- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Zero-Waste Packaging Market Growth, Trends & Forecast | CAGR 9.15%

Global Zero-Waste Packaging Solutions Market Size, Share, Analysis Report By Material(Biopolymer, Paper and Cardboard, Glass Packaging, Metal Packaging), Type(Reusable/Recyclable Packaging, Compostable Packaging, Edible Packaging), Distribution Channel(Online, Offline), Application(Food & Beverages, Healthcare, Cosmetics & Personal Care, Electrical & Electronics, E-commerce, Others), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034

Report Overview:

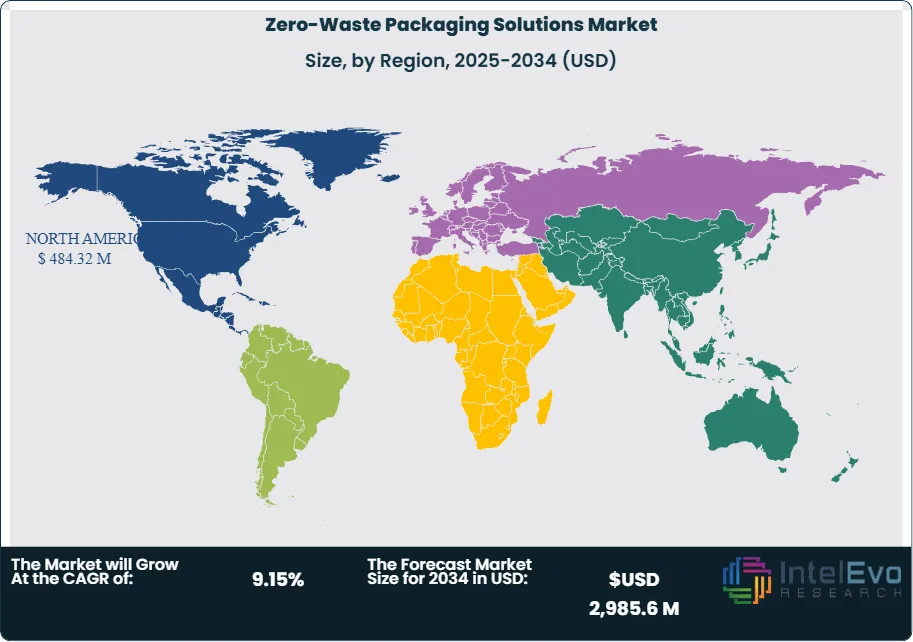

The Zero-Waste Packaging Solutions Market size is expected to be worth around USD 2,985.6 Million by 2034, up from USD 1,210.8 Million in 2024, growing at a CAGR of 9.15% during the forecast period from 2025 to 2034. This growth is fueled by increasing consumer awareness, stricter government regulations on plastic usage, and the rapid adoption of sustainable materials in food, retail, and e-commerce sectors. With major brands shifting toward eco-friendly alternatives, zero-waste packaging is emerging as a global megatrend, reshaping the future of packaging and sustainable supply chains.

Get More Information about this report -

Request Free Sample ReportZero-waste packaging refers to products created in such a manner that they are either recyclable and reusable or biodegradable, thereby not causing much waste and less damage to the environment. From all the drivers that have already impacted this market, it would appear the dynamics of this market have been changed by increasing awareness on environmental matters, regulatory pressure, and growing demand from customers for sustainable solutions. As a call from customers for reduction of carbon footprint, zero-waste packaging has become part of company strategies that drive a new wave in material and design innovation. Businesses are at present adopting these modern materials and designs, thereby hastening the increase of environmentally friendly packaging solutions in development.

Growth dynamics in the market for zero-waste packaging solutions are primarily driven by factors like increasing environmental concerns, government regulation and compulsions, consumer preference for sustainable products, etc. All these compelling reasons force businesses to invest more in eco-friendly packaging alternatives, not only for compliance with regulation but also enhancing brand reputation. Technological development in research and development can ensure better and more technologically advanced packaging solutions, such as biodegradable materials and reusable designs. Further, the tie-ups from packaging manufacturers to businesses operating in different industries promote zero-waste activities.

North America and Europe are considered to have the highest growth market for zero-waste packaging solutions mainly due to high regulatory pressures and greater sensitivities of consumers towards sustainability. Urbanization along with a shift of consumer preferences and the government policies of the region supporting green practices in the Asia Pacific region are the fastest-growing in the zero-waste packaging solutions market. Countries such as China and India are focusing on reducing plastic waste, which has further tremendous demand for zero-waste packaging solutions. Latin America and the Middle East and Africa are other growing markets due to rising environmental consciousness.

COVID 19 has had a mixed effect on the market size of zero-waste packaging solutions. Initially, demand was reduced by disruptions in supply chains and a shift to one-time-only packaging due to hygiene concerns. Interest in sustainable packaging options, however, increased as people and business shifts during the pandemic emphasized the importance of an environment. The influence of the pandemic quickened the shift to digital solutions, while packaging is zero waste and brings further innovation. Overall, the market is anticipated to take care of itself post the COVID-19 pandemic, fueled by a growing spotlight on sustainability.

, Type(Reusable/Recyclable Packaging, Compostable Packaging, Edible Packaging), Distribution Channel(Online, Offline), Application(Food & Beverages, Healthcare, Cosmetics & Personal Care, Electrical & Electronics, E-commerce, Others), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

Key Takeaways:

- Market Growth: The zero-waste packaging solutions market is expected to reach USD 2,985.6 million by 2034, growing at a robust CAGR of 9.15%, indicating strong market expansion.

- Material Segment Dominance: The material segment is dominated by biodegradable plastics, accounting for over 40% of the market share. This preference stems from the increasing demand for sustainable alternatives to traditional plastics in packaging applications.

- Type Segment Insights: Flexible packaging is anticipated to hold the largest market share, favored for its lightweight and space-saving properties. The growing e-commerce sector further propels the demand for flexible, sustainable packaging solutions.

- Driver: This is how the need for zero-waste packaging solutions benefits from improved environmental awareness and support at a regulatory level. Consumers and business establishments have shown interest in reducing plastic waste and thus becoming sustainable.

- Restraint: The cost of producing new materials and technologies is somewhat expensive, which limits the entry to the market for small manufacturers. Consumer awareness and acceptance are some of the challenges that require attention for broader usage.

- Opportunity: The rise of e-commerce and the push for sustainable packaging present significant growth opportunities. Collaborations between brands and sustainable packaging providers can lead to innovative solutions that meet market demands.

- Trend: The increasing focus on circular economy practices is shaping the market, with brands investing in packaging designed for reuse and recyclability, enhancing sustainability efforts.

- Regional Analysis: North America leads the market share due to strong sustainability initiatives, while the Asia-Pacific region is emerging rapidly, driven by increasing industrialization and consumer demand for eco-friendly packaging solutions.

Material Analysis:

Zero-waste packaging solutions market can be categorized by material. These include biodegradable plastics, glass, metal, paper, and plant-based. Biodegradable plastics are highly in demand because they break down naturally; thus, they can be employed for almost all purposes. Paper-based packaging, particularly kraft paper and recycled paper, is in high demand due to recyclability and sustainability. Glass and metals are always favored for their reusability and a high lifecycle. Plant-based materials are now gaining increasing importance, being derived from renewable sources, as consumers push for environmentally friendly alternatives. This segment would also experience robust growth with sustained innovation in the materials.

Type Analysis:

There are three categories for zero-waste packaging: reusable, recyclable, and compostable. Reusable packaging is gaining mainstream popularity as consumers become increasingly ecologically aware, especially of containers and bags, which are the most common examples of such packaging. Recyclable packaging remains a strong tool for brand companies looking to reduce their waste impact-to be sorted and post-consumer recycled. Compostable is organic packaging that can break down naturally in composting environments. These types are in high demand as more and more people nowadays have become aware of sustainability and corporate responsibility forcing companies to go for zero-wasting strategies in the packaging practice.

Distribution Channel Analysis:

Distribution channels in the case of the market segmentation of the zero-waste packaging solutions include online and offline. Online sales is gaining much traction because of e-commerce platforms as well as these consumers are not oblivious towards increasingly present sustainability products. Companies are using digital marketing channels to communicate their eco-friendly packaging solutions to the consumer directly. The off-line channels, including supermarkets and specialty stores, as well as direct sales, are still important to reach a larger number of consumers. A two-pronged approach helps brands to reach different kinds of consumers who have different preferences, thus further access markets and increase sales across all segments.

Application Insights:

Segments in this application include food and beverage, personal care, healthcare, and consumer goods. Zero-waste packaging solutions for the food and beverage segment are useful in limiting food waste and, hence, contributes to sustainability. Personal care brands have begun to embrace eco-friendly packs since they appear to resonate with the concerns of the green-minded consumer and contribute to a higher brand loyalty. Healthcare is also embracing sustainable packaging, especially for their medical products. Consumer goods companies are targeting zero-waste packaging because of growing demand for sustainable products. This segment emphasizes application areas and market growth.

Region Analysis:

North America Leads With 40% Market Share in the Zero-Waste Packaging Solutions Market: North America and Asia-Pacific are the regions with the highest market shares for zero-waste packaging solutions, driven by stringent environmental regulations and increasing consumer demand for sustainable products. North America holds approximately 40% of the market share, supported by a strong focus on eco-friendly practices among businesses and consumers alike. The presence of major players investing in innovative materials, such as biodegradable plastics and recycled paper, further enhances growth in this region. The Asia-Pacific region is projected to witness significant growth, with expectations to reach a 25% market share by 2034, fueled by rapid urbanization and changing consumer preferences.

The European market also holds a substantial share, characterized by advanced sustainability initiatives and a robust regulatory framework promoting eco-friendly packaging. Countries like Germany, France, and the UK are key players, actively investing in zero-waste solutions across various industries, including food and beverages and personal care. Additionally, Latin America and the Middle East and Africa represent emerging markets with substantial growth potential. In Latin America, increasing environmental awareness and regulatory support are driving the adoption of zero-waste packaging, while the Middle East and Africa are gradually recognizing the importance of sustainability, presenting new opportunities for market expansion in the coming years.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Material

- Biodegradable Plastics

- Recycled Paper & Cardboard

- Glass

- Metal (Aluminum, Steel)

- Plant-based Packaging (Cornstarch, Bagasse, Mushroom Packaging)

- Others

By Packaging Type

- Reusable Packaging

- Compostable Packaging

- Recyclable Packaging

- Edible Packaging

- Minimalist & Bulk Packaging

By Application

- Food & Beverages

- Personal Care & Cosmetics

- Healthcare & Pharmaceuticals

- E-commerce & Retail

- Industrial Packaging

- Electrical & Electronics

- Others

By Distribution Channel

- Online Platforms

- Retail & Supermarkets

- Specialty Stores

- B2B Industrial Distribution

By End User

- Consumers

- Retailers

- Manufacturers

- Logistics & E-commerce

By Region

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 1,321.6 M |

| Forecast Revenue (2034) | USD 2,985.6 M |

| CAGR (2025-2034) | 9.15% |

| Historical data | 2018-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Material (Biodegradable Plastics, Recycled Paper & Cardboard, Glass, Metal (Aluminum, Steel), Plant-based Packaging (Cornstarch, Bagasse, Mushroom Packaging), Others), By Packaging Type (Reusable Packaging, Compostable Packaging, Recyclable Packaging, Edible Packaging, Minimalist & Bulk Packaging), By Application (Food & Beverages, Personal Care & Cosmetics, Healthcare & Pharmaceuticals, E-commerce & Retail, Industrial Packaging, Electrical & Electronics, Others), By Distribution Channel (Online Platforms, Retail & Supermarkets, Specialty Stores, B2B Industrial Distribution), By End User (Consumers, Retailers, Manufacturers, Logistics & E-commerce) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Ecovative LLC, DS Smith plc, Avani Eco, Biome Bioplastics Limited, BIOPLA, Loliware Inc., Evoware, Sulapac Oy, TIPA, World Centric, Notpla Limited, Regeno, Hero Packaging |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, Type(Reusable/Recyclable Packaging, Compostable Packaging, Edible Packaging), Distribution Channel(Online, Offline), Application(Food & Beverages, Healthcare, Cosmetics & Personal Care, Electrical & Electronics, E-commerce, Others), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

, Type(Reusable/Recyclable Packaging, Compostable Packaging, Edible Packaging), Distribution Channel(Online, Offline), Application(Food & Beverages, Healthcare, Cosmetics & Personal Care, Electrical & Electronics, E-commerce, Others), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

, Type(Reusable/Recyclable Packaging, Compostable Packaging, Edible Packaging), Distribution Channel(Online, Offline), Application(Food & Beverages, Healthcare, Cosmetics & Personal Care, Electrical & Electronics, E-commerce, Others), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

Select Licence Type

Connect with our sales team

Zero-Waste Packaging Solutions Market

Published Date : 20 Dec 2024 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date