- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Women’s Health Market Size, Share & Growth Forecast | 5.6% CAGR

Global Women’s Health Market Size, Share & Analysis By Health Conditions (Gynecological Conditions, Mental Health, Cardiovascular Health, Maternal Health, Other Health Conditions), By Age Group (Adolescents, Adult Women, Elderly Women) Industry Regions & Key Players – Healthcare Access Trends & Forecast 2025–2034

Report Overview

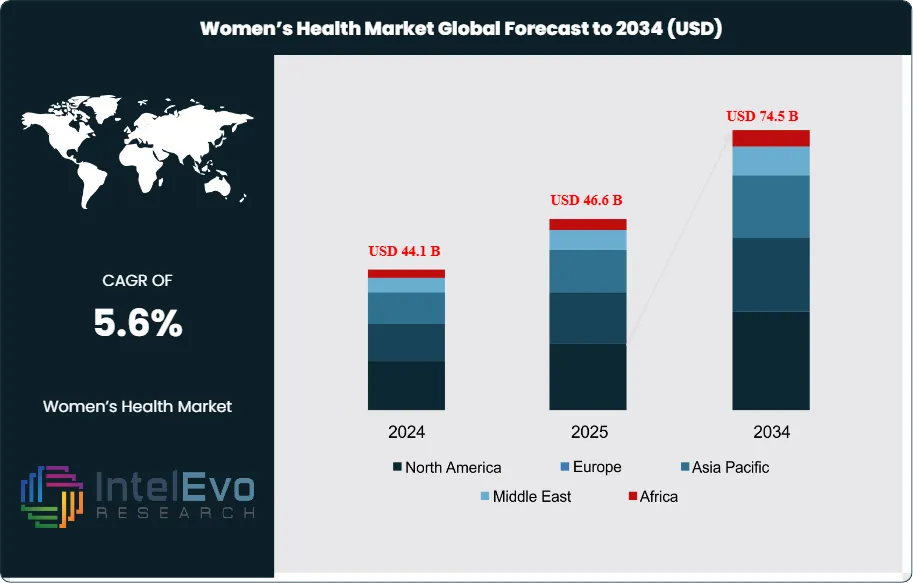

The Women’s Health Market is projected to rise from USD 44.1 Billion in 2024 to approximately USD 74.5 Billion by 2034, growing at a CAGR of around 5.6% during 2025–2034. Rising focus on preventive care and early diagnostics is significantly boosting investment in women-focused healthcare solutions. Digital health platforms, generative AI in diagnostics, and telehealth services are expanding access to personalized care worldwide. Growing awareness, supportive government policies, and innovation in reproductive and hormonal wellness products are accelerating global market adoption.

Get More Information about this report -

Request Free Sample ReportThe market has evolved significantly as women’s healthcare needs take center stage in global health priorities. Government initiatives, regulatory oversight, and heightened awareness of gender-specific conditions are accelerating demand for advanced solutions targeting reproductive health, maternal care, and chronic disease management among women. Organizations such as the World Health Organization (WHO) and the U.S. Food and Drug Administration (FDA) continue to shape policy frameworks, ensuring access to safe, effective, and equitable healthcare. Early detection measures for breast cancer, supported by WHO studies, highlight the sector’s life-saving potential, with screening programs improving survival rates by up to 30% in certain regions.

Market momentum is further reinforced by robust capital flows from venture capital and private equity firms. More than USD 2 billion in investments over the past year have been directed toward fertility services, telemedicine, and personalized care platforms, confirming investor confidence in the sector’s innovation capacity. The intersection of women’s health with pharmaceuticals, medical devices, wellness solutions, and mental health care has broadened the ecosystem, driving new revenue streams and positioning the industry at the crossroads of healthcare and consumer well-being. Notably, targeted interventions in cardiovascular health have contributed to a 30% decline in heart disease among women over the past decade, underscoring tangible progress.

Technological innovation is playing a transformative role. The widespread adoption of telehealth, artificial intelligence, and wearable health devices is enabling more personalized, data-driven care. Nearly three-quarters of healthcare organizations now deploy AI to enhance diagnostics, predict health risks, and support remote monitoring. These advances are reshaping how women engage with healthcare, making solutions more inclusive and accessible.

Regionally, North America and Europe remain leading markets due to strong healthcare infrastructure and regulatory support, while Asia-Pacific is emerging as a high-growth destination, fueled by expanding healthcare access, urbanization, and greater awareness of women’s health needs. Despite progress, challenges persist including limited healthcare availability for 1.6 billion women worldwide and persistent gender bias in clinical research. Addressing these gaps represents both a societal imperative and a commercial opportunity for stakeholders across the global healthcare value chain.

, By Age Group (Adolescents, Adult Women, Elderly Women) Industry Regions & Key Players – Healthcare Access Trends & Forecast 2025–2034")

Key Takeaways

- Market Growth: The Women’s Health Market is projected to expand from USD 41.3 billion in 2023 to USD 66 billion by 2033, representing a robust CAGR of 4.8%, propelled by increased investment in preventive care and personalized healthcare solutions.

- Condition Type: Gynecological conditions hold the leading market position, accounting for over 37% of revenue, fueled by rising incidence rates and improvements in early diagnostic solutions.

- Age Group: Adult women represent the primary consumer segment, commanding more than 46% market share due to broad health needs spanning fertility, chronic disease management, and menopausal care.

- Driver: Proactive government and private sector initiatives, including breast cancer screening and maternal health programs, have elevated global awareness and accelerated the adoption of women’s health services.

- Restraint: Limited healthcare access for an estimated 1.6 billion women globally, coupled with persistent gender bias in clinical research, remains a significant barrier to market growth and equitable outcomes.

- Opportunity: The emergence of telehealth, wearable devices, and AI-powered diagnostics is unlocking new possibilities for remote, personalized healthcare delivery, particularly in underserved regions.

- Trend: There is a pronounced shift toward mental health integration in women’s healthcare, as holistic models increasingly acknowledge the interplay of physical and psychological well-being.

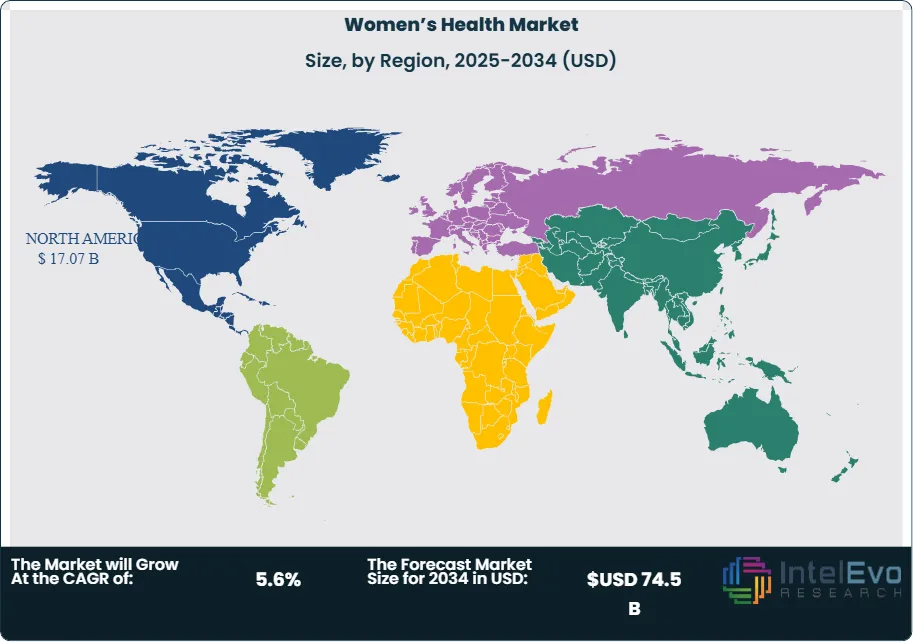

- Regional Analysis: North America leads with a 38.7% market share valued at USD 15.9 billion in 2023, backed by advanced healthcare systems and high consumer awareness, while Asia-Pacific is rapidly becoming a key investment hotspot due to expanding infrastructure and rising demand.

Health Conditions Analysis

The Women’s Health Market in 2025 demonstrates substantial segmentation according to distinct health conditions, with gynecological disorders such as ovarian cysts and uterine fibroids remaining the prevailing area of focus and accounting for over 37% of total market revenues . This leadership is primarily due to rising incidence rates and the widespread adoption of minimally invasive diagnostic and therapeutic approaches. Companies including Hologic, Bayer, and Boston Scientific are investing in advanced technologies, such as integrated imaging systems and hormonal therapies, to further improve patient outcomes.

Mental health continues to ascend as a priority within women’s healthcare, bolstered by increased societal acceptance and growing integration of mental health solutions into general wellness platforms . Mobile applications and telemedicine are now more frequently used for conditions such as depression and anxiety, reflecting a systemic shift toward accessible, stigma-free treatment. Simultaneously, cardiovascular health is rising in prominence as research increasingly highlights sex-specific risk factors and treatment complexities, prompting new initiatives around personalized care.

The maternal health segment further strengthens the market, with sustained attention to maternal morbidity, safe pregnancy outcomes, and innovative prenatal care models. Beyond these, areas such as osteoporosis and autoimmune conditions are gaining traction, powered by advances in prevention and early detection. Collectively, these segments underscore the need for strategic investment in female-specific health programs and policy reform, as the market acknowledges the diversity of women’s health needs

Age Group Analysis

The adult women demographic is projected to remain the leading segment in 2025, representing over 46% of market share owing to its broad spectrum of healthcare considerations, ranging from reproductive concerns to chronic and mental health management. Heightened awareness, enhanced healthcare delivery systems, and the rising incidence of non-communicable diseases underpin continued growth in this category. Corporate wellness initiatives and government awareness campaigns contribute to greater engagement with healthcare services.

Both adolescent and elderly women are experiencing marked growth in demand for tailored healthcare services. Targeted outreach and governmental policies focused on menstrual health and preventative care are positively impacting adolescents. In contrast, the growing elderly population is driving increased adoption of geriatric care, particularly for post-menopausal health challenges and chronic condition management. Companies are pivoting towards developing personalized solutions that address the evolving requirements of women throughout their life stages, reinforcing the market’s shift toward holistic care.

Regional Analysis

North America remains the most influential region in the global Women’s Health Market for 2025, maintaining a leadership position with more than 38.7% market share and a value surpassing USD 15.9 billion. The landscape is characterized by robust healthcare infrastructure, progressive regulatory environments, and persistent investment in biomedical research and innovation from leading organizations like Johnson & Johnson and Abbott Laboratories. Enhanced consumer trust and physician confidence result from strict evaluation standards and ongoing professional education.

The region’s market strength is further supported by focused initiatives from government bodies and non-profit organizations, which prioritize awareness, preventive care, and early intervention programs for women’s health concerns. As North America continues to advance in medical technology, increase household incomes, and experience demographic aging, the outlook for sustained market growth is positive. Still, emerging markets in Europe and Asia-Pacific, with expanding healthcare investments and changing population dynamics, are positioning themselves as increasingly competitive regions, providing new avenues for industry development and strategic expansion.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Health Conditions

- Gynecological Conditions

- Mental Health

- Cardiovascular Health

- Maternal Health

- Other Health Conditions

By Age Group

- Adolescents

- Adult Women

- Elderly Women

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2024) | USD 44.1 B |

| Forecast Revenue (2034) | USD 74.5 B |

| CAGR (2024-2034) | 5.6% |

| Historical data | 2020-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Health Conditions (Gynecological Conditions, Mental Health, Cardiovascular Health, Maternal Health, Other Health Conditions), By Age Group (Adolescents, Adult Women, Elderly Women) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Amgen Inc., Ferring B.V., Teva Pharmaceutical Industries Ltd., AbbVie Inc., Agile Therapeutics, Merck & Co. Inc., Blairex Laboratories Inc., Bayer AG, Pfizer Inc., Apothecus Pharmaceutical Corp., Other Key Player |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Age Group (Adolescents, Adult Women, Elderly Women) Industry Regions & Key Players – Healthcare Access Trends & Forecast 2025–2034")

, By Age Group (Adolescents, Adult Women, Elderly Women) Industry Regions & Key Players – Healthcare Access Trends & Forecast 2025–2034")

, By Age Group (Adolescents, Adult Women, Elderly Women) Industry Regions & Key Players – Healthcare Access Trends & Forecast 2025–2034")

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date