- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Wireline Services Market Size, Share & Forecast 2034 | CAGR 7.4%

Global Wireline Services Market Size, Share, Analysis By Service Type (Logging Services, Perforation Services, Pipe Recovery & Mechanical Services, Slickline Intervention, Memory Logging & Other Services), By Wireline Type (Electric Line Services, Slickline Services, Braided Line Services), By Hole Type (Cased-Hole Wireline Services, Open-Hole Wireline Services), By Application (Onshore Wireline Services, Offshore Wireline Services) Industry Region & Key Players–Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026–2034

Report Overview

| Market Size, 2025 | Forecast Value, 2034 | CAGR, 2026-2034 | Leading Region, 2025 |

| USD 10.4 Billion | USD 19.7 Billion | 7.4% | North America, 30.0% |

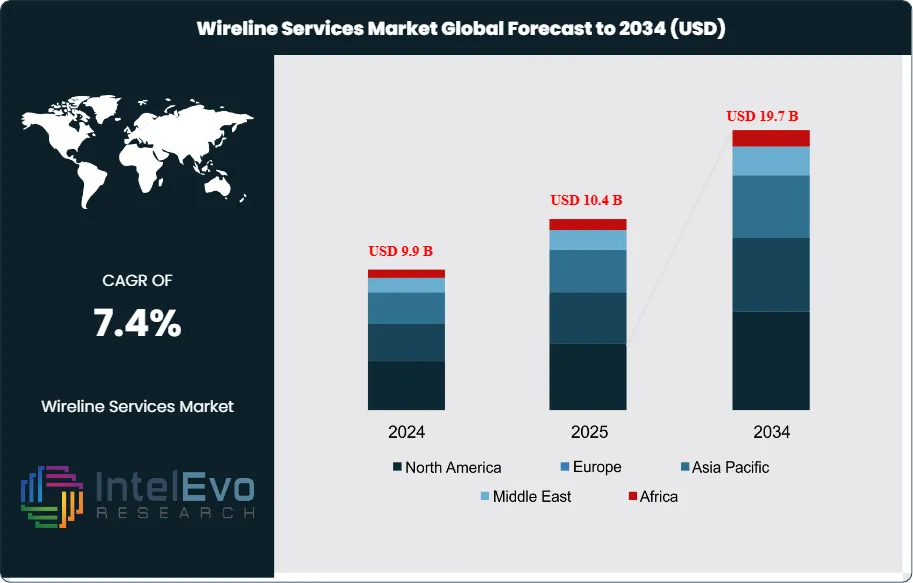

The Wireline Services Market was valued at USD 9.9 billion in 2024 and is projected to reach approximately USD 10.4 billion in 2025. The market is further expected to expand to nearly USD 19.7 billion by 2034, registering a compound annual growth rate (CAGR) of about 7.4% during the forecast period from 2026 to 2034. The Wireline Services Market is expanding because operators continue to prioritize reservoir evaluation, cased-hole diagnostics, perforation accuracy, production logging, and lower-cost intervention across mature and newly developed wells. Current market references support a 2025 global market around the low-USD 10 billion range, with one recent source estimating USD 10.4 Billion in 2025 and another placing the market at USD 11.14 Billion in 2025 under a more conservative growth profile. This report uses the first benchmark as the base scenario because it aligns more closely with current offshore, intervention, and diagnostic activity trends.

Get More Information about this report -

Request Free Sample ReportThe Wireline Services Market is closely tied to the mix of drilling, completion, production optimization, and well intervention work. Demand is strongest in mature fields, offshore developments, shale basins with high well counts, and brownfield programs where operators need frequent diagnostics without moving a drilling rig. North America remains the largest demand center because U.S. crude production stayed near a record 13.6 million barrels per day in 2025, while Federal Offshore Gulf of America crude production remained around 1.8–2.0 million barrels per day during 2025. Those volumes support recurring logging, perforation, production logging, and slickline activity. At the same time, Middle East upstream investment remains a major tailwind, with the IEA estimating about USD 130 Billion in oil and gas supply investment in 2025 across the region.

The Wireline Services Market also benefits from stricter safety and technical controls. BSEE states that its offshore regulatory programs include the Well Control Rule and related regulations designed to promote safety, protect the environment, and conserve resources. In offshore intervention environments, wireline lubricators, pressure-control heads, and well-control packages remain essential parts of intervention system design. These requirements keep barriers to entry high and favor companies with proven pressure-control equipment, offshore operating systems, and strong procedural discipline.

Technology is shifting the market toward higher-value services. Halliburton launched the Intelli portfolio of wireline-conveyed diagnostic well intervention services in December 2024. SLB launched the OnWave autonomous logging platform in July 2025 and acquired Stimline Digital in August 2025 to deepen well intervention software capability. Baker Hughes later secured work in Kuwait linked to advanced wireline, perforation, and Proxima advanced logging services. Weatherford added a four-year wireline services contract in Romania in early 2026. These developments show that automation, digital interpretation, autonomous logging, and integrated intervention workflows are lifting the value of the Wireline Services Market beyond conventional logging alone.

Risk remains present. Tariffs and equipment-cost pressure continue to affect service providers, and Baker Hughes warned in April 2025 that tariffs could reduce full-year core profit by USD 100 million to USD 200 million. Even so, the Wireline Services Market should maintain firm growth because wireline remains one of the fastest and lowest-footprint ways to gather downhole data, restore flow, and diagnose production issues across the life of the well.

, By Wireline Type (Electric Line Services, Slickline Services, Braided Line Services), By Hole Type (Cased-Hole Wireline Services, Open-Hole Wireline Services), By Application (Onshore Wireline Services, Offshore Wireline Services) Industry Region & Key Players–Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The Wireline Services Market was valued at USD 10.4 Billion, 2025 and is projected to reach USD 19.7 Billion, 2034, at a 7.4% CAGR during 2026–2034. Recent market references also place the sector in a similar 2025 range, with another estimate at USD 11.14 Billion, 2025.

- Segment Dominance: By service type, logging services led with 36.0% share, 2025, equal to USD 3.7 Billion, 2025. This segment leads because formation evaluation, production logging, and cased-hole diagnostics remain the core use cases for wireline fleets.

- Segment Dominance: By application, onshore wireline services held 59.0% share, 2025, equal to USD 6.1 Billion, 2025. Large shale and mature-field well counts keep land demand above offshore activity, even though offshore work carries higher revenue per job.

- Driver: The main driver is rising mature-field intervention and production optimization. Halliburton’s Brazil intervention award in 2024 covered nearly two-thirds of Petrobras’ offshore interventions and plug and abandonment work, showing the scale of intervention-led wireline demand.

- Restraint: The main restraint is equipment-cost and tariff pressure. Baker Hughes said tariffs could cut 2025 core profit by USD 100 million to USD 200 million, highlighting how service margins remain exposed to trade friction.

- Opportunity: The largest opportunity is autonomous and digital wireline evaluation. SLB launched OnWave in July 2025, and broader digital well-optimization trends across the sector are supporting more remote and software-led intervention workflows.

- Trend: The clearest trend is integration of wireline with advanced intervention diagnostics. Halliburton launched Intelli in December 2024, and Baker Hughes’ Kuwait award in 2025 included Proxima advanced logging and perforation services.

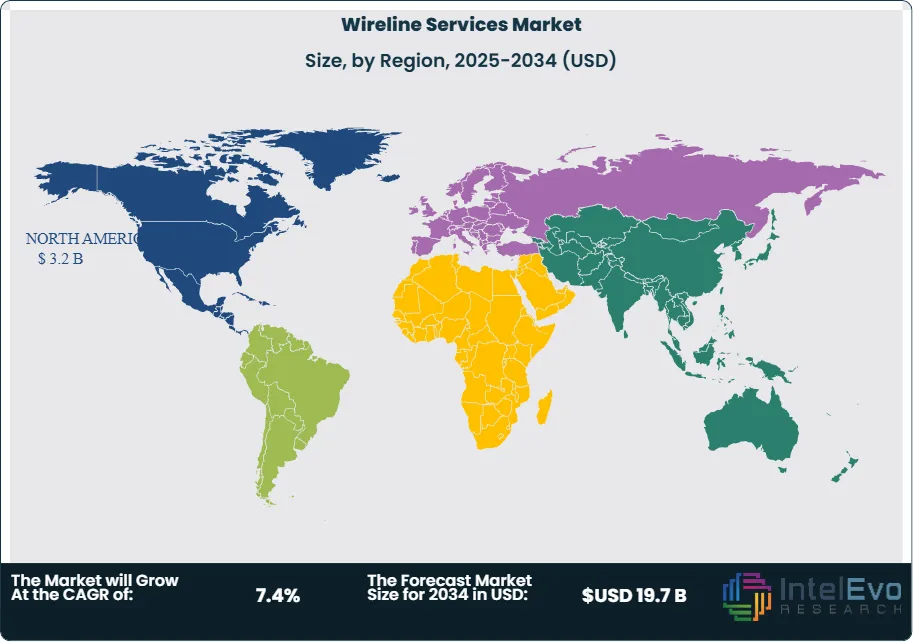

- Regional Analysis: North America led the Wireline Services Market with 31.0% share, 2025, equal to USD 3.2 Billion, 2025. Record U.S. production and a large installed well base support recurring wireline demand.

Competitive Landscape

The Wireline Services Market is moderately consolidated. The top four companies, SLB, HALLIBURTON, BAKER HUGHES, and WEATHERFORD, held an estimated 47.0% of global revenue in 2025. Competition is technology-driven in offshore and diagnostic work, but price and fleet availability still matter in land markets. Competitive intensity increased materially from late 2024 through early 2026 as Halliburton introduced Intelli, SLB launched OnWave and acquired Stimline Digital, Baker Hughes expanded advanced wireline work in Kuwait, and Weatherford won long-duration wireline contracts in Romania and Turkey.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| SLB | US | Leader | OnWave autonomous logging platform | Middle East, Latin America, offshore global | Launched OnWave in Jul 2025 and acquired Stimline Digital in Aug 2025 to deepen wireline and intervention software capability. |

| HALLIBURTON | US | Leader | Intelli wireline diagnostic suite | North America, Latin America, Middle East | Introduced Intelli in Dec 2024 and expanded offshore Brazil intervention and completion presence into 2025. |

| BAKER HUGHES | US | Leader | Proxima advanced logging services | Middle East, North America, offshore global | Secured a 2025 Kuwait award for advanced wireline, perforation, and logging services. |

| WEATHERFORD | US | Leader | Open Hole Wireline Tools / Wireline Services | Europe, Middle East, Latin America | Added a four-year Romania wireline services contract in Feb 2026 and a five-year open-hole wireline tools contract in Turkey in 2025. |

| EXPRO | US/UK operational base | Challenger | Slickline and intervention services | Asia Pacific, Gulf of America, Europe | Reported 2025 revenue of USD 1,607 million and maintained intervention-heavy contract momentum into 2026. |

| ARCHER | Bermuda | Challenger | Platform drilling and wireline services | Europe, North Sea | Continued strong North Sea intervention and platform-well service positioning through 2025. |

| CASEDHOLE SOLUTIONS | US | Niche Player | Cased-hole wireline and perforating services | North America | Maintained U.S. land-focused diagnostic and perforating market presence through 2025. |

| ALTUS INTERVENTION | Norway | Niche Player | Wireline and well intervention services | Europe | Continued North Sea wireline and intervention specialization through 2025. |

| CORE LABORATORIES | Netherlands/US | Niche Player | Reservoir and production diagnostic services | North America, Middle East | Continued reservoir diagnostics and production-evaluation work relevant to wireline-led surveillance through 2025. |

| WELLTEC | Denmark | Niche Player | Intervention and conveyance technologies | Europe, Middle East | Continued expansion of intervention technology deployment in offshore and mature-field applications through 2025. |

By Service Type

Logging services held the largest share of the Wireline Services Market at 36.0%, 2025, equal to USD 3.7 Billion, 2025. This segment leads because open-hole logging, cased-hole evaluation, production logging, and surveillance remain the basic information layer for reservoir decisions and mature-field diagnostics. Perforation services accounted for 29.0%, 2025, or USD 3.0 Billion, 2025, supported by completion and recompletion demand in both land and offshore wells. Pipe recovery and mechanical services represented 18.0%, 2025, equal to USD 1.9 Billion, 2025, while slickline-led intervention, memory logging, and other specialty services made up 17.0%, 2025, or USD 1.8 Billion, 2025. The service mix shows why large integrated providers still dominate. Logging creates the broadest recurring demand, but perforation and mechanical work often deliver higher margins in intervention-heavy wells. Halliburton’s Intelli release and Baker Hughes’ Kuwait work both point to stronger demand for diagnostic-led service bundles rather than isolated runs. SLB’s OnWave platform reinforces the same direction by reducing human dependence in data acquisition and improving measurement reliability in difficult well conditions.

By Wireline Type

Electric line services led with 48.0% share, 2025, equal to USD 5.0 Billion, 2025. Electric line remains dominant because it supports real-time data transmission, advanced formation evaluation, cased-hole logging, and powered intervention tools. Slickline services held 34.0%, 2025, or USD 3.5 Billion, 2025. That segment remains essential in mechanical intervention, valve shifting, gauge deployment, memory tools, and lower-cost well maintenance. Braided line services represented 18.0%, 2025, equal to USD 1.9 Billion, 2025, filling the gap where heavier mechanical loads, fishing, or more rugged intervention conditions are present. The competitive structure differs by type. Electric line is more technology intensive and favors companies with proprietary logging platforms, while slickline remains more fragmented because smaller regional players can still compete. Even so, digitalization is changing the balance. Halliburton’s Intelli suite, SLB’s OnWave platform, and Weatherford’s contract activity in open-hole wireline show that higher-value electric-line and hybrid intervention work are gaining share faster than simple mechanical slickline jobs. As the industry pushes toward autonomous logging and intervention data integration, electric line should continue to widen its share lead through 2034.

By Hole Type

Cased-hole wireline services accounted for 54.0% share, 2025, equivalent to USD 5.6 Billion, 2025. This segment leads because most mature-field intervention, production logging, casing inspection, pulsed-neutron work, and mechanical wireline operations occur after the well has already been cased and completed. Open-hole wireline services held 46.0%, 2025, or USD 4.8 Billion, 2025. Open-hole remains critical in exploration, appraisal, reservoir characterization, and petrophysical evaluation, but its market share is lower because it is tied more closely to drilling campaigns than recurring intervention cycles. The difference between these segments helps explain the market’s resilience. Cased-hole work supports recurring revenue through the life of the well, while open-hole activity rises and falls more directly with drilling intensity. That is why intervention-heavy regions and brownfield programs remain important. Halliburton’s December 2024 Intelli launch focused squarely on diagnostic well intervention. Weatherford’s 2025 Turkey award for open-hole wireline tools shows that open-hole still matters, but it is cased-hole surveillance and intervention that keep fleets working between drilling peaks. The strongest long-term growth sits where cased-hole diagnostics are integrated with production optimization and remedial planning.

By Application

Onshore wireline services held 59.0% share, 2025, equal to USD 6.1 Billion, 2025. This segment leads because land well counts are far higher than offshore well counts, especially in North America, the Middle East, and selected unconventional and mature-field areas. Onshore work includes open-hole evaluation, cased-hole intervention, perforation, production logging, and slickline maintenance across very large well populations. Offshore wireline services represented 41.0%, 2025, or USD 4.3 Billion, 2025. Offshore carries lower job volume but higher average revenue per operation because mobilization, pressure-control requirements, subsea access, and safety barriers are stricter. Offshore also benefits more from diagnostic-led interventions because the cost of failure or unnecessary rigless work is higher. The application mix shows a familiar pattern. Land work supports volume and fleet utilization. Offshore work supports premium technology, stronger pricing, and higher-value service integration. That is why SLB, Halliburton, Baker Hughes, and Weatherford remain strongest in offshore and international work, even while regional players can still compete aggressively in simpler land operations.

Regional Analysis

North America Wireline Services Market Regional Analysis

North America held 31.0% share, 2025, equal to USD 3.2 Billion, 2025. The United States dominates the region, followed by Canada, Mexico, and the Rest of North America. The region leads because it combines a massive installed well base, frequent intervention cycles, strong shale activity, and broad availability of cased-hole, slickline, perforation, and production-logging crews. U.S. crude production stayed near a record 13.6 million barrels per day in 2025, while monthly Federal Offshore Gulf of America output stayed broadly around 1.8–2.0 million barrels per day through the year. Those volumes support both land and offshore wireline demand. Canada adds mature-field logging and intervention demand across conventional and thermal operations, while Mexico contributes offshore and brownfield service demand. North America also remains highly competitive. SLB, Halliburton, Baker Hughes, Weatherford, Expro, Casedhole Solutions, and many regional specialists all operate here. The main growth limit is pricing pressure in land service markets. The main strength is recurring activity. Even when drilling slows, the installed well base keeps intervention and surveillance demand alive.

Europe Wireline Services Market Regional Analysis

Europe accounted for 15.0% share, 2025, equal to USD 1.6 Billion, 2025. The UK, Norway, Germany, and Romania are the most relevant countries, though the North Sea remains the real commercial anchor. Europe is a high-value region because offshore diagnostics, intervention, and well-integrity work carry strong technical requirements and high service intensity. Norway and the UK lead due to mature offshore assets and a large installed base of producing wells that require surveillance and intervention. Germany contributes more through engineering and service infrastructure than through field scale. Romania became more relevant in 2026 after Weatherford reported a four-year wireline services contract and a separate four-year wireline perforation and mechanical services contract there. Europe’s operating environment also favors experienced intervention providers because offshore work is governed by strict safety and environmental controls. Archer, Altus Intervention, SLB, Halliburton, Weatherford, and Expro all remain active in the regional mix. Europe will not match North America on total volume, but it remains one of the highest-value markets per job because mature offshore wells need repeated wireline-led evaluation and remediation.

Asia Pacific Wireline Services Market Regional Analysis

Asia Pacific captured 19.0% share, 2025, equal to USD 2.0 Billion, 2025. China, Japan, India, and Australia are the most relevant countries, followed by the Rest of Asia Pacific. China drives the region through broad upstream activity and a large land and offshore asset base. India adds recurring wireline demand through mature fields and offshore programs, while Australia supports premium offshore and gas-focused intervention activity. Japan matters more through technology and engineering participation than field scale. Asia Pacific’s mix favors both open-hole logging and cased-hole intervention, especially in offshore gas and mature oil developments. The region also benefits from strong international operator presence and growing digital adoption. The main challenge is uneven service pricing and localization across markets. The main opportunity is offshore gas and brownfield optimization, where wireline diagnostics can improve recovery at lower cost than full workovers. Asia Pacific should outgrow Europe in absolute market expansion through 2034 because of its broader upstream runway and rising intervention complexity.

Latin America Wireline Services Market Regional Analysis

Latin America held 11.0% share, 2025, equal to USD 1.1 Billion, 2025. Brazil dominates the region, followed by Mexico, Argentina, and the Rest of Latin America. Brazil is the main market because deepwater intervention, completions, and production diagnostics remain heavily service intensive. Halliburton’s Brazil intervention contract, announced in 2024 and set to begin in 2025, covers nearly two-thirds of Petrobras’ offshore interventions and plug and abandonment work. Petrobras also awarded Halliburton deepwater completion and stimulation contracts in October 2025, while SLB secured an USD 800 million integrated offshore services award in December 2024 tied to more than 100 deepwater wells. Those moves confirm that Brazil is one of the strongest global markets for premium wireline and intervention activity. Mexico remains a secondary offshore market, while Argentina adds land-based intervention and logging demand. Latin America’s core growth driver is offshore complexity rather than sheer well count. That favors SLB, Halliburton, Baker Hughes, Weatherford, and Expro over smaller regional providers. The key risk is that spending can move in large award cycles, making yearly growth less smooth than long-term demand suggests.

Middle East & Africa Wireline Services Market Regional Analysis

Middle East & Africa represented 24.0% share, 2025, equal to USD 2.5 Billion, 2025. Saudi Arabia, the UAE, South Africa, and the Rest of MEA define the region, though Gulf producers account for most demand. The IEA estimates that the Middle East will invest about USD 130 Billion in oil and gas supply in 2025, with Saudi Arabia alone at about USD 40 Billion of upstream oil and gas investment. This level of capital flow supports both drilling-related open-hole logging and large volumes of cased-hole intervention, production logging, perforation, and slickline maintenance. Saudi Arabia and the UAE lead the market due to scale, gas expansion, and long-life producing assets. South Africa remains a strategic coverage point more than a current revenue leader. The region is especially attractive for wireline services because large NOCs often sustain multi-year service relationships. Baker Hughes’ 2025 Kuwait award for advanced wireline and logging work, although technically in the broader Gulf, underscores the scale of regional opportunity. Weatherford, SLB, Halliburton, and Baker Hughes all remain highly exposed here. Middle East & Africa should be one of the fastest-growing markets through 2034 because recurring intervention needs remain high even when drilling activity fluctuates.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Service Type

- Logging Services

- Perforation Services

- Pipe Recovery and Mechanical Services

- Slickline Intervention, Memory Logging, and Other Services

By Wireline Type

- Electric Line Services

- Slickline Services

- Braided Line Services

By Hole Type

- Cased-Hole Wireline Services

- Open-Hole Wireline Services

By Application

- Onshore Wireline Services

- Offshore Wireline Services

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 10.4 B |

| Forecast Revenue (2034) | USD 19.7 B |

| CAGR (2025-2034) | 7.4% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Service Type (Logging Services, Perforation Services, Pipe Recovery and Mechanical Services, Slickline Intervention, Memory Logging, and Other Services), By Wireline Type (Electric Line Services, Slickline Services, Braided Line Services), By Hole Type (Cased-Hole Wireline Services, Open-Hole Wireline Services), By Application (Onshore Wireline Services, Offshore Wireline Services) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | SLB, HALLIBURTON, BAKER HUGHES, WEATHERFORD, EXPRO, ARCHER, CASEDHOLE SOLUTIONS, ALTUS INTERVENTION, CORE LABORATORIES, WELLTEC, SUPERIOR ENERGY SERVICES, OIL STATES, GEODYNAMICS, NOV, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Wireline Type (Electric Line Services, Slickline Services, Braided Line Services), By Hole Type (Cased-Hole Wireline Services, Open-Hole Wireline Services), By Application (Onshore Wireline Services, Offshore Wireline Services) Industry Region & Key Players–Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026–2034")

, By Wireline Type (Electric Line Services, Slickline Services, Braided Line Services), By Hole Type (Cased-Hole Wireline Services, Open-Hole Wireline Services), By Application (Onshore Wireline Services, Offshore Wireline Services) Industry Region & Key Players–Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026–2034")

, By Wireline Type (Electric Line Services, Slickline Services, Braided Line Services), By Hole Type (Cased-Hole Wireline Services, Open-Hole Wireline Services), By Application (Onshore Wireline Services, Offshore Wireline Services) Industry Region & Key Players–Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Wireline Services Market?

Global Wireline Services Market was valued at USD 9.9 billion in 2024 and is projected to reach USD 19.7 billion by 2034, growing at a CAGR of 7.4%. Explore key trends, offshore drilling demand, well intervention services, and oilfield technology growth.

Who are the major players in the Wireline Services Market?

SLB, HALLIBURTON, BAKER HUGHES, WEATHERFORD, EXPRO, ARCHER, CASEDHOLE SOLUTIONS, ALTUS INTERVENTION, CORE LABORATORIES, WELLTEC, SUPERIOR ENERGY SERVICES, OIL STATES, GEODYNAMICS, NOV, Others

Which segments covered the Wireline Services Market?

By Service Type (Logging Services, Perforation Services, Pipe Recovery and Mechanical Services, Slickline Intervention, Memory Logging, and Other Services), By Wireline Type (Electric Line Services, Slickline Services, Braided Line Services), By Hole Type (Cased-Hole Wireline Services, Open-Hole Wireline Services), By Application (Onshore Wireline Services, Offshore Wireline Services)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date