25 MARKET SHARE BY COUNTRY

FIGURE 26 WESTERN EUROPE WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 27 WESTERN EUROPE WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 28 MARKET SHARE BY COUNTRY

FIGURE 29 EAST ASIA AND PACIFIC WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 30 EAST ASIA AND PACIFIC WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 31 MARKET SHARE BY COUNTRY

FIGURE 32 SEA AND SOUTH ASIA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 33 SEA AND SOUTH ASIA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 34 MARKET SHARE BY COUNTRY

FIGURE 35 MIDDLE EAST AND AFRICA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 36 MIDDLE EAST AND AFRICA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 37 NORTH AMERICA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 38 U.S. WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 39 U.S. WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 40 CANADA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 41 CANADA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 42 LATIN AMERICA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 43 MEXICO WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 44 MEXICO WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 45 BRAZIL WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 46 BRAZIL WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 47 ARGENTINA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 48 ARGENTINA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 49 COLUMBIA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 50 COLUMBIA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 51 REST OF LATIN AMERICA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 52 REST OF LATIN AMERICA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 53 EASTERN EUROPE WHEELED HUMANOID ROBOTS CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 54 POLAND WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 55 POLAND WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 56 RUSSIA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 57 RUSSIA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 58 CZECH REPUBLIC WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 59 CZECH REPUBLIC WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 60 ROMANIA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 61 ROMANIA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 62 REST OF EASTERN EUROPE WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 63 REST OF EASTERN EUROPE WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 64 WESTERN EUROPE WHEELED HUMANOID ROBOTS CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 65 GERMANY WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 66 GERMANY WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 67 FRANCE WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 68 FRANCE WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 69 UK WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 70 UK WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 71 SPAIN WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 72 SPAIN WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 73 ITALY WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 74 ITALY WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 75 REST OF WESTERN EUROPE WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 76 REST OF WESTERN EUROPE WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 77 EAST ASIA AND PACIFIC WHEELED HUMANOID ROBOTS CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 78 CHINA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 79 CHINA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 80 JAPAN WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 81 JAPAN WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 82 AUSTRALIA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 83 AUSTRALIA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 84 CAMBODIA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 85 CAMBODIA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 86 FIJI WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 87 FIJI WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 88 INDONESIA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 89 INDONESIA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 90 SOUTH KOREA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 91 SOUTH KOREA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 92 REST OF EAST ASIA AND PACIFIC WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 93 REST OF EAST ASIA AND PACIFIC WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 94 SEA AND SOUTH ASIA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 95 BANGLADESH WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 96 BANGLADESH WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 97 NEW ZEALAND WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 98 NEW ZEALAND WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 99 INDIA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 100 INDIA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 101 SINGAPORE WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 102 SINGAPORE WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 103 THAILAND WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 104 THAILAND WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 105 TAIWAN WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 106 TAIWAN WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 107 MALAYSIA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 108 MALAYSIA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 109 REST OF SEA AND SOUTH ASIA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 110 REST OF SEA AND SOUTH ASIA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 111 MIDDLE EAST AND AFRICA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 112 GCC COUNTRIES WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 113 GCC COUNTRIES WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 114 SAUDI ARABIA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 115 SAUDI ARABIA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 116 UAE WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 117 UAE WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 118 BAHRAIN WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 119 BAHRAIN WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 120 KUWAIT WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 121 KUWAIT WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 122 OMAN WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 123 OMAN WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 124 QATAR WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 125 QATAR WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 126 EGYPT WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 127 EGYPT WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 128 NIGERIA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 129 NIGERIA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 130 SOUTH AFRICA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 131 SOUTH AFRICA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 132 ISRAEL WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 133 ISRAEL WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 134 REST OF MEA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 135 REST OF MEA WHEELED HUMANOID ROBOTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 136 U. S. MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 137 U. S. MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 138 CANADA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 139 CANADA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 140 MEXICO MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 141 MEXICO MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 142 CHINA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 143 CHINA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 144 JAPAN MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 145 JAPAN MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 146 INDIA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 147 INDIA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 148 SOUTH KOREA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 149 SOUTH KOREA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 150 SAUDI ARABIA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 151 SAUDI ARABIA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 152 UAE MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 153 UAE MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 154 EGYPT MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 155 EGYPT MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 156 NIGERIA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 157 NIGERIA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 158 SOUTH AFRICA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 159 SOUTH AFRICA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 160 GERMANY MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 161 GERMANY MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 162 FRANCE MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 163 FRANCE MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 164 UK MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 165 UK MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 166 SPAIN MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 167 SPAIN MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 168 ITALY MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 169 ITALY MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 170 BRAZIL MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 171 BRAZIL MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 172 ARGENTINA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 173 ARGENTINA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 174 COLUMBIA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 175 COLUMBIA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 176 GLOBAL WHEELED HUMANOID ROBOTS CURRENT AND FUTURE MARKET KEY COUNTRY LEVEL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 177 FINANCIAL OVERVIEW:

Key Players Analysis

SoftBank Robotics: Pepper and related social/service robots use a wheeled base and target retail, hospitality and reception markets; strong brand, large installed base and mature developer ecosystem.

UBTECH Robotics: Major consumer/service-robot manufacturer from China with compact interactive humanoids and education/service models (some wheeled or hybrid designs); strong distribution in APAC.

Aeolus Robotics: Developer of Aeo (dual-arm mobile humanoid/service robot) targeting security, delivery and facility services; emphasizes manipulation, human-height form factor and on‑site pilots.

Figure (Figure AI): Well‑funded humanoid robotics startup (large Series B in 2024) focusing on accelerating general‑purpose humanoid development for warehouses and commercial tasks.

Tesla (Optimus): High‑profile program aimed at general‑purpose humanoids with mass‑production ambitions; public roadmap claims commercialization targets and strong vertical integration with Tesla manufacturing.

Agility Robotics: Known for Digit (logistics‑focused humanoid) and strong emphasis on warehouse/mobile manipulation workflows; active in pilots for material handling and automation.

Sanctuary AI: Developing general‑purpose humanoids (Phoenix series) aimed at industrial and commercial work; emphasizes human‑level manipulation, safety and deployed pilot projects.

Halodi Robotics: Builds human‑safe humanoid platforms with compliant actuation and industry safety features targeted at human environments (service, security, care); emphasizes safe interaction and robustness.

Apptronik: Focused on general‑purpose humanoid systems and human‑robot collaboration (notably research partnerships including space/industry); emphasizes ruggedness and payload capability.

Engineered Arts (Ameca): Ameca is a highly expressive humanoid used primarily for R&D, demonstrations and human‑robot interaction research; commonly used as a research/demo platform in labs and public showcases.

Market Key Players

SoftBank Robotics

UBTECH Robotics

Aeolus Robotics

Figure (Figure AI)

Tesla (Optimus)

Agility Robotics

Sanctuary AI

Halodi Robotics

Apptronik

Engineered Arts (Ameca)

Drivers

Labor shortages & rising demand for automation

Aging populations in developed markets and chronic labor shortages in sectors like logistics, retail and healthcare are creating urgent, recurring needs that wheeled humanoid robots can address. Businesses facing high turnover, rising wages and difficulty filling repetitive or physically demanding roles see wheeled humanoids as a way to maintain productivity (they can operate long shifts, don’t require benefits, and reduce reliance on temporary labor). Because wheeled humanoids combine human‑oriented manipulation and interaction with efficient flat‑surface mobility, they map well to tasks such as in‑facility deliveries, front‑desk service, shelf stocking and basic caregiving—roles that are costly and time‑consuming to staff. The result is stronger buyer interest and more pilots from end users seeking deterministic ROI from automation, accelerating vendor investment and commercialization efforts.

AI, sensing and hardware improvements lowering capability/cost barriers

Rapid advances in perception (computer vision, sensor fusion), path planning, manipulation algorithms and compact power systems have materially improved real‑world performance and lowered the marginal cost of capability. Better onboard compute, pretrained embodied models and smaller, cheaper lidar/camera arrays enable wheeled humanoids to navigate crowded, dynamic indoor environments and grasp everyday objects with far higher reliability than a few years ago. Simultaneously, battery and actuator improvements boost usable runtime and payload, while economies of scale in electronics reduce BOM costs. These technology improvements shrink the gap between proof‑of‑concept demos and production‑grade systems, making purchases more defensible from an operational perspective and enabling software + service business models (updates, fleet management) that further reduce perceived risk for buyers.

Restraints

High upfront cost and integration complexity

The sticker price for capable humanoid platforms—coupled with customization, systems integration, facility adaptation and workforce training—makes total cost of ownership (TCO) high, especially for small and medium enterprises. Deployment is rarely plug‑and‑play: robots must be integrated into workflows, IT systems, safety zones and maintenance programs, and often require changes to physical layouts, shelving or interfaces. These one‑time and recurring expenses lengthen payback periods and increase procurement friction; procurement committees and finance teams may require extensive pilot evidence and long trials before committing to fleet purchases. For many buyers, alternative automation (simpler AMRs, conveyors, or human re‑allocation) can offer faster, lower‑risk ROI, slowing broader market penetration.

Safety, liability and regulatory uncertainty for human‑facing robots

When wheeled humanoids operate near people—carrying items, opening doors, or interacting with vulnerable groups like patients or the elderly—manufacturers and deployers face complex safety, insurance and legal questions. Standards and certification frameworks for human‑robot interaction are still evolving across jurisdictions; without clear regulatory guidance, vendors must over‑engineer systems for conservative safety, raising cost and slowing timetables. Liability questions (who’s responsible if a robot injures someone or damages property), privacy concerns (audio/video sensing in public and private spaces), and the need for predictable fail‑safe behaviors all contribute to cautious procurement policies from large institutions (hospitals, schools) and regulatory scrutiny that can delay commercial rollouts.

Opportunities

Healthcare, eldercare and in‑home assistance at scale

Demographic trends create a sustained, large addressable market for wheeled humanoids that can support caregiving tasks: medication delivery, remote telepresence with clinicians, mobility assistance, routine monitoring, and social/companion functions. Robots that can navigate homes and care facilities, manipulate everyday objects, and safely interact with frail users can reduce caregiver burden, extend independent living for older adults, and lower operational costs in long‑term care. Because these are high‑pain, high‑value problems, healthcare providers and insurers may fund pilots or reimbursement models that accelerate adoption; successful clinical pilots and clear evidence of safety and improved outcomes would unlock broader procurement and recurring service revenues.

Logistics, facility services and customer‑facing roles (scale pilots → production)

Structured indoor environments—warehouses, hotels, hospitals and retail stores—are highly compatible with wheeled humanoid designs: smooth floors, predictable layouts and repeatable tasks (deliveries, shelf replenishment, reception) simplify navigation and reduce edge‑case risk. Once pilots demonstrate consistent uptime and ROI, the business case shifts from one‑off purchases to fleets plus ongoing service contracts (maintenance, software updates, fleet orchestration). This fleet model enables scale economics (lower unit CAPEX, centralized learning from deployed robots) and recurring revenue for vendors, while end users benefit from reduced labor cost volatility and improved service consistency.

Threats

Competition from alternative platforms and solution consolidation

Many tasks targeted by wheeled humanoids can be served by cheaper or more mature alternatives: autonomous mobile robots (AMRs) for material transport, fixed automation/robotic arms for repetitive manipulation, or teleoperated systems for remote assistance. Large incumbents—cloud providers, industrial robot suppliers or e‑commerce giants—may bundle robotics into broader automation stacks and capture customers through integrated offers, undercutting specialized humanoid vendors. If buyers conclude that hybrid solutions (AMR + arm, ceiling conveyors + simple robots) meet performance needs at lower cost, demand for humanoid platforms could be limited to niche verticals, fragmenting the market and compressing vendor margins.

Economic cycles, procurement cycles and public acceptance risks

Capital‑intensive projects are sensitive to macroeconomic conditions; recessions, tighter corporate budgets or longer internal procurement cycles can delay or cancel robot purchases. Beyond finance, public sentiment and workforce reactions matter: high‑profile mishaps, privacy controversies or perceived job displacement could trigger negative press, protests, or stricter local rules that slow adoption. Even when technology and cost align, social acceptance, union negotiations and institutional conservatism can lengthen pilot phases and reduce the speed of scale deployments—making commercial success contingent not just on engineering but on policy, PR and stakeholder engagement.

Recent Developments

In Feb 2024 — Figure (humanoid startup) raised $675M Series B (major investors: Microsoft, NVIDIA, OpenAI Startup Fund, Jeff Bezos, others); announced collaboration with OpenAI and commercial acceleration plans.

In Apr 2024: Tesla / Optimus timeline comments: Elon Musk said Optimus humanoid “could be on sale by end of 2025” / limited internal production predicted — a high‑visibility signal from an OEM that influences investor & industry expectations:

In Apr 2024: Boston Dynamics unveiled a new all‑electric Atlas (retiring the hydraulic Atlas), positioning Atlas toward commercial/hyper‑industrial pilots (Hyundai named as early partner/test site):

In Apr 2024: Sanctuary AI announced pilots/partnership activity with Magna (automotive production use‑case for humanoids): (reported in market coverage noting March–April 2024 partnership activity)

In Mar 2024 (reported in 2024 market coverage): Agility Robotics (Digit) started moving beyond pilots with commercial warehouse/production integrations and announced partnerships (e.g., integration projects with supply‑chain partners): cited in industry reports and news roundups:

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

Platform(Indoor Navigation Platforms, Outdoor/Last-Mile Delivery Platforms, Cloud-Based Control Systems)End-User Industry (Healthcare, Logistics, Hospitality, Retail, Education & Research) Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

Platform(Indoor Navigation Platforms, Outdoor/Last-Mile Delivery Platforms, Cloud-Based Control Systems)End-User Industry (Healthcare, Logistics, Hospitality, Retail, Education & Research) Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

Platform(Indoor Navigation Platforms, Outdoor/Last-Mile Delivery Platforms, Cloud-Based Control Systems)End-User Industry (Healthcare, Logistics, Hospitality, Retail, Education & Research) Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

Platform(Indoor Navigation Platforms, Outdoor/Last-Mile Delivery Platforms, Cloud-Based Control Systems)End-User Industry (Healthcare, Logistics, Hospitality, Retail, Education & Research) Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")